Full Length Research Paper

ABSTRACT

This study aims to investigate the structure and the content of Integrated Reporting, a new corporate reporting model that seeks to link financial and non-financial information disclosed by companies. This paper assesses the nature and extent of non-financial disclosures in corporate reports of the mining companies listed on the Johannesburg Stock Exchange. The methodological approach is Content Analysis with the aim of carrying out an automated lexical/textual analysis on the content of non-financial information using software for collecting a Corpus of data from the analysed corporate reports. The results do not highlight good practices of non-financial disclosure: the overall analysis does not detect homogeneous behaviour among companies. Nevertheless, the higher incidence of issues on Key Performance Indicators (KPI) targets and governance structures could be due to their relationship to certain listing requirements. The analysed period is restricted to one year, and it could be interesting to perform a longitudinal analysis. There is also a lack of a comparative analysis by means of the assessment of other industries in South Africa. Integrated Reporting is still in its early stages; consequently, findings from the first adopters may provide an insightful overview about its threats and weaknesses and practical suggestions for its preparers and users. The research may contribute to studies on the mining industry in the first country that has required the adoption of Integrated Reporting. The present study focuses on the first adoption of a new reporting tool that may be able to improve corporate communication to a wide range of stakeholders.

Key words: Integrated reporting, textual analysis, disclosure index, non-financial information, mining industry, South Africa.

INTRODUCTION

This study focuses on an analysis of the first adoption of Integrated Reporting (IIRC, 2013a), a new model of business reporting that combines financial and non-financial information, with a particular focus on the environmental, social and corporate governance items (Eccles and Krzus, 2010, 2014; Adams et al., 2011; Eccles and Armbrester, 2011; Tilley, 2011; Busco et al., 2013; King and Roberts, 2013). Consequently, Integrated Reporting (IR) aims to disclose information about the company’s strategy, corporate governance and financial performance; to reflect the financial, social and environmental context within which companies operate; and to disclose a detailed description of companies’ value creation in the medium-long term (IIRC, 2013b; Eccles and Krzus, 2010, 2014; Churet and Eccles, 2014; PWC 2010). Although a standardized structure has not yet been defined and there are no detailed guidelines (Rossouw, 2010: Busco et al., 2013; Abeysekera, 2013), IR has already been adopted (CorporateRegister.com, 2013) by an increasing number of companies.

The purpose of this paper is to contribute to the empirical understanding of early Integrated Reporting practices among the South African listed companies. This is achieved by analysing the IR disclosures within a wide range of corporate reports in the first stage of IR adoption (fiscal year 2011). The research objectives are the following:

RO1: to identify the main items of non-financial information that should to be included in Integrated Reporting to highlight the major features of the IR content and structure;

RO2: to assess both the amount (how much) and themes (what) of non-financial information disclosed in corporate reports drawn up by 20 South African mining companies listed on the Johannesburg Stock Exchange (JSE).

The selection of South African companies is justified by several reasons; for example, there are interesting disclosure requirements issued by King Code of Governance Principles for South Africa (King III, 2009). In addition, the companies listed on the JSE are required to adopt Integrated Reporting for all financial years ending on or after March 1st 2010. There is also a strong propensity for developing countries to disclose items in the three categories of intellectual capital (Goh and Lim, 2004; Abeysekera, 2008) and social and environmental issues (de Villiers and van Staden, 2006).

The mining sector was chosen because of its significant role in the South African economy and its high risk with regard to ethical, social (Davis et al., 2012) and environmental issues (Firk, 2002; de Villiers and van Staden, 2006; Lodhia and Hess, 2014). The mining industry also includes companies with the highest environmental impacts, for example, high CO2 emissions (National Treasury, 2010; Hindley and Buys, 2012); it needs its operations to be legitimized by means of environmental disclosures and practices (de Villiers and Barnard, 2000).

Reflecting the growing importance of non-financial disclosures in the success and reputation of many companies, there has been a dramatic increase in the academic attention paid to various aspects of these items, but IR adoption is still in its early stage and only few studies have made an in-depth investigation of the first reports drawn up by South African companies at the outset of IR implementation (Hindley and Buys, 2012; Carels et al., 2013; Setia et al., 2015).

KING CODE III (THE KING REPORT ON GOVERNANCE FOR SOUTH AFRICA 2009)

Companies listed on the JSE are required to implement integrated sustainability performance and integrated reporting (all companies must issue an “integrated report” for financial years starting on or after March 1, 2010 m or explain why they are not doing so). The new requirements stem from the Institute of Directors, South Africa (IODSA)’s King Code of Governance Principles (King III). New JSE listing requirements put the Code into effect on 1 March 2010 for financial years ending 28 February 2011 and beyond. Although the King III enables companies to draw up separate reports for financial and non-financial information, the revolution brought about by the adoption of IR is represented by the deep cohesion among the different types of information: rather than being developed separately, financial, environmental, social and governance reports are produced in close connection with each other and made available simultaneously on the websites of listed companies.

King III recommends that entities adopt IR to enable stakeholders to make a more informed assessment of a company, based on a combination of its financial and social value, rather than its book value alone. In the words of Mervyn King, “Sustainability is the primary moral and economic imperative for the 21st century”. The term “integrated report” is used throughout the Code and is explained in chapter 9: “The integrated report should … have sufficient information to record how the company has both positively and negatively impacted on the economic life of the community in which it operated during the year under review, often categorized as environmental, social and governance issues (ESG).

Further, it should report how the board believes that in the coming year it can improve the positive aspects and eradicate and ameliorate the negative aspects” (King Code of Governance Principles for South Africa 2009: 9). King III’s key principles are the following: Leadership, Sustainability and Corporate Citizenship. In particular King III identifies certain principles of IR and disclosure (King III, Chapter 9) that should inform the process of IR.

Integrated reporting and disclosure requirements

The board should ensure that appropriate systems and processes are put in place to produce a report to stakeholders that provides a complete picture of a company’s financial and non-financial profiles such that the report is holistic and reliable. To comply with the recommendations of the Code, “reporting should be integrated across all areas of performance, reflecting the choices made in the strategic decisions adopted by the board, and should include reporting in the triple context of economic, social and environmental issues. The board should be able to report forward-looking information that will enable stakeholders to make a more informed assessment of the economic value of the company as opposed to its book value.” King III recommends companies adopt IR to show the following key elements of business:

1. Effective ethical leadership and corporate citizenship;

2. Governance of risk;

3. Governance of information technology;

4. Compliance with law, codes, rules and standards;

5. Their relationship with governing stakeholders.

More specifically: 1. Company decision-makers (the board of directors) should ensure the proper conduct of their firm in terms of their positive impact on the triple bottom line to qualify the company itself as a "good corporate citizen". 2. King III defines the roles and responsibilities for a risk management approach involving all types of business operations. 3. In addition, King III attaches great importance to the governance and management of information technology resources for the achievement of high specific skills. 4. Companies are required not only to comply with the rules established by law but also to follow those non-binding rules that can improve corporate governance. 5. A final aspect introduces an interesting new concept called "Alternative Dispute Resolution" (ADR), reported as Principle 8.10 in Chapter 8, "Managing stakeholder relationships", whereby King III places particular emphasis on stakeholders with the aim of providing adequate solutions to disputes that may arise in business relationships. To this end, it should be noted that the Code requires the Board to provide forecast information and ensure its quality and reliability, as this aspect represents a priority request by stakeholders.

The lack of a standard reporting framework may re-present a serious obstacle to the current implementation of King III by all listed companies. For this reason, the role of the Integrated Reporting Committee South Africa (IRC SA) becomes essential, in that it does not reiterate the disclosure principles of King III, but "it sets out a framework within which such disclosures can be reported using the principles of “apply or explain" and of "substance over the form" (IRC SA, 2012: 18). The processing of a report should be carried out thoroughly from the very beginning by implementing the principles in the company’s core business strategy to generate undoubted benefits, such as an increase in the legitimacy of the company's transactions and higher confidence among stakeholders.

The IRC and its framework working group will coordinate efforts with the Global Reporting Initiative’s (GRI’s) new International Integrated Committee (IIRC). The establishment of the IIRC is designed to support one of GRI’s goals for 2020, to converge ESG and financial reporting, which was announced at the Amsterdam Global Conference on Sustainability and Transparency in late May 2010 (www.amsterdamgriconference.org/ index.php?id=39&item=33). A fundamental support mechanism for the implementation of IR is the Global Reporting Initiative (GRI), a member of the International Integrated Reporting Council (IIRC), together with the International Accounting Standards Board (IASB), the Financial Accounting Standards Board (FASB), the Prince’s Accounting for Sustainability Project and the World Business Council for Sustainable Development (WBCSD). The GRI is a globally recognized organization that has de facto established the standards for ESG reporting. As is well-known, in addition, the GRI sets the guidelines not only for "what to report" but also for "how to report", as well as laying down the rules for the implementation of reports in accordance with the so-called triple bottom line. The G3 guidelines (G3) were developed in 2006 and represent the third generation of GRI Guidelines for sustainability reporting. The guidelines indicate the general principles, guidelines and communication standards that should be included in sustainability reports. Recently, GRI updated these guidelines and issued a new version, the 2013 G4 Guidelines (GRI, 2013).

LITERATURE AND BACKGROUND OF THE STUDIES

The strong need to change corporate reporting (Beattie, 2000; Singleton-Green, 2010) towards a gradual “managerialization”, that is, the adoption an internal perspective in the drawing up of external disclosure (Beattie and Pratt, 2003; Beattie et al., 2004; Zambon, 2011) has been boosted by the unanimous acknowledgement of the lack of information in traditional corporate reporting. The information gaps mainly concern the recognition and measurement of intangibles and intellectual capital (Striukova et al., 2008); more recently, environmental and sustainability items and ESG indicators (Environmental, Social and Governance) have become key information items (Gazdar, 2007; FEE, 2008; KPMG, 2011a, b; Hopwood et al., 2010; Eccles and Krzus, 2010, 2014; Porter and Kramer, 2011; IIRC, 2011, 2013a; ACCA and Eurosif, 2013; Iannou and Serafeim, 2014). Companies are being forced to re-evaluate how they can report financial and non-financial data as transparently as possible to all stakeholders (Rensburg and Botha, 2014). Non-financial disclosure is especially remarkable because it provides different stakeholders with information that financial reporting alone fails to provide (White, 2005). Stakeholder theory emphasizes the need for an organization to identify powerful stakeholders (Stainbank, 2012) to which it is accountable and to maintain a good relationship with these stakeholders, which could include voluntarily disclosing information (Deegan et al., 2000; Newson and Deegan, 2002; Van Staden, 2003; Gray et al., 2014).

The mining sector shows an exceptional sensitivity to ESG issues (Frik, 2002) and corporate social responsibility (de Villiers and Alexander, 2014). Therefore, stakeholders would give due attention to the industry’s environmental, social and governance performance. Jenkins and Yakovleva (2006: 272) state that there is an increased demand for the disclosure of social and environmental information by mining companies as a means of legitimizing their existence and documenting their performance (de Villiers and van Staden, 2006; Pellegrino and Lodhia, 2012; de Villiers and Alexander, 2014). Environmental legitimacy shows a strong relationship with environmental accountability, which involves the public evaluation of corporate environmental performance and reporting. This is also dependent on environmental proactivity, which requires companies to invest in environmental management and accounting systems, as well as stakeholder engagement (Alrazi et al., 2015).

Prior research: The case of South Africa and the mining industry

First, an overview of the existing literature evaluates the previous studies focused on corporate reporting referring to the integration of financial and non-financial information. As a preliminary result, a strong need for the disclosure of non-financial information can be emphasized in several studies (Robb et al., 2001; White, 2005; Bollen, 2004; Palenberg et al., 2006; Gazdar, 2007; Coram et al., 2009). According to Gray et al. (1995), non-financial reporting and especially social and environmental disclosure is country-dependent because independent studies in different countries provide different results. This type of disclosure in developing countries is crucial (Kumah, 2006; Islam and Deegan, 2008, de Klerk and de Villiers, 2012) and particularly necessary given the presence of multinational corporations in developed countries.

In depth-analyses mainly concentrate on the studies carried out in the mining industry, whereas, is well known, non-financial disclosure causes undoubted benefits in terms of transparency (KPMG, 2006). The increase and improvement of disclosure on intangibles, intellectual capital (Firer and Williams, 2003; Yongvanich and Guthrie, 2005), social (Coetzee and van Staden, 2011), sustainability (Borkowski et al., 2012) and environmental (Burritt, 1997; Antonites and de Villiers, 2003; Jenkins and Yakovleva, 2006) items is to be welcomed by mining industry stakeholders (Yakovleva and Vazquez-Brust, 2012). Moreover, it is possible to find several studies focused on Corporate Social Responsibility (CSR) (Warhurst, 1998; Tawiah and Dartey-Baah, 2005; Guenther et al., 2007; Hutchins et al., 2007) and on corporate governance within the mining industry (Abdo and Fisher, 2007; Mangena and Tauringana, 2007).

The previous content analysis studies based on companies’ annual reports within the mining industry have mainly focused on environmental and social disclosures (de Villiers and Barnard, 2000; de Villiers and Lubbe, 2001; Jenkins and Yakovleva, 2006; Kemp et al., 2010; Fonseca et al., 2014; Maubane et al., 2014; Lodhia and Martin, 2014; de Villiers et al., 2014), sustainable management practices (Maffini et al., 2015), IC measurements and reporting (April et al., 2003), voluntary disclosures (Stainbank, 2012) and risk disclosures. If we shift from content analysis studies based on traditional corporate reporting to content analysis studies based on IR, we find that few studies have attempted to explore the disclosures and practices of the first adopters of IR (Wild and van Staden, 2015) in the mining sector (Hindley and Buys, 2012; Carels et al., 2013).

To verify the crucial role of IR in overcoming the information gaps in traditional corporate reporting (Eccles and Krzus, 2010, 2014; Leuner, 2012), we sought to evaluate the content of non-financial information (Chauvey et al., 2013) and the materiality of non-financial Key Performance Indicators (KPIs) by performing a content analysis on IR via a sample of listed mining companies.

METHODOLOGY

Content analysis and text mining

The methodological approach is the content analysis (Krippendorff, 1980; Weber, 1990; Krippendorff and Bock, 2009), which is often adopted in social sciences to measure external disclosures (Beattie et al., 2004; Beattie and Thomson, 2007), which are sometimes supported by a disclosure-scoring system (Robb et al., 2001; Vanstraelen et al., 2003). This analysis may generate data that can take the form of judgments of kind, magnitude and frequency (Hayes and Krippendorff, 2007). In addition, this methodological approach is useful because content analysis as a well-established method in social science and can classify text units into categories (Beattie et al., 2004; Dumay and Cai, 2015). Despite the important contribution of content analysis to analyse the “narrative” portion of companies’ reports, many scholars have noted criticisms, for example: difficulties in delivering reliable content analysis (Boyatzis, 1998); difficulties regarding the choice of different units of analysis, such as words, sentences or pages (Gray et al., 1995; Beattie and Thomson, 2007); the need to test the reliability of the coding decision rules (Milne and Adler, 1999; Krippendorff, 2004; Krippendorff and Bock, 2009) and the disclosure rating (that is, by dummies or frequency counts).

The increasing and continuous production and spreading of digital text data, as well as the evolution of information technology, have enabled the development of methods and algorithms for the acquisition, classification and automatic management of a large amount of unstructured textual databases. In the 1960s and ‘70s, statistical studies on data expressed in natural language or textual data had already undergone deep changes as a result of the evolution of information technology, later leading to the introduction of automatic text analysis and textual statistics (Lebart and Salem, 1994). Today, the latest solutions are no longer based solely on statistical instruments but are in fact the result of a strict multi-disciplinary approach whereby such instruments are combined with computer and language instruments, particularly in a research area known as text mining (Sullivan, 2001; Zanasi, 2005; Bolasco et al., 2005). In this context, text mining has become essential to draw out knowledge from data (Korczak et al., 2013). The use of automatic techniques for text analysis thus becomes necessary whenever the amount of information is such that it hinders the manual resolution of problems in terms of data classification and clustering.

Given these premises, to limit certain criticisms (the first and third in the list indicated above) of content analysis and reach a great level of reliability avoiding subjectivity, this analysis should be performed by a specific software programme (Beattie and Thomson, 2007; Gumb and Noël, 2009). The use of software shows certain limitations due to the search and count of the unit of analysis; in our case, these limits are overcome due to the sophisticated treatment of the text by the software. It is important to emphasize that automatic content analysis is not able to indicate the location of the items as each company’s reports are combined into a single TXT file.

Disclosure index

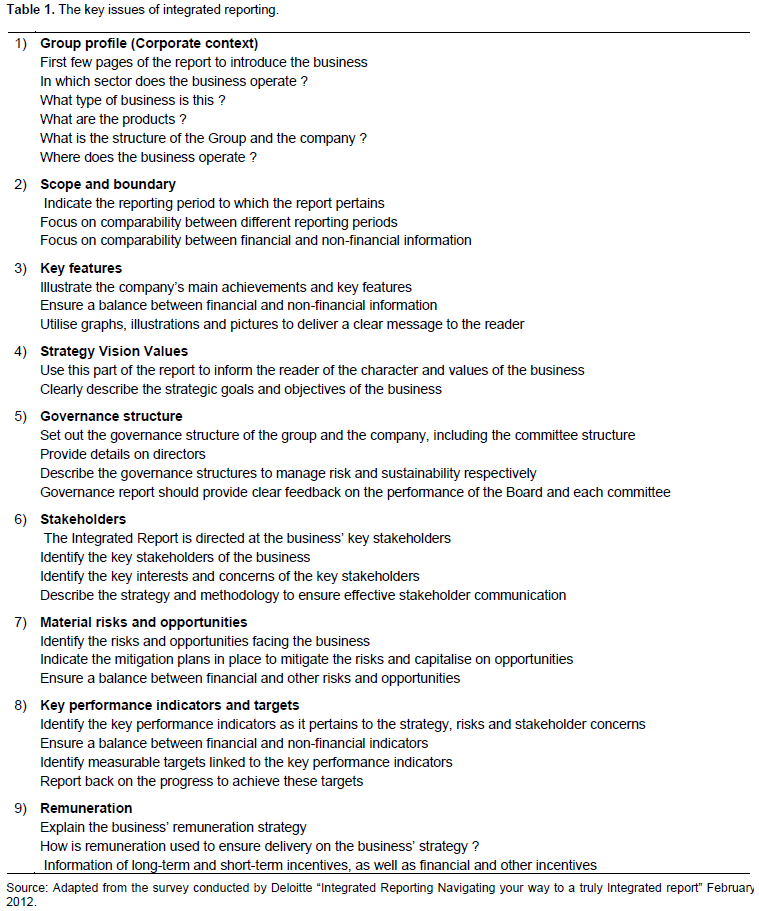

The main items of IR structure and content used in content analysis in the following tables contain a methodological reference in the following documents:

(i) ‘King Report on Governance for South Africa’ and ‘King Code of Governance Principles’ (King III). The Institute of Directors in Southern Africa, 2009;

(ii) Integrated Reporting Committee of South Africa (IRC SA), Discussion Paper, 25 January 2010;

(iii) International Integrated Reporting Council (IIRC), Towards Integrated Reporting - Communicating Value in the 21st Century, Discussion Paper, September 2011;

(iv) Survey conducted by Deloitte (2012) available in the paper “Integrated Reporting: Navigating your way to a truly Integrated Report”, February 2012.

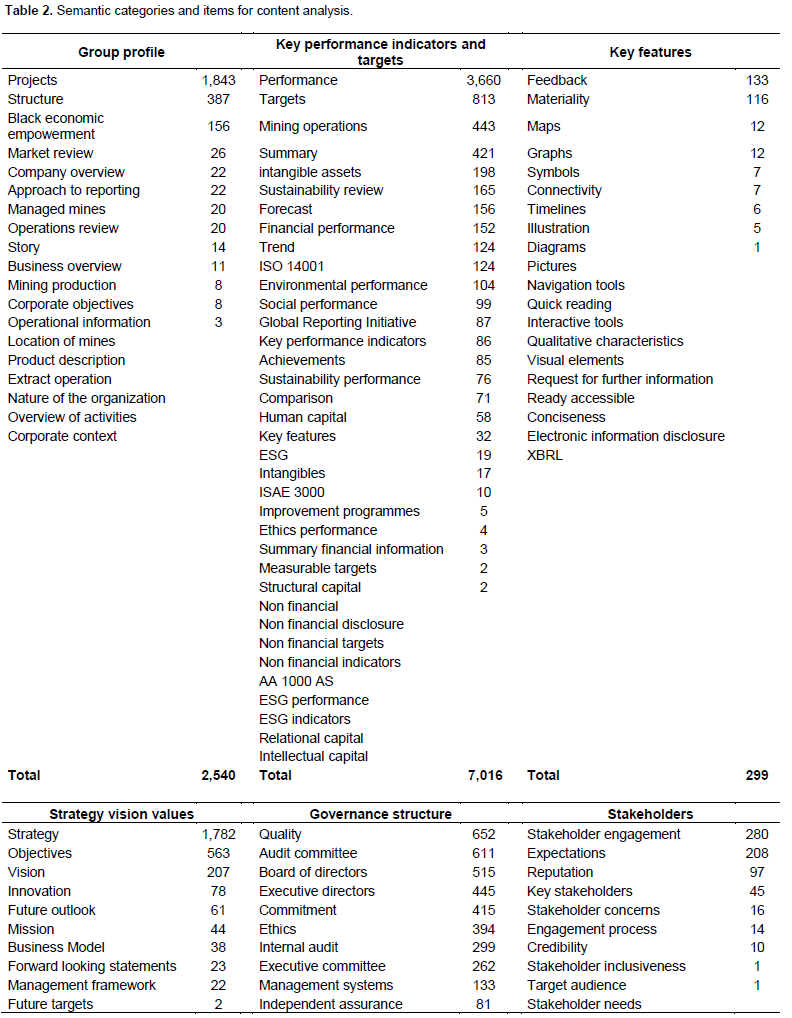

We decided to select nine semantic categories correlated to the key contents of IR (Table 1) on the basis of the framework issued by Deloitte (2011). For each category, we selected certain words or groups of words to understand how companies disclosed these issues within IR (Table 2).

Sample selection

The mining sector represents a significant portion of the South African economy (Davies et al., 2002; Maubane et al., 2014). All 20 South African mining companies listed on the JSE in 2012 were included in this study (Appendix 1). Mining companies were selected because the mining industry represents the largest market capitalization on the JSE (ADVFN, 2007). Consequently, the influence of the mining industry on the South African economy is substantial (PWC, 2013).

The 2011 corporate reports drawn up by the mining companies listed on the JSE were downloaded from the websites of these companies and analysed. The results of the content analysis were then tabulated in spreadsheet format using the Excel package. The extent of the quantity (how much) and themes (what) of disclosure and the benchmark assessment of the companies’ non-financial disclosures were captured in tables for analysis.

Johannesburg stock exchange SRI index

The JSE SRI was launched in May 2004 as a system to identify those companies listed on the JSE that incorporate the principles of the triple bottom line and good corporate governance into their business operations (JSE and EIRIS, 2010). Some of the companies provided the GRI disclosure index for their non-financial reporting, which made it easy to follow the extent of their non-financial disclosures. Listed South African mining companies are encouraged to adopt GRI as the basis of their sustainability reporting in terms of King III. In other terms, King III recommends that companies produce an integrated report in place of an annual report and a separate sustainability report and those companies create CSR reports according to the GRI Guidelines. This fact provided the impetus for the improvement in these disclosures.

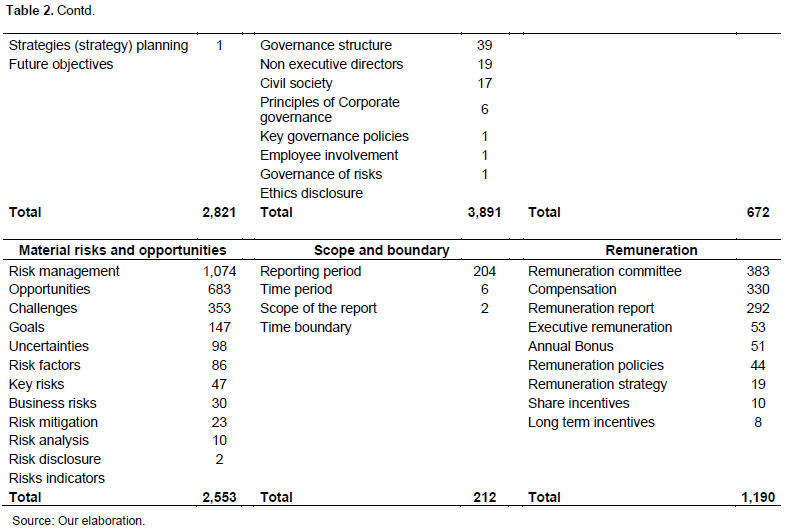

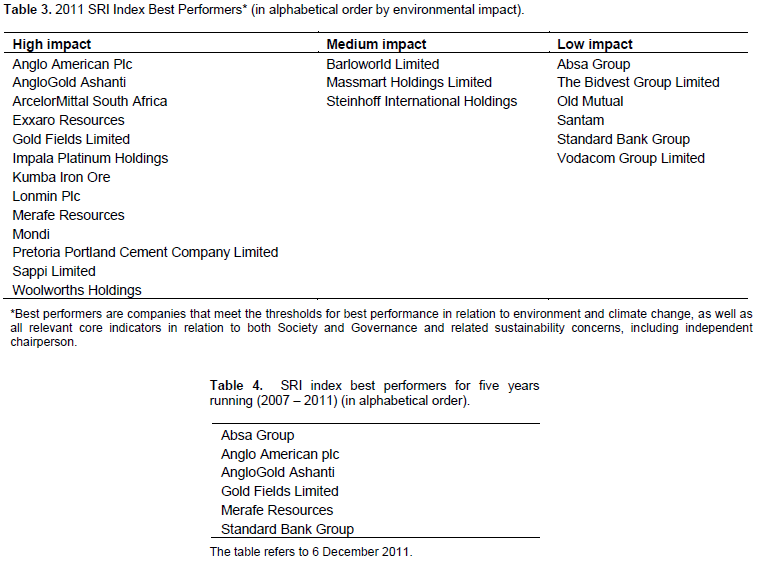

In the following tables, it is possible to notice the companies that have obtained the best results in terms of SRI index: in the first column labelled “high impact”, there are eight mining companies that are included in our sample (Table 3). Table 4 shows the companies that obtained the best results in the last five years, 2007-2011 (the so-called “consistent best performers”). Four of the companies in our sample are on this list: Anglo American Plc, Anglogold Ashanti, Gold Fields Limited and Merafe Resources.

Research design and data collection

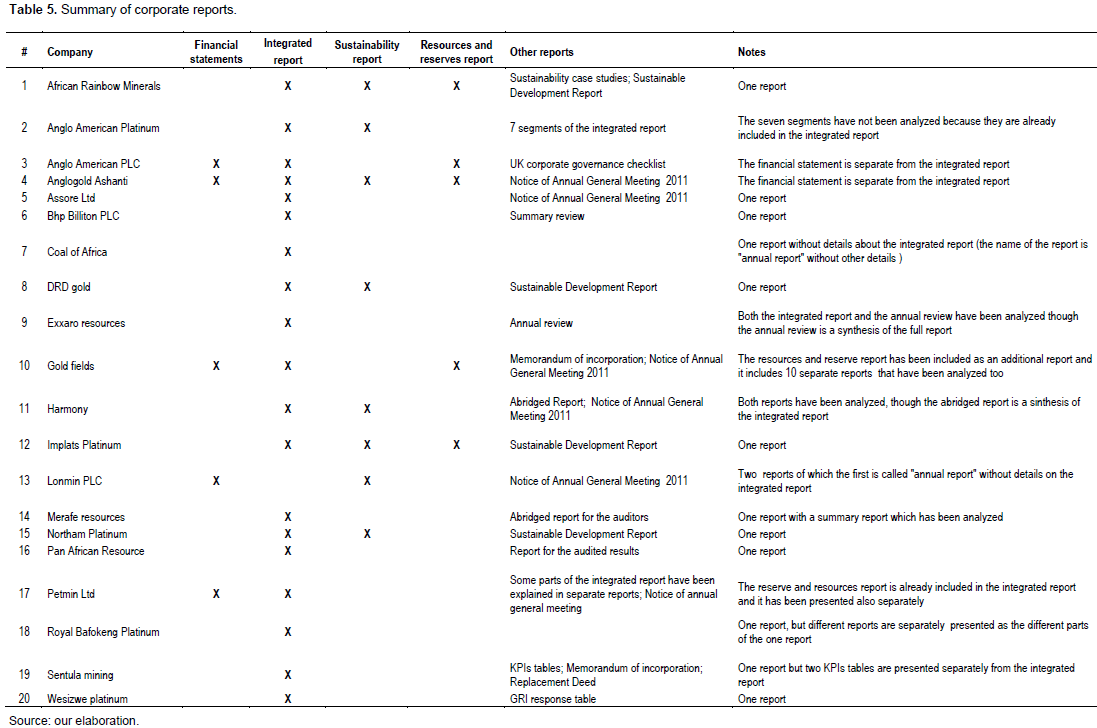

The empirical research sought to make a benchmarking analysis between the mining companies referring to both the amount and the themes of the information disclosed by the firms (Stainbank, 2012). An assessment of the degree of the companies’ compliance with reference to the guidelines required by the above-listed documents will be formulated by means of a disclosure checklist (Table 5). The Research Questions are below:

RQ1: What are the amount (how much) and themes (what) of the items included in nine semantic categories (that is, disclosure checklist, (Table 5) disclosed by the mining companies listed on the JSE?

RQ2: Is it possible to identify homogeneous behaviour within the sample of the companies?

RQ3: What is the degree of compliance with items selected, in spite of the lack of a common framework for creating an integrated report in SA?

The analysed corporate reporting material mainly included the following documents:

(1) Annual financial statements;

(2) Annual integrated reports;

(3) Sustainability reports;

(4) Mineral resource and ore reserve reports.

Annual report disclosures include a single component of an organization’s public communication (Aerts and Cormier, 2009). Previous content analysis studies note that only examining the annual report could lead to underestimating the extent of social disclosures and that focusing exclusively on annual report disclosures may yield irrelevant or misleading results (Unerman, 2000). Therefore, this study analyses integrated reports, sustainability reports and other reports, such as mineral resource and ore reserve reports, which are useful for conveying non-financial information (Coetzee and van Staden, 2011).

An analysis of the reports made available on the websites of the sample of companies highlights significant differences in their approaches. In some cases, companies only disclose one report, while in other cases, they either provide several reports or only summary reports. Alternately, sometimes an integrated report is provided as both a single document and separate segments focusing on specific subjects. This has forced us to make some choices, and there are cases where some data have not been included in the corpus because they were already inserted in the main document. In other cases, additional documents, such as tables with KPIs or the reports given to shareholders at Annual General Meetings, or other reports prepared on a voluntary basis, have been included.

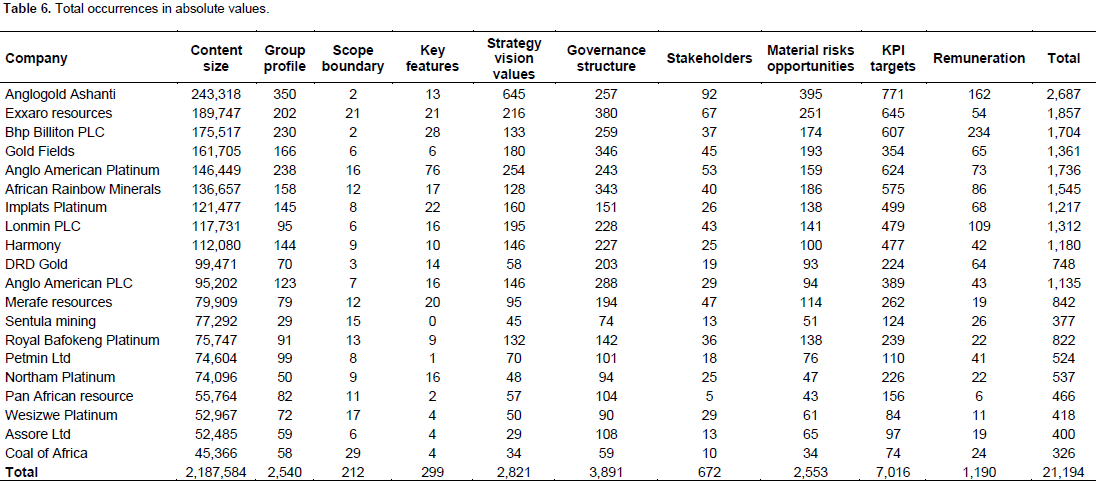

The overall size of the corpus (that is, all reports analysed) totals 2,479,586 occurrences of which 292,002 are occurrences of numerical elements, for a total of 2,187,584 text occurrences, excluding numerical occurrences. Textual analysis sought to identify the extent of the items belonging to nine semantic categories in the sample of corporate reports and highlight the correlation between mining companies and semantic categories. The analysis is carried out in three steps: 1. Identification of the semantic categories in the vocabulary and corpus through semantic tagging; 2. Extraction of the information by using software called Regular Expression (RE) and 3. Assessment of the correlation between companies and documents through an analysis of simple correspondences.

The lexical/textual analysis of the corpus has been carried out using TaLTaC2 software (Bolasco, 2010a), whereas SPAD 5.0 software was used for the analysis of correspondences. Semantic tagging recognizes the simple and complex forms of the nine semantic categories listed in Table 6 and records them in the vocabulary. The application of the RE allows for the identification of semantic categories in the corpus that were previously recorded in the vocabulary. Because this operation, a text variable can be generated in which the occurrences of the different semantic categories are calculated for each document.

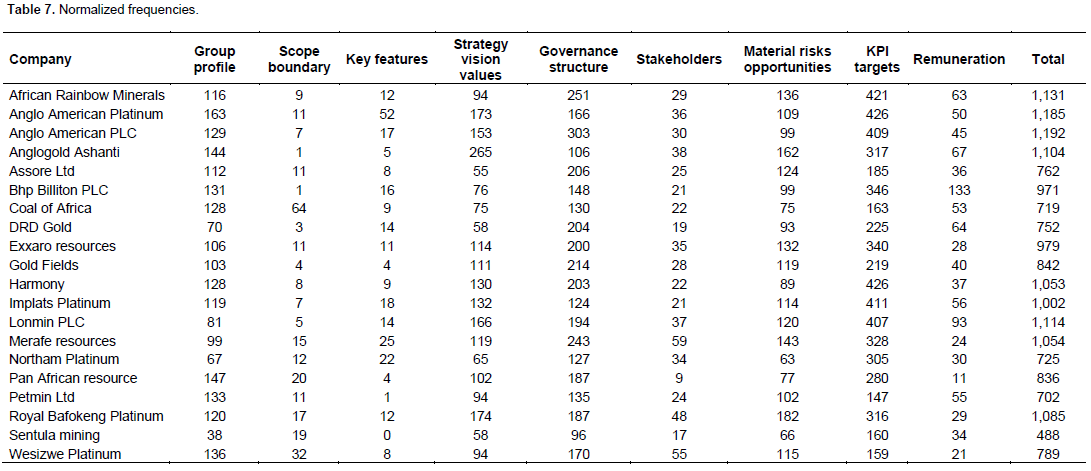

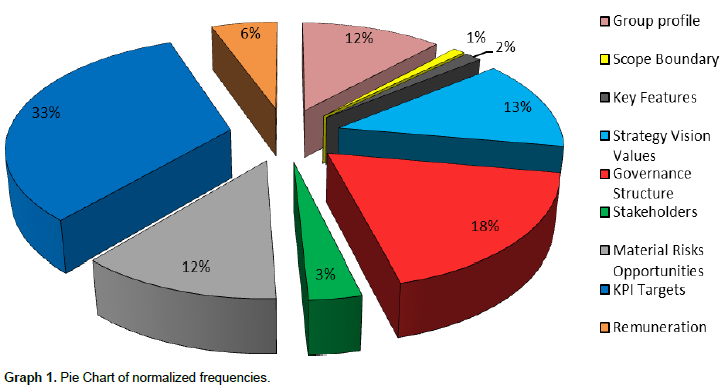

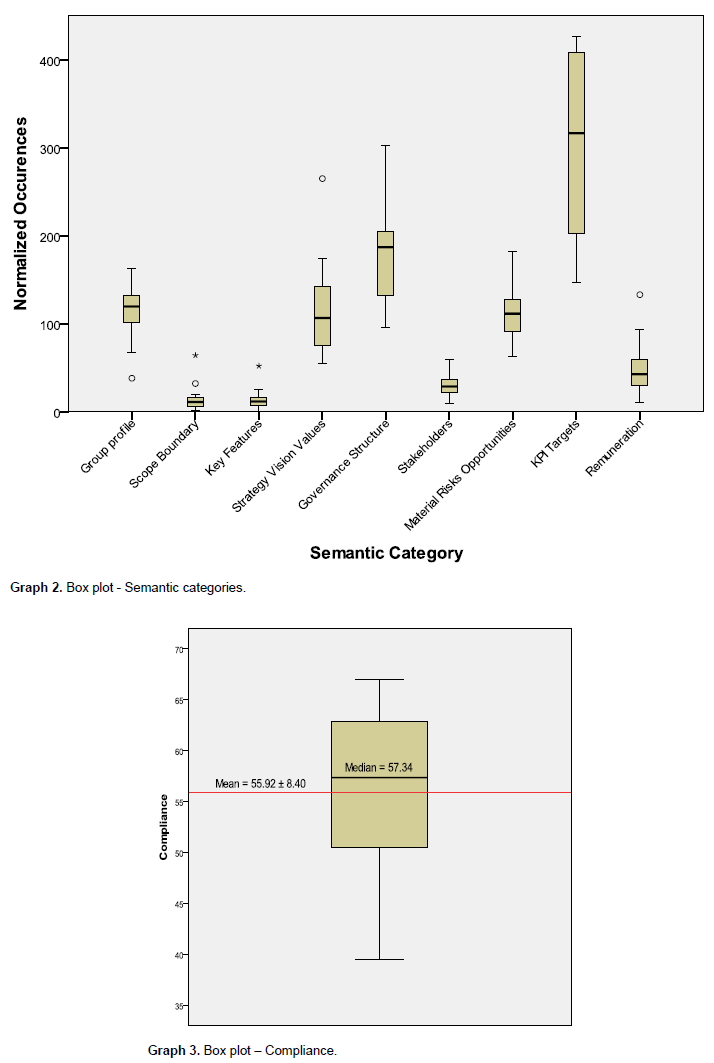

To better compare the use of items among the different companies, it is necessary to normalize the frequencies to delete the effect of the different sizes of the documents (Table 7 normalized frequencies) (Graph 1).

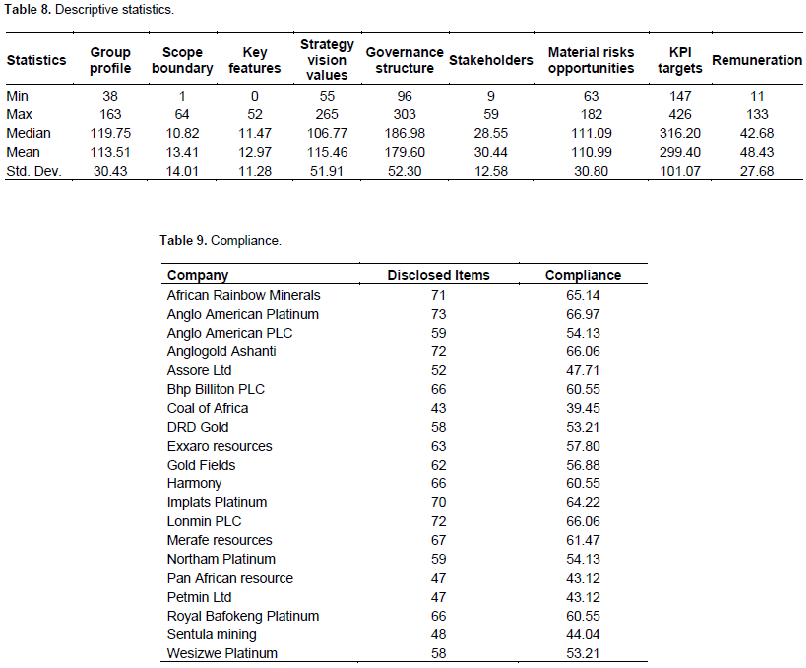

The results are also presented as percentages, which are used to measure to what extent each company discloses information in reference to each category of non-financial information within the analysed reports. Empirical findings are also shown using descriptive statistics (Yongvanich and Guthrie, 2005) to identify the companies with the highest and lowest disclosure levels for each category. In addition, the most commonly reported disclosure items were identified (Tables 8 and 9, Graphs 2 and 3).

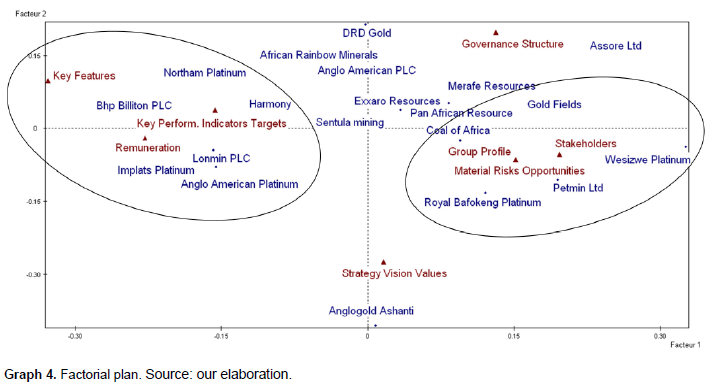

Through an analysis of simple correspondences applied to the Documents x Variables matrix (items) it is possible to represent on the factorial plan the correlations between companies and thematic categories. In order to have a better representation of the factorial plan, it has been necessary to exclude the "scope and boundary" variable from the analysis, because it is of small size and strongly correlated to Coal of Africa. In order to properly explain the picture of the factorial plan it must be emphasized that the more distant the documents and the variables are from the origin, the greater their contribution to the determination of the axes, whereas the proximity of the documents refers to a correlation between the two characters (Bolasco, 2010b) (Graph 4).

RESULTS AND DISCUSSION

The results shown in Tables 6 and 7, including the total occurrences and the normalized frequencies relating to each category enable us to evaluate the amount (how much) and the themes (what) of non-financial information disclosed by the mining companies listed on the JSE.

The first semantic category Group Profile (Corporate context) concerns the extent to which the information provided effectively communicates the “story” of the company to the stakeholders. Here, the main products and services of the organizations, its major markets and locations, key financial data and organization structure are described. Companies are generally doing well at setting out the corporate context in an easily readable and understandable format, sometimes using graphs, symbols, illustrations and diagrams, and the flow of information is generally logical. The disclosure checklist shown in Table 2 includes 19 items, 13 of which are detected with different absolute and normalized values (approximately 68% incidence). The following items have not been detected by the textual analysis:

(1) Location of mines

(2) Product description

(3) Nature of the organization

(4) Overview of activities

(5) Corporate context

The first and the second items concern technical aspects of the company’s production, but the other items are generic and concern the company profile. We expected more information about the characteristics of production to clarify the environmental and social practices adopted by companies. If we analyse the normalized frequencies, that is, those taking into account the size of the reports under analysis, the maximum value is attributed to Anglo American, whereas the minimum value remains associated with Sentula Mining. It is also interesting to estimate the percentage incidence of each item within the category: the item showing the highest incidence (72.6%) is "projects", whereas that with the lowest incidence is “operational information” (0.1%). Thus, there is clear evidence of a strong discre-pancy among the disclosures of the different items. In particular, we may notice that some items showing a specific relevance to the mining sector actually have rather low values; for example, items such as “mining production” and "managed mines” have a very low incidence, below 1, and Black Economic Empowerment (BEE), in particu-lar, has a value of approximately 6%. The BEE is indicated by the JSE as a required social indicator for the Socially Responsible Investment Index, and providing this information is one item of compliance with the rules established by the Broad-Based Black Economic Empowerment Act 53 2003 (the Act includes black Africans,Coloureds and Indians).

The part Scope and Boundary describes the comparability of financial and non-financial indicators, but it is necessary to note that the disclosure of non-financial data is relatively superficial and lacks information about non-financial targets, relational capital and intellectual capital. In this semantic category, only 4 items have been identified, making it the category with the smallest number of items and influencing the total number of occurrences that were identified in the analysis. The latter has detected only 3 items out of 4 (with an incidence of 75%); one of them, "time boundary", was not detected in the occurrences. The calculation of normalized frequencies shows Coal of Africa having the maximum value of occurrences in relative value (64), whereas both Anglogold Ashanti and BHP Billinton show the minimum value. As for the percentage incidence of each item within a single category, we can see that the item with the highest incidence – 96.2% - is the "reporting period"; the other two items have a very low incidence. The "scope of the report”, in particular, shows an incidence of approximately 0.01%. This may be seen as a sign of the companies’ increased emphasis on correctly identifying the accounting period of the financial reports, rather than the purpose of the reports themselves. The part Key Features contains the general characteristics of the report to address the key requirements of IR, specifically focusing on the length of the report, to whom the report is addressed and the balance between financial and non-financial data. Many companies put out non-financial KPIs about environmental and social performance. The third category analysed is composed of 20 items, of which only 9 were detected: in this case the incidence is 45%. An analysis of the data deducted from the influence of the size of the documents confirms the results of the evaluation of the data expressed in absolute value. In fact, we have a maximum value of 52 occurrences in Anglo American Platinum and a minimum value of 0 occurrences in Sentula Mining. The next step allows us to consider the percentage of each item within the category, and the resulting data show that the item with the highest incidence is "feedback" (44.5%), whereas the lowest incidence is registered by "diagrams" (0.3%). This result suggests an assessment of the incidence of similar terms that indicate the presence of graphs, diagrams and representations. If, for example, we consider the value of items such as “symbols”, “illustration”, “graphs” and “maps”, the resulting values are quite low, from 4 to 2.3% and down to 1.7%. This would suggest that mining companies do not generally focus on the part of their integrated reports that are devoted to graphs and pictures.

The main characteristics that are described in the part Strategy vision values are useful for understanding the vision of the future through challenges and relevant opportunities for the organization. More specifically, it examines the level to which the strategy goals, values and objectives correlate with the sustainability vision and whether the company has adequately assessed its key risks and opportunities. As for the items relative to strategy reports, the results show that only one item ("future objectives') out of a total of 11 was not found in any analysed report. In this case, the percentage is therefore high (91.6%) and allows us to give the semantic category a prominent position in the mining sector. Clearly, the number of occurrences must be estimated as a normalized value, but the overall judgment is very positive. As for the normalized values, a maximum value of 265 was detected in Anglogold Ashanti’s reports, whereas a minimum value of 55 was associated with Assore Ltd. The next step is the assessment of the percentage of each item in the category. As expected, the item with the highest percentage is "strategy" (63%), and the one with the lowest percentage is "strategy planning" (0.03%). However, the above items could be considered synonyms; consequently, in light of the results, the input of a single item would have been correct. Another item with a very low percentage (0.07%) is "future targets", where however, company disclosures have again preferred a more general term, such as "objectives", with an incidence of approximately 20%.

The part Governance Structures describes governance supports the strategic objectives of the organization related specifically to the approach to remuneration. The governance structure oversees the level to which strategy is linked to environmental, social and governance (ESG) risks and opportunities and the level of the integration with the business. The content of this part is formulated directly from King III, which clearly sets out the requirements for governance and specifically requires boards to include a statement on the integrity of the integrated report. The corporate governance category includes 18 items, and only one of them was not found in the reports analysed (that is, “ethics disclosure”), but as mentioned above, this item may be associated with "ethics", which has an absolute value of 394 out of a total of 3,891. The significant presence of nearly all of the items (94%) is evidence of the top priority assigned to this semantic category, as one might have expected in light of the significance attached to this aspect by the King III code. The normalized frequency table shows different results with respect to the absolute values: the highest value is associated with Anglo-American Plc, the lowest one with Sentula Mining. Thus, in this case, the size of the reports has been fairly influential. If we consider the importance of each item, the one with the highest incidence is "quality" (16.7%), whereas three items show the lowest incidence, namely, "employee involvement", "governance of risks" and "key governance policies". Examining the results, we think the positive quantitative judgment can be undermined by the strong presence of rather general items such as “quality” and “board of directors” rather than items such as “employee involvement”, “governance of risks” or “ethics”. Compliance with the King III code may therefore result in inadequate corporate governance and little attention to ethical conduct.

Integrated reporting provides insight into companies’ relationships (Section Stakeholders) with their key stakeholders (internal and external) and how and to what level the organizations understand and takes into account and responds to their needs and expectations. It is also necessary to ensure that major stakeholders are not overlooked or incorrectly prioritized. The link to which credibility is also achieved through external assurance must be assessed. The materiality of issues to stake-holders, however, cannot be assessed. Considering the significance of these issues within the organization itself and the overlap between what is important to both stakeholders and the company will define the truly material interests that should be described in IR. As for the items in the category concerning stakeholders, we can further note a strong correspondence with the items shown in the checklist: only 1 item out of a total of 10, “stakeholder needs”, was not detected in the analysed documents. The resulting data of the normalized frequencies show that the minimum value is associated with Pan African Resource, whereas the maximum value is identified with Merafe Resources. As for the assessment of the incidence of each item, the highest percentage is associated with “stakeholder engagement” (41.7), the lowest one with "stakeholder inclusiveness" and "target audience" (0.15). The most significant aspect of the non-financial information provided to stakeholders is therefore the need for the real involvement of all stakeholders in corporate life.

In the part Material Risks and Opportunities, there is a description of the circumstances under which the company works, including key resources and relationships on which it depends, the key risks and opportunities that will influence the organization, and how this will affect their business and the risk mitigation plan. It remains unclear, however, how organizations link these risks to their strategic objectives and how they translate to measurable KPI. The semantic category on risk and opportunity management totals 12 items, and only one (“risk indicators”) could not be detected by the TaL.TaC software. This category is therefore adequately represented in the reports of mining companies (91.67%). The results of the analysis of normalized frequencies shows that, with a value of 182, Royal Bafokeng scored the maximum value (182), whereas Pan Africa Resource scored the minimum value of 63. As for the percentage of each item within the category, it should be noted that the item showing the highest percentage (approximately 42%) is "risk management", with the lowest percentages belonging to "risk disclosure" (0.08%) and "risk mitigation" (0.4%).

The most important focus in the part Key Performance Indicators and Targets is obtaining an understanding of the level at which the chosen KPI meets the materiality criteria and whether the key targets linked to the sustainability strategy are described. The KPIs category has the greatest number of items; in fact, these indicators use both financial and non-financial information that can be located in different places within the companies’ reports. Thirty-six items are identified in the checklist, and if we observe the data expressed in absolute value, the total occurrences show the highest value. It is possible to note in primis that in the companies analysed, only 27 items (75%) were found in the reports. The results highlighted in the normalized frequency table are very different from the absolute values: the highest value is found for Anglo American Platinum and Harmony (426), whereas the lowest value (147) is that of Petmin Ltd. As for the incidence of single items, "performance" has the highest percentage (52.16%), whereas "intellectual capital", "measurable targets" (0.03%) and "improvement programmes" (0.07%) show the lowest percentage.

The part Remuneration covers the approach towards remuneration and how remuneration policies are aligned with the strategic objectives. The last category covers the disclosure of the board’s remuneration, and an analysis of the number of items in the checklist has shown that all of the 9 identified items appear on the table of total occurrences. The maximum normalized value is associated with BHP Billiton and the minimum with Pan African Resource. As for the incidence of each item within the category, "remuneration committee" is the item with the highest percentage (approximately 32%), whereas the lowest percentage is associated with "long term incentives". However, 100% compliance can be noted because all companies have identified all of the items on the checklist.

CONCLUSION

South Africa is one of the most important mining countries in Africa and the world. It has the world’s largest reserves of chrome, gold, vanadium, manganese and PGMs (platinum group metals) and accounts for nearly all of Africa’s metals and mineral production (Burger, 2006). According to White (1995) and Stainbank (2012), the mineral extraction and processing industry is the most dominant industry in the South African economy in that it contributes a substantial amount to its export earnings and opens employment opportunities that are crucial to South Africa’s economic and social concerns. In addition, due to their impact on the natural environment, mining companies are under close watch by environ-mental groups and society at large. There are many mining companies in emerging countries looking to Western stock exchanges to find markets for their stocks (Smith and Mokgoatlheng, 2003). Because the South African mining industry is in an emerging country, it may need to improve its non-financial disclosures to compete globally and meet the expectations of potential investors (Atkins and Maroun, 2015; Stainbank, 2012; PWC, 2013).

In South Africa, the elaboration of an integrated report has become compulsory after the recommendations included in the King Code of Governance Principles for South Africa 2009 (King III) and the definition of the listing requirements on the JSE (http://www.jse.co.za/Home.aspx). “South Africa is among the first countries in the world to require integrated reporting of listed companies. This puts way ahead of the game” Mervyng King told reporters (www.southafrica.info/news/business/143897.htm).

Companies listed on the JSE are obliged to comply with the JSE’s listing requirements, which involve compliance with the King Report III and the SRI index. A previous study of the South African mining sector (Stainbank, 2012) noted that the number of companies reporting according to the GRI increased by 20% in 2006 compared to 2004 or 2005. In addition, some companies provided the GRI disclosure index for their non-financial reporting, which made it easy to follow the extent of their non-financial disclosures. As a consequence, non-financial information is affected by compliance with mandatory regulations, even if the pressure exerted by the stakeholders urges companies to further increase the amount of information, particularly with regard to the human capital. Therefore, issues such as human rights and health and safety have become a priority to enhance the contribution exerted by the sector with a view to sustainable development in the areas of emerging economies (ICMM, 2006; ICMM, 2012).

Given these premises, the empirical research conducted on the basis of the checklist displayed in Table 2 showed some interesting results in terms of disclosures relating to the items in the nine semantic categories listed above. In brief, the textual analysis showed the following results:

1) The semantic categories that display the greatest compliance by companies are n. 4 Strategy Vision Values, n. 5 Governance Structures, n. 6 The Stakeholders, n. 7 Material Risks and Opportunities and n. 9 Remuneration. Many items in category n. 8, Key Performance Indicators and Targets, were not detected.

2) For each category, it is not possible to find total homogeneity in absolute occurrences and normalized frequencies because the maximum and minimum values are quite different. Existing differences in the individual words are partially due to the type of item selected. In fact, in certain cases, the most general items had higher values than more specific words or expressions. The boxplots (Graph 2) show homogenous behaviours for certain groups of companies in relation to certain semantic categories: examining the width of the boxes and the length of the "flakes" - "Mustache", we could say that KIP Targets are isolated with a high variability, Strategy Vision and Values Governance Structure has an average variability, Group Profile, Material Risks and Opportunities Remuneration have a moderate variability and, finally, Scope Boundary, Key Features and Stakeholders have a low variability.

3) Checking the degree of compliance on the part of the sample companies leads to the analysis of the number of items found in the documents with respect to the item totals in relation to the individual companies. The assessment of each company makes it possible to perform a comparative evaluation in overall terms. The results show that on average, the degree of compliance with the disclosure checklist (Tables 2 and 9) is approximately 55.92%, and the best results are achieved by the company Anglo American Platinum (66.97%), while the company with the lowest value is Coal of Africa (39.45%) (Table 9).

Overall, the empirical findings do not indicate homogeneous behaviour among companies; nevertheless, it can be noted that the higher incidence of the issues set forth above may be due to the correspondence with some areas noted in the criteria themes of SRI index. For example, category n. 6 Stakeholders may be associated with the topic “Society”, category n. 4 Strategy vision values with “policies and strategies”, and category n. 5 Governance Structures with “governance and related sustainability concerns”. Compliance with the essential requirements for ESG set by JSE for the SRI index may have exercised some influence (JSE and EIRIS, 2010).

The items related to environmental disclosures found in category n. 7 - such as sustainability review, environmental performance and sustainability performance - did not display significant values, and others, such as ESG indicators and ESG performance, were not detected. This seems to contradict the strong pressure exerted by various stakeholders and society in general about the growth of disclosures concerning the environment. In particular, the SRI index requires special attention to the issue of climate change with the intention of leading companies to consider what risks they face due to the anticipated effects of climate change, and how they are managing and reporting on their efforts to reduce carbon emissions (JSE, 2010).

Further clarification about the items related to the disclosure CI is needed. In this case, the information is rather lacking: for example, the item intellectual capital (category n. 7) was not found in the documents analysed. This confirms the results of a previous survey of 75 companies carried out in South Africa (Firer and Williams, 2003), which indicated that the association between the efficiency of value added by a firm’s major resource components (physical capital, human capital and relational capital) and the three traditional dimensions of corporate performance (profitability, productivity and market value) is limited and mixed. Consequently, the empirical findings of this study state that despite the efforts to improve its intellectual capital base, the business environment and market in South Africa still appear to place greater weight on corporate performance based on physical capital assets. This aspect also arises from another study (April et al., 2003) whose empirical results show that mining companies tend to report on fewer intellectual capital attributes than other companies.

In addition, results show that mining companies rate intellectual capital highly, but appear to be lacking in its measurement and reporting.

This research does not provide an optimistic view of the implementation of IR in its early stage because the results exhibit a wide range of diversity in the type and quantity of information reported. This finding confirms that the lack of a precise framework and IR standards produce a high diversity of IR practices (Wild and van Staden, 2014) in spite of the mandatory listing requirements in South Africa. This suggests that the first adopters are unable to achieve the IIRC aims and cannot produce concise, consistent and comparable reports. The findings show a high heterogeneity among corporate reports produced by companies.

This appears to be worrying in view of the need of enhancing disclosures linked to human capital, in particular, given the high frequency of accidents at work, which have a strong impact on reputation and corporate image. This item can also be considered a part of the social disclosure as a peculiarity of the mining sector, as mining activities generate significant social concerns in terms of their environmental impact and employees’ health and safety (Deegan and Rankin, 1996; Cho, 2009; Coetzee and van Staden, 2011). Davies et al. (2002) indicate that South Africa mining industry’s employees are extremely vulnerable to HIV/AIDS because they generally come from remote areas and are far away from their families. Hence, the effects of this disease on the labour force may cause a considerable impact on the South African economy.

As is generally known, the use of content analysis to measure non-financial information disclosure as an end in itself (references) and as an input in statistical regression studies to investigate the determinants of non-financial disclosures is increasing in similar studies (Kang and Gray, 2011). Consequently, further research could help to identify the potential reasons behind companies’ non-financial disclosures and practices. The determinants that influence disclosure and compliance are the firm’s size and its trends in share price and performance. Finally, this study shows certain limits. The analysed period is restricted to one year; consequently, we did not evaluate the temporal trend of potential improvements of non-financial information disclosures, and it might be interesting to perform a longitudinal analysis. Another caveat of this paper is the lack of comparative analysis by means of the assessment of other industries in the South African economy.

CONFLICT OF INTERESTS

The authors have not declared any conflict of interests.

REFERENCES

|

Abdo A, Fisher G (2007). The impact of reported corporate governance disclosure on the financial performance of companies listed on the JSE. Invest. Anal. J. 66:43-56. |

|

|

Abeysekera I (2008). Intellectual capital disclosure trends: Singapore and Sri Lanka. J. Intellect. Capital 9(4):723-737. |

|

|

Abeysekera I. (2013). A template for integrated reporting. J. Intellect. Capital 14(2):227-245. |

|

|

ACCA and Eurosif (2013). What do investors expect from non-financial reporting? Available at www.accaglobal.com Last access 30 August 2015. |

|

|

Adams S, Fries J, Simnett R (2011). The journey toward integrated reporting, Accountants Digest (ICAEW), Wolters Kluwer: UK. |

|

|

ADVFN (2007). Johannesburg Stock Exchange (JSE), available at View. Last access 28 August 2012. |

|

|

Aerts W, Cormier D (2009). Media legitimacy and corporate environmental communication. Account Org Soc. 34(1):1-27. |

|

|

Alrazi B, de Villiers C, van Staden CJ (2015). A comprehensive literature review on and the construction of a framework for, environmental legitimacy, accountability and proactivity. J. Clean Prod. 102:44-57. |

|

|

Antonites E, de Villiers CJ (2003). Trends in South Africa corporate environmental reporting: A research note. Meditari Account. Res. 11(1):1.10. |

|

|

April KA, Bosma P, Deglon DA (2003). IC measurement and reporting establishing a practice in SA mining. J. Intellect. Capital 4(2):165-180. |

|

|

Atkins J, Maroun W (2015). Integrated reporting in South Africa in 2012: perspectives from South African institutional investors. Meditari Account. Res. 23(2):197-221 |

|

|

Beattie V (2000). The future of corporate reporting: A review article. Irish Account. Rev. 7(1):1-36. |

|

|

Beattie V, McInnes B, Fearnley S (2004). Through the eyes of management: narrative reporting through three sectors, Institute of Chartered Accountants in England and Wales: London. |

|

|

Beattie V, Pratt K (2003). Issues concerning web-based business reporting: An analysis of the views of interested parties. Brit. Account. Rev. 36(2):155-187. |

|

|

Beattie V, Thomson SJ (2007). Lifting the lid on the use of content analysis to investigate intellectual capital disclosure. Account. Forum 31:129-163. |

|

|

Bolasco S (2010a). Taltac2.10 Sviluppi, esperienze ed elementi essenziali di analisi automatica dei testi (Taltac2.10, experiences and essential topics of automatic analysis of texts), LED:Milan. |

|

|

Bolasco S (2010b). Analisi Multidimensionale dei dati. Metodi, strategie e criteri di interpretazione (Multidimensional analysis. Methods, strategies and criteria of comprehension), Carrocci:Rome, 4th edition. |

|

|

Bolasco S, Canzonetti A, Capo F (2005). Text Mining – Uno strumento strategico per imprese e istituzioni (Text Mining – A strategic tool for companies and institutions). Cisu Editor:Rome. |

|

|

Bollen A (2004). The rise and rise of non financial reporting: How to use research to measure your reputation. London MORI, |

|

|

Borkowski SC, Welsh MJ, Wentzel K (2012). Sustainability reporting at Johnson & Johnson: A case study using content analysis. Int. J. Bus. Insight Transform. 4:96-105. |

|

|

Boyatzis ME (1998). Transforming qualitative information. Thematic Analysis and Code Development, Sage, Case Western Reserve University: Cleveland USA. |

|

|

Burritt RL (1997). Corporate environmental performance indicators: Cost allocation-boon or bane? Greener Manage. Int. 17:89-100. |

|

|

Busco C, Frigo ML, Quattrone P, Riccaboni A (2013). Redefining Corporate Accountability through Integrated Reporting. What happens when values and value creation meet? Strat. Finan. August. pp. 33-41. |

|

|

Carels C, Maroun W, Padia N (2013). Integrated reporting in the South African mining sector. Corporate Ownersh. Control 11:991-1005. |

|

|

Chauvey JN, Giordano-Spring S, Cho C, Patten DM (2013). The normativity and legitimacy of the CSR disclosure. Evidence from France. Working paper 36th European Accounting Association Congress, Tallinn, April. |

|

|

Cho CH (2009). Legitimation strategies used in response to environmental disaster. A French case study of Total SA's Erika and AZF incidents. Eur. Account Rev. 18(1):33-62. |

|

|

Churet C, Eccles RG (2014). Integrated Reporting, Quality of Management and Financial Performance. J. Appl. Corporate Finan. 26(1):56-64. |

|

|

Coetzee CM, van Staden CJ (2011). Disclosures responses to mining accidents: South African evidence. Account. Forum 35:232-246. |

|

|

Coram P, Monroe GS, Woodliff D (2009). The value assurance on voluntary nonfinancial disclosure. An experimental analysis. Audit. J Pract. Theory 28(1):137-152. |

|

|

CorporateRegister.com., (2013). CR Perspectives 2013. Global CR Reporting Trends and Stakeholders. |

|

|

Davies JR, de Bruin DG, Deysel M, Strydom M (2002). The SA mining industry enters the HIV/AIDS war zone. Meditari Accountancy Res. 10:25-51. |

|

|

De Klerk M, De Villiers C (2012). The value relevance of corporate responsibility reporting: South African evidence. Meditari Accountancy Res. 20(1):21-38. |

|

|

De Villiers CJ (1999). Corporate social reporting in South Africa: signs of a pygmy awakening? Soc. Environ. Account. 19(2):5-7. |

|

|

De Villiers CJ, Alexander D (2014). The institutionalization of corporate social responsibility reporting. Brit. Account. Rev. 46:198-212. |

|

|

De Villiers CJ, Barnard P (2000). Environmental reporting in South Africa from 1994 to 1999: A research note. Meditari Accountancy Res. 8:15-23. |

|

|

De Villiers CJ, Low M, Samkin G (2014). The institutionalization of mining company sustainability disclosures. J. Clean Prod. 84:51-58. |

|

|

De Villiers CJ, Lubbe JC (2001). Industry differences in respect of corporate environmental reporting in South Africa: A research note. Meditari Accountancy Res. 9(1):81-91. |

|

|

De Villiers CJ, Van Staden (2006). Can less environmental information be legitimising? Evidence from Africa. Account Org. Soc. 31(8):763-781. |

|

|

Deegan C, Rankin N, Voght P (2000). Firm's disclosure reactions to major social incidents: Australian evidence. Account. Forum 24(1):101-130. |

|

|

Deegan C, Rankin R (1996). Do Australian companies report environmental news objectively? An analysis of environmental disclosures by firms prosecuted successfully by the environmental authority. Account. Audit. Accountabil. J. 9(2):50-67. |

|

|

Deloitte (2011). Integrated Reporting – A better view?, 2011, Deloitte Global Service Limited. Available at View, Last access 30 August 2015. |

|

|

Deloitte (2012). Integrated Reporting Navigating your way to a truly Integrated Report, Issue 3, The future for corporate reports, February, available at View, Last access 30 August 2015. |

|

|

Dumay J, Cai L (2015). Using content analysis as a research methodology for investigating intellectual capital disclosure: A critique, J. Intellect. Capital 16(1):121-155. |

|

|

Eccles RG, Armbrester K (2011). Integrated Reporting in the Cloud, First Quarter 2011, 8:13-20. |

|

|

Eccles RG, Krzus MP (2010). One Report: Integrated Reporting for a Sustainable Strategy, John Wiley & Sons:New York. |

|

|

Eccles RG, Krzus MP (2014). The Integrated Reporting Movement: Meaning, Momentum, Motives, and Materiality. John Wiley & Sons:New York. |

|

|

FEE (Fédération des Experts comptables Européens) (2008). Discussion Paper, Sustainability Information in Annual Reports. Building on Implementation of the Modernisation Directive, available at |

|

|

Firer SS, Williams SM (2003). Intellectual capital and traditional measures of corporate performance. J. Intellect. Capital 4(3):348-360. |

|

|

Fonseca A, McAllister ML, Fitzpatrick P (2014). Sustainability reporting among mining corporations: A Constructive Critique of the GRI Approach J. Clean Prod. 84:70-83. |

|

|

Frik C (2002). Direct foreign investment and the environment: African mining sector, OECD Global Forum on International Investment and the Environment, Lessons to be learned from the Mining Sector, 7-8 February. |

|

|

Gazdar K (2007). Reporting non-financials. John Wiley & Sons:England. |

|

|

Global Reporting Initiative (GRI) G3 (2010), Sustainability Reporting Guidelines, Amsterdam, Available at www.globalreporting.org Last access 30 August 2015. |

|

|

Goh PC, Lim KP (2004). Disclosing intellectual capital in company annual reports: Evidence from Malaysia. J. Intellect. Capital 5(3):500-510. |

|

|

Gray R, Adams CA, Owen D (2014). Accountability, Corporate Responsibility and Sustainability: Accounting for Society and the Environment, Pearson: UK. |

|

|

Gray R, Kouhy R, Lavers S (1995). Constructing a research database of social and environmental reporting by UK companies. Account. Audit. Accountabil. J. 8(2):78-101. |

|

|

GRI (2001) Sustainability Reporting Guidelines & Mining and Metals Sector Supplement version 3.0, available at www.globalreporting.org Last access 30 August 2015. |

|

|

Guenther E, Hoppe H, Poser C (2007). Environmental Corporate Social Responsibility of Firms in the Mining and Oil and Gas Industries: Current Status Quo of Reporting Following GRI Guidelines, Greener Manage. Int. 53:7-25. |

|

|

Gumb B, Noël C (2009). CEO's Reports about Internal Control: A Content Analysis. Account. Eur. 6(1):81-106. |

|

|

Guthrie J, Abeysekera I (2006). Content analysis of social and environmental: What's new." J. Hum. Resour. Costing Account. 10(2):114-126. |

|

|

Hayes AF, Krippendorff K (2007). Answering the call for a standard reliability measure for coding data. Commun. Meth. Meas. 1:77-89. |

|

|

Hindley T, Buys TW (2012). Integrated Reporting Compliance With The Global Reporting Initiative Framework: An Analysis of The South African Mining Industry. Int. Bus. Econ. Res. J. 11(11):1249-1260. |

|

|

Hopwood A, Unerman J, Fries J (2010). Accounting for sustainability. Practical Insights, Earthscan: London. |

|

|

Iannou I, Serafeim G (2014). The Consequences of Mandatory Corporate Sustainability Reporting: Evidence from four countries, Work. Pap. 11-100:1-35. |

|

|

ICMM International Council of Mining & Metals (2006). International Council on Mining & Metals, available at http://www.icmm.com/ Last access 28 August 2012 |

|

|

ICMM - International Council of Mining and Metals (2012). Trends in the mining and metals industry, available at View Last Access 30 August 2015. |

|

|

IIRC - International Integrated Reporting Council (2011). Towards Integrated Reporting - Communicating Value in the 21st Century, Discussion Paper September 2011. |

|

|

IIRC (2013a). International Integrated Reporting Council (December 2013), The International <IR> Framework available at View Last access 30 August 2015. |

|

|

IIRC (2013b). International Integrated Reporting Council (December 2013). Basis for conclusions - The International <IR> Framework available at View Last access 30 August 2015. |

|

|

IRC (Integrated Reporting Committee) (2012). South Africa, Discussion Paper 25 January 2010, available at View. Last access 30 October 2012. |

|

|

Islam MA, Deegan C (2008). Motivations for an organization within a developing country to report social responsibility information: Evidence from Bangladesh. Accounting Audit. Accountabil. J. 21:850-874. |

|

|

Jenkins H, Yakovleva N (2006). Corporate social responsibility in the mining industry: Exploring trends in social and environmental disclosure. J. Clean Prod. 14:271-284. |

|

|

JSE and EIRIS, (2010). JSE SRI Index background and selection criteria 2010, South Africa, JSE and EIRIS. |

|

|

Kang H, Gray S (2011). The content of voluntary intangible assets disclosures. Evidence from emerging market companies. Int. J. Account. 46(4):402-423. |

|

|

Kemp D, Bond CJ, Franks DM, Cote C (2010). Mining water and human rights: Making the connection. J. Clean Prod. 18(15):1553-1562. |

|

|

King III (2009). Integrated Reporting – Sustainability Reporting No Longer a Poor Cousin to the Financial Numbers. |

|

|

King M, Roberts L (2013). Integrate: Doing business in the 21st Century, September, Juta & Company Ltd: Cape Town. |

|

|

KPMG (2006). Global mining reporting survey. Energy and natural resources, available at. View Last access 30 August 2015. |

|

|

KPMG (2011a). Integrated Reporting Performance insight through Better Business Reporting, Issue 1, available at View, Last Access 30 August 2015. |

|

|

KPMG (2011b). International Survey of Corporate Responsibility Reporting 2011. |

|

|

Krippendorff K (1980). Content Analysis; An Introduction to its Methodology, CA: Sage Beverly Hills. |

|

|

Krippendorff KH, Bock MA (eds.) (2009). The Content Analysis Reader, CA: Sage: Thousand Oaks. |

|

|

Kumah A (2006). Sustainability and gold mining in the developing world. J. Clean Prod. 14(3-4):315-323. |

|

|

Lebart L, Salem A (1994). Statistique Textuelle (Textual Statistics) Dunod:Paris. |

|

|

Leuner JB (2012). Integrated reporting takes hold. Communication World 3-4:33-35. |

|

|

Lodhia S, Hess N (2014). Sustainability accounting and reporting in the mining industry: Current literature and directions for future research. J. Clean Prod. 84:43-50. |

|

|

Lodhia S, Martin N (2014). Corporate Sustainability Indicators: An Australian Mining Perspective. J. Clean Prod. 84:107-115. |

|

|

Maffini GC., Kneipp JM, Kruglianskas I, Barbieri da Rosa LA, Schoproni BR (2015). Management for sustainability: An analysis of the key practices according to the business size. Ecol. Indic. 52:116-127. |

|

|

Mangena M, Tauringana V (2007). Disclosure, Corporate Governance and Foreign Share Ownership on the Zimbabwe Stock Exchange. J. Int. Financ. Manage. Account. 18(2):53-85. |

|

|

Maubane P, Prinsloo A, Rooyen NV (2014). Sustainability reporting patterns of companies listed on the Johannesburg securities exchange. Public Relat. Rev. 40(2):153-160. |

|

|

Milne MJ, Adler RW (1999). Exploring the reliability of social and environmental disclosures content analysis. Account. Audit. Accountabil. J. 12(2):237-256. |

|

|

National Treasury (2010). Available at View, Last access 30 August 2015. |

|

|

Newson M, Deegan C (2002). Global Expectations and their Association with Corporate Social Disclosure Practices in Australia, Singapore and South Korea. Int. J. Account. 37(2):183-213. |

|

|

Palenberg M, Reinicke W, Witte JM (2006). Trends in non-financial reporting, November 2006. Paper prepared for the United Nations Environment Programme, Division of Technology, Industry and Economics, Global Public Policy Institute available at www.gppi.net Last access 30 August 2015. |

|

|

Pellegrino C, Lodhia S (2012). Climate change accounting and the Australian mining industry: Exploring the links between corporate disclosure and the generation of legitimacy. J. Clean Prod. 26:68-82. |

|

|

Porter ME, Kramer MR (2011). Creating Shared Value. Harvard Bus. Rev. 89(1-2):62-77. |

|

|

Price Waterhouse Coopers (2010). Steering Point Integrated Reporting; Integrated Reporting – What does your reporting say about you? Harvard Business School Faculty Research Symposium May 20. |

|

|

Price waterhousecoopers (2013). Extractive value. What do investment professionals need from mining company reporting? September 2013, available at www.pwc.co.uk/mining Last access 30 August 2015. |

|

|

Raemaekers K, Maroun W, Padia N (2016). Risk disclosures by South African listed companies post-King III. S. Afr. J. Account. Res. 30(1):41-60. |

|

|

Rensburg R, Botha E (2014). Is Integrated Reporting the silver bullet of financial communications? A stakeholders perspective from South Africa. Public Relat. Rev. 40:144-152. |

|

|

Robb SWG, Single LE, Zarzeski MT (2001). Non financial disclosures across Anglo American countries. J. Account. Audit. Taxation 10:71-83. |

|

|

Rossouw R (2010). King III Integrated Report – Why it's crucial to plan ahead. Board Room 3:537-538. |

|

|

Setia N, Abhayawansa S, Joshi M, Huynh AV (2015). Integrated reporting in South Africa: Some initial evidence. Sustain. Account. Manage. Policy J. 6(3):397-424. |

|

|

Singleton-Green B (2010). Commentary: Is the Reporting Model Broken? Austral. Account. Rev. 20(4):409-410. |

|

|

Stainbank LJ (2012). The nature and extent of non-financial disclosures in the South African mining industry. Conference Proceedings Faculty of Ljubljana 35th Annual Congress European Accounting Association EAA, Ljubljana, May 9-11. |

|

|

Striukova L, Unerman J, Guthrie J (2008). Corporate reporting of intellectual capital: Evidence from UK companies. Br. Account. Rev. 40:297-313. |

|

|

Sullivan D (2001). Document Warehousing and Text Mining: Techniques for Improving Business Operations, Marketing, and Sales John Wiley & Sons, Inc.: New York. |

|

|

Tawiah KA, Dartey-Baah KD (2005). Corporate Social Responsibility in Ghana International Journal of Business and Social Sciences, Special Issue on Contemporary Issues in Business Studies, 2(17):107-122. |

|

|

The Institute of Directors in Southern Africa (IoDSA) (2009). King Report on Governance for South Africa and King Code of Governance Principles (King III) available at View. Last access 28 August 2015. |

|

|

Unerman J (2000). Methodological issues: reflections on quantification in corporate social reporting content analysis. Account. Audit. Accountabil. J. 13(5):667-680. |

|

|

Van Staden CJ (2003). The relevance of theories of political economy to the understanding of financial reporting in South Africa: The case of value added statements. Account. Forum 27(2):224-246. |

|

|

Vanstraelen A, Zarzeski MT, Robb SWG (2003). Corporate nonfinancial disclosure practices and financial analyst forecast ability across three European countries. J. Intl. Financ. Manage. Account. 14(3):249-278. |

|

|

Warhurst A (1998). Corporate social responsibility and the mining industry, Presentation at Euromines, Mining and Environmental Research Network (MERN), June 4th, Brussels. |

|

|

Weber RP (1990). Basic Content Analysis, Sage Publications: Newburry Park, CA. |

|

|

White AL (2005). New wine, new bottles: The rise of Non-Financial reporting, A Business Brief by Business for Social Responsibility. June, available from View. Last access 28 August 2015. |

|

|

Wild S, van Staden C (2015). The Development of Integrated Reporting: A Paradigm of Regulatory Capture? Paper presented at the ATINER 13th Annual International Conference on Accounting, 23-25 May 2015, Athens, Greece. |

|

|

Yakovleva N, Vazquez-Brust D (2012). Stakeholders perspectives on CSR of Mining MNCs in Argentina. J. Bus. Ethics 106(2):191-211. |

|

|

Yongvanich K, Guthrie J (2005). Extended performance reporting: an examination of the Australian mining industry. Account. Forum 29:103-119. |

|

|

Zambon S (2011). The managerialisation of Financial Reporting: An introduction to a destabilizing accounting change. Financ. Rep. Spec. Iss.: pp. 5-16. |

|

|

Zanasi A (2005). Text Mining and its applications to intelligence, CRM and knowledge management Southampton: WIT Press. |

|

APPENDIX

Copyright © 2024 Author(s) retain the copyright of this article.

This article is published under the terms of the Creative Commons Attribution License 4.0