ABSTRACT

The measurement of marketing function is vitally important to establish the performance of the brand. The aim of this study is to investigate the marketing performance measurement practices in the Hatfield Volkswagen group with reference to the following elements: the awareness of the importance of effectively measuring the marketing activity, the satisfaction with the current marketing performance measurement, the marketing performance measures considered by the company’s top management, the timeframes of gathering of the marketing performance measures, the significance that top management attaches to the marketing performance measures, the different kinds of benchmarks used to extract meaning from the marketing performance measurements, the measurement and timing thereof of the marketing asset and the challenges if any faced by the managers. The data represents the extent and status of the marketing measurement and evaluation in the Hatfield Group, by examining each departmental manager’s understanding, perception and challenges towards measurement and evaluation of marketing performance. Findings indicate that departmental managers are unsure about the measurement methods needed to determine the performance value of their marketing efforts. Top management measures the success of marketing with “financial measures” and place very little significance on non-financial measurements.

Key words: Marketing performance measurement, measurement practices, methods and time frames of measurement, brand performance, sustainable demand, and marketing asset terminology.

In order for any business, including a motor dealership, to be effective in marketing it has to advertise, promote and sell products and services, as well as interact through public relations, for these activities to be successful an investment is required to stimulate the demand for these products and services. Furthermore, the business requires a return on the funds that were invested. All companies have a primary goal of achieving maximum profits to increase shareholders’ wealth by generating the optimum return from their capital initially invested in the business (Shim and Siegel, 2007). Dealerships meticulously examine ways to increase income and decrease expenses and measure all the pertinent performance indicators to develop strategies to increase the return on investment. In relation, marketing practices should be measured with the same vigour. Papageorge (2005) states the importance of marketing, explaining that historically, the measurement of the marketing activities in South African companies has not been adequate and therefore marketing remains largely unmeasured. If the marketing function is better analysed and measured, this should assist in increasing the reach and success of advertising, promotion, selling and public relations, which should in turn, increase the return on the marketing expense.

The aim of the paper is to assist dealers in the Hatfield Volkswagen group to evaluate the marketing performance through exploration of management and the understanding of the marketing performance measures, the ability of management to measure marketing performance, the current measurements in place and the challenges in the adoption and implementation of marketing performance measurement and evaluation.

BUSINESS MANAGEMENT IN PERSPECTIVE

Business management involves the detailed analysis and understanding of enterprise with the objective of establishing the most efficient way to manage the enterprise (Le Roux et al.,1998). Business management is a science that examines and analyses the internal and external processes and procedures of a business enterprise. Nieuwenhuizen and Rossouw (2008) define management as the process of integrating and combining the precise measures of each factor of production available to them in a way that these achieve the objectives and goals of an organisation. This includes realising a profit and satisfying the needs of the society.

Marketing is fundamental to business as it establishes what the customers’ desires are and then directs the resources towards fulfilling these needs. Cant (2010) states that marketing has transformed from being a ‘making a sale’ practice to having the objective of satisfying the customer needs. Cant (2010) continues by arguing that in the marketing process, the act of exchange wherein people surrender something in order to receive something that they desire is of central importance. Boone and Kurtz (2009) emphasise that marketing embraces a broad spectrum of activities and is therefore not easy to define. The concept of marketing therefore encompasses all the activities that are entered into with the sole purpose to satisfy the customers’ needs and to obtain a return on the investment out of the activity (McPheat, 2010). Marketing according to McPheat (2010) has a direct influence over advertising, promotions, public relations and sales. When a company engages in marketing, time and money is spent, and as with any other expense in a company, there should be fair returns.

Woodburn (2005) states that marketing has traditionally been seen by companies as a function that is not accountable, and that it is an expensive way of communicating with customers. Marketers have traditionally avoided measurement of the marketing activities. However, in recent times this has changed with companies dissecting each function in the business with the sole purpose of extracting and maximising shareholders’ value. Senior management expect that management and marketers deliver a return on marketing activity as an intangible asset in order to increase shareholder value (Walker et al., 2004). Performance measurement needs to be broadened by not only measuring the financial outcome, but by encompassing a measurement of resources, processes, products and services and finally, financial deliverables. As motor dealerships and companies are under more pressure to deliver improved shareholder returns, management is expected to measure and contain all expenses and to increase income streams. In order to achieve this, management is required to measure and evaluate the performance of all areas of the business. Performance measurement is not a new business tool but rather a term and science that found relevant prior, with Kelvin who described the importance of measurement when he states (Shane, 2007):

“… I often say that when you can measure what you are speaking about, and express it in numbers, you know something about it; but when you cannot measure it, when you cannot express it in numbers, your knowledge is of a meagre and unsatisfactory kind…”

THE IMPORTANCE OF MEASUREMENT IN AN ORGANISATION

Measuring all activities of organisations has been an accepted and much debated practise for a long period of time. Kennerly and Neely (2003) state that terms such as “[w]hat gets measured gets done” and “[y]ou get what you measure” have indicated that companies should measure activities and implement the results into their objectives and strategies. In order to remain relevant, measurement systems should be updated and reviewed on an ongoing basis, but yet it seems that few companies have processes in place to ensure the applicability of performance management methods and systems aligned to the objectives of companies. Previous studies have exposed the positive link between a company’s ability to measure marketing activity and the performance of the company (O’Sullivan and Abela 2009).

Accenture (2001) conducted a study that exposed that three quarters of marketing managers in the USA and the UK are unable to calculate and indicate the ROI on a specific marketing campaign that they ran. The study emphasises that some of the reasons behind this is the inability of companies to integrate their sales, marketing and customer services tools. The analysis of data was emphasised further by the fact that 65% of the marketing managers find it difficult to integrate customer data throughout the company to establish a single view of a customer. Porter (2008) indicates that the competitive advantages of a company cannot be established by holistically analysing the company, but rather by dividing and measuring each activity of the company. The results can then be evaluated to establish the performance of each activity and the interrelationships between each activity.

MARKETING AND FINANCIAL PERFORMANCE

Financial analysis assists in measuring and identifying the strengths and weaknesses of a business and ultimately the sustainability of the organisation over time. The financial analysis consists of financial ratios that indicate and determine the relationship between the company’s activities such as current assets in relation to sales (Kretlow et al., 2006). The main reasons Sexton (2009) found for the slow progress made with the measurement of marketing return are the following:

1. Absence of understanding what marketing return constitutes. In many companies the managers reported that their company does not define the marketing return or ROI.

2. Shortage of time and resources dedicated to the marketing return. Many companies have not yet developed systems to measure the marketing return and therefore are not allocated time to the advancement of internal evaluation and measurement techniques.

3. Little motivation for staff to contribute to the marketing return measurement. The remuneration systems in companies do not encourage work on marketing measurement and return.

4. Shortage of skills and resources. Companies do not have the skills and resources internally to allocate to the research of marketing return and measurement or are reluctant to apportion it to the research.

5. Absence of collaboration between the marketing and finance departments. The marketing and finance functions seem to operate in separate silos and therefore there is no impetus to advance the understanding and improvement of marketing measurement.

6. Inertia. The managers in companies do not feel the need to change their current method of operation, neither have they the time to change.

The measurement of the marketing function continues to become more and more challenging because several factors, such as the highly competitive nature of markets and competitors, well-informed and educated customers, rapid advancement of technologies, development of new industries and new industry leaders.

MARKETING AND FINANCIAL PERFORMANCE

Financial analysis assists in measuring and identifying the strengths and weaknesses of a business and ultimately the sustainability of the organisation over time. The financial analysis consists of financial ratios that indicate and determine the relationship between the company’s activities such as current assets in relation to sales (Kretlow et al., 2006). The main reasons Sexton (2009) found for the slow progress made with the measurement of marketing return are the following:

1. Absence of understanding what marketing return constitutes. In many companies the managers reported that their company does not define the marketing return or ROI.

2. Shortage of time and resources dedicated to the marketing return. Many companies have not yet developed systems to measure the marketing return and therefore are not allocated time to the advancement of internal evaluation and measurement techniques.

3. Little motivation for staff to contribute to the marketing return measurement. The remuneration systems in companies do not encourage work on marketing measurement and return.

4. Shortage of skills and resources. Companies do not have the skills and resources internally to allocate to the research of marketing return and measurement or are reluctant to apportion it to the research.

5. Absence of collaboration between the marketing and finance departments. The marketing and finance functions seem to operate in separate silos and therefore there is no impetus to advance the understanding and improvement of marketing measurement.

6. Inertia. The managers in companies do not feel the need to change their current method of operation, neither have they the time to change.

The measurement of the marketing function continues to become more and more challenging because several factors, such as the highly competitive nature of markets and competitors, well-informed and educated customers, rapid advancement of technologies, development of new industries and new industry leaders.

BUSINESS PERFORMANCE MEASURMENT

In order for companies to be successful and to gain competitive and sustainable advantages, it is necessary to design and implement performance measurement systems and structures. Therefore, it is important to

measure and evaluate every function in the business with the objective to increase efficiency and ultimately profitability and business success (Taticchi, 2010). Eusibio et al. (2006) state that, notwithstanding the importance of business performance and the pressure on companies to measure the inputs, there has been little research done on the measures implemented to ensure marketing effectiveness.

Marketing performance measurement

Ambler and Robert (2008) define marketing as the actions the company as a whole engage in with the intent to create shareholder value. Therefore, it is not the performance of the department or a specific marketing activity but the company’s overall performance and achievement with regard to marketing that makes the enterprise successful. In order to evaluate the performance of marketing, it is necessary to adhere to three criteria namely a comparison to internal benchmarks, external benchmarks and adjustments for any variation in brand equity (Ambler et al., 2001; Mills, 2010).

Internal benchmarks

Measurement of performance has become essential to senior management in companies that are responsible for strategic and operational decisions. This has brought about the use of benchmarks to compare best performance in business (Jin et al., 2013). Marketing or business plans are generally considered as an internal benchmark for performance (Mills, 2010).

External benchmarks

The external benchmarking process compares the company’s performance against that of successful companies or competitors. No matter how good the performance of a company’s internal process and performance, it should always benchmark outside its environment against competitive forces and companies in order to ensure continued improvement (Stapenhurst, 2009).

An exploratory research was completed by Kokkinaki and Ambler (1999) regarding the current practices of marketing performance assessment as part of the Marketing Metrics project.

The research revealed that marketing performance measurement should be done in accordance with the following classifications:

1. Financial measures such as sales volume and turnover, profit, returns of capital.

2. Competitive market measures such as market share,

share of voice, relative price and share of promotions.

3. Consumer (end user) behaviour measures such as penetration and number of users and consumers, user and consumer loyalty and user gains and losses.

4. Consumer (end user) intermediate measures such as awareness, attitudes, satisfaction, commitment, buying intentions and perceived quality.

5. Direct customer (trade) measures such as distribution or availability, customer profitability, satisfaction and service quality.

No research was found on the marketing performance measurement of South African motor dealerships. Moerdyk (2010) does however state that in South Africa companies’, effective measure of the performance of the marketing function is scarce and as a result, company executives are becoming more aware of the importance thereof. Moerdyk (2013) emphasises the fact that research has shown that 20% of all advertising fails in South Africa and that the only way of establishing the success of marketing performance is to measure it.

The objective of this study, from a managerial perspective, is to examine the extent to which marketing is evaluated and measured in the Hatfield Volkswagen Group, and to discover the dimensions utilised in the current process. In the larger study objectives were group under the following categories:

1. Demographics

2. The extent of management awareness

3. Satisfaction of management

4. The current marketing performance measurement practice

5. Importance attached by top management

6. Benchmarks used

7. Marketing performance measurement practices

8. Challenges that the managers confront.

For the purpose of this study, selected variables from all categories are dealt with.

Zikmund and Brabin (2013) define marketing research as the application of a certain scientific method in order to discover the factual truths about marketing phenomena. They continue by stating that effective marketing research decreases uncertainty, and assists in achieving the marketing decision making process. The main objective of this study, from a managerial perspective, is to examine the extent to which marketing is evaluated and measured in the Hatfield Volkswagen Group and to discover the dimensions utilised in the current process. The research objectives of the study are:

1. To analyse the extent of management awareness of departmental management with regards to marketing performance measurement.

2. To measure the satisfaction of management with existing marketing performance measurements.

3. To assess the current marketing performance measurement practice with regard to measure collection.

4. To consider the importance that top management attaches to marketing performance measures.

5.To assess the benchmarks used in marketing performance measurement,

6. To gauge the marketing performance measurement practice with regard to the organisations “marketing assets”.

7. To explore the challenges that the managers confront in measuring marketing performance in the motor industry and specifically inside the Hatfield Volkswagen Group dealerships.

Research hypotheses

Weathington et al. (2012) define the hypothesis of research as a particular expectation about the relationship between two or more variables based on theory or earlier research. The expectations are made with the purpose of achieving the research objectives. The six categories identified to measure marketing performance are financial measures, competitive market measures, consumer behaviour measures, consumer intermediate measures, direct customer measures and innovativeness measures. With regards to the objectives the following hypotheses were formulated in Table 1.

The sample framework

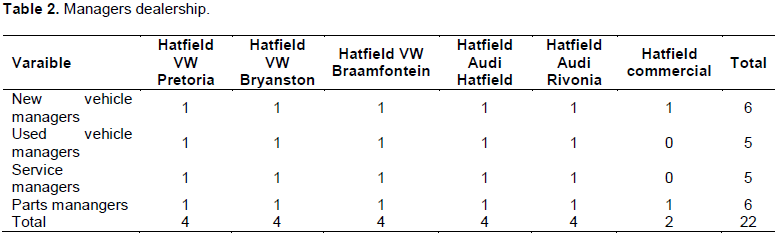

The population of study consists of all the managers of retail franchised motor dealerships. A purpose sampling strategy was used. A sample of 22 managers that are perceived to be experts were interviewed. Given the nature of this study, a sample size of between five and twenty was considered adequate (Zikmund, 2003). The researcher selected the respondents. The population in the research consisted of the departmental managers in motor dealerships within the Hatfield Volkswagen Group (Table 2). In the study, the departmental managers of the dealerships were selected through the purposive expert sampling method.

An online survey engine, Survey Monkey’ was utilised and the respondents received an email with information on the study as well as a link to the survey. The answers of the study were downloaded in a Microsoft Excel spreadsheet. Web-based surveys are infinitely more time efficient than email or telephonic surveys, when the respondents are initially contacted through email (Schonlau et al., 2002). In order to ensure a high response rate, the managing director of Hatfield Holdings sent the email directly through to the respondents and requested their co-operation. The response rate was 100%. The research needs to be reliable in such a way that it is understandable to the reader, and that further research can be done using the same method and can confidently produce the same results; or that the reader is confident in the results (Greener, 2010).

The data collected throughout the research is trustworthy, reliable and valid if the information answers the research questions, describes the sample and population and it can be related to individuals outside the study. Every step of the research process influences the trustworthiness and validity of the survey. In this study care was taken to be honest and thoughtful throughout the research study. In this partially replicated study, the same descriptive statistics were used as in Kokkinaki and Ambler (1999) and Mills (2010) study (skewness and kurtosis, frequency distribution, cross-tabulation and mean. The results of the survey conducted amongst the departmental managers in motor dealerships within the Hatfield Volkswagen Group were discussed.

Demographics

The respondents in the study were not requested to provide race, age or gender. 91% of the respondents represented dealerships of medium (less than a 100 employees) or large (more than 100 employees) sizes. The remaining 9% were from small (less than 50 employee) dealerships. A summary of the research findings revealed the following:

1. Comparison to the criteria for appropriate marketing performance measurement: The majority of respondents (77.3%) were aware of the importance of measurement of the marketing activity (aware, 45.5%; very aware 31.8%). Only 13.6% were completely unaware and 9.1% “neither unaware nor aware. A quarter of the departmental managers therefore conducted formal marketing performance measurement practices which consist of comparing the marketing performance measurement against internal and external benchmarks, and included the marketing asset and brand equity into their measurement process.

2. Dealership departmental managers’ satisfaction with the current marketing performance measurements and effectiveness thereof: Majority of respondents (54.5%) were satisfied with the current marketing performance measurements to some degree (fairly satisfied 27.3%, satisfied 22.7% and very satisfied 4.5%). In comparison, many respondents (36.4%) were neither dissatisfied nor satisfied with the current marketing performance measurements, and only 9.1% were fairly dissatisfied. The study results revealed that the size of the dealership had no effect on the level of satisfaction displayed by the departmental managers.

3. Marketing performance measurements reviewed by top management: Financial measures are the marketing performance measurement most considered by top management. Competitive market measures (77%), consumer (end user) behaviour measures (73%), consumer (end user) intermediate measures (73%), direct customer (trade) measures (82%) and innovativeness measures (64%) were considered regularly or more. Only 5% indicated that financial measures were never considered. Financial measures was collected by nearly 65% of the managers on a monthly or more frequent period, while only 9% never collected financial measures . The results confirmed that top management reviewed financial measures most often and therefore attaches most value to financial measures of marketing performance measurement (that is, sales volume, turnover, profit and return on capital) and less to non-financial measures (that is, distribution, commitment, penetration and market share).

4. Significance that top management assigns to marketing performance measures: The managers perceived top management to rate financial measures (91%) as the most important of the marketing performance measurements. Competitive market measures is rated the second most important (82%). The lowest measurement rated is innovativeness measures (68%) but is it still rated relatively highly. The earlier results reflect that financial measures are most reviewed by top management, most collected by departmental managers and perceived most important by top management in comparison with the other available non-financial measures.

5. Marketing performance benchmarks utilised by the managers: Financial measures (45%) and direct customer measures (36%) were mostly compared to the marketing plan/budget. Competitive market measures (41%), consumer (end user) behaviour measures (36%), consumer (end user) intermediate measures (41%), direct customer (trade) measures (36%) and innovativeness measures (32%) were all relatively high in the comparison to the total industry/category . The results indicated that the departmental managers compared most of the measures other than the financial measures against the total industry. Other than the total industry, the measurements indicated were mostly internal benchmarks such as previous year, marketing plan/budget and other units /departments in the group.

6. Measurement of the marketing asset: Majority of the managers (70% of the total sample) measured the marketing asset monthly by either financial valuation or other measures. 64% of the managers experienced some challenges regarding financial measures. These conclude that most of the respondents’ acknowledges that there is a marketing asset and has a term for it. It was established that the size of the dealership had no influence on the frequency with which the marketing asset was measured.

7. Marketing performance measurements collected: The study showed that the departmental managers collected financial measures the most, at 60% on a monthly or more bases. It is noted that it is significantly higher than the other measures which range between 41% for the direct customer (trade) measures, the second most and least which is innovativeness measures at 27%. The results revealed that departmental managers focus more on the collection of financial measures. In light of the fact that top management reviewed financial measures the most and as a result, the focus of departmental managers is on the collection of financial measures rather than the other available non-financial measures.

The aim of this paper is to investigate the marketing performance measurement practices in the Hatfield Volkswagen Group. In the light of the results of the research , it was concluded that financial measures were the foremost marketing performance measurement instrument used to assess the state of marketing performance in relation to non-financial measures such as competitive market measures, consumer (end user) behaviour measures, consumer (end user) intermediate measures, direct customer (trade) measures and innovativeness measures. It was also concluded that only a quarter of the departmental managers has a formal marketing performance measurement framework that would include internal benchmarks, external benchmarks and the measurement and adjustment of strategy to the brand equity.

Implementing the following recommendations derived from the research could assist in creating awareness of the importance of the measurement of marketing performance utilising the financial and non-financial measures, and the marketing asset as leverage to improve departmental and dealership performance.

1. Certain non-financial key performance indicators need to be embodied in financial statements and management accounts. The non-financial key indicators would include measures of customer satisfaction, marketing asset description and measurement, market share and comparison against best practise.

2. The analysis framework of marketing performance measurement necessitates the alignment to a balanced scorecard method that dissects the non-financial and financial areas of marketing performance measurement.

3. The strategy and objectives should be reviewed on a quarterly basis and amended to align for improvement and changes to the economical and group environment.

4. More external benchmarks need to be incorporated with which to measure performance. The danger of not incorporating a wider range of external benchmarks is that the departmental managers would have a false impression of their success in terms of measuring marketing performance measurement.

5. Guidelines need to be put in place to assist the departmental managers with the definition, importance and measurement of the marketing asset as well as the importance to align the measurement to the other formal marketing performance measurements such as internal and external benchmarks. These guidelines and assistance could consist out of specific training, implementation of marketing performance measurement tools and inclusion of the marketing performance measurement results in the management accounts. Quarterly review should be implemented to scrutinise the status of the marketing asset(s) with the definite actions for improvement measured and targeted.

This study offers a new perspective on the need for an increase in the focus on all the formal marketing performance measurement tools available in order to elevate marketing performance results more frequently and ultimately add value through increased profitability and sustainability of the group.

The authors have none to declare.

REFERENCES

|

Accenture (2001). Sixty Eight Percent of Executives Unable to Measure Marketing Campaign Return on Investment. [Online] Available from: View [Accessed:2013-06-29]

|

|

|

|

Ambler T, Kokkinaki F, Puntoni S ,Riley D (2001) Assessing market Performance: The Current State of Metrics. London Business School. Working Paper No.01-903.

|

|

|

|

|

Ambler T, Roberts JH (2008) Assessing marketing performance: don't settle for the silver metric. J. Mark. Manage. 24(7-8):733-750.

Crossref

|

|

|

|

|

Boone L, Kurtz D (2009). Contemporary marketing. Mason: South-Western Cengage Learning.

|

|

|

|

|

Cant M (2010) Marketing: An Introduction. 1st ed. Lansdowne: Juta & Co. Ltd.

|

|

|

|

|

Eusibio R, Andreu JL, Belbeze MPL (2006). Measures of marketing performance: a comparative study from Spain. Int. J. Contemporary Hospitality Manage. 18(2):145-155.

Crossref

|

|

|

|

|

Greener S (2008). Business Research Methods. Dr. Sue Greener & Ventus Publishing [Online] Available from: View [Accessed:2013-06-29]

|

|

|

|

|

Jin Z, Deng F, Li H, Skitmore M (2013). Practical Framework for Measuring Performance of International Construction Firms. J. Constr. Eng. Manage. 139(9):1154-1155.

Crossref

|

|

|

|

|

Kennerly M, Neely A (2003). Measuring performance in a changing business environment. Int. J. Oper. Prod. Manage. 23(2):213-229.

Crossref

|

|

|

|

|

Kokkinaki F, Ambler T (1999). Marketing Performance Assessment: An exploratory investigation into current practise and the role of

|

|

|

|

|

Kretlow WJ, McGuigan JR, Moyer RC (2006). Contemporary Financial Management. 10th ed. Ohio: South-Western, part of the Thomson Corporation.

|

|

|

|

|

Le Roux EE, Venter CH, Jansen van, Vuuren JE, Kritzinger AAC, Ferreira EJ, de Beer AA, Hubner CP, Jacobs H, Labushagne M (1998). Business management: a practical approach. Johannesburg: Lexican Publishers.

|

|

|

|

|

McPheat S (2010). Effective Marketing.UK: MTD Training and Ventus Publishing ApS.

|

|

|

|

|

Mills H (2010). An investigation of the marketing performance measurement practises of South African organisations. Unpublished Masters in Commerce Thesis: University of Stellenbosch.

|

|

|

|

|

Moerdyk C (2010). Market researchers might miss a big opportunity. [Online]. Available:

View. [2014-09-09].

|

|

|

|

|

Moerdyk C (2013). How much money are you wasting on marketing and advertising? [Online].Available:

View [2014-09-09].

|

|

|

|

|

Nieuwenhuizen C, Rossouw D (2008). Business Management: A Contemporary Approach. Cape Town: Juta & Co.

|

|

|

|

|

O'Sullivan D, Abela AV, Hutchinson M (2009). Marketing performance measurement and firm performance. European J. Mark. 43(5/6):843-862.

Crossref

|

|

|

|

|

Papageorge VM (2005). Measuring marketing performance in South Africa. Unpublished Masters in Business Leadership Thesis: University of South Africa.

|

|

|

|

|

Porter ME (2008). Competitive strategy: Techniques for analysing industries and competitors. New York: Simon & Schuster, Inc.

|

|

|

|

|

Schonlau M, Fricker RD, Elliott MN (2002). Conducting Research Surveys via E-mail and the Web. Santa Monica: Rand.

|

|

|

|

|

Sexton DE (2009). Value above cost: Driving superior financial performance with CVA, the most important metric you've never used. 1st ed. New Jersey: FT Press.

|

|

|

|

|

Shane JM (2007). What every chief executive should know: Using data to measure police performance. Looseleaf Law Publications: New York.

|

|

|

|

|

Shim J, Siegel J (2007). Schaum's Outline of Financial Management. 3rd ed. United States of America: The McGraw-Hill Companies.

|

|

|

|

|

Stapenhurst T (2009). The Benchmarking Book. Oxford: Butterworth-Heinemann.

|

|

|

|

|

Taticchi P (2010). Business performance measurement and management. 1st ed. Berlin:Springer-Verlag.

Crossref

|

|

|

|

|

Walker RH, Slater R, Callaghan B, Smyrnios K, Johnson LW (2004). Measuring marketing performance against the backdrop of intra-organisational change. J. Market. Intelligence Plann. 22(1):59-65.

Crossref

|

|

|

|

|

Weathington BL, Cunningham CJL, Pittenger DJ (2012). Understanding Business Research. New Jersey: John Wiley & Sons.

Crossref

|

|

|

|

|

Woodburn D (2005). Engaging marketing in performance measurement. Meas. Bus. Excellence 8(4):63-72.

Crossref

|

|

|

|

|

Zikmund WG (2003). Business Research Methods. 7th ed. Ohio: South Western, a division of Thompson learning.

|

|