Full Length Research Paper

ABSTRACT

This work aims at contributing to understanding the perception of CSR[i] by CEOs[ii]of Cameroonian SMEs[iii]and its possible practical translation on the field. To reach this target, we first highlighted theoretical explanation which aimed at defining stakeholders and the dependency towards resources theories. Then, on the empirical aspect, we attempted to carry out a field study. The explorative character of our research led to select a qualitative methodology based on case studies. Semi- directional interviews, nine month-follow-up and site visits were carried out in the presence of SMEs managers. These enabled us look into the different perceptions of managers and associated practices. From that, it could be observed that the concept of CSR is divergently perceived by SMEs, in accordance to the conviction of managers, their level of instruction and the activity sector. As SMEs are rarely involved in the three CSR pillars, they often put in place casual approaches concerning certain CSR aspects. However, SMEs wishing to position themselves favorably in their environment must associate the three logics. This category of enterprise must be backed up by public entities, business associations and certain of the civil society.

Key words: Corporate social responsibility (CSR), small and medium scale enterprises (SMEs), chief executive officer (CEO), Cameroon, case study.

[i] Corporate Social Responsibility

[ii]Chief Executive Officers

[iii]Small and Medium Scale Enterprises

INTRODUCTION

Some researchers have been trying for more than half a century to analyze and understand the notion of Corporate Social Responsibility (CSR) (Bowen, 1953; Carroll, 1979; Freeman, 1984). Different definitions of this notion have been given: Bowen, 1953; Davis, 1973; Carroll, 1979; Jones, 1980; Wood, 1990; Vert, 2001. These definitions have in common the idea that CSR refers to the obligation of a firm towards society or more specifically towards stakeholders of the firm, that is, those who are affected by the policy and practices of this enterprise.

According to Jenkins (2009), CSR concerns the activities that contribute to sustainable development, that is to say, the integration of economic, social and environmental management models to ensure business sustainability aspects.

The idea behind the concept of CSR is “moralise capitalism in order to build a better world” (Weber, 2002). To date, there are very limited numbers of studies dealing with CSR in small businesses in Africa, probably because they are perceived as lacking sufficient time, resources and knowledge to implement social actions. But according to Jenkins (2009), small and medium enterprises (SMEs) can take advantage of the opportunities presented by CSR and maximise the business benefits from making the most of such opportunities.

Although there is a consensus that the CSR is concerned about social obligations of firms, little certainty on the nature and the level of these obligations is noticed (Smith, 2003). Anyway, in the context of organizations management, the CSR must attempt to reconcile the economic, social and environmental dimensions.

Today, the CSR is the turning point of the enterprise strategy (Capron and Quairel Lanoizelée 2007). Moreover, research has mainly being focused on the behaviour of large enterprises, ignoring therefore, the SMEs population, (Jenkings, 2004). If the social impact of large enterprises constitutes today’s evidence, that of SMEs should not be minimized. On the numeric plan, the latter are in fact the dominant shaping of organizations on the world socio economic scenery. In the context of Cameroonian economy, this category of enterprises represents almost 99% of economy and about two thirds of employment in private sector (NSI, 2009). With this representation and the current context of economies globalization, the interplay of social responsibility for SMEs becomes essential. Thus, it can be understood that SMEs represent a significant part of the population of economic actors.

For instance, looking at the environmental dimension of CSR in Cameroon it could be clearly understood that the practice of CSR is critical in that the important environmental aspects are often neglected by industrial enterprises (Spence et al, 2007). According to the census survey enterprise (CSE) report (NIS/CSE, 2009), the industrial enterprises represent 13.1% of Cameroonian enterprises with 64% of them operating in the manufacturing sector. This sector employs about 87,889 people either 07 people per enterprise. In 2009, these enterprises have achieved a turnover of approximately 3.5 billion CFA francs representing 34.3% of the gross domestic product. This means the undeniable importance played by the industrial sector at the national level, including its social and economic benefits. Despite the positive impacts of the industrial sector in economic and social development, we should consider its contribution to environmental degradation. This necessitates greater environmental conservation. Indeed affluent discharges by different industries contribute in an undeniable way to the ruin of the environment. It therefore seems necessary to evaluate the practice of CSR among industrial enterprises established in Cameroon. Such an evaluation would guarantee the protection of the environment, as well as sustained growth of SMEs and therefore, development.

Despite their importance, in terms of global impacts and even though there is a little concern as subject of research on the CSR, growing interests for the study of

While in terms of research on the CSR, SMEs are relegated to the second class. Many reasons could be raised up among which the main is undoubtedly based on the insignificant individual impact of SMEs. In fact, when SMEs are considered individually, they have a less important impact than that of large enterprises whose consequences of a single decision could be devastating, mainly in under developed countries. SMEs have rather been until now encouraged to be spectators of social activism and to concentrate on the need to avoid a socially irresponsible behaviour (Thompson and Smith, 1991). Nevertheless, we think that the CSR is today a reality which imposes itself to all types of enterprises regardless of the sizes.

The present study has to do with the role played by SMEs with regards to the CSR of enterprises. Concerning the specific case of the Cameroonian CSR, what is the managers’ perception? What are the practices? What are the inherent implications of these practices?

These questions are important in the context of Cameroonian economy with the recurrent fines and penalties recently slammed on some SMEs by the authorities in charge of the protection of environment, especially the observation of managerial practices visàvis poor human resources.

This research aims at attaining the following specific objectives:

1. A better understanding of the CSR perception by Cameroonian CEOs of SMEs.

2. An identification of different stakeholders taken into consideration and their relations characteristics.

3. Recommendations of the results obtained.

4. Our theoretical framework will essentially focus on the theory of stakeholders (Freeman, 1984) as well as the theory of dependence towards resources (Pfefer and Salancik, 1978) that for the time being constitute the dominant theories to explain the CSR in the management science research

5. On the methodological plan, our choice will be the exploratory qualitative approach giving mutations between the survey results and the theory development. Our intention is not to provide a statistical analysis but to portray the beliefs of Cameroonian SMEs managers with regard to the CSR.

The development of our research shall be based on the following points:

1.Theoretical approach of social responsibility of an enterprise;

2.Methodological choice;

3.Presentation and discussions of findings;

LITERATURE AND THEORETICAL FRAMEWORK

The theoretical fundamentals of the CSR oscillate between two opposite poles. On the one hand, neo-classic theories which are based on the postulate of markets efficiency decline every idea of social respon-sibility of the enterprise other than that of making profit for its shareholders (Friedman, 1970) and consider other ends as being “subversive”. On the other hand, theories that mobilize a teleological principle and affirm that there exists a moral responsibility of decision makers towards future generations and of a large number of societal problems. We are hereby focusing on theories that affirm a more or less important convergence between the interest the enterprise and that of society, more specifi-cally, the society theory more specially stakeholders’ theory (Freeman 1984) and the theory of dependence towards resources (Pfefer and Salacok, 1978).

“CSR and the stakeholders’ theory”

The notion of stakeholder from the Anglo-Saxon jargon has been developed since the publication of Freeman (1984). This theory questions the supremacy of enterprises. It puts the enterprise at the heart of some relations with its partners who are no longer only shareholders but actors interested in the activities and decisions of the enterprise. The term stakeholders (parties involved) emerged in the strategic approaches and the analysis of the organization relations with its environment.

While the environment of the enterprise was globally apprehended, the stakeholders’ theory permitted the operationalization of strategic answers by enlisting the different categories of actors that constituted it. Strategic management must therefore identify and take into consideration the interests and constraints of these actors. So for a better delimitation of the concept and to dress up the stakeholders’ inventory, some actors have listed some typologies:

1. Primary or secondary stakeholders (Carroll, 1979 quoted by Capron and Quairel-Lanoizelee, 2007): Primary stakeholders are directly involved in the economic process and have an explicit contract with the firm. There are shareholders, employees, customers and suppliers.

Secondary stakeholders have voluntary relations with the firm in the form of implicit or moral contract. There are local associations, territorial administrations, NGOs, etc.

2. Voluntary and non-voluntary stakeholders (Clarkson, 1995, quoted in Capron, ibid): voluntary stakeholders agree (contractually in general) to be exposed to certain risks while involuntary stakeholders bear the risk without having any contractual relation with the firm; urgent, powerful, legitimate stakeholders (Mitchell, 1997 quoted in Capron, ibid): identify these factors as explaining the attention drawn on households to some types of stakeholders in the context of resources in limited time.

The power is held by these groups of actors which have the capacity to influence present or future decisions of the firm. The legitimacy of a group corresponds to its social recognition and acceptance. According to their attributes, stakeholders are unavoidable, dominant, dangerous, dependent and dormant. So, one of the stakeholders’ visions, “oriented business”, with the CSR as a tool presents the taking into consideration of stakeholders’ interests as a condition of the economic and financial performance of the enterprise (Capron, ibid). Therefore, the interest of the enterprise and its actors passes through the implementation of the adopted answers to the expectations of stakeholders. This instrumental approach falls on the perspective of the dependence theory towards resources.

CSR and dependence towards resources theory

The dependence theory towards resources (Pfefer and Salancik,1978) makes the enterprise depend on its environment and affirms that its perennial depends on its aptitude to manage demands of different groups, in particular those whose resources and support are determinant for its survival (Pfefer and Salancik, ibid).

To acquire the resources that it needs, an organization must hence interact with its environment: because it fetches resources in its environment, it depends on it (Pfefer and Salancik, 1978, op cit), the perennial of the organization depends on its capacity to manage the demands of its environment in particular those formulated by the groups which hold indispensable resources to its survival.

These actors mention the “external control” of the environment. The legitimacy will therefore ensure to the organization the approval of society and give the possibility of obtaining resources that it needs for its survival. “The social acceptability that is, as a result of the legitimacy might be more important than the economic performance” (Pfefer, 1994).

Thus, the organizational legitimacy becomes a strategic resource on which the organization survival depends. Organizations interact with their environment and must manage the demand of different stakeholders; but it is these stakeholders who will judge the organizational efficiency. Consequently, the organizational legitimacy depends partly on responses brought to environment expectations. In this framework the organization retains the possibility of influencing the acceptability of its activities. The organizational legitimacy would there be a socio-political question.

The holders of the strategic approach advocate that the organizational legitimacy lies on the notion of social contract, enlightened by Shocker and Sethi (1974). In fact, for these actors, the enterprise as any other social institution acts in society through an explicit or implicit social contract whose survival and development depend on the production of goods and services desired by society and the distribution of economic, social or political benefits to groups that bestow power on it.

Hence, to ensure their survival, organizations must comply with the values of society and respond to its expectations. This idea of the balance between social values and organizational actions was recalled by Dowling and Pfefer (1975) whose works constitute the veritable base of the legitimacy strategic approach. They indicate that the organizational legitimacy is obtained from the moment that this balance is studied. Exchanges between the organization and society cannot only be realized under this condition. Dowling and Pfefer (ibid) apprehended organizational legitimacy as the balance between social values and organizational actions. The legitimacy is determined by the mode of production, products, the goals and the sector of activity.

But if the legitimacy is a constraint that lies on organizations, it remains above all a dynamic constraint which is defined with the evolution of organizations. The legitimacy follows therefore a social judgment that stakeholders make on the organization process. The strategic approach of the legitimacy process was developed by Dowling and Pfefer (ibid), Ashforth and Gibbs (1990) and Lindblom (1994). It highlights the more or less formal mechanisms which organizations have in order to adjust to their environment.

After dealing with the theoretical process, it is high time we focused on the methodological framework of our study.

METHODOLOGY: AN EXPLORATIVE AND EMPIRICAL STUDY

This work is based on an explorative logic. Our proposals are illustrated by ten situations of SMEs managers. According to Evrard et al. (1997) there are four characteristics of an explorative study:

1. The narrow size of the sample (taking into account the weight and cost of data collection)

2. The interaction between the observed and observers

3. The observation as an instrument of case study analysis

4. The role of interpretation is fundamental during the collection of qualitative data.

Our research methodology is therefore qualitative in nature (Hlady-Rispal, 2002) due to the emerging character of the problem as stake. Qualitative research is in essence a work of arts and crafts (Wacheux, 1996). The setting up of qualitative research process consists in trying to understand the why and how of events in concrete situations.

Concerning an emergent theme, we have naturally privileged a qualitative method centered on case studies (Yin, 1994; Hlady-Rispal, 2002). According to Stake (2000: 11) “case study has become one of the most common ways to do qualitative inquiry”. The variable according to Yin (1990) is here the CEO of the SME. The limited number of managers in our sample does not allow the generalization of results.

The data collection was achieved through semi directional individual interviews (between 1 and 1 h 30 min time duration) conducted face to face with the CEO of SMEs during the second semester of 2013 were totally reproduced with the assistance of an interview guide made of many open questions referring to the SME. So, why getting interested in the CEO of SME?

The sample is made up of 10 SMEs managers from several sectors of activities. SMEs chosen were all created between 2001 and 2010; they are located in Douala, the economic capital of Cameroon. Questions were set in order to explore SME managers’ beliefs without suggesting any answer tips. We are hereby attempting to bring out factors which influence and are influenced by the CSR. The interview guide was structured into many sub-points in line with the objectives pursued by the study.

1. Creator’s profile (training, age, background).

2. The representations of SME managers interviewed on the CSR topic.

3. The identification and relations characteristics with employees, government, customers, suppliers, competitors, bankers, micro-finance establishments etc.

4. The internal social angle of the CSR based on the training of human resources, social dialogue, internal communication, working conditions, health, security at work and remuneration policy.

5. The internal social angle such as the protection of the image of the enterprise and its stakeholders.

6. The angle of sustainable development such as the eco-conception of products, utilization of biodegradable packaging materials, policy of wastes management …).

After dealing with the research methodology, it is high time we focused on the results of our study.

DISCUSSIONS OF FINDINGS

Having presented the methodological and theoretical framework of our research we are going to focus on the commentary of findings obtained as a result of the exploratory survey. We first of all present the descriptive analysis of this study.

Descriptive analysis

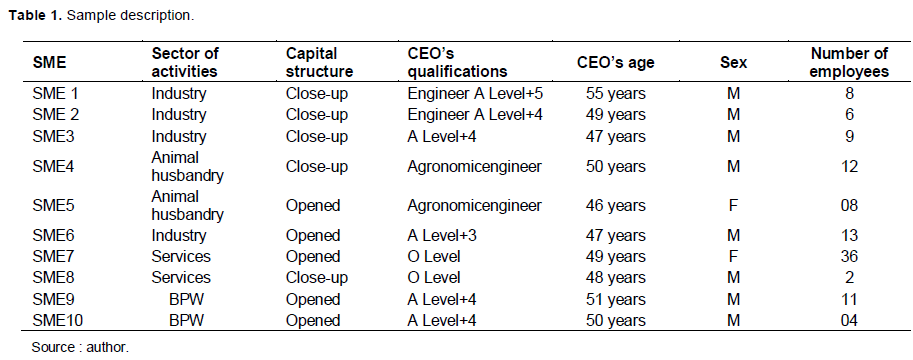

As can be observed from Table 1, among the SME CEOs of our sample, we have two women and eight men aged

between 47 and 55, which corresponds to an average age level of about 49 for the whole sample. The level of training of CEOs is relatively good (six out of ten have A Level + 5). However, they all have a significant past professional experience (of many years), with the exception of one CEO who created his enterprise after many internship exercises. Concerning the sector of activity, they are voluntarily heterogeneous in this study of exploratory character where no sectorial analysis is targeted. Among ten enterprises, four have a industrial activity (E1, E2, E3 and E4), two practice a pastoral polluting activity (E5 and E6), two in the services activity (E7 and E8) lastly, two in the building and public works (E9 and E10). The size of the sample SMEs varies from 2 to 36 permanent employees.

This analysis will follow five steps, which would be as much up to the level of analysis.

Perception of the CRS by the SME

How do SME managers of our sample define or perceive the CSR? The empirical survey carried out in this work highlights the diversity of SMEs. Between a SME of 02 employees and another one of 36 employees or a qualified manager (A Level +5) and another less qualified, the perceptions of the social responsibility are obligations of the enterprise towards public administration (fiscal administration , work administration, the ministry of nature protection, the ministry of commerce, the ministry in charge of SMEs etc).

These obligations could be streamlined to the payment of taxes, the protection of the environment, in short, to everything related to the regulation. Two CEOs assimilate the CSR to the granting of dominations to humanitarian organizations, the enrolment of trainees and the payment of taxes. Four managers have never heard anything about CSR and consequently ignore the contents the CSR should have. Among four other who have a perception, their economic entities belong to the industrial sector, however, all of them have an educational level of A Level+5 and they have at least once participated in a seminar reflecting the CSR. The perception of CEO is influenced by a certain number of indicators such as education, sensitization during seminars to subscription, enterprise social engagement, the belonging to a sector of activity, the obligation to respect the regulations, without losing personal convictions. These results corroborate certain theoretical predictions according to which SME managers define and develop their representations of the CSR with concepts in line with their personal convictions linked to beliefs, education and other socio economic factors including experiences related to SMEs activities. These factors are found in studies based on factors of ethical influence conducted by Brown and King (1982), Hambrick and Manson (1984).

Regarding the person in charge of the major orientations of the enterprise, all managers indicate that this responsibility lies on them. This is also valid for SMEs that are interested in questions related to CSR.

Identification of stakeholders

Questions about social involvement towards stakeholders of the enterprise are not new and practices are common without bearing somewhat the CRR label. During our interview we tried to make it clear to CEOs, the importance and stakeholders’ status identified in respect of the typology of Mitchell et al. (1997).

Employees

Environment in the context of protection of nature the State suppliers banks NGOs competition.

At the end of our interviews, the most determinant stakeholders for SMEs managers in our sample are customers (9/10), suppliers (7/10), family (7/10), micro finance institutions (7/10), employees (2/10), and the State (1/10). As can be noticed, customers and suppliers, other present a typology of stakeholders based on the presence of three attributes in their relationship with the enterprise. These attributes are:

1. Power: power to influence of stakeholders on the organizational decision

2. Legitimacy: the legitimacy of stakeholders’ relationship with the firm

3. Urgency: stakeholders’ urgency of complaints towards the firm.

This typology is utilized when a classification is to be made and analyze the influence of different stakeholders for each CEO. The family and micro-finance institutions are close to the enterprise and could be of this fact considered as partners.

Customers

The results obtained from our study show that SMEs have sustained relations with customers. These exchanges vary either according to scrupulous or less respect by the enterprise of consumer’s rights and offer them advantageous selling conditions (remission, bonus, discount, credit)

The family

The family plays a non-negligible role in the day-to-day behaviour of the SME CEO. He cannot escape from family obligations and responsibilities. Thus, concerning our interviews, family members influence the mode of functioning of an enterprise. This influence is observed during the level of recruitment of staff where family members are often given privilege without having required competences. However, this category of employees enjoys special treatment (salaries, unjustifiable absences, no submission to the procedures of management of the enterprise…). This is also applicable to health, school fees, assistance to home village, expenses as emphasized by Kammogne (1993:38), the enterprise is considered in Africa “as a source of unfinishable revenues put at the disposal of the community by the provider with distribution means to the whole community. The promoter’s family regularly imposes to him charges capable of getting the enterprise bankrupt. This proximity to the family, according to certain SME managers, results from the fact that “the entrepreneur lives in his family which he must honour according to norms and values”.

Employees

The staff has not been quoted among major stakeholders; this shows the little interest that SMEs managers in the sample give to employees. The studies of Courrent and Gundolf (2008) proposing to study the role of social capital on the ethical dimension of management of very small enterprises (VSE) (less than ten employees) culminates to a similar account, that is the priority position reserved to customers as major stakeholders neglecting somehow the employees’ situation. In a context characterized by a high rate of structural unemployment, the labour market is extremely imperfect to the extent that managers dictate their rules to the detriment of elementary rules in terms of management of human resources. 8 SMEs, out of 10 regularly recruit trainees not as in the frame-work of social responsible enterprise, but in view of reinforcing manpower, whereas the role of employees must be considered as essential to the pursuit of enterprise activities. In fact, employees constitute a group of stakeholders that the enterprise cannot afford to neglect. They have precise needs and claim that the enterprise must respond very fast. These needs and claims represent some stakes that the SME must manage. In this case, the relationship that an enterprise keeps with its employees is capable of influencing its social and economic performance.

The state

The State of Cameroon has power and legitimacy. According to SME managers in the sample, the State is not considered as a partner but as a repressive institution with which relations are frequently conflicting. In a general manner, we have noticed that the relation between the enterprise and the government and / or the State is less treated by literature materials. But it is established that the government and public authorities generally intervene in the management of many social stakes influencing social practices of firms; and this through the enforcement of a new work regulation, a law on the protection of environment, and the protection of consumers, etc. Hence, the enterprise is more and more obliged to consider legal responsibility in the management of its social stakes.

Although State/enterprise relation has shown a certain interest for a good number of practitioners and academics, it remains ambiguous. A certain number of academic works (Clakson, 1991), Enderle and Travis 1958) argue that the participation of the enterprise in the process of elaboration and implementation of public policies and to political life in general is by nature meant to favour a good social performance of the enterprise.

Bankers

To SMEs, bankers do not constitute an interesting segment in the conduct of their activities. In fact, SMEs believe that bankers are very sensitive towards “SME-risk” and systematically reject application files for financing submitted for their appreciation by this category of enterprise.

Suppliers

The results of our interviews show that suppliers constitute an important stakeholder according to SMEs managers. This importance is only appreciated from an economic viewpoint. The importance of maintaining close link with supplies is also emphasized by certain actors (Lefebvre and Singh 1992; Beland and Piche, 1998) without going into details about the nature of this engagement. Clarkson (ibid) attempted to render the relationship more concrete. In fact, he affirmed that a firm in the course of choosing its supplies must consider current social deals, which would certainly apply a positive influence on its socio economic performance.

Micro-finance Institutions (MFI)

Micro finance institutions are very close to SME managers. In fact, due to the reluctance of classic bank to give support to SMEs, the latter turn to MFI which are very receptive towards their appeals. Credit packages designed according to the size and needs are made available to the disposals of SMEs. However, it is surprising that the processing period is very short to bring a solution to the questions of SME financing. According to our respondents, the MFI have become an unavoidable instrument of development of their activities. Like the relations with suppliers, it is the economic aspect that overrides in the exchange with MFI. The concept of “green loan” and everything that refers to the social does not exist.

Internal social aspect of the CSR based on human resource management

If the CSR requires a strong implication of human resources offices and managers in large enterprises, the issue is more complex when it is the case of SMEs and SEs and VSEs in particular. Our interviews on the social internal aspect of the CSR were based on the following points:

1. Quality of life to work : health and conditions of employees’ work

2. Social manager and human management

3. Which objectives of human resources management?

4. How to achieve the mutation, diversified, the employment and the evolution of career?

5. Promote responsible behaviors towards employees: fight against addictions.

From our interviews:

Three (3) respondents revealed to have offered output bonus to the staff on the basis of a personal appreciation of the CEO. No SME in the sample practises human resources planning or a policy of employee promotion.

The security and amelioration of working conditions are not paid attention to by SME managers in our sample. 05 leaders agreed to have given presents to bereaved collaborators and even to have taken active physical part in the burial ceremonies. This equally concerns ceremonies arranged by a staff member to celebrate a happy event (marriage, birth, etc).

In theory, the financial inclination of employees, including the economic dialogue are tools which are situated at the economy and social affairs meeting point contribute to the implication of staff in the functioning of the enterprise. This practice often regarded as a means of associating employees to the progress of the enterprise, is unfortunately less present in the interviewed enterprises. The data from the respondents’ statements shows that for the SMEs which are at a staggering stage of social engagement (assistance to the bereaved for example), the CSR approach represents a new manner of thinking or of ameliorating the social relations inside an enterprise. This makes us ask questions like that of Messenghen and Chabaux (2010) if one can talk of HRM in SMEs? More specifically in Cameroonian SMEs?

External social aspect based on sponsoring and support to associations

The question that SMEs managers were asked was that of trying to know social practices put in place in the enterprise. In this regard, we are assured of the actions of the enterprise in favor of associated engagement (financing of sport or cultural associations for example). None of the SMEs in the sample is really involved in the promotion or the sponsoring of sport or cultural associations. The reason raised by all managers is the lack of financial means. Nevertheless, 4 SMEs sometimes sponsor sport and cultural actions which are organized internally during ceremonies marking the celebration of national and labor days in Cameroon.

External social aspect based on environment respect

Concerning practices in line with the preservation of environment, 3 SMEs of the sample among which 6 having a polluting activity were engaged in a formal structure of protection taking into consideration the protection of the biosphere. This structure concerns the evacuation of wastes and the pollution of the air. However, since March 2014 the legal obligation of enterprises, has asked them to no longer use biodegradable packaging materials. Some instead of using these packaging materials to serve customers decide to apply unhygienic practices by selling goods, for example bread without wrapping it. The concerned enterprises say that in the near future they will adhere to this measure. Public authorities did not sufficiently prepare them in the application of this measure.

CONCLUSION

This work aimed at attempting to measure CEOs’ perception of the CSR in Cameroonian SMEs, to identify stakeholders and the practices of CSR in SMEs so that some projections be made. Therefore the following results were obtained: SMEs in the sample do not generally make the CSR a major concern in their policy and management actions. Those who take the CSR into consideration are urged by personal conviction and legal obligations.

These convictions and SME implications for the CSR are linked. The mode of functioning of SMEs is strongly marked by CEOs’ determinant role and by proximity, be it with the enterprise or in the relationships with stakeholders. In this context, the integration of CSR in the SME depends on the representations that the manager has in mind. The CSR in the context of Cameroonian SME, the precipitating event is at large, the case of a stakeholder such as the customer (demand/need) or the competition (mimetic) and above all the State. Within this framework, urgency is generally at the center of the decision process concerning the CSR.

A hierarchical classification of stakeholders by SMEs was made. Customers, suppliers, the family, micro finance, institutions are considered by SMEs as close and important partners. The State and the classic bank entertain a quasi conflicting relationship with SMEs. Employees are relegated to the second class. Anyway, privileged relationships with certain stakeholders are base on economic motivation and not social motivations.

Generally, it clearly appears that SMEs as scarcely engaged in the three pillars of the CSR, often put in place punctual approaches concerning waste recycling and the use of biodegradable packages. This practice is carried out to avoid retaliations by the authorities in charge of the environmental protection.

The training and the amelioration of working conditions on the internal social aspect or the sponsoring on societal dimension are quasi-ignored by SMEs in the sample. The humanization of what remains thus less anchored on SMEs managers’ behavior in Cameroon forgetting that human resources constitute an important dimension of the failure or success of enterprises. Hence, the SME manager is convinced that he is the main input of his enterprise, but without taking into consideration his limited rationality in the midst of flows of information to manage particularly when the enterprise grows in size.

Based on the results obtained we wish that the integration of CSR principles by Cameroonian SMEs managers be a reality and even a strategic concern. The poor management of risks linked to the non adoption of CSR could be fatal for certain SMEs in the industrial sector. Some activities involve taking into consideration on daily basis the stakes linked to the CSR. And the enterprise must adapt an approach consisting in indentifying the potential risks, evaluating and choosing to implement the appropriate measures. These risks could involve a sanction from the customer (operational risks or technical risks, judicial, fiscal and environmental risks etc) and even of public authorities or society as a whole. The Cameroonian SME is gaining by being socially responsible. It must therefore be accompanied in this regard by public authorities, NG0s, labor unions and other stakeholders. In fact, a CSR policy by SMEs motivated an in-depth study seeking to give a sense to observation, realized together are appropriate. Despite this limit, this work rather gives many possibilities for research in future for the CSR in the context of SMEs in Cameroon. Qualitative research could be carried out revolving SMEs managers of the same sectors in order to bring out trends by sectors of activity and be able to propose adapted solutions according to the product and throughout the chain of value. Similarly, with a multi-perspective research analysis, a particular SME could be done not only for the protection of its manager but also that of stakeholders (collaborators, customers, community, suppliers, etc). This type of research about the identification and understanding of CSR attributes in SMEs take into consideration different points of view.

REFERENCES

|

Ashforth BE, Gibbs BW (1990). "The double-edge of organizational legitimating", Organization Sci. 1(2): 177-194. Crossref |

||||

| Beland PH, Piche J (1998). Faites le bilan social de votre entreprise fondation de l'entrepreneurship staff, published by Editions Transcontinental, Montréal, PQ, Canada. | ||||

| Bowen HR (1953). Social responsibilities of the businessman, Harper & Row, New York. | ||||

| Brown DJ, King JB (1982). Small business Ethics: Influence and perceptions. J. Small Bus. Manage. 20: 11-18. | ||||

| Capron M, Quairel-Lanoizelee F (2007). La responsabilité sociale de l'entreprise, la Découverte, collection Repères. | ||||

| Carroll AB (1979), A three dimensional conceptual model of corporate performance. Acad. Manage. Rev. 4(4):497-505. | ||||

| Clarkson MB (1995). A stakeholder framework for analyzing and evaluating corporate social performance, Acad. Manage. Rev. 20(1): 92-117. | ||||

| Courrent JM, Gundolf K (2008). Sentiment d'appartenance à une communauté et éthique managerial en TPE", Actes de la conférence de l'AIMS, Nice, 2008. | ||||

|

Davis K (1973). The case for and against business assumptions of social responsibilities. Acad. Manage. J. 16(2):312-322. Crossref |

||||

|

Dowling J, Pfeffer J (1975). Organizational legitimacy: Social values and organizational behavior. Pacific Sociol. Rev. 18(1): 122-136. Crossref |

||||

|

Enderle G, Tavis L (1958). A balanced concept of the firm and the measurement of its long-term planning and performance, J. Bus. Ethics 17(11): 1129-1144. Crossref |

||||

| Evrard Y, Pras B, Roux E (1997). Market-études et recherches en marketing, Nathan, Paris. | ||||

| Freeman RE (1984). Strategic management : A stakeholder perspective. Englemewood Cliffs, Prentice Hall, Boston. | ||||

| Friedman M (1970), "The Social Responsibility of business is to increase its profits", The new times Magazine, September 13, 32-34 | ||||

| Hambrick DC, Mason PA (1984). Upper echelons: the organization as a reflection of its top managers. Acad. Manage. Rev.9(2):193-206. | ||||

| Hlady-Rispal M (2002), Les études de cas, application à la recherché en gestion, DE BOECK, Bruxelles. | ||||

|

Jones TM (1980). Corporate Social Responsibility revisité, redefined. California Manage. Rev. 22(3): 599-668. Crossref |

||||

|

Jenkins H (2009). A 'business opportunity' model of corporate social responsibility for small- and medium-sized enterprises. Business Ethics: A European Review, 18: 21–36. Crossref |

||||

| Kammogne FP (1993). L'entrepreneur africain face au défi d'exeister, l'Harmattan, Paris. | ||||

| Lefebvre M, Singh J (1992). The Content and Focus of Canadian Corporate Social Performance and Disclosure. Paper presented at the Critical Perspectives on Accounting, New York. | ||||

| Vert L (2001). Promouvoir un cadre européen pour la responsabilité social des entreprises, COM, 366 final, Bruxelles. | ||||

| Messenghen K, Chabaux D (2010). Le paradigme de l'opportunité. Des fondements à la refondation, Revue Française de Gestion, 7(106): p.93-112 | ||||

| Mitchell RK, Agle BR, Wood DJ (1997). Toward a theory of stakeholder Identification and Salience: Defining the Principle of who and what really count, Acad. Manage. Rev. 22(4):853-886. | ||||

| NIS (2009), Recensement général des entreprises, édition INS, Yaounde'. | ||||

| Pfefer J, Salancik G (1978). The external control of organizations: A resource dependence derspective, Harper and Row. | ||||

|

Pfefer J (1994). Competitive advantage through people: unleashing the power of the work force. Harvard Business School press. Crossref |

||||

| Shocker AD, Sethi SP (1974). An Approach to Incorporating Social Preferences in Developing Corporate Action Strategies, in Sethi SP (ed.), The unstable ground: Corporate Policy in a Dynamic Society, Melville Publishing Company, Los Angeles, p. 67-80 | ||||

| Smith AJ (2003). Quantitative Psychokogy: A Practical Guide to Research Method front Cover, Sage Publications, New York. | ||||

| Stake RE (2000), "Case Study ", in DENZIN N.K. LINCOLN Y.S. (Eds.), Handbook of qualitative Research, Second edition. | ||||

| Thompson JK, Smith HL (1991). Social responsibility and small business: Suggestions for research, J. Small Bus. Manage. 29(1): 30-45. | ||||

| Wacheux F (1996). Méthodes qualitatives et rechercheen gestion, Economica, Paris. | ||||

| Weber M (2002). Le Savant et le Politique, Edition 10/18, 221 p. | ||||

| Wood DJ (1990). Business and Society: Harper Collins, New York. | ||||

| Yin RK (1990). Case Research, Design and methods. Applied Social Research Methods, Vol. 5, Sage, Newbury Park. | ||||

Copyright © 2024 Author(s) retain the copyright of this article.

This article is published under the terms of the Creative Commons Attribution License 4.0