ABSTRACT

When distribution is neglected, micro insurance fails. This considered, the objective of this study was twofold – to explore the nature of micro insurance distribution channels and to understand the distribution strategy of a commercial insurance company in Swaziland. Using interviews with the senior managers of a commercial insurer and its distribution partners, this study generated in-depth qualitative data on their experience and recollections of the nature of channels and the strategy of distributing micro insurance. In this study, the commercial insurer leveraged predominantly on non-traditional channels such as churches, post offices, and cooperatives. These are characterised by access to large groups of potential clients and the trust of the community – but were initially incapacitated by a lack of technical expertise in terms of being trusted business associates and trusted advisors to micro insurance clients in Swaziland. Four inextricable components – depicting novel partnerships, ease of doing business, channel communication, and bringing micro insurance close to the people – encapsulate the distribution strategy of the commercial insurer. Among the key imperatives for cost-effective distribution of micro insurance are tailored channel development, consumer education, and segmentation of non-traditional channels to match low-income clients. Given the findings, a simple framework of micro insurance distribution and implications for research are proposed.

Key words: Micro insurance distribution, distribution strategy, service distribution.

Without a low-cost and effective distribution network, micro insurance cannot protect low-income people from specific perils in Swaziland. The seminal article on “Serving the world`s poor, profitably” (Prahalad and Hammond, 2002) pointed out that “the critical barrier to doing business in the rural regions is distribution access” to the poor.

Currently, this barrier is also prevalent in densely populated areas in and around our modern cities, where low-income people live. It is naïve for business managers in any commercial insurance firm to expect micro insurance success by placing primacy on price, product and promotion – without cost-effective distribution. Profoundly low-income people are unique as clients. They are often typified by an irregular flow of income, a lack of formal employment to facilitate payroll deduction of premiums, and also lack of bank accounts that are needed for debit order collection (Merry et al., 2014).

The vulnerability of low-income people and the need for micro insurance in Swaziland is amplified by a variety of factors such as high levels of poverty, heavy reliance on subsistence farming and high incidence of Human immunodeficiency virus infection and acquired immune deficiency syndrome (HIV/AIDS) (Golomski, 2015). The low-income market is new and unfamiliar to many organisational leaders in commercial insurance firms that are accustomed to conventional markets. The traditional system of brokers, agents and direct sales is geographically limited to cities, fails to reach the poor – and is also expensive (Biese et al., 2016; Cheston et al., 2018). The task of managing evidence of the intangible mechanism of transferring risk is a big challenge in the effort to win the trust of low-income clients that are stereotyped as sceptical of insurance. A totally different approach is required (Williams et al., 2017).

Research on micro insurance is growing, but is still predominantly at an embryonic stage in many countries – including Swaziland (Cai et al., 2015:287). As such, commercial insurance managers and employees are facing a variety of distribution quandaries, without much insight from research. However, recent empirical studies on micro insurance have started to explore alternative models for the distribution of micro insurance in emerging economies (Zieniewicz, 2014); the growth potential of digital micro insurance distribution; and opportunities, obstacles and challenges to distribution innovation (Chummun, 2017; Hillier, 2018; Leach et al., 2015).

In particular, synthesis of the strengths, weaknesses and suitability of different distribution channels is closer to the current study (Merry et al., 2014). However, the experiences of commercial insurers, agents, regulators and other distribution partners from Swaziland are not explored in this synthesis. Local praxis of micro insurance distribution in Swaziland is missing – reflecting a contextual lacuna. A theoretical void was uncovered by Gebauer and Reynoso (2013) who assert that “established service theories and empirical generalizations derived … from medium and high income segments are not necessarily applicable to the bottom of the pyramid markets, or at least, not always and in the same ways”. Up till now, the low-income market has been under-served and under-researched (Cheston et al., 2018).

Managers and researchers in Africa are often reminded that there are “many questions to be asked and options to be tried before solutions on how to protect significant numbers of the world`s poor against risk that begins to emerge” (Cai et al., 2015). As no single research is ever likely to answer all the questions, there is a strong need for a variety of robust scholarly research on micro insurance in countries such as Swaziland.

The objective of this study was to explore the nature of distribution channels used, and to understand the strategy of a commercial insurance firm that was actually used to distribute micro insurance to low-income people in Swaziland – as perceived by senior managers from a commercial insurer and its various distributors. In pursuit of this research objective, two interrelated research questions were formulated:

(1) What is the nature of the channels used by the commercial insurance firm to distribute micro insurance to low-income clients in Swaziland?

(2) What strategy of the commercial insurance firm is manifested through the various decisions and interactions taken by different actors in distributing micro insurance to low-income clients in Swaziland?

This section delves into the notion of distribution and discusses cardinal elements of distribution in the domain of micro insurance.

The concept of distribution

In pursuit of scholarly rigour, it is meaningful to decompose the concept of distribution strategy into two: distribution and strategy. To this end, some scholars define distribution as “pathways a product or service follow after production, culminating in purchase and use by the final end-user” (Kotler and Armstrong, 2017). In other words, distribution is a network of independent but interdependent firms that are intermediaries (CIM, 2015). Network size, number of intermediaries and retail outlets are salient when considering distribution intensity that may be exclusive, selective or intensive. Alternatively, distribution also means “all interactions that have to take place between the underwriter of the risk and the ultimate client” (Kotler and Armstrong, 2017). This study adopts this latter definition – as it suggests that a service channel comprises firms, their intermediaries, and their consumers. Having defined the concept of distribution, it is timely to delve into the intellectual landscape of strategy. Johnson et al. (2017) suggest that strategy has six building blocks. These are:

(1) Direction over a long term

(2) Scope in terms of diversity of activities and markets involved

(3) Advantage being sought in a changing environment

(4) Configuration of resources and competences

(5) Environmental factors affecting ability to compete; and

(6) Value and expectations of stakeholders.

Mintzberg’s 5 P’s offers a unique way of understanding strategy – as either a plan, ploy, position, perspective, or pattern (Mintzberg, 1987). This study subscribes to strategy as a “pattern in a stream of decisions over time”, regarding any of the identified six aspects. Thus, focusing on “what is done” by people in relation to distribution is key to uncovering a distribution strategy. Allowing strategy practitioners to reflect on past actions and decisions is fruitful for accessing strategy, where strategy is secretive and not easily shared with outsiders. With hindsight, both organisational insiders and outsiders can decipher the strategy pursued by a company.

Three cardinal elements of micro insurance distribution

Studies related to distribution channel theory reflect a disjointed collage – as there is no unifying framework. However, three cardinal elements are discernible in terms of distribution of micro insurance at the bottom of the pyramid. In brief, these include:

(1) Complexity of channel selection as there are many issues to consider.

(2) Clarity on the level of interaction in the sales model, being mindful of the variety of client needs and costs; and

(3) Understanding informal risk management and how this fits into the socio-cultural ethos of a particular market. Each element is discussed below:

Complexity of channel selection

Making an informed selection of traditional channels to work with as “trusted advisors” to clients and also as “trusted partners” of the commercial insurance company is complex and demanding (Cai et al., 2015). Channel selection is crucial – especially when distribution success relies on attributes (for example, trust) and the productivity of intermediaries (for example, sales agent, broker) (Biese et al., 2016). In this vein, Kotler and Armstrong (2017) state that methodical selection of a channel requires robust and comprehensive criteria. It is advisable that such a criteria include:

(1) Low partnership risk

(2) Low-cost distribution for the insurer

(3) Willingness of the channel to prioritise micro insurance

(4) Popularity and trust of a channel, and

(5) The ability to scale in terms of accessing a large number of potential clients (Merry et al., 2014).

Additionally, the ability of a channel to offer product diversity, and to improve client understanding, are also critical in channel selection (Merry et al., 2014). In a different vein, Zieniewicz (2014) asserts that a cost-effective channel should pass the test of the 4A’s – availability, accessibility, affordability, and acceptability by clients. In the conventional insurance market in Swaziland, three traditional channels are common: broker, funeral parlour and credit provider (Hougaard et al., 2011).

As intermediation of conventional insurance is dominated by brokers (for example, Tibiyo Insurance brokers, AON and Dups Insurance Agency), the specific questions of how micro insurance is distributed to the poor in Swaziland, is enlightening. It is intriguing to note that a successful commercial insurer needs to look beyond traditional distribution channels. The variety of alternatives to traditional ways of distributing micro insurance products is growing (Glaesener-Nasr, 2017). For example, cash-based retailers (for example, Shoprite); credit-based retailers (for example, furniture retailers); utility providers (for examples, gas, water, electricity); and telecommunications companies have all played a pivotal role as non-traditional channels for micro insurance.

According to Merry et al. (2014), cooperatives, community-based organisations (forn example, trade unions, faith-based organisations, and small business associations), mobile network operators, and employers have formed part of micro insurance distribution in South Africa, India, Bangladesh and Brazil. In Swaziland, there were 36 brokerage houses and over 250 agents that included unaffiliated individual brokers and entities like funeral parlours in the insurance market in 2013 (Golomski, 2015). In view of the aformentioned, it is prudent for a commercial insurer to grapple with a variety of key issues within traditional and non-traditional channels – before deciding on a suitable mix of channels.

Clarity on level of interaction in the sales model

The degree of interaction between a sales agent and a client is critical as it influences the type of sales model, and transaction costs. Commercial insurers grapple with whether to use a passive or active sales model, and why. First, passive sales models are characterised by products placed on a shelf at a cash retailer, without any verbal communication by retailer staff (Leach et al., 2015). Interestingly, the rise of the digital channel has brought to the fore low touch, advice-less sales models that are inexpensive (Sandquist et al., 2015). The digital channel triggers disintermediation and cost reduction. In some instances, these types of channels are associated with loss of face-to-face support to illiterate clients who are unfamiliar with the legal language of micro insurance (Leach et al., 2015). Technology needs to be an enabler – as digital channels on their own (for example, selling of insurance over the internet initiated by a low-income client) cannot easily overcome the bias of people, without considerable persuasion through human channels (Cheston et al., 2018). Second, active sales models use representatives of an insurer or retailer who verbally inform and try to persuade a client to buy insurance (Sandquist et al., 2015). With face-to-face support by certified or uncertified insurance agents, high touch and advice-based sales models are more expensive (Leach et al., 2015). The level and quality of interaction is at the core of a sales model in micro insurance, as it reinforces or diminishes the credibility of intermediaries as trusted links with clients (Kotler and Armstrong, 2017).

Informal risk management

In many African contexts, there are many informal risk management mechanisms that are not officially registered, but are well-known and used by the poor. Loan sharks, risk-sharing groups (for example, rotation savings and credit associations), savings and credit clubs, and mutual lending between relatives and social networks with flexible terms, are some of the informal risk management mechanisms used by the poor in developing countries (Leach et al., 2015). There are also formal organisations that offer insurance products that are not registered with the authority. These are potential substitutes of formal micro insurance. The eligibility criteria used for most informal insurance mechanisms are unique. The criteria is often less demanding – but also is undocumented and based on social factors (for example, reputation, social visibility, and social integration). In this vein, it is wise that a commercial insurer is fully aware of how micro insurance is superior or inferior to informal ways of coping with risks, and how formal channels fit into the socio-cultural ethos of the poor in a particular context. According to Hougaard et al. (2011), informal savings clubs called Inhlangano; unlicensed organisations that provide funeral insurance; and self-insuring funeral parlours – are all noticeable in Swaziland. In the light of the aforementioned, the question relating to the actual nature of channels and strategies used to distribute micro insurance in Swaziland by a commercial insurer is very interesting, but under-researched.

This section describes how participating organisations and their senior managers were selected, and how data were collected and analysed.

Research paradigm

This phenomenological study was premised on a social constructivist paradigm, and was tolerant of multiple perspectives of reality upheld by people with lived experience of a phenomenon (Bryman and Bell, 2015). As a case study, the focus was on a contemporary phenomenon in a real-life context, where boundaries between a phenomenon and context were not clearly evident (Yin, 1994). In terms of epistemology, the researcher’s role was to interact closely with participants to get their deep understanding of subjective reality.

Multi-stage sampling

Selection of commercial insurance company

The researcher used purposive sampling to select a “critical case” of a commercial insurance company in order to get compelling insights into micro insurance distribution in Swaziland. Selecting a firm reflecting most characteristics of a commercial insurance company active in micro insurance distribution in Swaziland, was salient. To this end, the following three selection criterion were used:

(1) National coverage embracing urban and rural areas;

(2) Being a subsidiary of a foreign firm, especially the type of firms that dominated the market; and

(3) Being active in the micro insurance market for not less than five years.

At the time of the study, there were 10 commercial insurance firms in Swaziland. More importantly, the criteria for selection of the company considered that 9 of the 10 insurance companies were foreign firms responsible to their respective head offices outside the country. Furthermore, only 4 of the companies were operating in the micro insurance market. The selected commercial insurance company met the aforementioned criteria, and had experience in the conventional insurance market that was acquired before starting to distribute micro insurance. The top management team (TMT) of the selected commercial insurance firm was willing to reflect on their own decisions and actions regarding micro insurance distribution.

Selection of organisations in the distribution chain

The researcher used snowball sampling to select four different types of organisations – a cooperative, church, funeral parlour and a post office – which distributed the micro insurance of the selected commercial insurer. This was helpful to verify or validate initial results from members in preceding organisations.

Selection of individual participants

The focus of the study was on senior managers comprising the TMT in each of the specific distributors selected. A total of 8 participants – 6 males and 2 females – were purposively selected for this study. Thus, 4 senior managers were from the selected commercial insurance company; 1 was from a post-office, and another was from a funeral parlour. Two (2) senior managers were from different affinity partners – a cooperative and a church. The participants were aged 35-50 years. A minimum of three years of experience in distributing micro insurance offered by the selected commercial insurance company was a pre-requisite. This was to ensure that each participant could meaningfully understand, reflect and report on what was actually done – not only in his or her organisation, but also in others – to provide a deep understanding of the nature of channels, but also the strategy of the selected commercial insurance firm.

Data collection

Data were collected through 12 semi-structured, in-depth and retrospective interviews with 8 senior managers. An interview guide was used to assist senior managers in their reflection on what was done by various actors in the commercial insurer and its distribution partners. The questions in the interview guide were framed to delineate:

(1) Perceived objectives of the commercial insurance company regarding distribution of micro insurance.

(2) Characteristics of routes or channels used to deliver micro insurance.

(3) Decisions and interactions made by people in the commercial insurer, distribution partners and clients that depict strategy to distribute micro insurance; and

(4) The variety of consequences of distribution-related decisions and actions that were taken.

On average, each interview took 30 min. Follow-up interviews were taken to probe specific issues, and to enhance clarity. Overall, sampling of organisations, individuals, and data collection ceased because of data saturation.

Data analysis

Data were broken down into codes that were constantly compared with each other to develop broader categories. Subsequently, similar categories were classified to ultimately induce relevant themes reflecting the nature of channels and the strategy of distributing micro insurance. To illustrate this, the theme of ‘ease of doing business’ was derived from comparing what the commercial insurer was doing for distributors (for example, removing obstacles) with what partners were doing for clients and how (for example, supporting clients with data transmission, revision of policies, and posting proof of payments). Progressively, comparisons were also made with how partners influenced client transactions (for example, high credibility of churches and post-offices, technical know-how of post-offices in data transmission) and clients’ view of transactions (for example, easy, convenient, and safe). Ultimately, these actions and views at different levels led to the theme that was initially labelled “ease of doing business at multiple levels” – before becoming simply ‘ease of doing business’.

Trustworthiness

The researcher used member check or respondent validation to allow clients to provide feedback – in order to ensure integrity or credibility of the findings. Additionally, procedures, processes and quotes from participants in this study are clearly documented to provide an audit trail. This enhanced the dependability and confirmability of the study. Lastly, triangulation of perspectives of participants helped to corroborate views, ensure comprehensiveness of accounts, and identified nuances.

This section presents the findings of the study which manifest the nature of channels used – before depicting what was manifested as the strategy of a commercial insurance company in terms of distributing micro insurance in Swaziland.

Limited variety of five non-traditional channels

The commercial insurance company in Swaziland leveraged on a very limited variety of non-traditional channels, and was incapacitated initially by lack of technical expertise in micro insurance. Seven senior managers said that a limited variety of five non-traditional channels were used for helping micro insurance to reach consumers in Swaziland. In terms of type, these included two local community-based organisations (for example, the church and cooperative), a state-owned organisation (for example, the post office), and two private businesses (for example, funeral parlours and brokers). The nature of the church as a channel was construed in terms of low-cost and scale to appeal to many in the communities – as elucidated by a senior manager in the quote below:

We need to keep costs low ... commission also needs to be low. So, we have been diversifying to other distribution channels selling our products … rather than concentrating on the usual brokers ..., I spoke about our partnership with funeral parlours … churches to distribute cheaply to their congregations (Manager 1).

Furthermore, the churches and post offices were commonly characterised as being more reliable and trusted, and also provided a convenient, countrywide network of branches that served as channel members:

(Name of commercial insurer) has been successful in identifying more trusted distribution partners, such as Swazi Post which has 34 post offices in Swaziland, the Swaziland Conference of Churches with 137 affiliated member churches whose membership is over 200,000 nationwide. Swazi Post, in particular, is present in the rural areas where the post offices are still a main, reliable business centre for the masses … possible retail clients for us (Manager 7).

Predominantly, the channels used by the commercial insurer exhibited an initial lack of technical expertise to give quality advice for the choice of micro insurance products, servicing of policy post sale, and settlement of claims by clients. To address this, one of the senior managers exemplified the scope of technical assistance rendered to one of the cooperatives as a channel member:

[Name of insurer] assisted [Name] Savings & Credit cooperatives to understand risks of clients not being able to claim, the requirements of [Name of cooperative] to service its member … .use their knowledge of when clients get ... money to help them with choices. … legal compliance … and obligation to clients were clarified to them as a distribution partner (Manager 8).

The nature of channels used by the commercial insurer brought up novel challenges. Generally, a lack of selection criteria cropped up as a result of the novelty and non-traditional character of channels. This resulted in frustration of people within the insurer but also of prospective affinity partners – as it created bottlenecks in finalising partnerships. In particular, the church as a novel channel brought to the fore controversial religious beliefs and intra-group differences that were inherent to the nature of this particular channel, and this was clarified by one of the senior managers:

Negative attitude by some church members … saying insurance is for those with little or no faith was strange to me … a different problem from the usual untimely remittance of premiums … some customers paying as and when they are able to rather than on a regular basis. Group schemes undermined by slow pace of decision making, and some individual members opting to join on their own (Manager 5).

The next section reveals, in detail, the strategy of the commercial insurance firm regarding how micro insurance was actually distributed.

Manifested strategy: Multi-channel micro insurance distribution

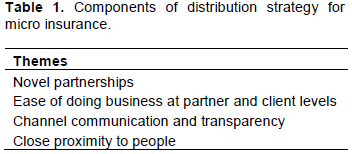

The findings show that the commercial insurer in Swaziland used a multi-channel distribution strategy characterised by a variety of four interrelated components:

(1) Novel partnerships

(2) Ease of doing business at partner and client levels

(3) Channel communication; and

(4) Close proximity of micro insurance to people.

This ‘manifested’ distribution strategy is summarised in Table 1. Each of the four components is illustrated below.

Novel partnerships

All eight senior managers in this study agreed strongly on how an indirect distribution model and bulk retailing were possible as a result of novel types of partnerships with affinities and brokers. This was surmised by one of the senior managers, as follows:

Our objective as (name of commercial insurer) was not to directly sell to clients, but rather [to] do bulk retail selling through new partnerships with affinities such as cooperatives. That’s why bulk retailing partners for [name of commercial insurer] engaged with individual customers in the administration and queries on their policies (Manager 2).

In fact, it was a commercial insurer’s impetus of penetrating the existing market through new channels that led to novel partnerships, but also coincidental access to a new consumer segment with unique needs. There was a lack of planned and intelligent segmentation of distribution channels by a commercial insurer to match with low-income people as an intended consumer segment. This was reiterated in this way:

Distributing micro insurance was not initially planned as a deliberate move for us. It was a coincidental result of a partnership with affinities … who had [their] own clients whom they served. We were exploring more convenient ways to get more clients ... getting a bigger share of the same pie … not looking for a new pie (Manager 3).

Ease of doing business at partner and client levels

According to five of the eight senior managers, high credibility of partners, technical know-how in facilitating a variety of key activities needed by clients (for example, purchasing of policy, remittance of premium and submitting of proof of premium payment), but also convenience and safety, contributed to making micro insurance-related interactions easy. In particular, post offices as a non-traditional channel made a variety of transactions easy for clients while also making additional revenue from other services such as data transmission:

(Name of commercial insurer) has been working with the partners to find safe means of remitting premiums and sending proof of payments in cost-effective ways, for example, after depositing premiums in the nearest bank the customers then post the proof of payment – thus reducing travelling costs for customers in remote areas.

Using the post office to purchase policies, send data, and update policies is safe, and has also saved customers costs (Manager 7).

The commercial insurer’s removal of obstacles to quick and easy transactions in selling and collecting the premium motivated partners in their pursuit of increased market share:

Slow decision-making is an obstacle … competition is high. So quick decisions... easy transactions in selling and collecting premium are good to … gain market share (Manager 6).

Channel communication

Five senior managers deciphered how channel communication was pivotal in the attempts of a commercial insurer to enhance client understanding, deliver a variety of benefits to clients, and promote transparency at various levels of the channel. One of the senior managers echoed this as follows:

(Name of insurers) is serious … it tries to ensure customers understand the benefits on their existing policies and conditions in which their claims can be made or even declined. The [name of insurer] communicates to everyone from customers all the way to funeral parlours … to know who does what ... when ... until premiums ... is received or a claim is processed (Manager 6).

Another senior manager was clear that the use of simple names, and the translation of product terms and conditions into the local language benefited different types of consumers – but also the sales team in the channels:

Besides naming the products simply, e.g. the ‘simple life cover’, the product terms and conditions are indeed simple to understand … written in plain English and others translated to SiSwati. It’s easy for us to explain … to even make older people understand the product features and benefits (Manager 5).

Close proximity to people

According to all the eight senior managers, there was an economic (for example, sales team visits to distant rural areas reduced costs for clients) and behavioural dimension in respect of how micro insurance was close to people (for example, trusted collectors of premiums). One of the senior managers exemplified close proximity to the people as follows:

The agent selling micro insurance goes as far as Nkonjaneni in northern Hhohho region, visits people … at workplaces then waiting for people to come to agents’ offices in Manzini. Instead of paying E20.00 for transport to make a E11.00 premium payment, the local Alliance church accepts and remits the premiums on behalf of the individuals (Manager 4).

In a different vein, the use of people residing within the local community and from local community-based organisations to collect premiums meant that micro insurance was socially close to the people:

The churches, church elders are near and in touch with the people ... they get premiums from as low as E11.00 for E3,000 cover on an individual member joining at the maximum age of 85 years on the [local name] funeral plan. This is affordable. Other insurers charge E36.00 for a person who is 65 years and above (Manager 2).

It is noteworthy that a commercial insurer needs to achieve its full potential in micro insurance distribution – by increasing the scope of the novelty and diversity of non-traditional channels that already transact with low-income people. However, the nature of channels used by the commercial insurer in Swaziland manifested as a limited variety of non-traditional channels typified by faith-based organisations (for example, a church), state-owned organisations (for example, post office), co-operatives (for example, credit and saving cooperatives) and private businesses (for example, funeral parlour, broker).

Studies by Merry et al. (2014) with more than 60 partners distributing micro insurance in different countries (for example, Haiti, Ghana, South Africa, Pakistan) revealed that the diversity of non-traditional channels for micro insurance is ever growing. For instance, cash and credit-based retailers, utilities (for example, gas, water, electricity), telecommunications companies, mobile network operators and agricultural suppliers are some of the alternative channels for micro insurance in India, Bangladesh, South Africa, Zimbabwe and Tanzania (Merry et al., 2014; Sandquist et al., 2015).

While it is positive that non-traditional channels are characterised by scale in terms of the ability to access a large group of potential clients at a low cost, and trust within the community, initial lack of technical expertise has the potential to negatively affect partner productivity. In fact, “if partners are not productive quickly, they do not receive value and lose interest in the scheme” (Merry et al., 2014).

Furthermore, productivity also suffers when both distribution partners and beneficiaries are all in an uncharted or unfamiliar market. This underscores the need for tailored non-traditional channel development, consumer education and a learning culture, and a climate for everyone to learn and develop to their full potential (Biese et al., 2016:29; Kotler and Armstrong, 2017).

It is clear that the non-traditional channels used by the commercial insurer were predominantly human and not much enabled by technology. Biese et al. (2016) state that human channels are more expensive than digital channels. To ensure high-volume, low-cost, ease of administration, and sending text message (SMS) reminders for premium payments – commercial insurers in Swaziland are advised to consider partnerships with mobile network operators who already have high market penetration (Leach and Kachingwe, 2015).

Studies in Kenya have shown that the entry of mobile payment models such as M-PESA has solved problems of premium collection and claims payments (for example, a vast network) – thereby removing a significant constraint to insurance distribution (Biese et al., 2016). Nonetheless, it is prudent to always balance the human and digital aspects of a channel. Despite the efficiency of digital, the adage remains that insurance is not bought, it is sold (Lewin, 2014). Thus, face-to-face persuasion is key to overcoming prejudices of low-income people regarding insurance (Kotler and Armstrong, 2017; Leach and Kachingwe, 2015).

The way distribution partners are selected is critical, and requires a methodical approach. Arguably, a bricolage which Weick (1993) characterises as using “whatever resources and repertoire one has to perform whatever tasks one faces”, is closer to how partners were chosen by the commercial insurer in this study. In this way, commercial insurers are not exhaustive enough to ascertain all critical issues, in order to select a cost-effective and non-traditional channel to reach low-income people (Merry et al., 2014).

The innovative and evolving nature of diverse non-traditional partners necessitates that commercial insurers develop, update and use comprehensive criteria to select appropriate distribution channels and members (Kotler and Armstrong, 2017; Cheston et al., 2018). The manifested strategy of the commercial insurer to distribute micro insurance in Swaziland is interesting – as it hinged on four inextricable components related to novel partnerships, ease of doing business, channel communication, and delivery of micro insurance close to the people.

Firstly, it is interesting that there was no segmentation of partnerships or distribution channels by the commercial insurer to match with a particular consumer segments – leading to coincidental access to low-income clients. Some commercial insurers are sceptical about market demand for micro insurance, such that they offer products in the micro insurance space without deliberately designing and targeting them for the segment of micro insurance in the market.

The consequence is the en passant or incidental distribution of micro insurance products that may only achieve ephemeral success, if any. Hougaard et al. (2011) advise that “where the majority are poor, there is a convincing argument to stop regarding micro insurance as peripheral “microbusiness” with few homogenous clients. This resonates with the findings of a study in India which found that micro insurance is an enormous business opportunity not only to serve the underserved informal economy – but also to attain sustainable economic development (Shaik and Babu, 2018).

Secondly, the manifested distribution strategy also underscores that mutual trust perceived, experienced and managed at multiple levels of the client, partner and commercial insurer in a distribution channel, is a fundamental part of relationship-orientated channel management, if alternative channels are to be trusted advisors for low-income people and trusted business associates for commercial insurers (Cheston et al., 2018).

In this vein, Hougaard et al. (2011) concluded that despite the convenience of a transaction platform, low-income people in Swaziland would only find insurance attractive if more information and education was available – because they believe that sales people do not always have their best interests at heart. Thus, while trust generates cooperation of clients, it also exposes them to opportunism and exploitation (Reiersen, 2017). It is crucial that low-income clients trust non-traditional channels, commercial insurers, micro insurance products, and also the convenient transaction platform based on understanding. This also illustrates how a distribution channel is an inter-organisational collective where the needs of every player should be analysed and satisfied (Kotler and Armstrong, 2017). Research attests that the distribution of micro insurance helped the post office in Morocco to increase profits, but also retain its clients (Merry et al., 2014). It is valuable for a commercial insurer to decipher distribution partners’ need and how each of them can get a competitive advantage by distributing micro insurance to their existing base of clients.

Thirdly, channel communication in this study was useful to communicate and ensure client understanding of benefits and conditions in policies which is a key part of the quality of sales. A study which focused on mobile micro insurance in Zambia concluded that when low-income people lack a basic understanding of micro insurance, they do not use it properly, often feel deceived, and subsequently fail to renew the policy concerned (Leach and Kachingwe, 2015). Arguably, selling insurance which is not understood properly, is a self-defeating strategy.

Lastly, the study revealed how reducing geographical distance and its economic implications for clients is just one of the key aspects to getting micro insurance products and service closer to people. Micro insurance was also socially close to people when local individuals who know their communities and are themselves known by the people were involved and accepted to give technical advice or to reinforce premium collection from clients. This is a significant pointer to a sociological system where human social interactions, local rules and processes bring solidarity, and separate low-income people not only as individuals, but as members of a micro insurance group – especially in environments with little insurance culture. Micro insurance firms need to offer incentives not just at the organisational level (for example, church), but also the level of individuals (for example, sales force) in non-traditional channels. Given the aforementioned, it is more edifying to bring out from these findings a set of basic components and their relationships – in order to propose a useful distribution framework.

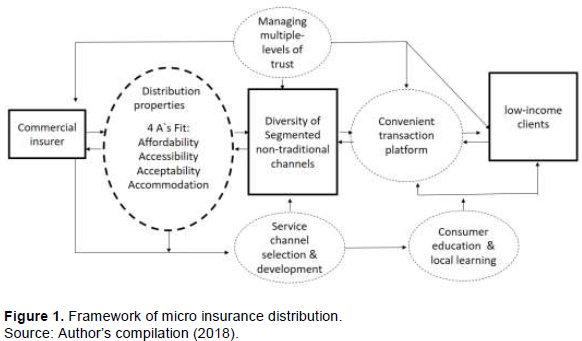

Framework of micro insurance distribution

The framework of micro insurance distribution that is proposed suggests that effective micro insurance distribution occurs when specific distribution properties – namely affordability, acceptability, accessibility and accommodation (4A’s) – permeate a variety of non-traditional channels, and also become part of a convenient transaction platform for ensuring that low-income people are reached by micro insurance. In the micro insurance distribution framework in Figure 1, components have been defined, while statements of relationships are highlighted.

Distribution properties: 4A’s

It is fundamental that a commercial insurer needs to ensure that alternative channels for micro insurance are:

(1) Acceptable

(2) Affordable and

(3) Accessible to low-income people. While meeting these needs of clients, it is also important that a commercial insurer ensures that the business needs of non-traditional channels are also met, or

(4) Accommodated in a profitable and sustainable way (Cheston et al., 2018).

A non-traditional channel is more effective when most of the four 4 A’s complement each other to distribute micro insurance. The way that non-traditional channels are trained and clients educated needs to also reinforce the 4 A’s as key in reaching low-income people (Lewin, 2014). The outcome of interactions in non-traditional channels with their respective contexts and clients may also redefine the meaning of any of the aspects of the 4 A’s. Scholarly understanding of what facilitates or inhibits the distribution of the 4 A’s in micro insurance distribution channels or transaction platforms, has triggered research interest.

Diversity of segmented non-traditional channels

As the plethora of non-traditional channels for micro insurance continues to grow (for example, digital channels, retailers, churches), it is important for a commercial insurer to also increase the diversity of channels and their members (Leach et al., 2015; Prashad et al., 2014). Thus, diversity and segmentation of the various channels to match with consumer segments – is necessary to meet the needs of different types of clients of micro insurance (for example,. literacy levels, age, gender), and to deliver value to commercial insurers and non-traditional distribution partners (Hillier, 2018). An alternative channel is cost-effective if it delivers the 4 A’s for the commercial insurer and is also well-matched to satisfy the needs of distribution partners and low-income people. Non-traditional partners expect more than an additional source of revenue stream derived from their role in micro insurance distribution. Merry et al. (2014) advise that a commercial insurer’s product needs to solve an important problem for the distributor. This is key to incentivising distributors in order to ensure a product’s success. Feedback on how well the 4 A’s are manifested or not in the channels is valuable for informing the nature and mix of non-traditional channels.

Convenient transaction platform

Processes (for example, premium payment, servicing) and structures (for example, mobile, social and physical infrastructure) are necessary for ensuring reliable, convenient and simple execution of various micro insurance-related activities by clients and distribution partners (Glaesener-Nasr, 2017). For instance, ease of revising policies is important for clients while regular payment of premiums by clients is a key transaction for distribution partners and the commercial insurer. With role clarity and group processes, some individuals are entrusted to facilitate premium collection and payment on behalf of others. Mobile payment solutions enabled by technology are increasingly offering a reliable platform for transactions – irrespective of where low-income people live.

Managing multiple levels of trust

Trust is a barrier if it does not prevail between the commercial insurer and distribution partners, and also between distribution partners and clients (Cheston et al., 2018). When clients distrust micro insurance, they do not take it up, and cancel or refuse to renew micro insurance policies. Thus, commercial insurers and distribution partners have a key role in managing trust at multiple levels (e.g. product, partner and insurer levels) to reduce the cost of precautions and monitoring, and also to make cooperation easier. Trust acts as a “booster” to enable people in a group to enter into a mutually committed relationship (Reiersen, 2017). However, this is insufficient if clients do not trust the product and its benefits or the transaction platform. Within networks, members meet regularly, know each other well and may be willing to punish those who fail to keep promises. Trust functions as an effective enforcement mechanism in formal and informal agreements of cooperation – while reducing opportunism (Reiersen, 2017). Trust is valuable among low-income clients in small-scale interactions within local groups or networks in the communities (Reiersen, 2017).

Service channel selection and development

Training and development of carefully selected alternative channels and channel members (which may have nothing to do with insurance) is critical for effective micro insurance distribution, and quality of sales - not just quantity (Belanger, 2016). Different non-traditional channels have different training needs to enhance capability and scalability of distributing micro insurance.

Lewin (2014) posit that tailored and continuous channel development and training is key for meeting the different needs of diverse non-traditional partners so that they become trusted advisors for clients, trusted business associates for commercial insurers, reliable sales force or platforms for payment. Continuous training of intermediaries is key to maintain consistency, enforce quality, and at the same time provide flexibility to encourage non-traditional distribution partners to think creatively when serving low-income clients. Shifting vendors of air time from a purely mobile payment platforms to an agency role is key to future channel development in micro insurance (Chummun, 2017:12-15).

Consumer education and learning

Consumer education and awareness is key for low-income clients to understand not just micro insurance principles, but for making informed comparisons and product choices and for learning to trust distributors and transaction platforms (Lewin, 2014). As alluded to earlier, many low-income people are sceptical of insurance providers, insurance sales agents and of the insurance products themselves. Insurance education and learning are very important for enlightening such consumers and should embrace the diversity of potential clients. Informal mechanisms also need to be used as a stepping stone into the formal system and to at least raise awareness of the insurance mechanism.

Two aspects make the proposed framework of micro insurance distribution unique and more holistic. First and foremost, micro insurance scholars (Biese et al., 2016; Merry et al., 2014; Zieniewicz, 2014) have to date not developed any framework or model on micro insurance distribution. Instead, we have catalogues or descriptions of what have been construed as strengths and weaknesses of various non-traditional channels, and lists of critical components in micro insurance distribution – as construed by different scholars. Some of these lists overlap, while others do not. For example, Biese et al. (2016) have listed most, but not all the components in the proposed framework. In this way, their list is not comprehensive. It has omitted distribution properties and multiple-levels of trust. The proposed framework depicts micro insurance distribution as a whole, with constituent components and various interrelationships.

Kotler and Armstrong (2017) as marketing scholars, have provided a generic framework of distribution, and have focused only on levels of distribution channels between the producer and consumer to show the pathways. The proposed framework includes pathways, but also facilitative issues such as nature of trust, transaction platform, and consumer education – which are all key components in micro insurance distribution. The proposed framework is holistic in that it offers practitioners a basis to meaningfully theorise their practice, but also to practise the theory of distributing micro insurance without ignoring any key component.

Implications for research

It is noteworthy that all the various components of micro insurance distribution, as proposed in the framework, need to be subjected to further exploratory research involving a variety of senior managers, in different types of commercial insurers and distribution partners. The framework is less abstract, such that the need to capture as much contextual diversity as possible – is imperative for enhancing explanatory power.

Three implications are identified regarding channel comparisons, the research sample, and sociological understanding of micro insurance distribution. This study focused on the number, type and characteristics of non-traditional distribution channels. Future research needs to go beyond the nature of channels to undertake systematic comparisons “between channels and within channel members” – to gain a deep understanding of the internal functioning and socio-economic relations in non-traditional channels.

A major limitation of the study is the exclusion of views of non-managerial stakeholders. More inclusive empirical studies are needed to include lower-level employees, micro insurance clients and regulators in the sample – to enrich our understanding of micro distribution in this context. It is also prudent that future studies also use a variety of data (Yin, 1994). If accessible, documents may help by revealing events and actions that may not be remembered by senior managers.

Lastly, the study has revealed that bringing micro insurance close to people has three dimensions: economic, behavioural, and social. These should not be analysed in isolation. However, the social dimension opens up the sociology of distribution. Thus, how distribution of micro insurance through non-traditional channels is shaped by sociology, particularly small-scale interactions, social conditions and norms at the level of groups or community, is an interesting area for future research.

Many non-traditional channels characterised by scale to reach large groups of potential clients at low cost and the ability to provide quality technical advice to clients, if trained and developed properly – are helpful for enhancing micro insurance distribution. Furthermore, the study also concludes that the failure of a commercial insurer to segment and match non-traditional channels with low-income clients, undermines the cost-effective distribution of micro insurance.

In pursuit of a multi-channel distribution strategy, a commercial insurer should underpin four cardinal and inextricable aspects – novel partnership which may sometimes involve non-commercial partners, ease of doing business, channel communication, and bringing micro insurance close to the people geographically and socially. It is interesting that the social notion that micro insurance is also socially close to people, opens up a potentially fruitful line of inquiry into the sociology of distributing micro insurance. Pragmatically, the framework of micro insurance distribution proposed in this study offers micro-level, practical nuances of “doing” micro insurance distribution – to achieve scale and efficiency in a specific context or any other similar contexts. In this concrete way, the study is original and pragmatic for commercial insurance practitioners who are currently hesitant to venture into this vast and untapped market in Africa. Although the framework is less abstract, it is a significant start to fuelling further exploratory research to generate a contextually relevant practice of distributing micro insurance with greater explanatory power, across a variety of contexts where the poor live in Africa.

The authors have not declared any conflict of interests.

REFERENCES

|

Belanger MC (2016). Building insurance through an NGO: Approaches and experiences from a rice insurance pilot in Haiti. Agricultural Finance Review 76(1):119-139.

Crossref

|

|

|

|

Biese K, McCord MJ, Sarpong MM (2016). The Landscape of micro insurance Africa 2015. Micro insurance Network, Munich Re Foundation and Micro Insurance Centre.

|

|

|

|

|

Bryman A, Bell E (2015). Business research methods. USA: Oxford University Press.

|

|

|

|

|

Cai H, Chen Y, Fang H, Zhou L (2015). The effect of micro insurance on economic activities: Evidence from a randomized field experiment. Review of Economics and Statistics 97(2):287-300.

Crossref

|

|

|

|

|

Cheston S, Kelly S, McGrath A, French C, Ferenzy D (2018). Inclusive Insurance: Closing the Protection Gap for Emerging Customers. A joint Report from Center for Financial Inclusion at Accion and the Institute of International Finance

View. Accessed on 5 December, 2017.

|

|

|

|

|

Chummun B (2017). Mobile micro insurance and financial inclusion: the case of developing African countries. Africa Growth Agenda (3):12-16.

|

|

|

|

|

CIM (2015). Marketing and 7Ps: A brief summary of marketing and how it works. Berkshire, UK: Chartered Institute of Marketing.

|

|

|

|

|

Gebauer H, Reynoso J (2012). An agenda for service research at the base of the pyramid. Journal of Service Management 24(5):482-501.

Crossref

|

|

|

|

|

Glaesener-Nasr J (2017). An interview with Joseph Owuor, Insurance Regulatory Authority, Kenya. The State of Micro Insurance: The Insider's Guide to Understanding the Sector 3:61-80.

|

|

|

|

|

Golomski G (2015). Compassion technology: Life insurance and the remaking of kinship in Swaziland's age of HIV. American Ethnologist 42(1):81-96.

Crossref

|

|

|

|

|

Hillier D (2018). Facing Risk: Options and challenges in ensuring that climate/disaster risk finance and insurance deliver for poor people. Oxfam GB, UK.

Crossref

|

|

|

|

|

Hougaard C, Chelwa G, Swanepoel A (2011). Swaziland micro insurance review: A market and regulatory analysis. Cape Town: Centre for Financial Regulation and Financial Inclusion.

|

|

|

|

|

Johnson G, Whittington R, Scholes K, Angwin D, Regner P (2017). Exploring corporate strategy: Text and cases.11th Edition. London: Pearson Education Limited.

|

|

|

|

|

Kotler P, Armstrong G (2017). Principles of marketing. 11th Edition. Harlow: Pearson Education Limited.

|

|

|

|

|

Leach J, Tappendorf T, Ncube S (2015). Can digitalization of micro insurance make all the difference? Assessing the growth potential of digital micro insurance. Sommerville, MA: Bill and Melinda Gates Foundation.

|

|

|

|

|

Leach J, Kachingwe M (2015). Managing risk while facilitating innovation: The case of m-insurance in Zambia. Midrand: Fin Mark Trust.

|

|

|

|

|

Lewin P (2014). Promising starts in mobile micro insurance: Tigo Senegal and Telnor Pakistan.

|

|

|

|

|

Merry A, Prashad P, Hoffarth T (2014). Micro insurance distribution channels: Insights for insurers. Geneva: ILO Impact Insurance Facility.

|

|

|

|

|

Mintzberg H (1987). The strategy concept 1: Five Ps for strategy. California Management Review 30(1):11-24.

Crossref

|

|

|

|

|

Prahalad CK, Hammond AL (2002). Serving the world's poor, profitably. Harvard Business Review 9:48-57.

|

|

|

|

|

Prashad P, Saunders D, Dalal A (2014). Mobile phones and micro insurance. Geneva: ILO Micro Insurance Article No. P 26.

|

|

|

|

|

Reiersen R (2017). Trust as a booster. Journal of Business Economics and Management 18(4):585-598.

Crossref

|

|

|

|

|

Sandquist E, Gasc JF, Sollmann R, Knight M (2015). Reimagining insurance distribution. Accenture Research Group.

View. Accessed 14 June 2018.

|

|

|

|

|

Shaik G, Babu P (2018). Micro insurance – mechanism and opportunities for the sustainable development of Indian economy. International Journal of Mechanical Engineering and Technology 9(2):857-865.

|

|

|

|

|

Yin RK (1994). Case study research: Design and methods. London: Sage Publications.

|

|

|

|

|

Zieniewicz M (2014). The distribution channels of insurance products in Poland and in selected European countries. Economics questions, issues and problems. Poznan: Poznan University of Economics.

|

|

|

|

|

Weick KE (1993). The collapse of sense making in organisation: The Mann Gulch disaster. Administrative Science Quarterly 38:628-652.

Crossref

|

|

|

|

|

Williams AJ, Ubom AU, Ubom, UB (2017). Micro insurance, Micro investments and Sustainable Development in Nigeria. Expert Journal of Finance 5(1):41-48.

|

|