Full Length Research Paper

ABSTRACT

This research investigates the residential real estate market in an emergent European country, Romania. Using data from approximately 300 sales transactions and another 300 nationally relevant rent transactions conducted between midyear 2010 and midyear 2011, the real estate market prices and rental prices have been processed using statistical techniques such as the General Linear Model, in order to identify the characteristics of properties with a significant influence over the analyzed context. The results show that heterogeneous real estate location related and physical characteristics such as type of real estate, existence of an elevator, thermal insulation, finishing works and floor area are significant variables that influence real estate prices in Romania. Moreover, the paper offers a database in the form of descriptive statistics for asset pricing, in this case residential single-family properties, the same as for the Gross Income Multiplier. This represents a starting point in developing a statistical basis on which future studies can attempt to explain the pricing differences observed in real estate.

Key words: Emerging market, real estate, appraisal, influential factors.

INTRODUCTION

Real estate market represents the largest market in developed European and worldwide countries, estimated to 30% - 40% of the value of all the underlying physical capital (Fabozzi et al., 2010). In recent years this has also been the case in emergent countries, where the real estate bubble sometimes exceeded the levels attained in developed countries.

Real estate appraisals have been requested in recent years to secure (mortgage) financial debts, assets financial reporting, tax and/or insurance estimations, sales transactions and estate planning situations. Mortgage valuation was one of the privileged objectives of assets appraisal. As a result, we may consider that the real estate market and valuation play a role in assuring banks’ well-being and are connected with the economic crisis due to banks’ over-exposure to a real estate property boom. Thus, the quality of mortgage valuation is critical; correlated with the possibility of auction sale in case of default and, in a depressed market, it may help in seeking policy solutions to distress the banking industry, as shown for Nigeria in the study of Aluko (2007).

Reliable valuation information represents the foundation of investment management in general and it is of particular concern in real estate valuation. Regardless of its objective, considering that valuations are all connected to the market, the lack of market price information on the real estate market remains a problem for banks, public institutions, other organizations and individuals. Knowing the real estate selling prices and their influential factors may support investment decision making, both internal and external, by combining the profitability of different industries.

This research is the result of market data collection regarding real estate, which has been statistically processed in order to develop and interpret useful indicators for real estate appraisal. The case study is conducted on Romania, a European, former communist country, currently classified as an emergent market. Usually, emergent markets cover the former socialist countries in Central and Eastern Europe (CEE) and in East Asia, the new independent states of the Soviet Union and the developing countries in South-East Asia, Middle East, Latin America and Africa. In this study, we sometimes make comparisons with other emergent countries, in order to highlight the Romanian specific environment.

The first proposed objective of the research emphasizes the importance of the real estate market in the period between 2010 and 2011 compared to a reference period which presents the impact of the global economic crisis and in relation to the real estate characteristics. The second objective of our study is to obtain, using a fundamental base, market multiples useful for real estate appraisal. Finally, the third objective of the present research determined the manner in which market data regarding real estate appraisal was collected in relation to the logic behind a model meant to identify and measure the intensity of influential factors of real estate selling prices. This step is useful for applying market corrections regarding the relevant elements of the grid to those corrections specific to the sales comparisons method.

The findings of our research could present interest for real estate valuators and other stakeholders in the real estate market, as well as in the academic environment. Our research has the potential to serve real estate practitioners as it provides reference regarding residential real estate prices, the characteristics of real estate that significantly influence the actual market price and the Gross Income Multiplier (GIM). The same results could be useful, even with an educational aim, to price real estate assets through the sales comparisons approach and the adjustment grid method and by using a hedonic model based on the statistical technique General Linear Model (GLM).

The remainder of the paper is organized as follows: Section 2 contains a literature review considering the characteristics of real estate as an element of the valuation process in general, real estate market, valuation approaches and methods specific to real estate, respectively; section 3 presents briefly the elements that define the Romanian real estate market, which represents the case study of our research; section 4 presents the research design; section 5 contains the analysis results; the last section discusses the study contributions and presents the conclusions.

Real estate market and valuation approaches

Real estate market

From a theoretical perspective, real estate assets (and in particular residential real estate) are viewed as a combination of a consumption asset and a leveraged investment (Fabozzi et al., 2009). Real estate appraisal is different from the valuation of other types of assets given the differences in liquidity across their market and in the type of investors (Damodaran, 2002). Archer and Ling (1997) distinguish between three types of markets that determine real estate prices. They show property markets as the markets where asset-specific discount rates, property values, and capitalization rates are determined and they add space markets and capital markets. Space markets represent the markets where local market rents are present (i.e., the market for leasable space).

By combining the property and space market under the notion of real estate market, we could say that this market is less liquid than in the case of other assets, transactions occur less frequently, transaction costs are higher and there are fewer buyers and sellers. Another viewpoint shows that the assets are traded in illiquid, highly segmented and informational inefficient local markets (Clayton et al., 2009). The illiquid state of the real estate market has an impact on the availability of market data, and this problem becomes more severe in emergent contexts. As an exception the real estate market is much more liquid during economic booms or recessions (prices are rising or are depressed). Thus, the real estate market is an imperfect market, as the units offered for sale fail the product homogeneity test and each unit is unique. According to Case and Shiller (1989, 1990) quoted by Fabozzi et al. (2009) the housing market is inefficient due to serial correlation and inertia in housing prices, as well as in the excess returns.

Because the market value of a property is generally reflected in a range rather than a precise point, it is important to consider all factors affecting a property’s value (Berger, 2007). Considering the objective of our research, we refer to the sensitivity of the estate investments to local trends. Those local characteristics are critical when hedonic appraisal models are used, which represent one of our methodological issues, including for the case of residential real estate. Hence, local economic, demographic and geographic variables are taken into account (Abraham and Hendershott, 1996; Lamont and Stein, 1999, Ghysels et al., 2007). Berger (2007) offers examples of relevant local characteristic: demographic changes in the surrounding neighborhoods, the inflation rate, the strength of the local economy, and the amount of money and effort the owner has expended to maintain the property. Also, using the findings of Shiller and Weiss (1999), Fabozzi et al. (2009) show a greater risk for the financial stability of households due to geographic fluctuations in property. Finally, Blackley et al. (1986) offer strong empirical evidence of the heterogeneity of interurban pricing.[hl1] All this local specificities make the market more localized, with information asymmetric.

The selling prices of real estate are also affected by macroeconomic variables that could make the difference between countries. The rules applied to real estate pricing are characterized by diversity. This is caused by specific institutional frameworks that cover legal aspects (regarding property right and tax system), economic (business cycles of different length), social (specific levels of satisfaction of the demand for real estate) or individual conventions underlying the organization of the company (such as the duration of lease contracts) (Kucharska-Stasiak and Zelazowski, 2006). In what concerns legal aspects we could mention tax laws that have a serious impact on the real estate, mainly because of change in depreciation methods and tax rates on ordinary income and capital gains, change in local laws, respectively (such as zoning requirements, property taxes and rent control) (Damodaran, 2002).

Real estate valuation approaches

Uncertainty associated with the process of assets appraisal has led to the development of several approaches acknowledged by professional associations and legally unrestricted, approaches the valuator judges as a choice. Three approaches have been developed and they became classical due to their intense use, respectively the market, income and cost approaches, from which several valuations methods derived.

Real estate appraisal methods range from the direct sales comparison approach/ method to more complex discounted cash flow models. No consensus exists on what is the best valuation method. Damodaran (2002) supports the approach (method) of comparables. Others such as Sharpe et al. (1999), Brealey and Myers (2000) and Bodie et al. (2005) quoted by Chen et al. (2010), recommend mainly the discounted cash flows supplemented with leverage, tax, and other adjustments. Copeland et al. (2000) and Penman (2003) are in favor of using accounting numbers and analyst forecast of earnings in a framework known as ‘residual income valuation’ or the ‘excess earnings method’ (Chen et. al, 2010).

The market approach is widely considered the most appropriate approach for valuing residential real estate in an active market (Woezala et al., 1995). The approach based on market comparison is the most reliable when there is an active market which supplies a sufficient number of real estate sales for comparison, sales that can be independently verified by reliable sources (ASA, 2004). Moreover, this approach is best suited to, and is the most reliable in, the appraisal of single family homes. The market approach is also known as the sales-comparison approach, market-data approach or direct market comparison approach.

The market approach is similar if we consider its theoretical neoclassical microeconomic foundation, with the implicit markets model of Rosen (1974). This is because it relies on market efficiency and the similarity between a specific property and another recently traded asset (Payne and Redman, 2002). It starts from the assumption that there exists a comparable property that is fully let on a very long lease at a rent that is adjusted at the beginning of each year to reflect market conditions (Ward, 1982). According to Berger (2007), the market approach is based on the substitution principle, as the property subject to valuation is compared to comparable properties in a competitive market. Thus, the process of market value estimation is based on actions of real buyers and sellers in a marketplace, not on a hypothetical model.

The most frequently used method derived from the market approach is the sales comparison grid, which is used to justify the real estate value estimate. Between properties there are differences in income production, size, scale, location, age and quality of construction (Damodaran, 2002). Further, given the class prices indexes the issue of finding appropriate comparable arises. All of these have to be accounted for in order to conduct the comparison. Some of these adjustments are simple (for example differences in size) and others are subjective (for example differences in location).

More recently, hedonic pricing (multiple regression) models have also been used to complete the sales comparison method. The literature shows that the prevalent property valuation method, based on the research of Rosen (1974) and Rosen and Topel (1988) and further developed in papers such as DiPasquale and Wheaton (1994) or Mayer and Somerville (2000), is the one based on establishing a hedonic price index for a property with given characteristics. Regression approach as hedonic modeling implies the price as the dependent variable, while the independent variables are the elements causing differences in real estate value, such as vacancy rates, size and capacity to generate income (Damodaran, 2002). Roddewigg et al. (2006) indicate that linear multiple regression analysis has been considered in the last decades a tool to directly predict market prices and to determine adjustment factors when analyzing comparable sales. The same author shows that a fourth approach to value, or an alternative to the three traditional approaches, was taken into consideration although it is not widely used, except for mass appraisal assignments at most. Different hedonic models are available in the literature based on characteristics of assets which receive value and become similarities measures for real estate prices. A review of the literature on this subject was conducted in the study of Sirmans et al. (2005) which analyzes the hedonic pricing models of 125 empirical studies. The main conclusion of the study is that there are differences between the authors’ viewpoints regarding the extent and direction of the effect of certain characteristics of real estate (houses particularly). Some examples of studies conducted on emergent countries in which arises the critical need to find alternative valuation methods are ?ipo? and Crivii (2008) for Romania, Moschidis et al. (2008) for Cyprus, Anim-Odame et al. (2009) for Ghana or Kuburic et al. (2012) for Slovenia.

Borderline between the income and the market approach is the usage of a standardized value estimate, of certain multipliers. Such standardized value estimators are the Gross Income Multiplier (GIM) along with the size multiplier. The former represents a ratio tool that can be used in residential properties and can develop an indication of value by dividing the sale price (capital value) by the monthly rent (periodic income). This tool relies on consistency between the extraction and application of the ratio (Rattermann, 2006). GIM incorporates a part of the differences between properties such as scale, construction quality and location. It is determined regardless of the financing conditions, prior to debt repayments. It is based on the premise that in the same location, real estate has very similar growth and risk characteristics, the only remaining differences being related to the capacity to generate income (Damodaran, 2002). There have been attempts to estimate market indexes for classes of real estate investments. Thus, in the case of residential real estate we could mention Case and Shiller(1) who for the period 1970-1989 estimated an index for using actual transaction prices to estimate the value. This is only an example of multiplier established for developed countries. We cannot say the same for emergent countries, where the lack of such useful tools for appraisals is being felt.

The Romanian real estate market

In this paper we focus on residential real estate, at the level of the individual property, within a case study conducted on the Romanian real estate market, a European market. At this point, when the effects of the economic crisis are still being felt, we can state that the European real estate market is not homogeneous. The current and future situation of each member state depends on its initial status (needs, demographical trends, economic fundamentals), recent market correction, the national economy’s specific exposure to the crisis and the degree of corrective measures undertaken and their results (Kaklauskas et al., 2010).

Romania is a former communist country, currently classified as an emergent market. In the decades following the end of the Second World War until 1991, Romania was a country with absolute domination, the communist influence being extremely powerful. The role of the state in the society, including in the valuation culture, was significant. The period following 1991 is marked by the fall of the communist regime and the transition from a socialist economy to a market economy. It is the first phase of a transitional economy. The centralized institutional structures of the socialist economy disappeared, the mechanism price was reactivated and spontaneous business activity on the market was permitted. Commercial banks, financial institutions, capital market, trading and communication networks were to be formed and the legal framework have been permanently updated according to the instances and instruments of the new economic environment. In time, after almost ten years, it can be considered that the market economy was formed. After another ten years, it can be considered that the legal environment is consistent with the challenge of turning the economy into a functional market economy. In recent years the economy progressed and real GDP annually had a positive growth rate so that according to the World Bank’s Development Indicators Romania reports $179.8 billion for 2011 and it is classified as an upper middle income country. The current population is of 21.39 million people.

With reference to the Romanian real estate market, we could say that there is no central market place and the details of many transactions are not publicly available. Although investors require a common denominator such as property indices for assets valuation and income prediction, such indexes are not to be found in Romania. The information is not consistent and complete across valuators in a low information environment such as the Romanian one. However, there are uniform standards, in the form of International Valuation Standards imple-mented by all valuators members of the national professional association, ANEVAR, but there are differences regarding information availability in a unitary framework in comparison to developed countries that have various indices published by specific organizations, indices that highlight the performance of the real estate market. The history of the sale and rent transactions is recorded only by real estate agents, such as real estate brokers and appraisal practitioners who compile their personal databases. Aluko and Olaleye (2005) observe a similar situation regarding available market information in the case of Nigeria – another transitional country. Although there is available information on the market trend, the situation is different when it comes to independent transaction prices, which in most cases are confidential. Comprehensive data on property investment performance is difficult and costly to collect. The absence of market data makes appraisals difficult and subjective, thus the need to improve the recording and availability of transactions data, to compose historical data series (price indices) and a centralized database is justified. Aluko and Olaleye (2005) emphasize the importance of such a database, developed with the contribution of property valuation firms and property companies, designed to allow forecasting at national, regional and local market/city levels by sector. Likewise, Moschidis et al. (2008) show that, despite the real estate sector's importance for the Cypriot economy, there is not an official publication of real estate prices.

If we were to present the evolution of the Romanian real estate market in the last decade we could define three different periods. The first period begins in 2002 and ends in 2007, when prices grew significantly, also due to the fact that Romania was preparing to join the European Union (the accession took place in 2007). Then the prices plunged as a result of the economic crisis. After three years of powerful decline, 2008-2010, in the last part of 2010 the recovery of the real estate market started with positive signs for 2011. The slight recovery of the market is suggested by the growing number of transactions for all types of real estate, even with increasing prices. Furthermore, according to data from specialized reports such as the index price/rent deter-mined by Collier International (Collier, 2012), the value of the index increased from 153 in September 2008 to 163 in May 2010. Another indicator of the real estate market’s evolution is provided by the National Statistical Institute (INS) through residential property price indices. At national level, with the exception of the capital, in the fourth quarter compared to 2009 the indices were 91.59 for 2010 and 77.43 for 2011, respectively. The real estate agencies present the following trends compared to the previous year regarding the housing price in values adjusted to the inflation rate: -16.86% in 2009; -9.19% in 2010; -1.05% in 2011. In 2010 compared to 2008 there is a drop of 42% in the prices of real estate (apartments). We can provide some estimates regarding the evolution of apartments’ average price considering that there is no official reference at national level. In our estimation we used verified information from several sources. In 2006, before the real estate bubble reached its peak, the apartment price per square meter was approximately 1,350 Euros. In 2008 the price increases to 1,800 Euros but in 2010 it drops to 1,300 Euros and now the price per square meter is approximately 950 Euros. Likewise, the monthly rent for an apartment with 2 rooms sharply decreased from 600 Euros in 2008 to 350 Euros in 2010 and 300 Euros in 2012. This is market information. The interesting fact is the incongruity between these data which suggest a drop of 15-20% of the price and the data provided by INS which show an increase of approximately 8%[hl2] . The same slight difference in estimation can be noticed for the price of apartments if we compared the same information sources. These findings only come to support the need to develop a national database of selling prices and useful indexes for real estate appraisal.

[hl1]This paragraph is very rich in ideas, but the author should consider reorganizing the context, as the ideas are present.

[hl2]I tried to follow the rational of this topic. Where does the INS 8% increase appears?.

Maybe present a table to explain the described data.

RESEARCH DESIGN

Analysis model

This research has taken into account items which suggest the factors that reflect the perception of the real estate market participants when making the decision to sell or buy. Having in mind their expectations, we conducted a literature review and the results of this analysis were correlated with observations from the Romanian appraisal practice. These represent the theoretical fundament for applying a multi-criteria model suitable for an empirical investigation. The model is part of the hedonic category, is supported by descriptive statistics and is based on GLM technique.

The theoretical reasoning first allowed us to identify the market approach from the acknowledged valuation methods as the most implemented method in the case of residential real estate appraisals. Thus, after comparing the methods mentioned in the literature and part of the market approach, we focused on the adjustment grid method. Moreover, this is the most familiar method to Romanian valuation professionals. We aim to support this method by providing information regarding the location related and physical influential factors and the value of the corrections applied to the comparables. In addition to the implementation of the adjustment grid method, we are also in favor of appraisals based on market multiples, such as GIM. According to the literature the method is somewhere between the market and the income approach and completes the market analysis in order to estimate the value taking also into account future income expected from the valuated property. Determining GIM differentiated on real estate characteristics represents, along with selling prices, extremely useful reference for the valuation practice.

The literature review continued with the identification of empirical research which focused primarily on identifying real estate characteristics that influence selling prices the most (Fabozzi et al., 2009). In what concerns residential real estate and location related and physical influential factors, which are of interest to our study, earlier literature considered as several influencing factors of the real estate market participants’ perception on transactions prices. Zietz et al. (2007) refer to square footage, lot size, bathrooms, floor type, garage, exterior siding, sprinkler system, distance to city center, bedrooms. Other regression models include factors like location, storey, bedrooms, garage, outhouse (auxiliary buildings, facilities), detached, semi- detached, floor, state freehold, landscaping, gross internal floor area, plot size, tenure (Anim-Odame et al., 2009).

The results from this body of literature have been often conflicting as to the impact of a variable on selling price, and the meaning and importance of the significant variables. The interesting aspect is that in emergent countries the influence of all the analyzed elements statistically significant (?ipo? and Crivii, 2008; Anim-Odame et al., 2009). Previously we presented the real estate characteristics analyzed in the study of Anim-Odame et al. (2009), for which statistical significance was determined. The other model we referred to is developed in the study of ?ipo? and Crivii (2008) which focuses on the case of a Romanian city - Timi?oara, and reviews 164 transactions with apartments that where conducted during the first 8 months of 2008. The explanatory variables considered were: main neighborhoods of the city, number of rooms, net area, improvements made to the property, floor and comfort level. The study ascertains the significant influence of these variables on transactions prices. For these reasons, in the current research we aim to test significant characteristics that determine selling prices in the Romanian real estate market.

The current study analyses apartments with 1 or 2 rooms. The choice was determined by the availability of data, since transactions with these apartments have been more frequent; however, the unanimous opinions in the literature (Sirmans et al., 2005) according to which the number of bedrooms has a positive impact on pricing had a major influence as well. As a result we focused on the same type of residential real estate i.e. apartments and we considered the number of rooms the major characteristic that impacts the selling prices. Another argument in favor of this choice is connected to the fact that since real estate is not sold frequently, price indexes are available for classes of assets and risk parameters are estimated for these classes (Damodaran, 2002). This is the reason why our study is focused on residential real estate, more exactly single-family residence such as apartments.

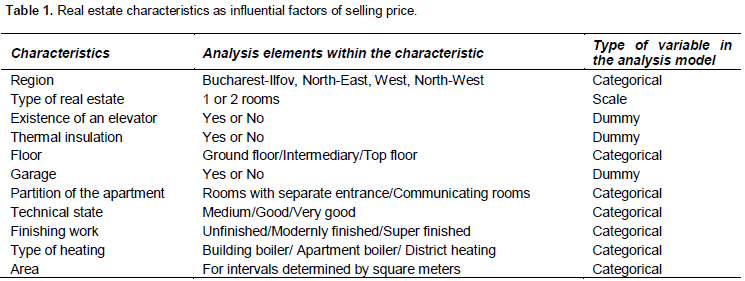

This research aims to identify the influential factors of selling prices, with an emphasis on physical and location related characteristics of real estate. In the hedonic model proposed in this paper we considered firstly the location related characteristics of real estate. Thus, region was the first characteristic, since regional differences are implicitly considered in the hedonic models. In this paper the notion region refers to the county capitals which denote the development degree of the real estate market, being thus conclusive for the whole region. We studied five cities, Bucharest (the capital of Romania), Iasi, Timisoara, Cluj-Napoca and Arad. This hierarchy is based on size, in decreasing order. Thus, we cover 4 regions of the country: Bucharest-Ilfov, North-East, West and North-West(2) . The second location related characteristic is the organization inside the city such as streets, neighborhoods and regions.

Taking into account the suggestions in the literature in correlation with the Romanian appraisal practice, physical characteristics are the factors that affect heavily the decision making about the value of real estate in Romania. Out of these we selected the factors that could aid the quantification of differences between properties. Those are mostly usual standard housing characteristics: property regime (number of floors), age of the building (year of construction), the existence of an elevator, exterior thermal insulation, level (floor), net area without balconies, area of the balconies/ledges, area of the loggia, area of the basement, garage, partition, technical condition of the apartment, finishing work and type of heating installation.

The model for which we collected data contains all the characteristics mentioned above, some of which we will not present in this research either due to lack of information in the data collection, or because of the smaller impact on the purchase and sale decision that we allocated. Thus, in the category untabulated statistics we included elements regarding the transaction date (month, year), location of the transaction (street, neighborhood, area), construction year, area of the balconies/terraces, area of the loggias/semi loggias, area of the basement, and the reliability degree of each transaction such as certainty, high reliability, medium reliability and doubtful reliability.

For the statistical processing we took into consideration 1 regional characteristic and 10 physical characteristics as presented in Table 1.

Tools and sample

Considering the objectives of our research, we used statistical tools adapted to the types of variables integrated in the proposed model and the relationships between the variables.

Thus, the processing of data in the real estate transactions sample started with univariate analyses that materialized in statistical description of data by elaborating a series of frequencies and determining parameters (mean and median, standard deviation, minimum, maximum, quartiles) and continued with statistical inference, by determining the limits of reliability intervals for the mean and proportion and by applying statistical tests (Buiga, 2001). Firstly, we collected descriptive statistics regarding the selling price in real estate transactions, as well as the rental price, but the latter are not detailed in the present research. Descriptive statistics are presented both in general and specifically, according to the real estate characteristics selected as relevant.

Further, in order to test distribution considering the probability law, from the tests suggested in the literature we selected the parametric concordance test developed by Kolmogorov Smirnov. This allowed us to study the normal distribution of real estate selling prices.

Finally, we considered relevant and we applied the multivariate analysis which enabled us to develop a model based on the General Linear Model (GLM) technique that led to the simultaneous study of the explanatory variables group related to variations in properties’ selling prices (Buiga, 2001). The model improves as the number of influential factors taken into account increases. For our model we considered the 10 physical characteristics of the analyzed residential real estate. The proposed analysis model is similar to hedonic models largely tested in prior research by means of linear multiple regression. We refer to the use of OLS regression and the more recent quartile regression (Zietz et al., 2007). The model we propose has the content of a hedonic model of prices which breaks down the real estate price into separate components that determine the price. Moreover, according to the characteristics of a hedonic model that does not necessarily separate all the factors that could be separated, but only those that affect the usefulness of what is being sold for a buyer, our model focuses on the physical factors of the real estate. The difference between our study and previously mentioned research is that we do not use regression, but GLM.

In order to study the dependency and association relations between transaction prices of real estate we used bivariate analyses considering the type of variables included in our model. Using the GLM technique, relevant influential factors of selling prices were identified and the influence of the identified apartment characteristics was thoroughly analyzed.

In order to prepare the database designed for the aim of our research we collected market information regarding real estate transactions made between midyear 2010 and midyear 2011, based on the developed analysis model. Although appraisals do not have a validity period and the market changes continuously, the results regarding real estate prices determined in our study for this period could be useful for current appraisals. This is also because, as Fabozzi et al. (2009) show, participants’ expectations regarding price on the local real estate market are strongly influenced by the most recent series of prices (Fabozzi et al., 2009). Also, our database can be adapted and used for the introduction in the hedonic model of the time of sales as a characteristic of the property and the estimations to be made at a single point in time.

The unit of analysis is represented by one and two room apartments, more exactly ‘buildings apartments’. The sample technique used is the non-probability sampling, the transactions being selected based on certain geographical areas, so as to be considered representative at regional level. Our option is consistent with the idea that when we work with case studies, the aim is not statistical generalization but rather theoretical generalization, and the selection doesn’t need to be probabilistic (Karlsen et al., 2008). We believe that the sample in our research is representative at a multiregional level as we surveyed four out of the seven development regions in Romania. The population studied contains 307 sales transactions that have been collected by interviewing real estate agents or representatives of real estate consultancy firms. In addition, data regarding 324 rent transactions has been collected and processed, but this data is only tangentially presented in the current research.

ANALYSIS RESULTS

Descriptive statistics regarding real estate selling price

General analysis of real estate selling prices

Table 2 presents the analysis of real estate transactions based on the selling price of properties selected as research object i.e. apartments with 1 and 2 rooms. The values have been adjusted to round numbers.

Table 2. Descriptive statistics regarding real estate selling prices.

The average transaction price for the analyzed apartments is 43,368 Euros, as half of the properties were sold at prices smaller than 42,500 Euros. The transaction values started from the minimum of 11,500 Euros and reached the maximum of 110,000 Euros, with a standard deviation of 14,143 Euros.

Taking into account the large variety of transaction prices and the standard deviation slightly over 30% of the mean, we find it useful to test the situation in which transaction prices are equally grouped around the mean in order to observe if there is a reference average value for the real estate market as a tendency situation for the analyzed transactions. Thus, the Kolmogorov-Smirnov test was applied to the set of transactions taken into consideration (Table 3).

The results of the test show that the distribution of transaction prices of properties around the mean is not perfectly balanced (after the test was conducted, the null hypothesis was accepted for a significance threshold of 5% which shows that the standard deviation of properties in relation to selling prices follows the normal distribution law).

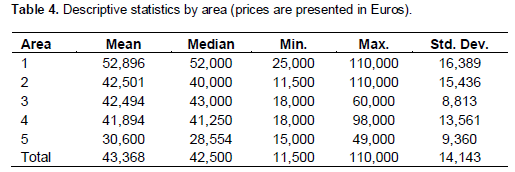

As we mentioned in the presentation of the sample, we considered an analysis conducted nationwide, as we selected representative regions in what concerns the development degree and assets as real estate transactions, respectively. Thus, we considered the capital cities for the selected four regions, identified as areas 1-5 (Table 4).

The statistics of transaction prices according to the regions in which they occurred suggest certain similarities between the real estate market in areas 2, 3 and 4 and a clear difference between the previously mentioned areas and the state capital, area 1. Thus, in the three mentioned areas the mean transaction value ranges from 41,894 Euros in area 4 and 42,501 Euros in area 2, while in area 1 the average transaction value is of 52,896 Euros.

Also, in what concerns areas 3 and 5 that are part of the same administrative classification as they represent North-West Romania, there is a significant difference between average transaction’ prices in area 3 compared to area 5 in the context of a similar standard deviation, which is at the same time different from the other regions. These findings suggest that an analysis of the sub markets within the development regions could lead to significant differences between different poles of activity (for example counties). This would mean that for more accurate valuations a careful segmentation of the market would be needed according to the characteristics of the valuation object on the real estate market[hl1] .

Analysis of the Gross Income Multiplier (GIM)

Untabulated statistics provide rental prices for the same periods and real estate characteristics as considered for selling prices in the previous section. Table 5 shows data regarding the average values of rent transactions for the general sample.

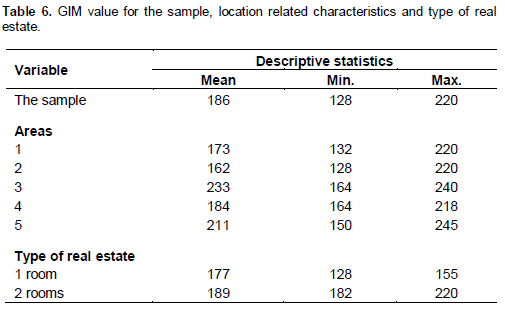

Untabulated descriptive statistics regarding rental prices according to real estate characteristics followed by their correlation with real estate selling prices allowed us to determine GIM, in general for the whole sample, and then separately for each type of real estate and location related characteristic (Table 6).

The values have been adjusted to round numbers.

The average rental price for apartments is 233 Euros and half of the analyzed rent transactions were concluded at prices lower than 215 Euros. Rental prices range from the minimum value of 90 Euros to the maximum value of 500 Euros, with a standard deviation of 86 Euros. Thus, the value range for GIM is a mean of 186, with the minimum of 128 and the maximum of 220. The GIM value for area 4 comes close to the general mean, and areas 3 and 5 represented by cities with smaller population show the highest value of the multiplier. GIM has a higher value for two room apartments but not much different, in terms of mean, from the value for one room apartments.

Analysis of the influences of real estate characteristics on the selling price

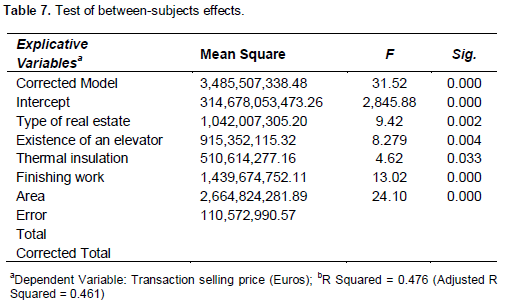

In order to identify the influence of and correlation between different characteristics of real estate and the value of the transaction (in a data series with no numeric values for these characteristics, but only categorical or dummy variables), we used the General Linear Model (GLM). In other words, we aimed to identify those characteristics of real estate that influence the transaction values the most. The applied tests are presented in Table 7, after eliminating the insignificant variables from the model (Sig.?0.05).

We notice that the transaction value depends upon the type of real estate, the existence of an elevator, thermal insulation, finishing work and area. Although the descriptive statistics showed a difference in perception of the parties involved in the transaction of apartments with 1 or 2 rooms as regards the floor, the existence of a garage, the partition of the apartment, technical state, type of heating system, these variables did not prove to be statistically significant in what concerns their influence on the transaction price.

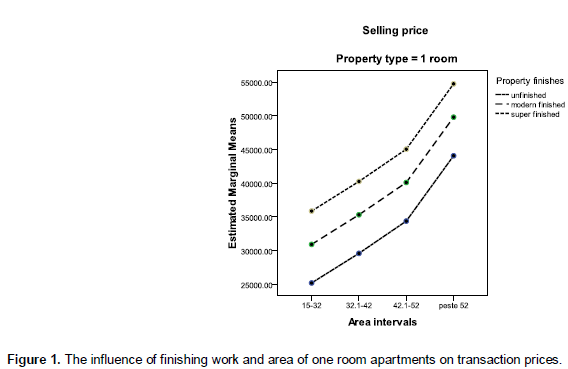

The analysis was furthered for the characteristics with the highest statistical significance (Sig.=0.000). Two of the characteristics which presented a significant influence over the transaction price (finishing work and area) have been analyzed in correlation. The transaction price was considered a dependent variable differentiated by the number of rooms of the apartment (Figure 1).

The average transaction value estimated for apartments with one room is increasing relatively constantly and similar from one floor area range to another, depending on the degree of finishing work. The higher ascending evolution for the last area range (over 52 square meters) is due to the fact that within this range several sub intervals are included (the explanation is previously detailed in the descriptive statistics regarding the area of the apartment) (Figure 2).

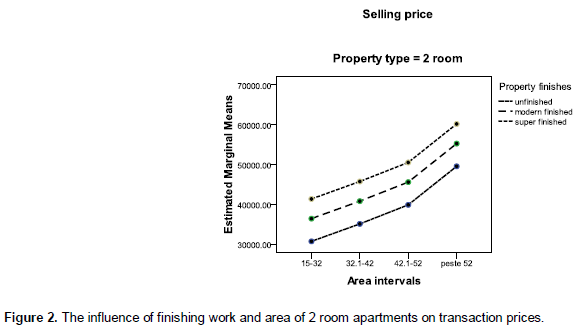

The evolution of the average transaction value for apartments with two rooms is similar with the evolution of the average transaction value for apartments with one room, increasing relatively constantly and similar from one area range to the next, depending on the finishing degree, providing in both cases a justified starting point in the absolute and relative estimation of finishing work value on the considered intervals.

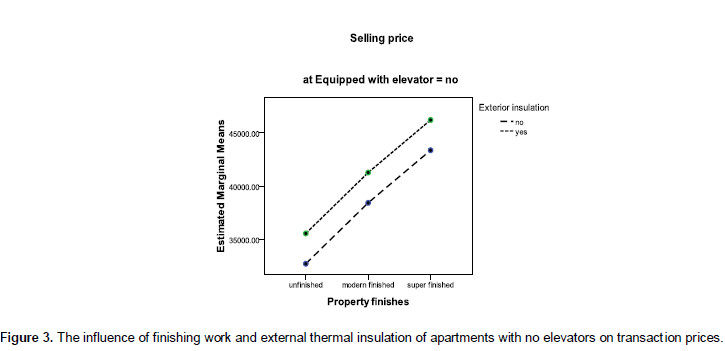

Furthermore, we tested the cumulative influence of other characteristics that have proven to be significant (finishing work, existence of an elevator and external thermal insulation) on transaction prices (Figure 3).

The average transaction value for apartments situated in buildings with no elevator has an upward trend from one degree of finishing work to the next, in the case of the three analyzed levels of finishing work, depending on the existence of exterior thermal insulation. If the apartment building has no elevator there is a difference in the increase of the average transaction value estimated because, as the graph shows, if the apartment has no thermal insulation, there is no elevator, but the apartment is super finished then the line representing the evolution of the average transaction value is smoother than in the case of apartments with thermal insulation. In other words, super finished apartments with no elevator are more sensitive to price change than the other two categories (considering finishing work) depending on the existence of external thermal insulation (Figure 4).

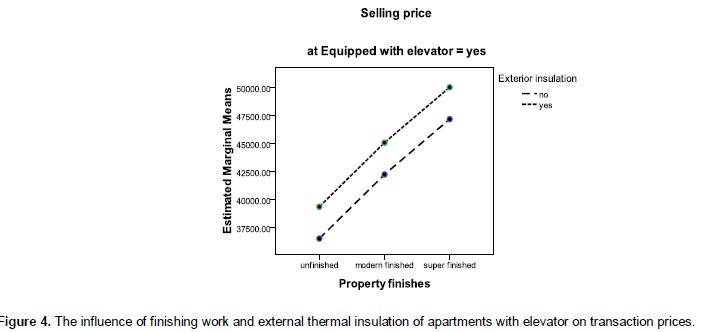

The average transaction value for apartments with elevators is ascending and somewhat similar across the levels of finishing, in the presence or absence of external thermal insulation (the line showing the evolution of the average transaction value for apartments with elevators is slightly more inclined in the presence of thermal insulation). Super finished apartments with elevators show a surprising evolution considering the existence or absence of thermal insulation. Super finished apartments with elevators but no thermal insulation are estimated to be sold at higher values than apartments with external thermal insulation. This evolution is hard to explain in the absence of market information and furthermore it is difficult to correlate it with the expected evolution for unfinished and modernly finished apartments. Market information could refer to specific situations of certain types of apartments and/or regions/markets or sub-markets, such as, for example, the apartment buildings developed prior to 1989 (buildings with an average age) and given into use before elevators were installed in buildings – in these situations elevators were installed with the effort of the owners, in certain cases many years after the building was given into use. Because the expenses for elevators to be installed in the buildings were borne by the owners, their expectations regarding the transfer price could be optimistic, especially if there are similar apartments on the market (possible with higher height classification) in buildings where elevators where not installed.

CONCLUSION

This research offers empirical evidence regarding average selling prices, GIM and real estate characteristics, for the period between midyear 2010 and midyear 2011 using a representative sample for Romania. From this point of view it can be considered the starting point for developing a statistical database on which future studies can attempt to explain the observed pricing differences for real estate. Thus, the findings are relevant for valuation companies, valuators and authorities. Finally, our paper pleads for the disclosure of real estate prices and other information regarding real estate characteristics in the Romanian market by an official authority. Moreover, the results of our research could be applicable in other emerging economies, especially in CEE countries, if there is a system that records transactions and the market conditions are similar. Also, it can represent a reference for assets valuation based on market approach in an emergent context, as several European studies revealed the difficulty of cross countries comparisons due to different valuation approaches applied (Maestri, 2013).

The present research sub-serves in demonstrating the importance of justifiable corrections. Our research focused on identifying real estate characteristics that could potentially influence the purchase and sales decision and consequently are analysis criteria within the market approach and sales grid method[hl1] . The study focuses on apartments with 1 and 2 rooms respectively and their location related and physical characteristics. Thus, their influence over prices was identified in order to provide future reference for appraisals. Identifying influential factors of selling prices and arranging them in a hierarchical system according to their statistical signifi-cance facilitates legitimate measurement of corrections applied to transaction prices in order to modulate and estimate the value of a given property. This eliminates arbitrary measures and distortion of valuation results. Practitioners and theoreticians alike may follow rigorously the analysis method, especially the test of highest and best use and the selection of comparables; they may determine adjustments acknowledged by the market; they may realize the applicability and limits in the process of estimating corrections; they may find it useful in the process of defining different market segments as value area and market perception; they may provide professional advice regarding the market segment for our analysis object i.e. apartments with 1-2 rooms. The hedonic model used is based on GLM statistical techniques and allows for the systematic application of valuation approaches in order to identify and analyze real estate prices.

Another contribution is that our study supports the empiric substantiation of the Gross Income Multiplier (GIM), a concept considered subjective by real estate valuators. Along with selling prices the results of our research present the net returns for apartments with 1 and 2 rooms as types of real estate, based on data provided by the most important players on the market i.e. real estate agencies and real estate consultancy companies. It provides details regarding GIM values in general for the whole sample and then differentiated according to the type of real estate and location related characteristics. Thus, average values for GIM in an emergent context for the period 2010-2011 could be extrapolated and used in the capitalization approach of residential real estate (apartments) valuation. It is a contribution for a certain segment of the real estate market, and with further investigation the evolution of this important parameter of real estate value could be studied in time.

The results of this research should be interpreted in light of a number of limitations, some of which leading to research perspectives. Firstly, a larger sample of real estate transactions could be useful in order to further our findings. Future research could extend the analysis in relation to macroeconomic and sectorial variables such as economic growth, population income, demographic evolution, cost of utilities, competition specific to real estate market, or infrastructure projects that could influence certain real estate markets or major real estate projects. Also, some limitations of this research are determined by the use of a hedonic model, as it is well known that the methods associated with hedonic indices inherit all the common problems known for multi-criterial analysis, mainly multi collinearity and model selection. Moreover, we would like to suggest the possibility of investigating other potential influential factors than those analyzed in this paper location related and physical characteristics. Finally, the investigation was conducted in a single country, narrowing thus the international relevance of its results.

Notes

(1) The S&P/Case-Shiller Home Price Indices are the leading measures for the US residential housing market, tracking changes in the value of residential real estate both nationally as well as in 20 metropolitan regions. Read more at http://www.housingviews.com/

(2) The development regions represent eight statistical measures, with no legal personality, created in 1998 through the Association of County Councils in Romania, in order to coordinate the regional development required for Romania’s accession to the European Union.

[hl1]The applied test does not measure influences in the purchase and sales decisions, but characteristics that are higher or lower valued as price. It lacks also the ability to price those characteristic.

An interesting analysis would be to compare the GIM and the tax rates investor could have on governmental bonds or in the Romanian risk free rate. If investment on real estate proprieties provide higher returns than risk free rate, it would have a positive impact in the willing decisions of buyers and sellers and the overall market would go up.

CONFLICT OF INTERESTS

The authors have not declared any conflict of interests

REFERENCES

|

Abraham JM, Hendershott PH (1996). Bubbles in metropolitan housing markets. J. Housing Res. 7:191–207. http://dx.doi.org/10.3386/w4774 Crossref |

||||

| Aluko BT (2007). Accuracy of auction sale caluations in distressed bank lending in Nigeria. J. Bus. Econ. Manag. 8(3):225-233. http://dx.doi.org/ 10.1080/16111699.2007.9636172 | ||||

| Aluko BT, Olaleye A (2005). Unitization and securitization of property investment: Implications for future valuation. J. Bus. Econ. Manag. 6(3):125-134. http://dx.doi.org/ 10.1080/16111699.2005.9636101 | ||||

| American Society of Appraisers (ASA) (2004).Valuing machinery and equipment. Bucharest. ANEVAR 2000 translation. | ||||

| Anim-Odame WK, Key T, Stevenson S (2009). Measures of real estate values from land registration and valuation systems in emerging economies: the case of Ghana. J. Real Estate Lit. 17(1):63-84. | ||||

|

Blackley DM, Follain JR, Lee H (1986). An evaluation of hedonic price indexes for 34 large SMSAs. Amer. Real Estate Urban Econ. Assoc. J. 14(Summer):179-205. Crossref |

||||

| Buiga A (2001). Metodologia de sondaj ÅŸi analiza datelor în studiile de piaţă [Survey methodology and data analysis in market studies]. Ed. Presa Universitară Clujeană. Cluj-Napoca. Cluj. | ||||

|

Chen F, Yee KK, Yoo YK (2010). Robustness of judicial decisions to valuation-method innovation: An exploratory empirical study. J. Bus. Financ. Account. 37(10):1094–1114. http://dx.doi.org/10.1111/j.1468-5957.2010.02193.x Crossref |

||||

|

Clayton J, Ling DC, Naranjo A (2009). Commercial real estate valuation: fundamentals versus investor sentiment. J. Real Estate Finance Econ. 38:5-37. http://dx.doi.org/10.2139/ssrn.2087383 Crossref |

||||

| Collier International (2012). Research and forecast report mid-year 2012, Romania. available at: http://www.colliers.com/~/media/files/emea/romania/research/romania/2012-h1-romania-research-report.ashx (accesed 5 january 2013). | ||||

| Damodaran A (2002). Investment valuation – Tools and techiques for determining the value of any asset. 2nd edition.Wiley Finance. New York, NY. | ||||

|

DiPasquale D, Wheaton W (1994). Housing market dynamics and the future of housing prices. J. Urban Econ. 35:1–27. http://dx.doi.org/10.1016/S0166-0462(04)00015-8 Crossref |

||||

| Fabozzi FJ, Shiller RJ, Tunaru RS (2010). Property derivatives for managing European real-estate risk. Euro. Finan. Manage. 16(1):8-26. http://dx.doi.org/10.2139/ssrn | ||||

|

Ghysels E, Plazzi A, Valkanov R (2007). Valuation in US commercial real estate. Europ. Finan. Manage. 13(3):472-497. http://dx.doi.org/10.2139/ssrn.937800 Crossref |

||||

| Kaklauskas A, Zavadskas EK, Bagdonavicius A, Kelpsiene L, Bardauskiene D, Kutut V (2010). Conceptual modelling of construction and real estate crisis with emphasis on comparative qualitative aspects descriptions. Transformations in Business and Economics. 9(1):42-61. | ||||

|

Karlsen TJ, GrÓ•e K, Massaoud MJ (2008). Building trust in project-stakeholder relationships. Baltic J. Manage. 3(1):7-22. http://dx.doi.org/10.1108/17465260810844239 Crossref |

||||

| Kuburic M, Tomic H, MastelicIS (2012). Use of multicriteria valuation of spatial units in a system of mass real estate valuation. Preliminary Communication. KiG 17(11):59-74. | ||||

| Kucharska-Stasiak E, Zelazowski K (2006). Implementation of international standards in an emerging market – threats and opportunities: The case of Poland. Valuation J. 1:37-55. | ||||

|

Lamont O, Sten J (1999). Leverage and house price dynamics in US cities. RAND J. Econ. 30:498-514. http://dx.doi.org/10.3386/w5961 Crossref |

||||

|

Maestri V(2013). Imputed rent and distributional effects of housing-related policies in Estonia, Italy and the United Kingdom. Baltic J. Econ. 13(2):35-58. http://dx.doi.org/10.1080/1406099X.2013.10840532 Crossref |

||||

|

Mayer C, Somerville C (2000). Residential construction: using the urban growth model to estimate housing supply. J. Urban Econ. 48:85-109. http://dx.doi.org/10.1006/juec.1999.2158 Crossref |

||||

| Moschidis OE, Livanis S, Lazaridis IT (2008). Investigation of criteria used by Cypriot real estate agents in the decision-making for the valuation of real estate market – empirical research findings. J. Finan. Manage. Anal. 2(2):36-46. | ||||

|

Payne TH, Redman AL (2002). The pitfalls of property valuation for commercial real estate lenders: Using a comparative income approach to improve accuracy. Briefings Real Estate Finance. 3(1):50–59. Crossref |

||||

| Rattermann MR (2006). Considerations in gross rent multiplier analysis. Valuation J. 1:59-71, republished by The appraisal institute 2006, summer. | ||||

| Roddewigg RJ, Frey JD (2006). Testing the reliability of contingent valuation in the real estate marketplace. The Appraisal Journal. Summer:267-280. | ||||

|

Rosen S, Topel R (1988). Housing investment in the United States. J. Polit. Econ. 96:718-740. Crossref |

||||

|

Rosen S (1974). Hedonic prices and implicit markets: product differentiation in pure competition. J. Polit. Econ. 82:34-55. http://dx.doi.org/10.1086/260169 Crossref |

||||

| Sirmans GS, Macpherson DA, Zietz EN (2005). The composition of hedonic pricing models. J. Real Estate Lit. 13(1):3-46. | ||||

| Șipoș C, Crivii A (2008). A linear regression model for real estate appraisal. Valuation J. 2(5):49-57. | ||||

|

Ward CWR (1982). Arbitrage and investment in commercial property. J. Bus. Financ. Account. 9(1):93-108. Crossref |

||||

| Zietz J, Zietz E, Sirmans GS (2007). Determinants of house prices: A quantile regression approach. Middle Tennessee State University. Department of Economics and Finance. Working Papers Series. May 2007, available from: http://www.mtsu.edu/economics/FacPapers/Quantile_Reg_working_paper.pdf (accessed 10 November 102012). | ||||

Copyright © 2024 Author(s) retain the copyright of this article.

This article is published under the terms of the Creative Commons Attribution License 4.0