ABSTRACT

Stakeholders’ conscious follow-up on companies’ operation pressured business organizations to be responsible for the society and environment. Companies social and environmental reporting is essential to ease this pressure. Despite its importance, there is no clear consensus on the motivation of companies for their reporting. Therefore, the aim of this study was to examine the motivational factors influencing social and environmental reporting from large tax payers in Ethiopia. An explanatory research design through quantitative research approach was employed by using both primary and secondary data source which was collected from 262 sampled firms in 2018. The regression result revealed that firm age, size, profitability, board size and industry sensitivity had a positive and significant influence on social and environmental reporting, whereas, leverage had a negative and significant impact on social and environmental reporting. This result implied that beyond the voluntary nature of Ethiopian companies’ social and environmental reporting, they have been using their reporting to legitimize their position in the society.

Key words: Agency theory, legitimacy theory, social and environmental reporting, stakeholder theory.

The prevailing world’s environment and impact of mankind on the ecology of the world at large have led to the increased public concern and scrutiny of operations and performances of companies (Agbiogwu et al., 2016). Businesses have bilateral impact on the environment: in one way it contributes to economic and technological advancement and in the other it causes different social and environmental problems such as pollution, resource depletion, etc. Nowadays, companies are under pressure to become accountable and expected to demonstrate that they are aware and addressing the impact of their operations on the environment and society in general (Ding et al., 2014).

The rapid growth in business activities and increasing concern of societies for their environment has brought the need for companies to disclose their environmental and social activities in annual report (Agbiogwu et al., 2016). Theoretically, firms are expected to deal with environmental reporting in order to be successful and acceptable by different stakeholders around the business. Accounting scholars have used legitimacy theory, stakeholder theory and agency theory to articulate company’s relationship with the environment using social and environmental accounting (Reverte, 2009; Deegan, 2002). The theoretical frameworks were intended to explain the existence of social contract between the company and different stakeholders; and breaching these social contracts will threaten the sustainability of the organization. This posits social and environmental accounting as a key to companies’ competitiveness and survival (Deegan, 2002).

However, currently there is no universally accepted theoretical framework for why companies disclose social and environmental information (Suttipun and Stanton, 2012; Nguyen et al., 2017). Scholars argue that companies reporting on social and environmental information should comply with the existing regulation; nevertheless, there is no stringent regulation compatible with general financial reporting. Moreover, an increasing number of companies are disclosing social responsibility activities with in voluntary framework. Existing empirical studies have evolved the nature of social and environmental reporting (SER) and captured meaningful substances in explaining motivational factors of SER (Reverte, 2009; Gray, 2006; Parker, 2005; Deegan, 2002).

One faction to be noted is that, most of the literatures were concentrated on developed nations where stakeholders and different regulatory bodies can exert high pressure on the organization for its impact on the environment and societies, its standard also originated and implemented. Cumming (2006) also suggested a new research area of social and environmental reporting by which studies should stress on creating broader geographical evidence across nations for the purpose of fully depicting its status and underlying determinants.

In Ethiopia, the reporting system is at its infant stage and undergoing thorough tremendous changes. The financial reporting regulatory body has been focused on implementing International Financial Reporting Standard without considering sustainability reporting. On the other hand, the issues of environmental protection, sustainable development and environmental rights have been explicitly covered by the country’s constitution without handing over the monitoring responsibility to a specific authoritative body. Within these perplex issues containing non-mandatory regulation, the motivational factors for social and environmental reporting in Ethiopian companies should be investigated to influence its degree of improvement. Therefore, this study has identified factors that influenced social and environmental reporting among Ethiopian companies; more importantly, it has provided an insightful explanation for the factors by using different theoretical perspectives.

Theoretical review

Previous studies produced diverse body of academic literature which explains the underlying motivational factors of company’s social and environmental reporting; however, a comprehensive theoretical framework is still elusive. The most dominant theories that have been used were legitimacy, stakeholder and agency theories (Nguyen et al., 2017; Suttipun and Stanton, 2012; Ali and Rizwan, 2013; De Burgwal and Vieira, 2014).

Legitimacy theory provides a comprehensive perspective of social and environmental reporting as it explicitly recognizes that companies are bound by social contract. The theory explains this social contract as an arrangement in which the firms agree to perform various socially desired actions in return for approval of their objectives and other rewards which will ultimately guarantee their continued existence and legitimation (Deegan, 2002). According to Nguyen et al. (2017), an entity can exist when its value system is consistent with the value system of the larger social system in which it is located. Additionally, Ali and Rizwan (2013) argue that only legitimate company has the right to utilize society’s natural and human resources. This implies that organizations are required to respond for the changing expectations of the society to maintain their legitimacy (Woodward et al., 2001). The theory suggested that larger companies have to act more in response to reporting in order to have a greater influence on social expectations since they have more stakeholders than small companies (Ohidoa et al., 2016).

The other theoretical perspective is stakeholder theory, which divides the whole society into groups called stakeholders. It is more oriented to managerial tool for managing the informational needs of the various powerful stakeholder groups (shareholders, suppliers, customers, employees, general public, government and others) (Nguyen et al., 2017). This makes it in some way different from legitimacy theory in which, legitimacy theory discusses the expectations of society in general (Ali and Rezwan, 2013). Stakeholder theory states that all stakeholders are concerned with the environmental performance of the company but different stakeholders will have different views on how an organization should conduct its operations. Therefore, reporting is considered as a dialogue between the company and its stakeholders for negotiating this different social contract with each group of stakeholders (De Burgwal and Vieira, 2014).

Finally, agency theory deals with the relationship of firms with various economic agents who act opportunistically within efficient markets. In agency relationships, management is required to provide periodic reporting on the performance of the company to its principal and then, performance of management is assessed by the principal based on the report that has been submitted. Through this assessment, reporting can serve as a means of accountability and transparency of management performance to the principal in determining debt contractual obligations, managerial compensation contracts or implicit political costs (Reverte, 2009). In the corporate annual financial statement, there is additional information on corporate responsibility in environmental aspect. However, company’s environmental reporting and its accountability are based on fulfilling the principal's desire (Wahyuni and Mahmud, 2017). The contract between principal and agent is under the assumptions of short-termism, utter selfishness and utility maximization (Gray et al., 2014). This assumption limits the scope of relevant social and environmental reporting as well as its intended purpose; so far, principals mainly creditors might sit uncomfortably with more investment on the area which they believe will return evasive market advantage. On the other hand, there is a belief that social and environmental reporting helps organizations to attract new investors and obtain financing at a lower cost (Jizi et al., 2014).

Empirical review and hypotheses development

The discussed theories have different perspectives on the same issue and viewed as complementary in explaining social and environmental reporting. Previous studies have also used different theoretical approaches to explain the factors that influence social and environmental reporting of firm’s indifferent part of the world (Hussainey et al., 2011; Nguyen et al., 2017; Esa and Anum Mohd Ghazali, 2012). Therefore, based on the reviewed literatures and the stated theoretical frameworks, the current study has formulated hypotheses to explain the factors that influence social and environmental reporting practice of companies as the following.

Legitimacy theory is concerned with the whole public and consequently companies that are deemed to be more highly exposed to public scrutiny are subject to high pressure on their social and environmental activities from the public, consumer, employees, and government regulatory bodies. Larger companies and older firms are more likely dominant in the society and thus these companies are expected to have larger and diversified stakeholders in their product market and across diversified geographical area (Knox et al., 2006; Aerts et al., 2006). Consequently, they will be highly visible for social activists or regulators and thus they will use social and environmental reporting as a way to enhance their legitimacy through establishing their social responsibility credentials which will reduce the pressure of public scrutiny (Wachira, 2017; Ohidoa et al., 2016).

Moreover, older firms are more likely to be bigger firms and for them the cost and ease of gathering information is less than the small and young companies, their accounting system is relatively effective; so participating and reporting social and environmental practices will be less costly than that of small firms (Nguyen et al., 2017). From an empirical perspective, various studies have found both firm age and size have a positive influence on social and environmental reporting (Welbeck et al., 2017; Kansal et al., 2014; Dyduch and Krasodomska, 2017; De Burgwal and Vieira, 2014; Reverte, 2009). Hence, the first two hypotheses are developed as follows:

H1: There is a positive and significant relationship between firm size and social and environmental reporting.

H2: There is a positive and significant relationship between firm age and social and environmental reporting.

According to stakeholder theory, profitable firms are more motivated to satisfy the information needs of the stakeholders (Ismail and Chandler, 2004). There can be several underlying explanations for this positive relationship. According to Pirsch et al. (2007), profitable firms have the necessary economic means to practice in social and environmental reporting, since companies with less economic resources are expected by their owners to focus on activities that have more direct return for the company. The other explanation was a management that has the knowledge to make a company profitable will also have the knowledge and understanding of social responsibility (Adda et al., 2016). Moreover, managers in more profitable companies disclose social and environmental information in order to support their own position and compensation (Fernandez, 2016).

However, previous empirical studies revealed a mixed result in regard to the relationship between social and environmental reporting with profitability (De Burgwal and Vieira, 2014; Hussainey et al., 2011; Welbeck, 2017; Dyduch and Krasodomska, 2017). Based on reviewed literatures, the study presumed that more profitable firms want to keep their social contract to maintain their place in the eye of their immediate stakeholders (that is, supplier and customers), the public as a whole and then, they will focus more on social and environmental reporting. Accordingly, to test this argument the following hypothesis was formulated:

H3: There is a positive and significant relationship between firm profitability and social and environmental reporting.

Leverage is another factor used in the literature to explain social and environmental reporting. The agency argument stated that, highly leveraged firms are more likely to voluntarily disclose more information (Jensen and Meckling, 1976). In line with this theory, Naser and Hassan (2013) evidenced that a company with higher debt to equity ratio disclose more detailed information than company with low leverage in order to satisfy the need and requirements of lenders. However, according to Wahyuni and Mahmud (2017), the disclosed information is based on the desire of the principal which positioned reports of social and environmental information on the willingness of creditors and shareholders. In line with this, there is also an argument which states that highly levered firms face financial difficulties; thus, it is difficult for them to invest in social and environmental reporting which has no short-term financial return (Chiu and Wang, 2015). On top of these arguments, most research findings inclined to the negative relationship of leverage and social and environmental reporting (Purushothaman et al., 2000; Brammer and Pavelin, 2008; Chiu and Wang, 2015). Therefore, this study has developed the following hypothesis:

H4: There is a negative and significant relationship between firm leverage and social and environmental reporting.

Board size is another attribute which was frequently used as explaining factor of social and environmental reporting studies. Larger board size can help boards to overcome skill insufficiencies in making more flexible disclosure related to future earnings (Dyduch and Karasodomska, 2017). Studies by Siregar and Bachtiar (2010) and Esa and Anum Mohd Ghazali (2012) confirmed that as the number of board member increases, the extent of social and environmental reporting also increases simultaneously. In the current study, the assumption was when the board size is larger, then the members will more likely be versatile than a smaller one because they have expertise from various disciplines that optimally mobilize resources from the social contract. Based on the mentioned reasoning the following hypothesis was developed:

H5: There is a positive and significant relationship between firm board size and social and environmental reporting.

Both legitimacy and stakeholder theory stated that sensitive industries are considered to feel a great pressure from society or certain stakeholders to provide environmental information and thus, they are more likely to disclose this information to avoid a legitimacy gap between society and corporate operations (De Burgwal and Vieira, 2014). Environmentally sensitive industries are referred to industries whose activities affect the environment directly (like: mining, chemical, and manufacturing) (Reverte, 2009). Since, firms in sensitive industries have a direct and visible effect on the environment and will face a great pressure to comply with strict environmental regulations. Otherwise, stakeholders (NGOs, government and the general public) and especially investors may assume that the social contract is breached (Clarkson et al., 2008; Brammer and Pavelin, 2006). Most results of previous studies (Reverte, 2009; Bayoud and Kavanagh, 2012; Naser and Hassan, 2013; Dyduch and Karasodomska, 2017) support the aforementioned argument. Thus, the current study has also developed the following hypothesis:

H6: There is a positive and significant relationship between industry sensitivity and social and environmental reporting.

Study design

This research has adopted explanatory research design with quantitative research approach to identify the causal relationship between environmental reporting and factors that can influence social and environmental reporting of large tax payer companies in Ethiopia. The study has utilized both primary and secondary data. The primary data has been collected through structured questionnaire which included both closed and open-ended questions. The closed ended questions were used to collect categorical data, whereas the open-ended questions have been utilized for enabling the respondents to provide a detail of self-expression that deals with environmental disclosure. On the other hand, audited financial statement of the sampled companies was used as secondary data.

The target populations of this study were large tax payer’s companies in Ethiopia. According to Ethiopian Revenue and Custom Authority (ERCA), there were 1050 large tax payer companies during the study period (2018). Out of the total population, 290 sample size was determined using Yamane (1967) formula. However, as the response rate was 90.3%, only 262 companies were considered as subject for the analysis.

Model specification and variable measurement

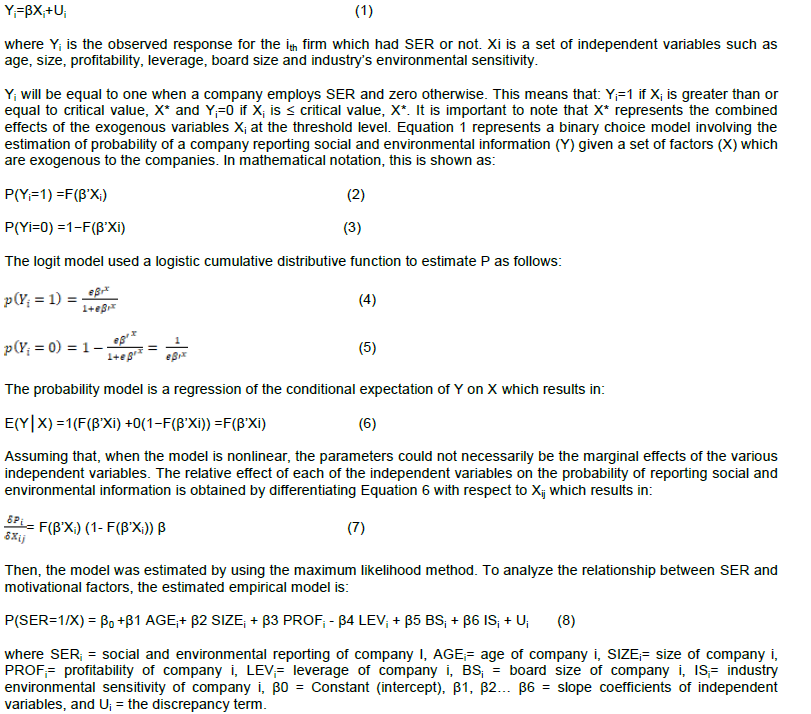

In order to investigate factors that affect social and environmental reporting, the study used binary logistic regression model. The binary logistic regression model was selected due to the nature of the dependent variable (categorical variable) with having only two categories (disclosing companies and non-disclosing). To capture the phenomena in a mathematical form:

According to ERCA companies are classified as large taxpayers when they have annual turnover (revenue) more than 37 million Ethiopian birr.

Descriptive statistics

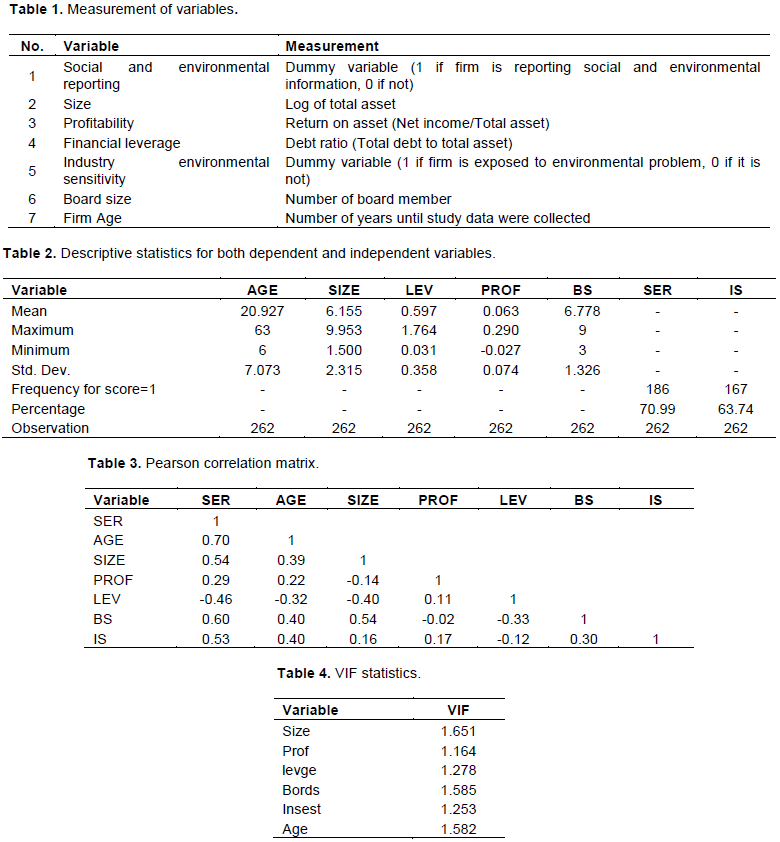

From the sampled companies, 70.99% were reporting their social and environmental practice (Table 1). Moreover, out of the sampled companies, 63.74% were engaged in either in mining or agriculture or manufacturing industry and thus, they were considered as sensitive industry for the environment. The mean value of age, size, leverage, profitability and board size were 20.93, 6.155, 0.597, 0.063 and 6.78, respectively. The minimum and maximum value of age was 6 and 63, respectively. Then, these results had shown a bigger variability among the sampled companies (Table 2).

Correlation analysis among variables

To observe SER association with the motivational factors and ascertain whether the independent variables were not highly correlated with each other, Pearson correlation matrix was employed. As it was illustrated in Table 3, social and environmental reporting had a positive linear relationship with all explanatory variables except leverage, which had a negative relationship. The values of correlation coefficient for independent variables were all below the recommended threshold (0.8) by Gujarati and Porter (2003). Furthermore, the VIF (Table 4) also confirms that there is no evidence of multi-collinearity.

Regression results

The study had employed a logit regression model. Heteroscedasticity problem was expected since the collected data were cross-sectional. To test heteroscedasticity problem, the study used the following hypothesis:

Ho: λ LR=2[Log Lu-LogLr] > critical value at 5 % significance level, Heteroscedasticity

Ha: λ LR=2[Log Lu-LogLr] < critical value at 5 % significance level, no Heteroscedasticity

where log Lu is the value of unrestricted log-likelihood function and Lr is the value of restricted log –likelihood function. λ LR had a distribution with n degrees of freedom where n is the number of independent restrictions. The LR statistics of testing the null hypothesis of homoscedasticity assumption is given by:

LR =2[Log Lu- Log Lr]

where Log Lu is the maximized value of unrestricted log-likelihood function and Log Lr or the maximized value of restricted log-likelihood function estimated only with constant term. In this model, the value of the log-likelihood with only constant term (restricted log-likelihood) was -157.78164 and the maximized log-likelihood value of full model (Unrestricted log like hood) was -20.117624. Therefore, the result of the test for the model is shown as:

LR =2[-20.117624-(-157.78164)] =275.328032

The critical value of Equation 6 is 12.5916 at 5% significance level. Thus, the LR exceeds the critical value, which implies that the model has heteroscedasticity problem. Thus, in order to correct such problem, robust standard errors estimation was employed.

The model was statistically acceptable as 87.25 of the variation explained in the logit model. The Chi-square test showed that the model was significant at 1%, which in turn declared the overall model was a good fit with p-value of 0.0000. The regression result showed age, size, profitability, board size and industry’s sensitivity had a significant positive impact on social and environmental reporting of companies, whereas leverage had a negative effect.

A positive impact of age, size and industry’s sensitivity on Ethiopian companies’ engagement in reporting of their social and environmental information were as expected, which then indicated that when a company gets older or bigger or environmentally sensitive, they were more likely to report their social and environmental practice. Given that these explanatory variables were more related with social visibility; firms wanted to be perceived as a good company for the society and gained a public confidence by disclosing their social and environmental information which in turn maintains their social contract; keeping their dominancy and enabled them to minimize evil eye on the company (Reverte, 2009; Knox et al., 2006; Aerts et al., 2006; Wachira, 2017; Ohidoa et al., 2016; De Burgwal and Vieira, 2014; Naser and Hassan, 2013). According to these results, legitimacy theory was relevant for Ethiopian companies, because they have reported to sustain their legitimacy or to avoid a legitimacy gap between the society and firm’s operation.

The impact of profitability on companies social and environmental reporting was significantly positive, which implied that when Ethiopian companies were more profitable, they would be more ambitious for satisfying the information needed of their stakeholders; especially stakeholders who were in control of the important resources of the firm. This result is in line with stakeholder theory and previous studies (Adda et al., 2016; Pirsch et al., 2007), which confirmed that profitable firms have more economic resource to invest in building their reputability and maintain their position in addition to investing on activities which had direct return like those with a less profitable companies do.

On the other hand, this study revealed that leverage had a negative significant effect on Ethiopian companies’ social and environmental reporting which then implied that unlevered firms reported more environmental-related information than levered firms. This finding also suggested that, when companies in Ethiopia were more levered, their creditors can exert much pressure on them to participate in investment activity which has more direct financial return. Therefore, even if agency theory stated that levered firms have more disclosure than less levered one for minimizing the agency cost, the reporting of levered firms was not inclined to social and environmental information, which was similar to the findings of Wahyuni and Mahmud (2017), Reverte (2009) and Dyduch and Kasodomska (2017).

Finally, board size had a significant positive impact on social and environmental reporting. This result indicated that when board size became larger in Ethiopian companies, they were more likely to have expertise who were capable of observing the bilateral nature of companies’ relationship with its environment from various angle. The result was in line with finding of Siregar and Bachtiar (2010) and Esa and Anum Mohd Ghazali (2012) which reported that, as the number of board member increased, the social and environmental reporting could also have moved in the same direction.

In Ethiopia, there was no regulatory body for social and environmental reporting and thus, around 71% of sampled companies were reporting their social and environmental information during the study period but such figure was obtained due to companies were engaged through voluntary framework. Hence, the study was aimed to investigate the motivational factors influencing reporting of social and environmental information voluntarily among large tax payer companies in Ethiopia. Accordingly, the result of the study would be helpful for different stakeholders to design any policies or regulation to sustain the companies reporting practice and increase quality and quantity of social and environmental information provided for the public.

The result of the study also evidenced that size, age and industry’s sensitivity were positively affected by the social and environmental reporting practices of Ethiopian large tax payer companies. This indicates socially visible companies were more involved in reporting their social and environmental practice. Ethiopian companies voluntarily reported their social and environmental reporting for enhancing their position and image in the society, legitimizing their activity and mitigating the negative impact of their operation to the environment.

Profitability of companies also positively affected their social and environmental reporting. This indicated that profitability can relax companies’ investment decision, even if that investment enhances companies’ evasive advantage. Then, it implied that profitable companies could use their reporting to sustain their profitability and maintain their social contract. Moreover, it is obvious that engaging in social and environmental reporting has its own cost and as a result of this cost, a decision to report social and environmental practices could be hard for any manager without a direct observable return. Therefore, profitable companies have futuristic manager who has knowledge of its social responsibility in addition to making the company profitable.

Moreover, the result of the study has indicated that board size positively affected social and environmental reporting. This is an indication of board member’s expertise is important for organizations involvement in social and environmental reporting. It is also known that board members are among the top supervisor of the organization and when larger member of expertise combined together it can result in a greater social responsibility. The other finding of this study evidenced that leverage impacted negatively the social and environmental reporting. This in turn implied that companies’ indebtedness caused inflexibility to engage in social and environmental reporting as a result of creditors orientation towards companies’ short-term return.

Finally, this study majorly depends on firm characteristics that lead to social and environmental reporting; however, it believed that there are also other external factors which might contribute for their voluntary reporting. Future study on the problem area can go though both firm characteristics and other external factors (such as local and international level regulation, accounting standard, and others). Furthermore, the absence of common accepted standard for social and environmental reporting makes it difficult to go through the content of companies reporting. Therefore, dummy variable was used to measure the social and environmental reporting of Ethiopian companies. With this respect, further study is recommended to use content analysis in order to draw better conclusion.

The authors would like to acknowledge Wolkite University for financial and material support for this study.

The authors have not declared any conflict of interests.

REFERENCES

|

Adda G, Azigwe JB, Awuni AR (2016). Business Ethics and Corporate Social Responsibility for Business Success and Growth. European Journal of Business and Innovation Research 4(6):26-42.

|

|

|

|

Aerts WW, Cormier D, Magnan M (2006). Intra-Industry Imitation in Corporate Environmental Reporting: An International Perspective. Journal of Accounting and Public Policy 25(3):299-331.

Crossref

|

|

|

|

|

Agbiogwu AA, Ihendinihu JU, Okafor MC (2016). Impact of environmental and social costs on performance of Nigerian manufacturing companies. International Journal of Economics and Finance 8(9):173-180.

Crossref

|

|

|

|

|

Ali W, Rizwan M (2013). Factors Influencing Corporate Social and Environmental Disclosure (CSED) Practices in The Developing Countries: An Institutional Theoretical Perspective. International Journal of Asian Social Science 3(3):590-609.

|

|

|

|

|

Bayoud NS, Kavanagh M (2012). Factors Influencing Levels of Corporate Social Responsibility Disclosure by Libyan Firms: A Mixed Study. International Journal of Economics and Finance 4(4):13-29.

Crossref

|

|

|

|

|

Brammer S, Pavelin S (2006). Corporate reputation and social performance: the importance of fit. Journal of Management Studies 43(3):435-455.

Crossref

|

|

|

|

|

Brammer S, Pavelin S (2008). Factors influencing the quality of corporate environmental disclosure. Business Strategy and the Environment 17(2):120-136.

Crossref

|

|

|

|

|

Burgwal DVD, Vieira RJO (2014). Environmental disclosure determinants in Dutch listed companies. Accounting and Finance Journal 25(64):60-78.

|

|

|

|

|

Chiu TK, Wang YH (2015). Determinants of social disclosure quality in Taiwan: An application of stakeholder theory. Journal of Business Ethics 129(2):379-398.

Crossref

|

|

|

|

|

Clarkson P, Li Y, Gordon R, Vasvari FP (2008) Revisiting the Relation Between Environmental Performance and Environmental Disclosure: An Empirical Analysis. Accounting Organizations and Society 33(4-5):303-327.

Crossref

|

|

|

|

|

Cumming D (2006). Adverse selection and capital structure: Evidence from venture capital. Entrepreneurship Theory and Practice 30(2):155-183.

Crossref

|

|

|

|

|

Deegan C (2002). Introduction: The legitimising effect of social and environmental disclosures-a theoretical foundation. Accounting, Auditing and Accountability Journal 15(3):282-311.

Crossref

|

|

|

|

|

Ding Y, Phang CW, Lu X, Tan CH, Sutanto J (2014). The role of marketer-and user-generated content in sustaining the growth of a social media brand community. In 2014 47th Hawaii International Conference on System Sciences pp. 1785-1792.

Crossref

|

|

|

|

|

Dyduch J, Krasodomska J (2017). Determinants of Corporate Social Responsibility Disclosure: An Empirical Study of Polish Listed Companies. Sustainability 9(11):1-24.

Crossref

|

|

|

|

|

Esa E, Anum Mohd Ghazali N (2012). Corporate social responsibility and corporate governance in Malaysian government-linked companies. Corporate Governance: The International Journal of Business in Society 12(3):292-305.

Crossref

|

|

|

|

|

Fernandez RM (2016). Social responsibility and financial performance: The role of good corporate governance. BRQ Business Research Quarterly (19):137-151.

Crossref

|

|

|

|

|

Gray R (2006). Social, environmental and sustainability reporting and organizational value creation? Whose value? Whose creation? Accounting, Auditing and Accountability Journal 19(6):793-819.

Crossref

|

|

|

|

|

Gray R, Adams CA, Owen D (2014). Accountability, social responsibility and sustainability. Pearson Education Limited.

|

|

|

|

|

Gujarati DN, Porter DC (2003). Basic econometrics (ed.). New York: McGraw-HiII.

|

|

|

|

|

Hussainey K, Elsayed M, Razik MA (2011). Factors Affecting Corporate Social Responsibility Disclosure in Egypt. Corporate Ownership and Control 8(4):432-443.

Crossref

|

|

|

|

|

Ismail KN, Chandler R (2004). The timeliness of quarterly financial reports of companies in Malaysia. Asian Review of Accounting 12(1):1-18.

Crossref

|

|

|

|

|

Jensen M, Meckling W (1976). Theory of the firm: Managerial behavior agency cost and ownership structure. Journal of Financial Economics 3(4):305-360.

Crossref

|

|

|

|

|

Jizi M, Salama A, Dixon R, Stratling R (2014). Corporate Governance and Corporate Social Responsibility Disclosure: Evidence from the US Banking Sector. Journal of Business Ethics 125(4):601-615.

Crossref

|

|

|

|

|

Kansal M, Joshi M, Batra GS (2014). Determinants of corporate social responsibility disclosures: Evidence from India. Advances in Accounting 30(1):217-229.

Crossref

|

|

|

|

|

Knox S, Maklan S, French P (2006). Corporate Social Responsibility: Exploring Stakeholder Relationships and Programme Reporting Across Leading FTSE Companies'. Journal of Business Ethics 61(1):7-28.

Crossref

|

|

|

|

|

Naser K, Hassan Y (2013). Determinants of Corporate Social Responsibility Reporting: Evidence from an Emerging Economy. Journal of Contemporary Issues in Business Research 2(3):56-74.

|

|

|

|

|

Nguyen LS, Tran MD, Nguyen TXH, Le QH (2017). Factors Affecting Disclosure Levels of Environmental Accounting Information: The Case of Vietnam. Problems and Perspectives in Management 6(4):255-264.

Crossref

|

|

|

|

|

Ohidoa T, Omokhudu OO, Oserogho I (2016). Determinants of environmental disclosure. International Journal of Advanced Academic Research| Social and Management Sciences 2(8):49-58. Available at:

View

|

|

|

|

|

Parker L (2005). Social and environmental accountability research. Accounting, Auditing and Accountability Journal 18(6):842-860.

Crossref

|

|

|

|

|

Pirsch J, Gupta S, Landreth-Grau S (2007). A Framework for Understanding Corporate Social Responsibility Programs as a Continuum: An Exploratory Study. Journal of Business Ethics 70(2):125-140.

Crossref

|

|

|

|

|

Purushothaman M, Tower G, Hancock P, Taplin R (2000). Determinants of corporate social reporting practices of listed Singapore companies. Pacific Accounting Review 12(2):101-133.

|

|

|

|

|

Reverte C (2009). Determinants of Corporate Social Responsibility Disclosure Ratings by Spanish Listed Firms. Journal of Business Ethics 88(2):351-366.

Crossref

|

|

|

|

|

Siregar SV, Bachtiar Y (2010). Corporate social reporting: empirical evidence from Indonesia Stock Exchange. International Journal of Islamic and Middle Eastern Finance and Management 3(3):241-252.

Crossref

|

|

|

|

|

Suttipun M, Stanton P (2012). A study of Environmental disclosure by Thai listed companies on websites. Elsevier procedia economies and finance 2(2012):9-15.

Crossref

|

|

|

|

|

Wachira M (2017). Determinants of Corporate Social Disclosures in Kenya: A Longitudinal Study of Firms Listed on the Nairobi Securities Exchange. European Scientific Journal, 13(11):6-18.

Crossref

|

|

|

|

|

Wahyuni SH, Mahmud A (2017). Determinant of Environmental Disclosure on Companies Listed in Indonesia Stock Exchange (IDX). Accounting Analysis Journal 6(3):380-393.

|

|

|

|

|

Welbeck E (2017). The influence of institutional environment on corporate responsibility disclosures in Ghana. Mediterranean Accountancy Research 25(2):216-240.

Crossref

|

|

|

|

|

Welbeck E, Owusu G, Bekoe RA, Kusi JA (2017). Determinants of environmental disclosures of listed firms in Ghana. International Journal of Corporate Social Responsibility 2(11):1-12.

Crossref

|

|

|

|

|

Woodward D, Edwards P, Birkin F (2001). Some evidence on executives' views of corporate social responsibility. British Accounting Review 33(3):357-97.

Crossref

|

|

|

|

|

Yamane T (1967). Statistics: An Introductory Analysis, 2nd Edition, New York: Harper and Row.

|

|