Full Length Research Paper

ABSTRACT

The Nigerian tax reform in the early 1990s was a fallout of market reform in the mid- 1980s, while the structural adjustment program (SAP) piloted a transition to market driven economy where emphasis is laid on market forces with minimal government intervention, hence, the introduction of Value Added Tax (VAT) in 1994. This study empirically examined the impact of VAT on the level of economic activities in Nigeria from its inception to 2014. The study uses secondary data which was analyzed using Johansen (1988) co-integration test. The quarterly data ranged from 1994 Q4 to 2014 Q4. The study found evidence of a significant positive impact of VAT on economic growth. In the same vein, other government revenues, which include all oil receipts and other receipts into the federation account other than VAT were also found to be positively related to economic growth during the study period. The study, therefore, recommends that VAT should be sustained hence; all identified administrative loopholes should be covered for VAT revenue to continue to contribute more significantly to economic growth of the country. There should also be accountability and transparency in the management of all sources of government revenue.

Key words: Value added tax, economic growth, Gross Domestic Product (GDP), other government revenue, Nigeria.

INTRODUCTION

Taxation is one of the most important revenue generation mechanisms in any given economy. In fact, one of the main sources of government revenue is tax which is obtainable from different sources. Government has the mandate to impose tax via its various regulations. An efficient and effective tax system is capable of ensuring the basic necessities and services in the country. Taxes are used to achieve economic growth, achieve equity in income and wealth distribution and maintain equilibrium in the economy. Taxes are not only the most traditional means through which governments generate revenue; they are also the most reliable and predictable. One of these taxes is Value Added Tax (VAT).The Value Added Tax, is a special type of indirect tax in which a sum of money is levied at each stage of production and distribution of a product or service. Referring to history, Okoye and Gbegi (2013) reported that in 1954 the Value Added Tax system was initiated by the then Joint Director of the tax authority of France, Maurice Laure. VAT came into effect for the first time on 10th April 1954; although, a German Industrialist Wilhelm Van Siemens proposed the concept in 1918 the value added tax system has been adopted by different nations across the world. VAT has become a major source of revenue in many developing countries. In sub-Saharan Africa for example, VAT has been introduced in Benin Republic, Cote d’Ivore, Guinea, Kenya. Madagascar, Mauritius, Niger Republic, Senegal, and Togo. Evidence suggested that in these countries, VAT has become an important contributor to total government tax revenues (Adereti et al., 2011). In 1994, the revenue profile of the federal government and by extension sub-national governments increases. This is because, in addition to oil revenue and other taxes such as company income tax, government receives revenue at each stage of production.

VAT was introduced in Nigeria following a study group set up by the federal government in 1991 to review the nation’s tax system. It was this group that proposed VAT and in that same manner, a committee was set up to conduct feasibility study on the implementation of the VAT. The introduction of VAT in Nigeria through Decree 102 of 1993 marks the phasing out of the Sales Tax Decree No. 7 of 1986. The Decree took effect on 1st December, 1993 and became operational in Nigeria on the 1st of January 1994. VAT is administered centrally by the federal government using the existing tax machinery of Federal Inland Revenue Services (FIRS) in close co-operation with the Nigeria Customs Service (NCS) and the State Internal Revenue Services (SIRS). Evidence so far supports the view that VAT revenue is already an important source of revenue in Nigeria. For instance, actual VAT revenue for 1994 was =N=8.189 billion, which is 36.5% higher than the projected N6 billion for the year. In terms of contributions to total federally collected revenue, VAT accounted for about 4.06% in 1994 and 5.93% in 1995 (Ajakaiye, 2000). While the performance of VAT as a source of revenue in Nigeria is encouraging, it remains difficult to find attempts to thoroughly assess the impact of VAT on the economic growth. Various studies on the impact of government revenue on economic growth hardly consider VAT as a separate variable; hence, the study intends to test the following hypotheses: Hoa: Value Added Tax has no significant positive relationship with economic growth in Nigeria. Hob: Value Added Tax has no significant long-run effect on economic growth in Nigeria. The main objective of this paper is to test the aforementioned hypotheses. In achieving this objective the paper is divided into five sections including this introduction. The rest of the paper is organized as follows; section two presents the review of related literature. Section three gives the detailed methodology of the work, section four presents the empirical results while section five summarizes and concludes the paper.

LITERATURE REVIEW

As the name implies, the VAT refers to the tax on the value added. What is the value added? The value added of a firm is the difference between a firm’s sales and its purchases of inputs from other firms. In other words, it is the amount of value a firm contributes to a good or service by applying its own factors of production namely land, labor, capital and entrepreneurial ability. In Nigeria VAT is charged at a flat rate of 5% on selected items of goods and services. Though, exemption are granted in respect of medical and pharmaceutical products, basic food items such as maize, rice, wheat, milk and fish infant food items, books, newspapers and magazines, educational materials (laboratory equipment). Baby products such as carriages, clothes and napkins, as well as sanitary towels, commercial vehicles and spare parts, tractors, public transport, passenger vehicles, motorcycles, tanks and other armored fighting vehicles, and bicycles; agricultural equipment such as those for soil preparation or cultivation, harvesting or threshing, milking and dairy machinery, poultry keeping machinery, veterinary medicine equipment, fertilizers and farming equipment (Ajakaiye 2000). Literature on VAT abounds, here we present a review of the most recent and related. Emmanuel (2013) investigated the effects of VAT on economic growth and total tax revenue in Nigeria. The study used Simple Linear Regression method to analyze time series data relating to VAT, Gross Domestic Product (GDP) and Total Revenue for period 1994 to 2010. The researcher also employed the use of SPSS for computation. The results of his findings showed that VAT has significant effect on GDP and also on Total Tax Revenue. On the other hand, Onodugo (2013) employed the Ordinary Least Square (OLS) method of simple regression analysis to evaluate the contribution of VAT to resource mobilization. The study examined the relationship between VAT and Real Gross Domestic Product (RGDP), VAT and Current Revenue (CREV), VAT and Internal Revenue (INREV). Generally, their findings revealed that value added tax has significantly contributed to resource mobilization and capital formation in Nigeria. The study recommended that both the tax payers and tax administrators should be adequately motivated to enable them perform well to ensure higher level of efficiency and effectiveness. Also, Awolabi and Okwu (2001) studied value added tax and development of Lagos State economy. They used simple regression analysis to evaluate the effect of value added tax revenue to the economic growth of Nigeria. Their analytical results showed that value added tax revenue contributes to the development of infrastructural development, environmental management, education sector development, youth and social development, agricultural sector development and transportation sector development.

In a similar vein, Ikpe and Nteegah (2013) empirically examined the influence of VAT on price stability in Nigeria using partial equilibrium analysis. The analysis was carried out by applying multiple regression analysis, using data from 1994 to 2010 periods. The results revealed that VAT exerts a strong upward pressure on price levels, most likely due to the burden of VAT on intermediate outputs. The study ruled out the option of VAT exemptions for intermediate outputs as a solution, due to the difficulty in distinguishing between intermediate and final outputs. Instead, it recommended a detailed post-VAT cost benefit analysis to assess the social desirability of VAT policy in Nigeria. Gbegi and Okoye (2013) using secondary data spanning 2001 to 2010 and employing the use of table and simple percentages while the hypotheses formulated were tested using Product Moment Correlation Coefficient and Student t test. The findings revealed that revenue generated through VAT has a significant influence on wealth creation in Nigeria and also that revenue generated through VAT has a significant effect on total tax revenue in Nigeria. Ekeocha (2010) however, made a simulation study advocating value added tax trade from 5 to 15%. He argued that an increase in the rate of value added tax will affect the country’s revenue base. Yakubu and Jibril (2013) investigated the relative impact of value added tax on economic growth in Nigeria. Johansen co integration test was employed. The result of co integration test does not provide any evidence of long-run equilibrium relationship among the variables. An unrestricted vector auto regressions (VARs) technique was employed. Impulse response functions (IRFs) and Forecast error Variance decompositions (FEVDs) were computed through 1000 Monte Carlo simulations. The results derived from the impulse response function (IRF) and forecast error variance decomposition (FEVD) entailed that value added tax have positive impact on economic growth in Nigeria , they also added that where variation in this variables growth rate will cause variation in real economic activity with about 50% in the near future. The study concluded that the policy makers in Nigeria should continue this fiscal policy with other macroeconomic indicators. They recommended that this policy will enhance the Nigerian economy positively, more specifically in this time of economic crisis in the world.

Bakare (2013) investigated the enormity of the impact of the value added tax on output growth in Nigeria. The study employed the use of ordinary least square regression analytical technique, the study found that a positive and significant relationship exist between value added tax and output growth in Nigeria. The results further showed that the past values of value added tax could be used to predict the future behavior of output growth in Nigeria. The study therefore concluded that Value Added Tax has the potential to assist in the diversification of revenue sources, thereby providing enough funds for economic growth and development and reducing dependence on oil for revenue. Hence, the findings support the need for the government to satisfy the principle of economic justice in the allocation of VAT revenue. The study then suggested that the revenue generated from VAT should be efficiently utilized for building infrastructure required for sustainable growth and development. Chinnwe (2013) evolved survey research design to investigate the value added tax remittance of developing countries. These findings revealed that there was continuous decrease in revenue returns. The study therefore recommended that the Nigerian government should make adequate provision for retrieving the proceeds of Value Added Tax and other agents of collection. Basila (2010) empirical investigated the relationship between VAT and GDP in Nigeria. Applying time series data set spanning the period from 1994 to 2008 using Pearson’s Product Moment Correlation (PPMC) The test revealed a strong at about 96% strength. Further, a test of significance confirmed that VAT revenue is significantly different at 99% confidence level in relation to GDP. It also shows that there is a strong positive correlation between VAT revenue and GDP. Chigbu and Ali (2014) empirically analyzed the relationship between VAT and economic growth in Nigeria. Using the Engle and Granger cointegration technique on annual data covering 1994 to 2012, the result of their findings showed that VAT has positive effect on economic growth. The results also showed absence of both long-run and short-run relationship between VAT and economic growth. The study recommended that government should therefore put in place measures to enhance productivity so as to increase the contribution of VAT to economic growth in Nigeria. Okubor and Izedonmi (2014) examined the contribution of VAT to the development of the Nigerian Economy. They employed time series data on the GDP, VAT Revenue, Total Tax Revenue and Total (Federal Government) Revenue from 1994 to 2010. They used both simple regression analysis and descriptive statistical method. The result of their findings revealed that VAT Revenue and total revenue account as much as 92% significant variations in GDP in Nigeria. Also, a positive and significant correlation exists between VAT revenue and GDP. According to the authors, both economy variables fluctuated greatly over the period with VAT Revenue to be more stable. The study therefore recommended that all identified loopholes be plugged for VAT revenue to continue to contribute more significantly to economic growth of Nigeria.

METHODOLOGY

The data for this study was mainly secondary which was collected from the Statistical Bulletin of the Central Bank of Nigeria (CBN) and National Abstract of the National Bureau of Statistics (NBS). The data was in respect of 1994 to 2014. The reason behind the choice of the study period is that VAT was introduced in 1994 and therefore, it is the period during which the required data is available.

Diagnostics test and estimation strategy

One of the methods of testing whether series are stationary or not is Dickey Fuller (DF) (1979). The DF test is very important in terms of measuring the degree stationarity of series, but it does not consider an autocorrelation in disturbance terms. If however, disturbance terms contain autocorrelation, DF test is invalid. But in this situation, by adding lagged terms of dependent variable to explanatory variable, Generalized Dickey-fuller (augmented Dickey Fuller) is used, Vuranok (2009). The cointegration test is an important statistical tool for estimating the pattern of relationship that exists between time series variables. Generally, a set of variable is said to be cointegrated if a linear combination of the individual series, which are I (1), is stationary. Intuitively Xt ~I (1) and Yt~ I (1), a regression is run, such as:

Yt= BXt+ µt (1)

This study uses Johansen (1988) approach, which allows it to estimate and test for the presence of multiple cointegration relationships, r, in a single-step procedure.

Model specification

Following the model used by Onodugu et al (2013) in their investigation of the impact of value added tax and economic growth in Nigeria; this study adopts a modified version of the model, in order to take care of those variables not captured in the previous study. The modified version of the model is specified:

GDPt = α + α1VATt + α2 OGRt + α3 INFt + µt (2)

Where:

GDPt = Gross Domestic Product

α = Constant parameter

α1 – α3 = Coefficient of independent variables

VATt = Value of value added tax

OGRt = Other government revenue

INFt = Inflation

µt = error term

RESULTS AND DISCUSSION

Here the results of the data analyzed is presented. The presentation is in two parts; the first part contains the descriptive analysis while the second part contains the inferential analysis.

Descriptive statistics

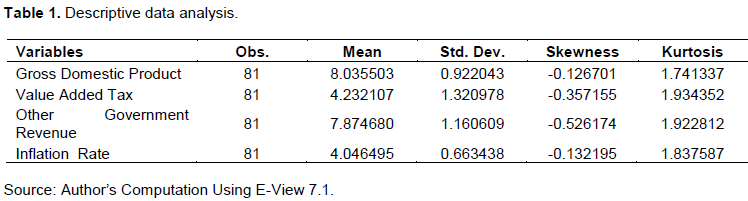

This comprises the variables, observations, mean, standard deviation, skewness and kurtosis of the data on variables employed in the research within the study period as presented in Table 1 and analyzed. Table 1 shows the results of the data used; using 81 observations for each of the variables to estimate the relationship between value added tax and economic growth in Nigeria from 1994 to 2014 for the descriptive statistics. The mean describes the average value in the series and the standard deviation measures the volatility of the data or the amount of deviation of the data from the average. The skewness measures whether the distribution of the data is symmetrical or asymmetrical. A positive skewness value indicates that the distribution of the data has a long right tail, while a negative skewness value shows that the distribution of the data has a long left tail. Mean of GDP depicts the series cluster around 8.035503, it standard deviation is 0.922042 which indicates wide disparity away from the mean, skewness of -0.126701 which is negatively skewed and decimal places away from being perfectly symmetric distribution, kurtosis 1.741337 which is positive and platokurtic therefore, the measures of central tendency and measure of dispersion suggests a sign of abnormality in the distribution of Gross domestic product. Value added tax shows the mean value of 4.232107, standard deviation depicts 1.320978 which indicate a wide disparity away from the mean, these figures, however indicated that abnormality exist between the mean and standard deviation and low negative value of skewness for value added tax (-0.357155) shows that the data is relatively and negatively skewed to the left, and the kurtosis of 1.934352 indicates that the data has platokurtic distribution.

On the other hand, the mean inflation value is 4.046495 and standard deviation is 0.663438 which indicated abnormality among the two while skewness figure is -0.132195 and kurtosis is 1.837587 which depicts abnormality. Other government revenue data in the period under study has average value of 7.874680 and standard deviation is 1.160609. These reveal that the data is not much spread out from the mean and low volatility. The skewness value of -0.526174 shows that the data is negatively skewed to the left, and the kurtosis of 1.922812 indicates that the data are relatively peaked compared to normal (Leptokurtic distribution). The implication of the descriptive statistics results could be due to the high volatility associated with the variables examined from the Nigerian economy and the quality of their data generation process. With effective policies to ensure more macroeconomic stability and qualitative data, it is expected that the variables would be well behaved statistically.

Inferential statistics

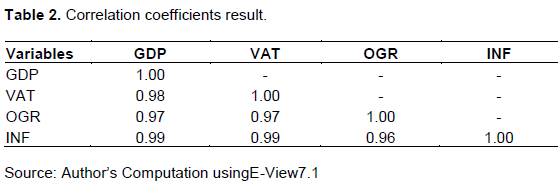

Table 2 present the result of correlation coefficient of the variables used for the estimation. Table 2 presents the result of correlation coefficient of the variables used for the estimation. The question whether or not VAT revenue is correlated to GDP is confirmed by this test that there is a strong positive correlation between them. They are positively correlated at 98.0%. This shows that activities in the markets are inter-linked and entirely dependent of each other.

Stationarity and unit root test

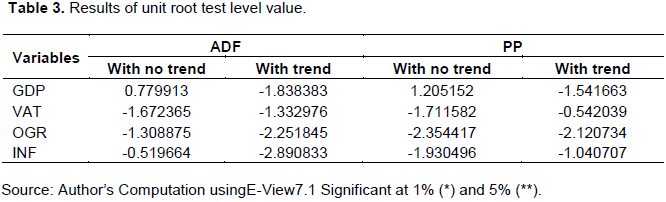

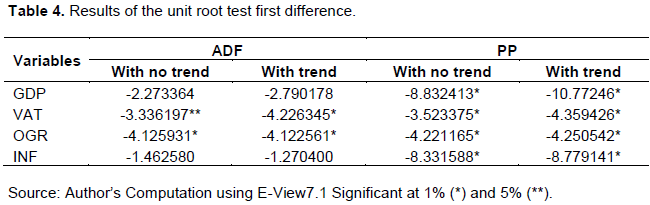

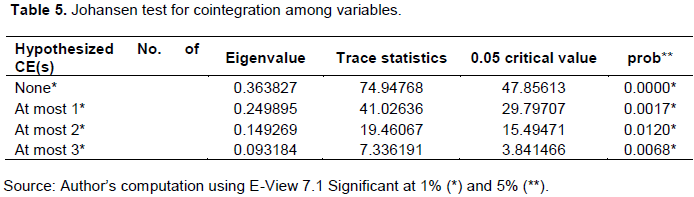

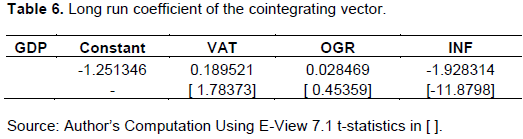

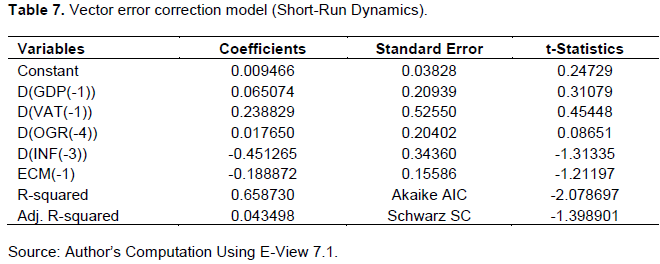

Table 3 shows the result of Augmented Dickey Fuller (ADF) and Phillips-perron (PP) unit root test on the variable used for the study to ascertain order of integration. Tables 3 and 4 present the results. Table 3 presents the result of unit root test using Augmented Dickey Fuller (ADF) and Phillips-perron (PP) unit root test at level value. The column shows Augmented Dickey Fuller (ADF) and Phillips-perron (PP) with no trend and with trend. All the variables are non stationary at level value in Table 4. Table 4 presents the result of unit root test using Augmented Dickey Fuller (ADF) and Phillips-perron (PP) unit root test at first difference. The column shows Augmented Dickey Fuller (ADF) and Phillips-perron (PP) with no trend and with trend. After taking the first difference all the variables become stationary I (1) series at 1 and 5% respectively. Table 5 presents the result of the trace statistics test, the trace statistics indicates (4) two cointegration equation at 0.05% level of significant this denotes rejection of the null hypothesis at the 0.05% level of significant. This indicates the existence of a long run relationship among the variables. Table 6 presents the result of long run relationship among the variables. The table shows that there exists long run positive and statistically significant relationship between VAT and GDP. Other Government revenue (OGR) has a positive and statistically insignificant long run relationship with GDP while, inflation has negative and statistically significant long run relationship with the GDP. Table 7 presents the results of the vector error correction model (VECM). The negative and statistically significant coefficient implying that there is a possibility of the restoration of equilibrium in case of distortions in the economy. Giving the ECM coefficient of -0.188872, only 5.0% of equilibrium can be restored quarterly and adjustment to equilibrium is very slow. However, the negative coefficients of the ECM further support the long run relationship among the variable. The R2 test is used to show the total variation of the dependent variable that can be explained by the independent variable. The R2 is equal to 0.758730 that is 75.87% of the dependent variable GDP can be explained by the change in value added tax, other government revenue and inflation in the economy within the period under review.

Long run relationship between VAT and GDP

The result of long run relationship among the variables, shows that there exists long run positive and statistically significant relationship between VAT and GDP which is in conformity with the work of Enokela (2010), Adereti et al. (2011) and Emmanuel (2013) that reveals positive and statistically significant relationship between VAT and GDP.

Long run relationship between other variables and GDP

The other Government revenues (OGR) have a positive but statistically insignificant long run relationship with GDP. On the other hand, the result of inflation has negative and statistically significant long run relationship with the GDP which is in line with the a priori expectation.

CONCLUSION AND RECOMMENDATIONS

This study empirically investigated the impact of VAT and GDP in Nigeria from the time of its inception in 1994 (1st Quarter) to 2014 (4th Quarter). The data set were first subjected to unit root test, using Augmented Dickey fuller Test and Phillip-Perron Test at level value none of the data were stationary but at first difference all the data set become stationary that is I (1) series. Johansen cointegration test for long run relationship, short-run dynamics were conducted. The results revealed the following findings.

1. The result revealed that at level value none of the data are stationary but at first difference all the data set become stationary that is I (1) series.

2. From the result it indicates that there exists a long run relationship between the variables with four cointegration equation. VAT has positive and statistically significant long run relationship and GDP.

3. The short-run dynamics revealed that there is possibility of the restoration of equilibrium in case of distortions in the economy and adjustment to equilibrium is very slow.

The study applied Johansen (1988) co-integration test on quarterly data ranging from 1994 (4th Quarter) to 2014 (4th Quarter) and finds that value added tax contributed significantly to the growth of the Nigerian economy during the study period. Therefore, the study concludes that VAT has the potential to assist in the diversification of revenue base of the Nigerian economy thereby reducing dependence on oil revenue. In the same vein, other government revenues which include all oil receipts and other receipts into the federation account other than VAT are also found to be positively and statistically related to economic growth in Nigeria. Based on the findings it is therefore recommended that value added tax should be sustained, hence, all identified administrative loopholes should be covered for VAT revenue to continue to contribute more significantly to economic growth of the country. There should be accountability and transparency from government officials on the management of other government revenue and also citizens should be able to benefit from it. The study also recommended that government should intensify efforts to check inflation in the country so that the positive impact of VAT on the economic growth of Nigeria can be realized.

CONFLICT OF INTERESTS

The authors have not declared any conflict of interests.

REFERENCES

|

Ajakaiye D. (2000). Macroeconomic effects of value added tax in nigeria a computational general equilibrium analysis. Afr. Econ. Res. Consort. (AERC) P 92. |

|

|

Adereti SA, Sanni ME, Adesina JA (2011). Va1ue Added lax and Economic Growth of Nigeria. Eur. J. Humanit. Soc. Sci. 10:455-471. |

|

|

Owolabi OA, Okwu AT (2011). Empirical Evaluation of contribution of Value Added Tax to Development of Lagos state Economy. J. Middle East. Financ. Econ. 1(9):24-34. |

|

|

Bakare AS (2013). Value Added Tax and Output Growth In Nigeria". Proceedings of 8th Annual London Business Research Conference Imperial College. London, UK, 8-9 July. |

|

|

Basila D (2010). Investigating the Relationship Between VAT and GDP in Nigerian Economy. J. Manag. Corp. Gov. 2(2): 65-72. |

|

|

Vuranok BH (2009). Public Finance (24th edition). New Delhi, Vikas Publishing House PVT Ltd. |

|

|

Chigbu EE, Ali PT (2014). An Econometric Analysis Of The Impact Of Value Added Tax Economic Growth In Nigeria. Eur. J. Bus. Manag. P 6 (18) ISSN 2222 – 190s ISSN 2222 – 2839 (online) |

|

|

Emmanuel CU (2013). The effect of Value Added Tax (VAT) on the Economic Growth in Nigeria. J. Econ. Sustain. Dev. 4(6):190-202. |

|

|

Enokela SA (2010). The impact of Value Added Tax on Economic Development of Nigeria. |

|

|

Izedonmi FIO, Okunbor JA (2014). The Roles of Value Added Tax in the Economic Growth of Nigeria. Br. J. Econ. Manag. Trade. 4(12) ISSN:222-0984. |

|

|

Johansen S (1988). Statistical Analysis of Co-integrating Vectors. J. Econ. Dyn. Control. 12(2-3):231-254. |

|

|

Onaolapo AA, Aworemi RJ, Ajala OA (2013). Assessment of value added tax and effect an revenue generation in nigeria of value added tax on revenue generation in Nigeria. Pakistan J. Soc. Sci. 10(1): 22-26. |

|

|

Onodugo V (2013). An evaluation of the contribution of value added tax (VAT) to resource mobilization in Nigeria. Eur. J. Bus. Manag. 5(6). |

|

|

Yakubu M Jibril SA (2013). Analyzing the impact of value added tax (VAT) in economic in Nigeria. Theory. Math. Model. 3(14):16-23. |

|

Copyright © 2024 Author(s) retain the copyright of this article.

This article is published under the terms of the Creative Commons Attribution License 4.0