ABSTRACT

The main aim of this study was to examine the extent to which internal control practices affected health service delivery in Rukungiri District. The research adopted a case study design using both quantitative and qualitative approaches. The target population was 140 key stakeholders that lived and worked in Rukungiri District and a sample size of 104 was drawn from the target population. Our findings from the descriptive statistics, interviews conducted from key stakeholders and documentary reviews revealed a positive and significant relationship between internal control practices and health service delivery in Rukingiri District. The regression analysis results also indicated a modest model fit with adjusted r square of 0.137 which implies that about 14% variation in health service delivery was predictable by internal control practices, while the remaining 86% is explainable by other factors.

Key words: Internal control practices, health services, Local government.

Internal control systems in organizations have existed since ancient times; for instance, in Hellenistic Egypt Internal control were manifested in a dual administration, with one set of bureaucrats charged with collecting taxes and another with supervising them (Lee, 1971). The effectiveness of internal controls helps to enhance the desired health service quality in local in local government (Gordon and Abbey, 2019). Therefore organizations that implement internal controls tend to have improved performance in health service delivery and are they are likely to meet stakeholders’ expectations. According to the 1995 Constitution of the Republic of Uganda (Republic of Uganda Constitution, 1995), the government has an obligation to provide basic health services to its people while promoting good nutrition and healthy lifestyles. It further provides for all people in Uganda to enjoy equal rights and opportunities, have access to health services, clean and safe water and education. The National Health policy, calls for sustainable development, management and use of national financial resources, to provide better health services.

Uganda fully embraced internal control processes with the formulation the Public Finance Management Act (cap. 115) that provides for the control and management of the public finances of Uganda, audit and examination of public accounts and the accounts of statutory bodies and sectors, including health services. Additionally, the Uganda Public Finance Management Act (2015) provides for the development of an economic fiscal policy frame work to regulate the financial management of the government funds, prescribe responsibilities of persons entrusted with government financial management in the government and internal audit. To understand the internal control procedures, we refer to the five components of COSO (2013), namely: control environment, risk assessment, control activities, information and communication and monitoring. These components work to establish the foundation for sound internal control within the organization through directed leadership, shared values and a culture that emphasizes accountability for control (COSO, 2013). Rukungiri District adopted internal control practices as guided by the Uganda Public Finance Management Act which include financial controls, financial accountability and Monitoring and evaluation controls (Rukungiri District Development Plan, 2015). Minimum health care packages were developed to improve health service delivery and access to health services improved through construction and upgrading of primary health care centers, increased immunization coverage, distribution of insecticide-treated nets and antimalarial drugs, expansion of HIV awareness.

Despite the adoption of internal control practices as mentioned above, the health service delivery in the district was yet to fully realize the desired results. The Rukungiri District Internal Audit Report (2015) indicated persistent drug stock outs, no medical doctors, absence of reliable medical equipment, and poor houses for medical staff with poor housing conditions characterized by leaking roofs for newly constructed houses. The health worker inventory showed that the district has 256 health workers with three doctors in government health centers that were absent much of the time. The District Analysis Report (2016) indicated that these problems were persistent. The study attempted to examine the above gaps by analyzing the extent to which internal control practices affected health service delivery in the district.

The outcomes would help stakeholders to understand the nature and weakness in internal control practices at the district and how they affect health service delivery and how to strengthen them so as to improve on health delivery. Our recommendations will thus help the government regulators and other researchers to carry out other investigations in area of internal control practices and their linkage to health service delivery which currently has limited literature on similar studies within the region, hence the study outcomes will be an addition to the extant literature.

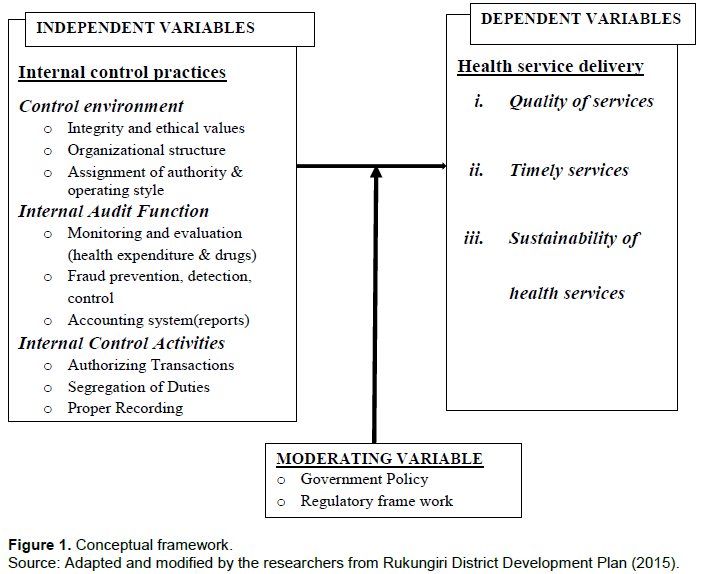

Conceptual frame work

As indicated in the conceptual framework (Figure 1), this study adopted internal control practices as independent variable (represented by control environment, internal audit function and internal control activities) in health service delivery. The dependent variable was represented by health service delivery identified through quality of service, timely service, and sustainability. Government policy conceptualized as regulatory framework was adopted as the moderating variable. The conceptual framework was used to hypothesize relationship between internal control practices and health service delivery. The relationship between the independent variable and the dependent variable was explained by the direction of the arrow. The moderating variable has strong contingent effect on the independent – dependent variable relationship (Sekaran, 2000). The researchers adopted government policy and regulation as moderating variables.

We adopted a case study design which is known to provide an in-depth investigation of an individual, group, institution and make detailed examination of a single subject (Mugenda and Mugenda, 1999). The researchers used the case study to make an intensive investigation on how internal controls affect health service delivery at individual unit, group and entire community. Both quantitative and qualitative approaches were used to achieve a high degree of validity and reliability of results. This study was conducted in Rukungiri District, located in Kigezi sub-region, Southwestern Uganda. It shares boundaries with Kasese and Mitooma in the north, Ntungamo in the East, Kabale in the South and Kanungu in the west. It is composed of two counties and one municipality. Note that for this study, the researchers concentrated on two counties of Rujumbura and Rubabo County – Rukungiri District. It has an area of 1524.3 Km2.The district population stands at 321,300 according to UBOS Census estimates 2014. The District is remote, about 400km from Kampala the capital city of Uganda with limited oversight from accountability functions like office of the auditor general thus making it a good choice for a study on internal controls.

Study population and sampling

According to Rukungiri district development plan 2015/16-2019/20, the district had 53 governmental and 36 non-government organizations (NGOs) managed health centers, which are evenly distributed within all the sub counties in the district. For this study five health centers with a target a target population of 140 people comprising of individuals who implement internal control practices at the district level such as the Chief administrative officer (CAO), chief Finance officer (CFO), Chairperson Local Council five (LCV), Heads of district departments, district Councilors, health staff and community. Out of total population of 140, a sample size was 104 was adopted based on Krejcie and Morgan sample size table (1970). Our sampling procedures included probability and non-probability sampling with the use of simple random and purposive sampling techniques. This was advantageous because the researchers relied on the respondents that were critical to the research. Purposive sampling was used for the groups with limited numbers of possible respondents since all the groups were seen to have all the required information (Mugenda and Mugenda, 1999). Simple random sampling gave a chance to all respondents to be picked. The sampling frame included district top management, district administration staff, district gov’t health staff, sub-county officials and councilors, NGO health workers and community health beneficiaries (users). The sample size was determined using the Krejcie and Morgan sample size table (1970). The sample size table was preferred to other techniques due to its simplicity in use, as the only information normally required when using the table is the size of the population (Sekaran and Bougie, 2016). The sample size for this study was determined as 104; and according to Amin (2005), a sample size above 30 is generally enough.

Data collection, quality control and analysis

We adopted both primary and secondary data using questionnaire survey and interview methods administered with key stakeholders. Structured questionnaire guide was used to collect factual quantitative data; interview guide was used to collect in-depth qualitative to supplement questionnaires. We also carried out a review of electronic journals, research dissertations, reports, articles and presentations made on internal control practices, MandE reports, budget performance reports and health performance reports. The questionnaire views from the respondents were solicited using five Likert-point scale where: 5 means Strongly Agree; 4, Agree; 3, Neutral; 2, Disagree; and 1, Strongly Disagree.

Validity as the accuracy and meaningfulness of inferences, which are based on research results (Sekaran, 2000). We conducted a repeated review of the instrument by carrying out a field pre-test where the questionnaires that were given to experts in area of internal control practices to assess its content validity. Validity was established through a validity test using content validity index (CVI), which measures the degree to which data collected using a particular instrument represents a specific domain of indicators or content of a particular concept. The content validity index (CVI) is also an indication of the degree to which the instrument corresponds to the concept it is designed to measure. According to Amin (2005) the formula for establishing the CVI is given as:

To be accepted, the variables should have a CVI of above 0.70 or 70% as the recommended value for the instruments to be considered relevant (Amin 2005, p.286). The instruments for this study were valid to be used because it had an average C.V.I of 92%. This was computed using the SPSS Version 20.

Amin (2005) asserts that reliability of an instrument is the consistence with which it measures what it is intended to measure. Carmines and Zeller (1979) opine that reliability concerns the extent to which an experiment, test, or any meaningful procedure yields the same results on repeated trials. The reliability of the instrument was tested using Cronbach’s alpha test in the range between 0.5-1, using statistical packages. If the reliability falls in the range of 0.5-1, it would be considered reliable, but below 0.5 there will be need to improve instruments (Amin, 2005). The Cronbach’s Alpha reliability coefficient was calculated by running a statistical test using Statistical Package for Social Scientists (SPSS) version 20.

The questionnaire was given to technical staff and then re-administered after 5 days and the scores were evaluated and correlated. According to Amin (2005), all the measurements in the instrument that show adequate levels of internal consistency of Cronbach’s alpha of 0.7 and above are accepted as reliable. For this study the instruments were consistent and reliable at an average Cronbach’s Alpha reliability coefficient of 0. 8. The analysis entailed computations, descriptive and relational statistics like correlation and regression analysis, through which relationships supporting or conflicting with the hypotheses were subjected to statistical tests to determine the extent to which data indicated any conclusions.

To analyze the data gathered, responses from the administered questionnaires were first compiled. Out of sample of 104, a total of 103 returned the questionnaires representing a response rate of 99.04% which is above the 70% threshold of good response in descriptive studies (Mugenda and Mugenda, 2003). Our findings on the influence of internal control practices on health service delivery in Rukungiri District are presented and discussed.

Control environment and health service delivery

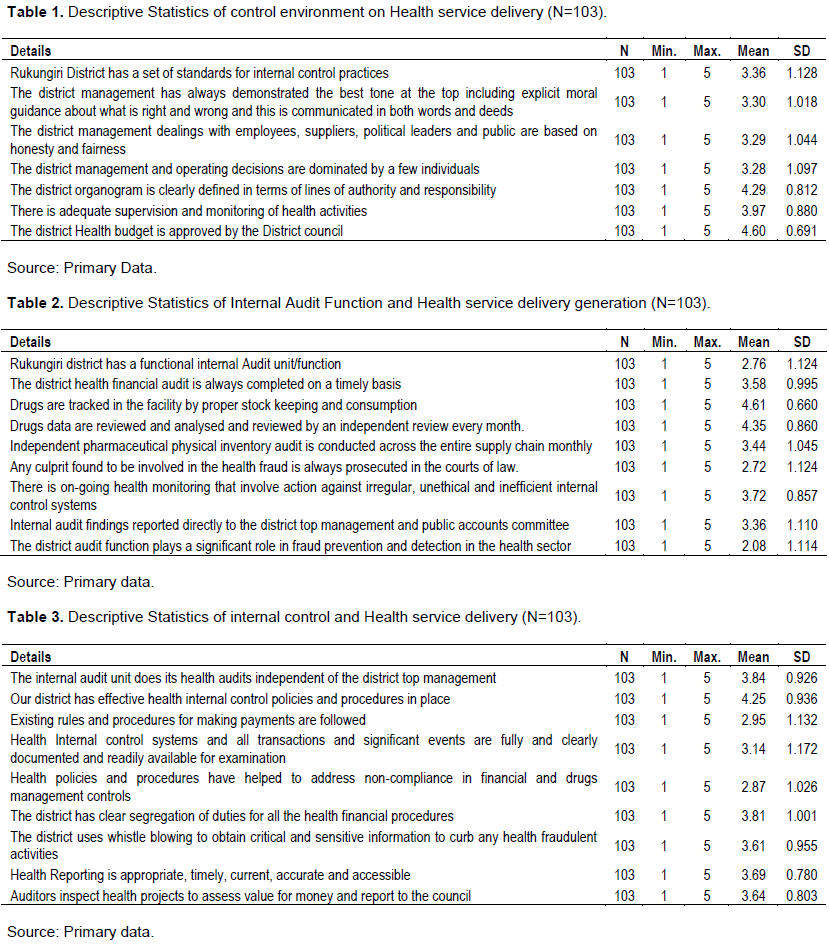

Control environment in this study was conceptualized as integrity and ethical values, organizational structure and assignment of authority and operating style. The responses from respondents are summarized in Table 1. The study found out that on all the questions above, the calculated mean was above 3, which indicated that most of the respondents were in agreement with the statements. This was further supported during the interviews as one respondent, the Buhunga sub county chief said, ‘as a district we have various strong internal control practices”. The results from the District Development Plan documentary of 2015 – 2020 review showed that Rukungiri district has strong internal control practices from the LCI to the top district level. However, the district annual health analytical report 2016 reviewed at the district showed many gaps in supervision health facilities by citing the transportation challenges and inadequate facilitation of health monitoring team.

Internal audit function and health service delivery

Internal audit function in this study was conceptualized as Monitoring and evaluation (health expenditure and drugs), Fraud prevention, detection and control as well as Accounting system (reports) as shown in Table 2. The study found out that on the question of whether “Rukungiri district has a functional internal Audit unit/function”, 31.1% of the respondents were in agreement, 24.3% were not sure, while 44.6% disagreed with the statement. A mean of 2.76 and SD of 1.124 were calculated, which implied that most of respondents disagreed with the statement since mean calculated is below 3. This implies that Rukungiri district does not have a well-functioning internal audit unit. This was further supported by Fact Sheet for Anti-Corruption Report (2015), on a research undertaken in Uganda on the link between internal audit function and health outcomes, which demonstrated the negative implications of financial leakages in local governments. On the question “The district audit function plays a significant role in fraud prevention and detection in the health sector”, a mean of 2.08 and SD of 1.114 were calculated which indicated that most of respondents were not in agreement with the statement since mean calculated is below 3. This implies that the district audit function doesn’t play a significant role in fraud prevention and detection in the health sector.

On the whole, the study revealed that some of the respondents were in agreement that health financial audits were done, drugs tracking and store keeping with independent reviews as well as monitoring against irregular, unethical and inefficient internal control practices. However, for some questionnaires and interviews, it was found that the district does not have a well functional internal Audit unit because it does not play a significant role in fraud prevention and detection; culprits in health fraud are always set free for political reasons and are not heavily charged. This was supported by Ministry of Health Report (2015) that delivery of better health services was in one-way or another affected by a weak internal audit unit or function.

Internal control activities and health service delivery

Internal control activities in this study were conceptualized as authorization of transactions, segregation of duties, proper recording and independent checks (Table 3). Except for health question of whether “Health policies and procedures have helped to address non-compliance in financial and drugs management controls” where the calculated mean was 2.87, all the other responses to the questions had calculated mean above 3. This indicated that majority most of the respondents answered in affirmative of internal control activities in Rukungiri District.

Moderating effect of government policy

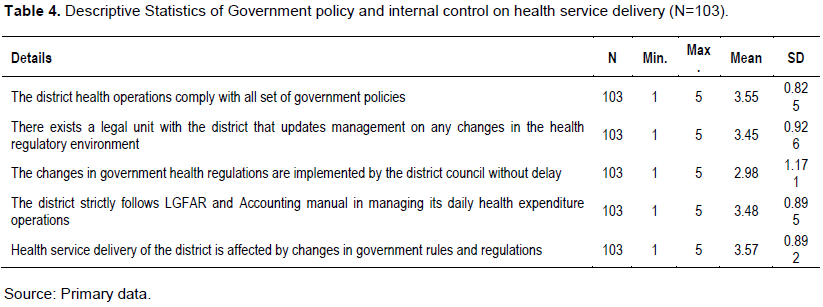

The moderating variable was conceptualized to include the regulatory framework and the responses from respondents are presented in Table 4. The study found out that nearly in all the questions above, the calculated mean was above 3, indicating that most of the respondents were in agreement. For the question of whether “The changes in government health regulations are implemented by the district council without delay”, where mean of 2.98 and SD of 1.171 were calculated indicating that respondents were not in agreement with the statement since mean calculated was slightly below 3. However, Byarugaba et al. (2014) said that despite the elaborate government policy for health sector in local governments in Uganda, Rukungiri district internal control systems are ineffective as there is little participation of key health workers, citizens and communities and tendency has been towards top-down approaches where health policy making is done by key consultants who are not implementers. This resonates well with results reached by Imoniana and da Silva (2019) that unawareness of control consciousness of the public servants in the healthcare units reflects on the behavior that emanates unintended consequences of flaws in internal control procedures.

Correlation analysis results

We discovered the following correlation results between the independent, dependent and the moderating variables as discussed below.

Internal control environment and health service delivery

Our findings indicated that there exists a relatively weak positive and significant relationship between internal Control environment and Health Service Delivery in Rukungiri District because the Pearson’s correlation coefficient r = .364**significant at 0.01 (99% confidence level) as the value of 0.000 is less than 0.05. The adjusted R2 = 0.124 and significance 0.000 suggested that internal Control environment was a strong significant predictor of Health Service Delivery in Rukungiri District but with low variation in Health Service Delivery. Hence internal control environment is a predictor of health service delivery in Rukungiri District. The study revealed that much as there is an indication of strong internal control practices as obtained in the control environment but they are largely ineffective. Majority of the health staffs were left out of internal control practices implementation and are not given feedback on the outcomes of meetings as key stake holders.

Internal audit function on health service delivery

The findings indicated there is a relatively weak positive and significant relationship between internal audit function and health service delivery in Rukungiri District because the Pearson’s correlation coefficient is r = 0.304**significant at 0.01 (99% confidence level) as the value of 0.01 is less than 0.05. This showed a statistical significance effect of internal audit function on health service delivery hence internal audit function is a predictor of health service delivery though the variation in health service delivery explained by internal audit was low. The findings also revealed that the district did not have a well functional internal Audit unit because audit did not play a significant role in fraud prevention and detection.

Internal control activities on health service delivery

The analysis also revealed that there is a weak positive and significant relationship between internal control activities and health service delivery in Rukungiri district where the Pearson’s correlation coefficient r = 0.319** significant at 0.01 (99% confidence level) as the value of 0.01 is less than 0.05 and this was statistically proven to be significant. Therefore, when internal control activities are improved, health service delivery is expected to improve.

The moderator effect on internal control practices and health service delivery

The results showed that there is a there is a weak positive and significant moderating effect of government policy on internal control practices and health service delivery in Rukungiri District where the Pearson’s correlation coefficient r = 0.335**significant at 0.01 (99% confidence level) as the value of 0.01 is less than 0.05. Therefore, if the managers of Rukungiri district follow government policy on internal control practices and health service delivery, corresponding outcomes are expected and this was statistically proved to be significant. The study findings also indicated that changes in government health regulations are not implemented timely by the district council, which negatively affects the health service delivery.

Regression analysis results

The study used linear regression analysis to predict the compounded effect of control environment, internal audit function and internal control activities, and health service delivery. The findings obtained from SPSS version 20 are presented in the Table 5. The model summary in the table above shows that R = 0.403a, R-square = 0.163 and adjusted R-square = 0.137. This means that 13.7% (0.137*100) variations in health service delivery is predicted by Control activities, Control environment and internal audit and government policy. The remaining 86.3% variation in health service delivery is explained by other factors that were not part of this study.

The findings from the descriptive statistics, interviews conducted from key stakeholders and documentary reviews revealed that that there is a positive and significant relationship between internal control practices and health service delivery. Health service delivery was dependent on internal control environment, internal audit function and internal control activities. If these variables are improved, health service delivery is expected to improve. Based on the findings of this study, the following recommendations are provided; It is recommended that internal control environment be strengthened at each and every stage of health service delivery so as to provide quality service delivery; There should be adequate supervision and monitoring of health activities to realize better health service delivery in Rukungiri district because this will help to minimize on some such as absenteeism by health staff; There is a need to increase the effectiveness of internal audit function to enhance accountability in the health sector; There is a need to have increased effectiveness of internal control activities in the health sector program activities through sensitization, performance management and accountability; There is a need to equip people with skills in health expenditure monitoring and reporting to minimize on the abuse of financial resources during implementation so as to effectively provide better services; There is need to sensitize and avail information related to changes in government policy and ensure timely implementation by relevant stakeholders; The district should put in place mechanisms on how it can disseminate information on any health policy updates from the Ministry of Health; Management should strengthen the stakeholder participation in formulating and implementing internal control practices to enable full ownership and responsibility.

The study recommends that future research be carried out on internal control practices but focus should be on other services such as education, roads, agriculture, water and sanitation. There are several other factors that affect health service delivery in Rukungiri district such as funding, political, culture, environmental and the user community. Another study could also be instituted to establish these other factors apart from internal control practices.

The authors have not declared any conflict of interest.

REFERENCES

|

Amin EM (2005). Social Science Research: Conception, Methodology and Analysis. Makerere University Press, Kampala.

|

|

|

|

Byarugaba C, Karyeija GK, Twinomuhwezi I (2014). Financial Management Practices and Health Service Delivery in Uganda Local Governments: A Case Study of Rukungiri District. International Review of Social Sciences and Humanities 6(2):72-90.

|

|

|

|

Carmines EG, Zeller RA (1979). Reliability and validity assessment. Sage publications.

Crossref

|

|

|

|

Committee of Sponsoring Organizations Framework (COSO) (2013). COSO Internal Control- Integrated Framework. Available at:

View

|

|

|

|

Fact Sheet for Anti-Corruption Report (2015). The Link between Corruption and Poor Health. Produced by the Anti-Corruption Coalition of Uganda.

View

|

|

|

|

Gordon O, Abbey K (2019). Internal controls and quality of health service delivery in a public health sector. A case study of a local government in Uganda. African Journal of Business Management 13(16):557-563.

Crossref

|

|

|

|

Imoniana JO, da Silva WL (2019). Understanding internal control environment in view of curbing fraud in public healthcare unit. African Journal of Business Management 13(18):602-612.

Crossref

|

|

|

|

Krejcie RV, Morgan DW (1970). Determining sample size for research activities. Educational and Psychological Measurement 30(3):607-610.

Crossref

|

|

|

|

Lee TA (1971). The historical development of internal control from the earliest times to the end of the seventeenth century. Journal of Accounting Research 9(1):150-157.

Crossref

|

|

|

|

Ministry of Health, Uganda (2015). Annual Health sector performance Report 2013/2014. Ministry of Health, Uganda.

View

|

|

|

|

Mugenda OM, Mugenda AG (1999). Research methods: Quantitative and qualitative approaches. Acts Press.

|

|

|

|

Mugenda OM, Mugenda AG (2003). Research Methods: Quantitative and Qualitative Approaches. African Centre of Technology Studies, Nairobi, Kenya.

|

|

|

|

Republic of Uganda (1995). The Local Government Act. Cap. 243. Kampala: Ministry of Local Government.

View

|

|

|

|

Rukungiri District Development Plan (2015). Rukungir District Development Plan, 2015/16-2019/20). Rukungiri District.

|

|

|

|

Rukungiri District Analysis Report (2016). Rukungiri District Local Government.

|

|

|

|

Sekaran U (2000). Research methods for business. United States of America: 2000.

|

|

|

|

Sekaran U, Bougie R (2016). Research methods for business: A skill building approach. John Wiley & Sons.

|

|

|

|

Uganda Public Finance Management Act (2015). The Public Finance Management Act 3 Cap. 115.

View

|