Full Length Research Paper

ABSTRACT

This study examines the effect of independence factors on audit expectation gap in listed deposit money banks in Nigeria. The population of the study comprises of the investors/shareholders, lenders and other creditors and a sample of 385 respondents was selected using Cohran sample size formula. The period under study is from January, 2012 to December, 2019. The study used a questionnaire drawn on a five point likert scale to collect data. The questionnaire has been pilot tested for reliability and validity, using the Cronbach alpha and Kendall’s coefficient of concordance. The data was analyzed using descriptive statistics and multiple-regression analysis. The study concludes that auditor depends on client economically. Competing for audit market, carrying out non-audit market service, receiving gifts from management and prospects for reappointment are strong determinants of audit expectation gap in deposit money banks in Nigeria. The study opines that the independence factors have significant positive impact on audit expectation gap in listed deposit money banks in Nigeria. This finding is in line with that of Salehi et al., Amaechi and Chinedu as well as Kamau et al. but is not consistent with findings of Ogweno and Kamau. The study recommends that regulatory authority and professional accounting associations should ensure that auditors avoid economic dependence on the client, carrying out services which are not audit related, and collecting gifts from management and that the regulatory authority has to emphasize on auditors tenures and appointment of auditor shall be through a centrally organized body and not allow audit firms to be competing among themselves.

Key words: Audit, expectation gap, independence factors, Banks, Nigeria.

INTRODUCTION

The need and demand for auditing arose from the desire for an independent person to monitor the contractual arrangements between principal and agent. If an auditor lacks independence, the parties to the contract place little or no value on the service provided, especially statutory audit. External auditors play a critical role in validating company’s finances. Creditors and investor rely heavily on auditor’s report since credibility has been added to such reports (Madison, 2018). The statutory audit and assurance play an important role of ensuring confidence by the users / stakeholders (Chandler et al., 1993), and thus the society expects auditors to exercise professional judgment as well as maintain professional skepticism in their function. Auditors must exercise professional judgment and skepticism in their work, while the preparation of financial statement is the sole responsibility of management. Moreover, users and the public have different expectations regarding the assurance level and often assume absolute assurance (Enofe et al, 2013).

Auditing emerges to provide an independent check on the affairs of an organization. This is made possible because ownership has been separated from control, which succinctly supports agency role. Public trust is vital to every profession, accounting profession in particular and the profession suffers societal skepticism and depletion where trust has been eroded which affects users value relevance especially, that Financial Statements form the basis for a sound decision making. That is to say expectations and belief by the public fundamentally, breed a series of dissatisfaction with performance of auditors, which consequently affect end users trust, which affects the public confidence users had in the financial statements so examined by the auditor.

In Nigeria however, the major corporate financial irregularity and related fraud which occurred leading to sudden collapse of corporate institutions such as the Cadbury, Intercontinental Bank, Oceanic Bank and Spring Bank and on, has further brought the expectations gap to limelight. This is because the users had a strong belief that since Auditors are independent, then the Auditors are responsible for detection and reporting of all forms of irregularities and frauds, hence the collapse of these organizations came as a surprise to the shareholders and users. This perception was further upheld because users view fraud detection as the main function of auditing, hence the audit Expectation gap becomes more pronounced as a result of these corporate crisis in Nigeria and the misperception by users.

Audit Expectation Gap is worth researching because its continuous existence would lead the Society not to appreciate or recognize auditors’ contribution to the society, which will subsequently weaken the significance of audit purpose. Therefore, it is against the backdrop that this study assesses the impact of independent factors on audit expectation gap in listed Deposit Money Banks in Nigeria. To achieve this objective the hypothesis below was formulated and tested.

Ho1: Auditors the impact of independent factors on audit expectation gap in listed Deposit Mone Nigerian Deposit Money Banks.

Theoretical framework

Credibility theory

This theory re-emphasize the role auditing can play in enhancing reliance on financial statements that is addition of credibility. This is because, agents stewardship function can be enhanced such that the principal will have more faith in the agent, and this will consequently reduce information asymmetry.

Quasi-judicial theory

Quasi-judicial theory has it that auditor is seen as a judge in the financial distribution process (Hayes et al., 1999). However, Porter (1990) opines that the quasi-judicial theory can be perceived from three perspectives: (a) that an auditors independence differs greatly from that of a judge, because of different reward systems involved; (b) that an auditors decision and decision process are not publicly available; and (c) that what was regarded as the doctrine of precedence and consistency is not guaranteed in auditing.

Therefore, to perceive auditor as judge is out of place, hence this theory should not have much weight.

Agency theory

Agency theory is rooted in the existence of relationships between agent (management) and owners (investors/ principal) (Jensen and Meckling, 1976). Both credibility, quasi-judicial and agency theories, has been anchored for the purpose of this study.

REVIEW OF EMPIRICAL STUDIES

Salehi et al. (2019) evaluate the auditor’ auditor n, and Adibianty, quasi-judicial a relationship among users of information in listed companies on Teheran Stock Exchange (TSE) market. A sample of 78 listed companies on the TSE from 2012-2016 using integrated data technique of the multiple regression models. The study finds that the independence of the director boards and audit committee members fulfill the expectation gap of individual users (among others). The independence factors have an impact on audit expectation gap. Although, there are several works in this area both quantitative and qualitative; however, the authors claimed that their work is the first quantitative work, this is not true. Hence, they failed to agree or contest any work in the literature.

Sabuj et al. (2019) aims at finding the impact of audit expectation gap among the auditors, investors, general users of audit report and the academia with regards to an independent auditor in Bangladesh. The study used questionnaire to collect data, after it has been tested for validity and reliability with NOVA as statistical analysis technique. The study finds that users and independent auditors are alike in their perception about the audit independent factors.

Onulaka et al. (2019) in their works investigates the extent to which the provision of Non-audit service (an independence factor) by external auditors to clients affects auditors of Non-audit service (an independence factor) by external auditors to clients affects auditors’ independence and consequently audit expectation in Nigeria. The study used 30 semi-structured face to face interviews to obtain data from the respondents after the questionnaire has been tested for reliability. This was followed by a thematic data analysis of the respondents. The study finds that the provision of non-audit service by audit firms to their audit client is regarded by auditor as a matter of economic necessity. Nevertheless, it is also perceived as impending auditors independence and increasing the gap between the auditor and public expectations. However, the study fails to show the clients perceived economic pressure on auditors to undertake non-audit service.

Ogweno (2018) investigates the factors affecting expectation gap in listed companies in Nairobi Stock Exchange (NSE) that is auditorted companies in auditorit competence and userpe knowledge of auditordg role. The study used a descriptive research design. A population of 62 listed companies at NSE was selected. A questionnaire was administered to a purposely selected respondent from a sample of 58. The data was analyzed using multiple regression and correlation analysis to test the relationships. The study finds that auditorn and correlation sely selected respondcreasing the gaudit expectation gap. It has been recommended that the independence of the auditor should be strengthening by drafting legal laws promoting the independence of the auditors in Kenya.

Toumeh et al. (2018) identify the factors that affect the expectation gap in Jordan. The population of the study is 327 audit firms in Jordan. A sample of 158 firms was randomly selected out of which 109 was used and the questionnaire was drawn on a five point scale to test the reliability of the questionnaire and correlation between questions using arbitrators and Chronbach alpha. The statistical tool used to analyze the data includes the t-test and the descriptive statistics. The results showed among others that uncertainty in the auditor’s independence has less impact on increasing the expectation gap in the audit process in Jordan. It is recommended that strengthening auditor’s independence by neutralizing the controls of the disputing parties and also reducing auditor and client personal relationships. Hence, the study failed to test for the reliability of the instrument.

Amaechi and Chinedu (2017) examined if independence factors pose as challenge to internal auditors of public sectors entities. The population of the study is 80 respondents, drawn from the accountants and auditors in the Accountant General and Auditor General offices of Anambra state; however, a sample of 57 respondents was actually used. The study adopts survey design approach, with questionnaire drawn on a five point likerts scale. The data was analyzed using the descriptive statistics and Mann-Whitney U-test. The study finds that independence factors affect internal auditors of public sector entities independence, thereby increasing expectation gap. However, the study has some mixed up in the population actually used and the ones mentioned.

It has been recommended that independence of auditor should be enthroned to reduce expectation gap.

Kamau et al. (2014) examine internal auditor independence motives in Kenya. A four point likert scale has been used to analyze the 21 questionnaires, Cronbach alpha was used to test the reliability of the instrument. Regression analysis techniques were used for the hypothesis testing. The study finds that the level of involvement by internal auditors in the management activities significantly affects their professional independence. Audit committees effectiveness plays a significant role in enhancing auditor independence and that causal relationship existed between internal auditors skills and auditors independence. However, the study fails to look at undertaking of non-audit service, and accepting gifts from the company’s management.

Kamau (2013) investigates the determinants of audit expectation gap in Kenya. One of the objectives of the study is to determine whether independence contribute to expectation gap in Kenya. The target populations are the audit firms in Kenya and a Sample of 110 firms are selected. The variables used in the study are auditor’s efforts, skills, structure, independence, public knowledge, audit scope and users’ needs. The study employed a mixed research design comprising descriptive statistics, survey design and the data collected. The study found that an independence factor does not significantly contribute to audit expectation gap in Kenya. The study however, fails to examine reliability factors and responsibility factors.

Population of the study

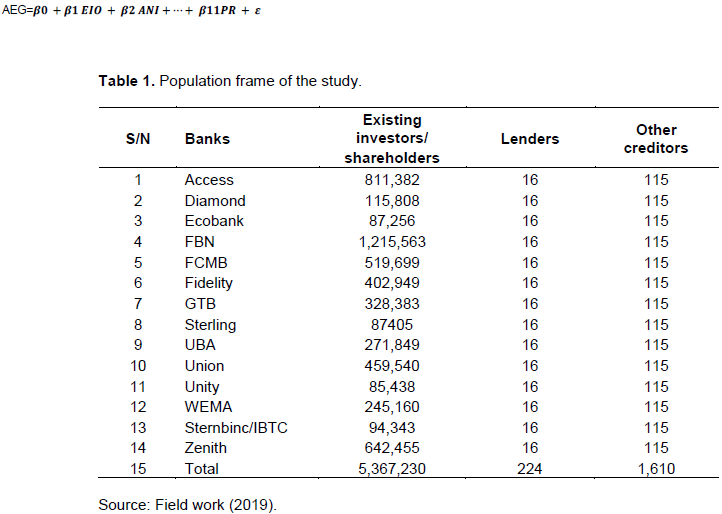

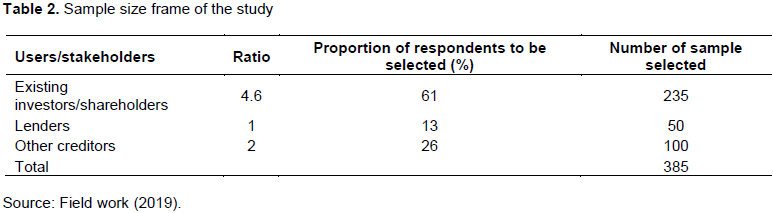

The population of the study consists of primary users of financial statement numbering 5,369,064 out which a sample of 385 respondents was chosen using Cochran (1977) sample size formula (Table 1).The sample size of the study which is 385 respondents was chosen in Table 2 using Cohran Sample Size fomular (1977). A confidence level of 95% was chosen, a margin of error of 5% that is 0.05. The 95% is chosen because it is most commonly used Confidence level (Taylor, 2014). Therefore, a sample size of 385 has been selected, while the sampling frame was chosen using sampling and elevation factors. Copies of Questionnaire were distributed to each category of primary users, existing investors/shareholders, lenders and other creditors. The questionnaire used was adopted from Porter (1990) and Schelluch (1996), however with slight modification to suit the objectives of the study (Table 3).The Study used the descriptive statistics and Multiple Regression for the analysis and the following model was used:

MATERIALS AND METHODS

The study reviews relevant materials such as literature related to the topic, conceptual issues and theories.

The audit expectation gap concept

Au Audit Expectation Gap refers to “the difference between the Levels of expected performance by an independent auditor and the users of financial statement (Liggio, 1974). Expectation gap was used to draw a corollary and describe a situa tion between group which relies upon certain expertise and those who provide such expertise, which resulted in variance between what the society expects from the independent Auditor and what the accounting profession entails. Porter (1993), Ruhnke and Schmidt (2014) and Toumeh et al. (2018) concur with this definitions.

The expectation gap concept was introduced initially by Liggio (1974) and it was agreed that the concept originated from America. The study by Humphrey et al. (1993) concurs with these assertions. To investigate reasons for audit expectatio n gap, Cohen Commission was set up in 1978. Other commissions set up in the United States of America include; the 1976 Mtcalf Committee, and 1978 Treadway Commission. In the United Kingdom Commission like the Cross Committee (1977) and the 1978 Greenside Commission; while in Canada similar commissions were set up which include the Adams (1977) and Macdoald (1988).

Individual researchers carried a lot of work on Audit Expectation Gap for example, Van Liempd et al. (2019), Mansur and Tangl (2018), Porter (1993), Dixon et al. (2006), Fadzly and Ahmed (2001) the three groups examine the roles and responsibilities of an auditor, while the meanings and Nature of audit reports was examined by Monroe and Woodliff (1994) and Gay et al. (1978); whereas Alleyne et al. (2006), Lin and Chen (2004) and Sweeney (1997) each assesses audit independence.

Audit Expectation Gap problems was examined using a metaphorical style by Tweedie (1987); thus, a burglar alarm system, a radar station, a safety net, an independent auditor coherent communications that is protection against fraud, early warning of future insolvency, general reassurance of financial wellbeing, safeguards for auditor independence and understanding of audit reports respectively. It was opines that given these concerns shows clear mis-understanding of audit, more so, that no auditor can provide these yearnings hundred percent. He concluded that as we cannot have hundred percent auditor independence in practice, likewise not all users/stakeholders can have a clear understanding of audit reports, hence audit expectations gap shall widen up

Audit expectation gap components

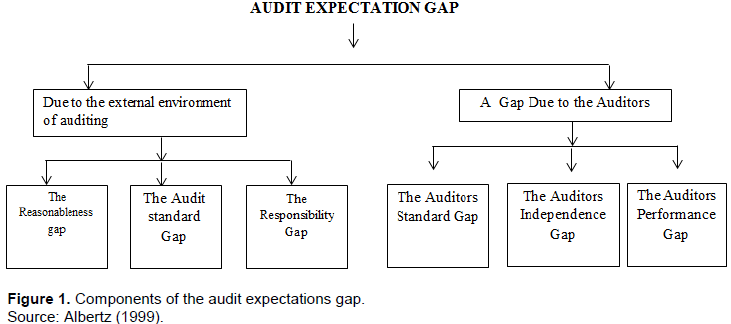

Diversity in definitions of audit expectation Gap gave rise to emergence of different components of audit expectation gap, which includes the reasonableness, deficient performance and gaps. The reasonableness gap is the difference between society’s expectations and auditor actual accomplishment. The deficient Standard gap covers gaps existing between duties reasonably expected of auditors and duties provided by law; while the deficient performance gap is difference between expected standard of performance or existing duties and performance (Füredi-Fülöp, 2017; Masoud, 2017; Macdoald Commission, 1988). However, Albaz (1999) opines that in auditing, the expectation gap can be observed more clearly from the perspectives of components and alternatively the sub- gaps which can be divided into two groups: the first group are those due to the auditing external environment; whereas the second are those expectation gap due to the auditors themselves (Figure 1).

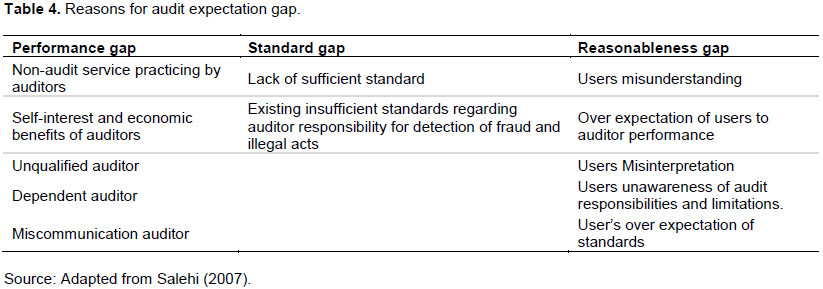

Reasons for audit expectation gap

Salehi (2011) examines major reasons for expectation gap to include services which are Non-audit undertaken by auditors, self-interesting auditors, economic relationships with clients, auditors who are not qualified and auditors dependent on the client, other reasons are as shown in Table 4.

Independence factors

The concept of independence in literature provides that there can be independence in fact and independence in appearance, which can amplify the idea of threat to independence. Independence of the mind is an attitude of the mind, its evaluation is difficult to observe. However, literatures are for perceived independence, since perceptions are fundamental to public confidence in financial reporting (Carmichael, 2004). However, some definitions were proffered by several authorities for instance, Knapp (1985) viewed independence as the ability to resist client pressure. This definition raises further questions; for example to resist clients pressure in which way, how, where and when. However, a more acceptable definition of independence was provided as follows: “Freedom from those pressures and other factors that compromise, or can reasonably be expected to compromise, an auditor’s ability to make unbiased audit decisions” (ISB, 2000). Although, this definition is better than the one provided by Knapp (1985), however it fails to capture certain areas of independence like carrying out non-audit services. Nevertheless, these definitions show how important objectivity and integrity are major fundamental aspect for assessing auditor’s independence.

There are quite a number of factors that affects independence factors, these include; closeness to the client either through marriage or blood relationship, to depend on client economic wellbeing , influenced by a desire of social economic success, acceptance of gifts from clients directly or indirectly, audit market competition and prospects for re-appointments (Sucher and Maclullich, 2004).

Other issues that impinge on independence include cases where auditor may have to defend on Management, rely solely on external Debtors confirmation received from circularization of Debtors, Creditors and or Bank accounts or requires the management for assets verification/valuation purposes. Re-appointment of auditors technically is the duty of the shareholders at Annual General Meeting (AGM); however, this function was compromised by management who influence the nomination thereby injuring auditors’ independence factors.

Beattie et al. (1999) listed four factors militating against independence constraints to independence, and they include Instances where auditor depends on client for economic wellbeing, competing for Audit market; the regulatory guidelines and the provision of services unrelated to auditing duties (NAS).

Gill and Cosserat (1999) are of the opinion that independence is key to auditing. Where there is no independence, one cannot rely on auditor’s opinion. Also, third parties believe that where there is no independence then external audit is unnecessary. Third parties’ acceptance of an auditor’s role is likened to independence as corporate accountability instrument. For an auditor to maintain independence despite pressures of practice, he has to be conscious of any negative influences on his planning.

Investigation and reporting independence

Perceptions by users of what is audit independence are important because real perception depends on society’s perception of what could impair real independence. The external auditors must ensure that quality and performance of auditor should not be compromised. The issue of Auditor independence is an area of concern in audit expectation gap (Humphrey et al., 1993; Moizer, 1997; Sweeney, 1997; Alleyne et al., 2006). According to the Independence Standards Board of the American Institute of Certified Public Accountants (2000, cited in Alleyne et al., 2006), auditor’s ability to be unbiased and free from pressures and any factor that can make him compromise his positions is necessary. The general public and audit profession benefits greatly when auditor is independent. Lack of it puts ordinary people’s investment at risk (Gettler et al., 2002); while the audit profession enjoy professional status and public stewardship (Kleinman and Palmon, 2001) and as Gill et al. (2001) stated: ‘independence is the livewire of the auditing profession and where it is lacking then auditors opinion is suspect, and where public suspect auditor opinion this further generates expectation gap. The view of Kleinman and Palmon (2001) and Gill et al. (2001) are in tune with the view of the audit profession. Since the Public Oversight Board’s Panel on Audit Effectiveness (POB, 2000) observed as follows that: an auditor must be independent both in fact and in appearance. Independence in fact means auditor’s state of mind, to make his decisions objective that is unbiased (Dykxhoorn and Sinning, 1982); whereas, independence in appearance is the perception that auditor has no direct or indirect relationship with client, which can lead to conflict of interest (Pierce, 2006). Pierce (2006) grouped independence factors into three categories as follows:

(i) Programming independence: this occurs when audit techniques and procedures are selected without external parties influence whether direct or indirect.

(ii) Investigative independence: it is attain where auditor is able to access and examine all the necessary audit evidences in all areas without restrictions.

(iii) Reporting independence: is achieved where auditor is able to communicate his audit opinions freely devoid of external interference.

RESULTS AND DISCUSSION

The following section discusses the descriptive, results of diagnostic tests, Regression analysis hypothesis testing and findings.

Descriptive statistics

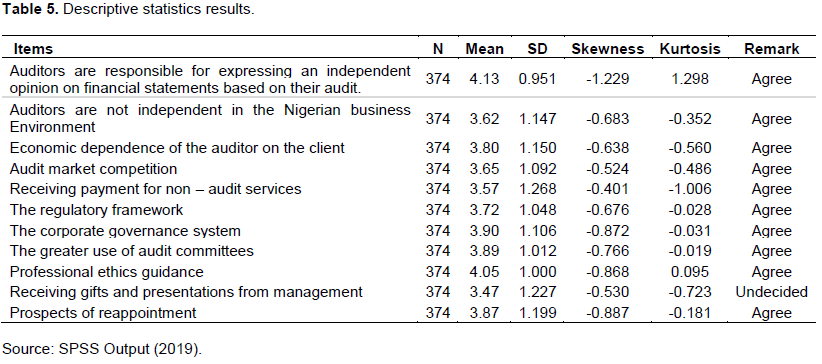

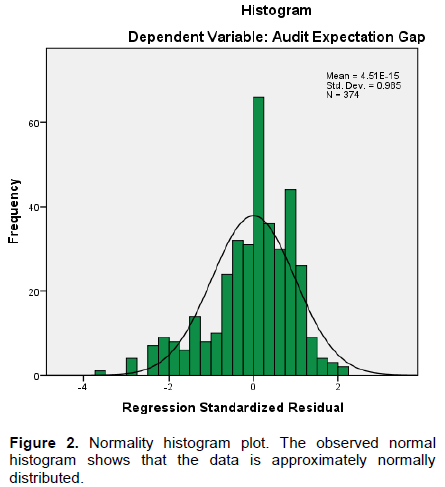

The standard deviations across all variables are relatively very small; the mean values can adequately be used to represent each construct variable, which signify that the data is approximately normally distributed (Table 5). Moreover, the respondents agreed, on the average, in each case, with the entire independence factors for audit expectations gap in Nigeria. Also the coefficients of skewness which ranges from -1 to +1 signifies moderate skewness and kurtosis are relatively small compared to their corresponding mean, which signify that the values are mostly clustered about the mean, thus the data is approximately normally distributed (Figure 2). On the average, the respondents agreed, with a mean value of 3.62, that in the Nigerian business environment the auditors are not independent. Similarly, the respondents agreed, with a mean value of 3.57, that the auditors are receiving payment for non-audit services rendered. These are potential independence factors for audit expectations gap in Nigeria.

Diagnostic tests for independence factors

The following diagnostic tests have been carried out to examine the significance of the independence factors of audit expectation gap. The R-Square of 0.188 indicate that Prospects of reappointment, expressing an independent opinion, auditors are not independent in Nigeria t, the regulatory framework, receiving gifts and presentations from client, audit market competition, professional ethics guidance, the use of audit committees, receiving payment for services not auditing related, auditor’s economic dependence on the client, the corporate governance system as components of independence factors collectively have moderate positive impact on audit expectations gap in Nigeria. Also to check the independence of observations, Durbin Watson was used. The Durbin-Watson statistic of 1.570 implies that there is no autocorrelation in the model, since the value of 1.570 is near 2 clearly implies that there is no autocorrelation in the model. Hence, the regression model is good (Table 6).

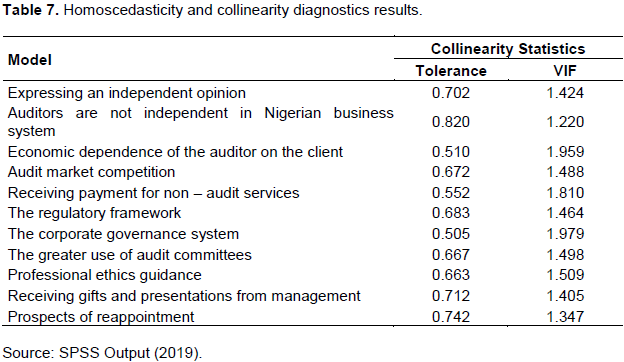

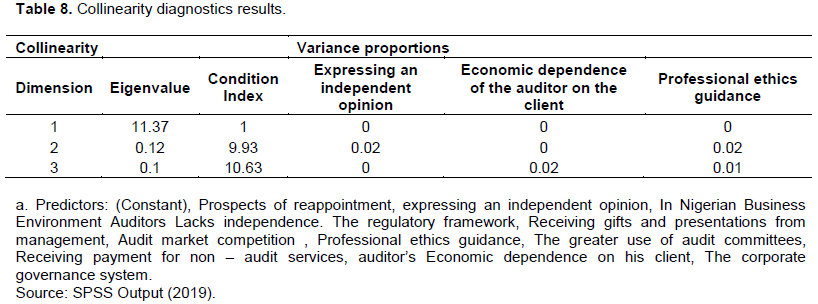

The error variances are homoscedastic and not hetrodastic, since none of the VIF is up to 10 throughout the model. The Collinearity diagnostics shows the variance inflation factor (VIF) tolerance of 0.663, 0.510 and 0.702 respectively, which signifies absence of serious multicollinearity in the data, because the independent variables do not interfere with each other. Hence, we conclude that the model is sufficient in terms of exploring linear relation as well as for prediction and control (Table 7). Another way for carrying out collinearity diagnostics test is by use of eigen value and condition index. The results shows that all the condition index values are less than 30, while the eigenvalues are small; this shows that there is no serious multicollinearity problem (Table 8 and Figure 3).

Regression analysis

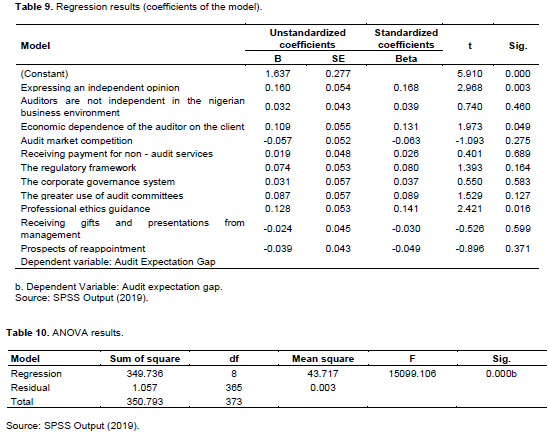

The following regression analyses were used to build linear models that explore predictability and relations among independence factors of audit expectation gap. The result of the regression equation provide a constant of 1.673 and the value of the regression coefficient which ranges from 0.031 to 0.16 this shows that independence factor accounted for between 0.031 percent and 16 percent of audit expectation gap problem. The entire standardized beta coefficient shows significant positive results (Table 9).

Tests of hypothesis

The hypothesis tested is;

H01: Auditors independence factors do not significantly impact on the audit expectation gap in deposit money banks in Nigeria. ANOVA Table 10 was used to test the research hypothesis at the 5% level of significance. The aim is to examine the significance of the factors of audit expectation.

Decision criteria

At the 5% level of significance, in each case for the regression coefficients, the null hypothesis can be rejected if the p<0.05, otherwise accept the null hypothesis. The computations using the SPSS are as follows. Table 10 shows that the independent factors are statistically significant (p<0.05). In other words, the model is good in terms of exploring linear relationship among independent factors of audit expectations gap in Nigeria as well as for prediction and control. Hence, the components of independence factors collectively have positive impact on audit expectations gap in Nigeria. Using the t-test, the model coefficients are also statistically significant (p<0.05) for expressing an independent opinion, auditor’s economic dependence and professional ethics guidance.

The result of various diagnostics tests carried out shows that; 82.4% of the respondents agreed that auditors are responsible for expressing an independent opinion on financial statements based on their audit is an independence factor for audit expectations gap in Nigeria. Also, 63.6% of the respondents agreed that auditors are not independent in the Nigeria. Again, 63.6% of the respondents agreed that the auditor’s economic dependence on client is an independence factor for expectations gap in Nigeria. Also, 60.4% of the respondents agreed that audit market competition is an independence factor for audit expectations gap in Nigeria. Again, 54.8% agreed that auditors receive payment for non-audit services is an independence factor for expectations gap in Nigeria.

Furthermore, 63.9% of those who participated agreed that the regulatory framework is an independence factor for audit expectations gap in Nigeria. Again, 70.9% of the respondents agreed that the corporate governance system in Nigeria is an independence factor for audit expectations gap. Also, 71.1% of those questioned agreed that the greater use of audit committees is an independence factor for audit expectations gap in Nigeria. Again, 73.0% of the target population agreed that the professional ethics guidance is an independence factor for audit expectations gap in Nigeria. Also, 58.0% of those who filled the questionnaire agreed that receiving gifts and presentations from management is an independent factor for audit expectations gaps in Nigeria. Again, 69.0% of the respondents agreed that a prospect of reappointment is an independence factor for audit expectations gaps in Nigeria. In general, the respondents agreed with the independence factors.

The components of independence factors like expressing an independent opinion, auditor’s economic dependence on the client, market competition for audit, receiving payment for non-audit duties, greater use of audit committee, regulatory framework, receiving gifts from management and prospects of reappointments collectively have positive impact on audit expectations gap in Nigeria. That is to say the independence factors are determinants of audit expectation gap in listed deposit money banks in Nigeria. This is in line with the findings of Salehi et al. (2019), Onulaka et al. (2019) and Amaechi and Chinedu (2017) but contradicts the findings of Kamau (2013).

CONCLUSION

The result of the hypothesis tested showed that independence factors have significant impact on audit expectation gap in listed deposit money banks in Nigeria. The study thus found out that independent factors such as expression of an independent opinion, auditor’s economic dependence on the client, audit market competition, receiving payment for non-audit services, receiving gifts and presentations from management, prospects of reappointment have positive impact on audit expectation gap. This shows that independence factors are determinants of audit expectation gap in listed deposit money banks in Nigeria. The study recommends that auditors should avoid dependence on the client for economic survival, engaging in non-audit services, avoid collecting gifts from management and that the regulatory authority of the Central Bank of Nigeria (CBN) has to emphasize on auditors tenure and that appointment of auditors shall be through a centrally controlled organize body; thus checking individual audit firms from competing among themselves.

A study can be carried out on behavioral component of audit expectation gap determinants such as auditors efforts, auditors skills etc. The study considers primary users of financial statements as target population comprising of existing investors/shareholders, lenders and other creditors.

CONFLICT OF INTERESTS

The authors have not declared any conflict of interests.

REFERENCES

|

Albaz MA (1999). The use of Causal Theory in predicting the Expectation Gap between Auditors and users of Financial Statements: An Empirical Study on Canal Governorates in Arab Republic of Egypt. The Arab Journal of Accounting 3(01):10-24. |

|

|

Alleyne PA, Devonish D, Alleyne P (2006). Perceptions of auditor independence in Barbados. Managerial Auditing Journal 21(6):621-635. |

|

|

Amaechi EP, Chinedu EF (2017). An Empirical Examination of Challenges faced by internal Auditors in Public Sector Audit in South Eastern Nigeria. Asian Journal of Economics Business and Accounting 3(2):1-13. |

|

|

Beattie V, Brandt R, Fearnley S (1999). Perceptions of auditor independence: UK evidence. Journal of International Accounting, Auditing and Taxation 8(1):67-107. |

|

|

Carmichael DR (2004). The PCAOB and the social responsibility of the independent auditor. Accounting Horizons 18(2):127. |

|

|

Chandle R, Edwards J, Anderson M (1993). Changing perceptions of the role of the company auditor. Auditing Business Research Journal 23:443-459. |

|

|

Cochran WG (1977). Sampling techniques (3rd ed.). New York: John Wiley. |

|

|

Cohen Commission (1978). The report of the Commission on Auditors on responsibilities: Reports, Conclusion and Recommendations. American Institute of Certified Public Accountants. |

|

|

Cross Committee (1977). Report of the Committee under the Chairmanship R1.Hon the Lord of Chelsea, Accountancy 160:80-86. |

|

|

Dixon R, Wood head AD, Sohliman M (2006). An investigation of the expectation gap in Egypt. Management Audit Journal 21(3):293-302. |

|

|

Dykxhoorn HJ, Sinning KE (1982). Perceptions of auditor independence: Its perceived effect on loan and investment decisions of German financial statements users. Accounting, Organizations and Society 7(4):337-347. |

|

|

Enofe AO, Mgbame C, Aderin A, Ehi-Oshio OU (2013). Determinants of audit quality in the Nigerian business environment. Research journal of finance and Accounting 4(4):36-43. |

|

|

Fadzly MN, Ahmed Z (2001). Audit expectation gap: The case of Malaysia. Managerial Auditing Journal 17(7):897-915. |

|

|

Füredi-Fülöp J (2017). Factors leading to audit expectation gap: An empirical study in a Hungarian context. Theory Methodology Practice: Club of Economics in Miskolc 13(02):13-23. |

|

|

Gay G, Schelluch P, Reid I (1997). Users' Perceptions of the Auditing Responsibilities for the Prevention, Detection and Reporting of Fraud, Other Illegal Acts and Error. Austraian Accounting Review 7(13):51-61. |

|

|

Gettler G, Gordon J, Ravlic T (2002). Corporate shake up hits Accountants. The Australian Financial Review. pp. 1-8. |

|

|

Gill GS, Cosserat G (1999). Modern Auditing in Australia. John Wiley & Sons Ltd, Chichester, United Kingdom, 1999. |

|

|

Gill GS, Cosserat G, Leung P, Coram P (2001). Modern Auditing and Assurance Services, 6th edition, Queensland: Wiley. |

|

|

Hayes RS, Schilder A, Dassen R, Wallage P (1999). Principles of Auditing: An International Perspective. McGraw-Hill Publishing Company, London. |

|

|

Humphrey C, Moizer P, Turley S (1993). The audit expectations gap in Britain: An empirical investigation. Accounting and Business Research 23(1):395-411. |

|

|

Independence Standards Board (ISB) (2000). Statement of independence concepts: A conceptual framework for auditor independence. Exposure draft, Independence Standards Board. |

|

|

Jensen MC, Meckling W (1976). Theory of the Firm: Managerial Behavior, Agency Costs an Ownership Structure. Journal of Finance and Economics 3(4):305-360. |

|

|

Kamau CG (2013). Determinants of Audit Expectation gap: Evidence from Limited Companies in Kenya. International Journal of Science and Research 2(1):480-491. |

|

|

Kamau GC, Kariuki SN, Mutiso AN (2014). Exploring internal auditor independence motivators: Kenyan perspective. |

|

|

Kleinman G, Palmon D (2001). Understanding Auditor Client Relationship: A Multifaceted Analysis, Princeton: Markus Wiener Publishers. |

|

|

Knapp MC (1985). Audit conflict: An empirical study of the perceived ability of auditors to resist management pressure. Accounting Review 60(2):202-211. |

|

|

Liggio CD (1974). Expectation gap-accountants legal Waterloo. Journal of contemporary business 3(3):27-44. |

|

|

Lin ZJ, Chen F (2004). An empirical study of audit expectation gap in the people's republic of China. International Journal of Auditing 8(2):93-115. |

|

|

Macdoald Commission (1988). Report on the Commission to Study the Publicicetedrom Limited Companies in Kenya. ed Mattersrsort on the Commission to Stud. |

|

|

Madison M (2018). Financial Statements Town of Madison, Maine June 30, 2018. |

|

|

Masoud N (2017). An empirical study of audit expectation-performance gap: The case of Libya. Research in International Business and Finance 41:1-15. |

|

|

Moizer P (1997). Independence. Current issues in auditing 3 p. |

|

|

Monroe G, Woodlif D (1994). An Empirical Investigation of the Audit Expectation Gap: Australian Evidence. Accounting and Finance Journal 34(1):47-74. |

|

|

Ogweno JA (2018). Factors affecting Audit Expectation Gap in listed Companies in Nairobi Security Exchange. KCA Academic commons, official KCAU Institutional Repository. |

|

|

Onulaka P, Shubita M, Combs A (2019). Non-Audit fees and Auditor Independence: Nigeria Evidence. Managerial Auditing Journal 34(8):1029-1049. |

|

|

Pierce A (2006). Ethics and the professional accounting firm: A literature review, Institute of Chartered Accountants in England and Wales. |

|

|

Porter B (1993). An Empirical Study of the Audit Expectation Gap-Performance Gap. Accounting and Business Research. Journal of Finance and Accounting 24(93):49-68. |

|

|

Porter BA (1990). The Audit Expectation-Performance Gap and the Role of External Auditors in Society, PhD Unpublished Thesis, Massey University, New Zealand. |

|

|

Public Oversight Board (POB) (2000). The panel on audit effectiveness report and recommendations August 31, 2000. |

|

|

Ruhnke K, Schmidt M (2014). The audit expectation gap: existence, causes, and the impact of changes. Accounting and Business Research 44(5):572-601. |

|

|

Sabuj S, Arif A, Momotaz B (2019). Audit Expectation Gap: Empirical Evidence from Bangladesh, SSRG. International Journal of Economics and Management Studies 6(5):32-36. |

|

|

Salehi M (2007). Reasonableness of Audit Expectation Gap: Possible Approach to Reducing. Journal of Audit Practice 4(3):50-59. |

|

|

Salehi M (2011). Audit Expectation Gap: concept, Nature and trace. African Journal of Business Management 5(21):8376-8392. |

|

|

Salehi M, Jahanban F, Adibian MS (2019). The relationship between audit Components and audit expectation gap in listed Companies on the Teheran Stock Exchange. Journal of Financial Reporting and Accounting 18(1):199-222. |

|

|

Schelluch P (1996). Long-form audit report messages: further implications for the audit expectation gap. Accounting Research Journal 9(1):48-55. |

|

|

Sucher P, Kosmala?MacLullich K (2004). A construction of auditor independence in the Czech Republic: Local insights. Accounting, Auditing and Accountability Journal 17(2):276-305. |

|

|

Sweeney B (1997). Bridging the expectation gap - on shaky foundations, Accountancy Ireland 2(2):18-20. |

|

|

Taylor C (2014). How to calculate the Margin of Error. Available at: www.statistics.about.com |

|

|

Toumeh AA, Yahya S, Siam WZ (2018). Expectations gap between auditors and user of financial statements in the audit process: an auditors' perspective. Asia-Pacific Management Accounting Journal 13(3):79-107. |

|

|

Tweedie D (1987). Challenges Facing the Auditors: Professional Fouls and the Expectation Gap, The Deloitt, Haskins and sells Lecture, University College, Cardiff. |

|

Copyright © 2024 Author(s) retain the copyright of this article.

This article is published under the terms of the Creative Commons Attribution License 4.0