ABSTRACT

The rise of accounting scandals has prompted the need to improve the relevance of financial reporting by setting up good corporate governance structures. The relationship between corporate governance and fraudulent activities has been strongly debated in the developed countries. It is recently that attention has turned to the study of corporate governance and financial reporting in developing countries. This paper examines and investigates the effects of corporate governance codes in curbing fraudulent activities in private organisations in Nigeria. This means that this paper is comparing two codes, the one of 2011 and the newer one of 2016. Specifically, this piece of work focuses on the characteristics of boards of directors and audit committees of 20 private companies listed on the Nigerian Stock Exchange during the period 2011-2016, by analysing whether the independent directors on boards and audit committees are associated with reduced levels of fraudulent activities. The objective of this study is to: 1) Ascertain whether a higher number of independent directors on boards of directors are associated with less fraudulent activities. 2) Investigate whether audit committees comprising independent directors are associated with less fraudulent activities. The study gathered data from the companies on the Nigerian stock exchange and the fraudulent activities variable, which is used to refer to either financial fraud or manipulated earnings was measured by discretionary accruals according to Dechow et al. (1995). The financial statements of the companies were used to determine discretionary accruals and the corporate governance variable data were obtained from the company’s corporate governance information as presented in their annual reports. The results supported the null hypotheses:1) Companies with higher number of independent directors on boards are associated with less fraudulent activities. 2) Companies with audit committees comprising independent directors are associated with less fraudulent activities. Therefore, the study adds to the limited research of the relationship between corporate governance mechanisms and fraudulent activities in Nigeria. It has also provided empirical evidence on the importance of some of the regulatory requirements established by the Nigerian Corporate Governance Codes.

Key words: Corporate governance, financial fraud, manipulated earnings, board of directors, independent directors, audit committee.

Controlling and managing corporate businesses has continued to be an issue to investors, lenders, creditors, government, accountants, regulators and all types of stakeholders in the world today. The introduction of the

recent corporate governance codes in Nigeria has enhanced supervisory roles on the board of directors to eradicate managers’ inaccuracies of financial reporting because investors, practitioners and regulators doubt the integrity of financial reporting after the various accounting scandals over the years. Throughout the 1990s and 2000s, there was a general shareholders’ dissatisfaction. Shareholder groups became increasingly critical of how management groups and boards of directors oversee their organisations. They complained about management's lack of proper accountability, ineffectiveness, excessive managerial compensation, and a general lack of focus on the importance of shareholders’ relationship with management.

The duty of directors acting as managers (agents) for owners of corporations (shareholders) has continued to cause fraudulent activities, because of the authority delegated to them to administer the affairs of these organisations. This process has led to conflict of interests as managers want to increase earnings to attract higher bonuses and shareholders want to have increased value on their shares and the maximization of long-term wealth. Honda (2015) defined an agency relationship to be a contract whereby one or more persons (principal/s) engage another person (agent/s) to perform business transactions on their behalf. If both persons in the relationship maximise values, then the principal and agent can have different objectives but the principal should be able to structure incentives with the agent’s best interests at heart; and with those incentives, the agent can perform in a way that could lead to appropriate outcomes for the principal. However, there is always a belief that the agent may not act in the best interest of the principal. This belief relates to the positive accounting theory, which assumes managers work for self-interest and exhibit opportunistic behaviour with the use of accounting methods (Watts and Zimmerman, 1990).

For the purpose of this study, fraud is defined as any irregularities and illegal acts characterized by intentional dishonesty which can be perpetrated by persons inside or outside the organization for the benefit or to the detriment of the employer; fraudulent activity is categorised into financial fraud or accounting fraud and manipulated earnings (Reurink, 2016). For fraud to occur three elements must be present: A perceived pressure, perceived opportunity, and some way to justify the fraud as acceptable. These three elements make up the fraud triangle. Ultimately, management is responsible for running firms and firms fail because of the decisions taken by their boards and management. These decisions are made within a firm’s corporate governance frame-work. As a result, fraud exposes significant shortcomings in the governance and risk management of firms and the culture and ethics which support them. This is not principally a structural issue; it could be a failure in behaviour, attitude and in some cases, competence (Young, 2002).

The purpose of this study is to analyze the relationship between corporate governance mechanisms as contained in the code and financial fraud or manipulated earnings. In particular, this write-up aims to ascertain whether companies with higher number of independent directors on boards are associated with less fraudulent activities and also to investigate whether companies with audit committees comprising independent directors are associated with less fraudulent activities.

Financial fraud and manipulated earnings

Financial fraud is defined as a deliberate misstatement or omission of amounts or disclosures in financial statements to deceive financial statement users, particularly investors and creditors (Young, 2002). The concept of fraudulent activities can be classified into financial fraud or accounting fraud and manipulated earnings. The concept of fraudulent earnings is significant if it is related to real earnings. A real earning, for business people, is a profit figure corresponding to reality or fact. Usually, earnings reported by corporations and used by investors and managers are sometimes inaccurate numbers. This is because they are based on multiple assumptions and subjective estimates. This does not mean that financial reports are useless, but it is important to set a standard for useful and high quality earnings.

Financial fraud can be committed through the following tools

(1) Falsification, alteration or manipulation of material financial records, supporting documents, or business transactions;

(2) Material intentional omissions or misrepresentations of events, transactions, accounts, or other significant information from which financial statements are prepared;

(3) Deliberate misapplication of accounting principles, policies, and procedures used to measure, recognize, report, and disclose economic events and business transactions;

(4) Intentional omission of disclosures or presentation of inadequate disclosures regarding accounting principles and policies and related financial amounts.

Fraud can be divided into two categories according to Young (2002): Management fraud and employee fraud. Management fraud is a fraud committed by a member of the management team. It is sometimes difficult to detect due to collusion; if a small mistake is not rectified when it is discovered, it can become a fraud. Some of the causes that enable fraud to occur include failure to allocate responsibility for its prevention and overriding of controls. Employee fraud is a fraudulent activity initiated by one of the company’s employee working in the day to day activities of the company. The best deterrent for fraud is an effective functioning system of internal controls, board of directors and audit committees. These are some of the corporate governance mechanisms. Rezaee (2002) identified three conditions that could motivate the involvement of employees and managers in fraudulent activities. They include Condition, Corporate structure and Choice.

Condition

Economic pressures, such as pressure to meet analysts’ earnings estimates, are one of the most relevant elements in the process of committing fraud. Costs/benefits evaluation is fundamental in this process. Managers compare the benefit in terms of positive effects on company’s stock price or the cost saving of preventing the negative impact on share price, with the possible cost consequences of fraud accomplishment in terms of probability of detection, prosecution and sanction. Financial pressures, such as inability to meet analysts’ earnings estimates or declines in quality and quantity of earnings, are often motivations for management involvement in financial frauds. Rezaee further asserts that it is obvious that very often financial frauds are linked to conditions such as: Ineffective corporate boards; existence of management with no accountability and insufficient market’s accountability and lack of responsible corporate governance.

Corporate structure

The existence of effective corporate governance mechanisms (such as internal control structure, boards of directors and audit committees) would discourage managers from committing fraud. The role of corporate governance devices can also be discussed in relation to other social and economic characteristics of different countries where fraud can be accomplished.

Choice

Independent of the external contest and corporate structure, managers have their own characteristics or choice in terms of aggressiveness and lack of moral principles; as a result fraud is also a matter of choice regardless of environmental pressure or corporate structure. Some people could be interested in committing fraud without any consideration for the consequences of their action and of the agreements.

Corporate governance

According to Cadbury (1992), corporate governance can be referred to as the pattern in which corporate businesses are organised and monitored. It is also the framework in which, the various responsibilities in an organisation are apportioned. It consists of various set of legal and institutional mechanisms aimed at safeguarding the interests of corporate shareholders and of reducing agency costs deriving from the separation of ownership (shareholders) from control (managers and/or controlling shareholders). The most important elements in a corporate governance system are the mechanisms that provide shareholders with information about the activities and the operations of the corporation, and legal rules that establish management’s and board of directors’ responsibilities as well as the penalties for irresponsible behaviours. Individuals who direct and control companies could behave in an opportunistic manner; as a result, regulators have set codes and reforms that organisations can follow to discharge their duties to stakeholders in order to minimize fraudulent activities. Notwithstanding the various regulations in place, fraud continues to occur in corporate organisations.

According to Bhasin (2016), corporate governance guarantees fairness, accountability, responsibility and transparency. It protects the interests of stakeholders including shareholders. It inspires trust and increases investors’ confidence leading to cheaper source of capital. It meets legal requirements and fiduciary responsibility to investors. It also attracts and retains directors, gains community support and competitive advantage or competitors.

Analysis of principal weaknesses in corporate governance

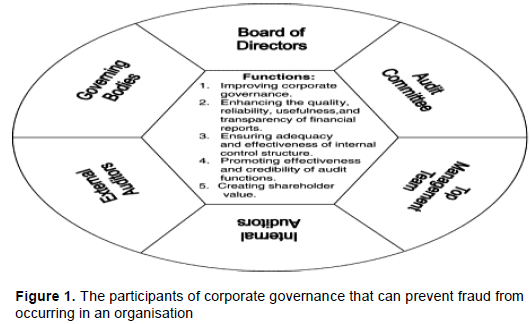

Rezaee (2005) identified in Figure 1 the participants of corporate governance that can prevent fraud from occurring in an organisation. These corporate governance participants are employed to minimize the agency problems that emanate from the relationship between shareholders and managers, and to improve investor’s confidence in companies’ financial reports. This process is referred to as the key role of corporate governance (Uwuigbe et al., 2014). However, with the existence of these roles and responsibilities, fraudulent activities still reoccur. The major weaknesses in corporate governance that give opportunity to fraudulent activities in corporations are summarized as follows.

The leadership structure

According to Zahra et al. (2005), leaders (directors) with ethical behaviours encourage a critical appraisal of lower managers and this improves honesty standards across the organization, which invariably introduces appropriate monitoring roles. Whenever boards of directors are ethical, those they appoint to administer the affairs of the organisation follows accordingly, however if they are not, then unethical behaviour may occur. For instance, if the top management level should give opportunities for fraudulent activities as a result of inadequate monitoring and controls (oversight) in place to supervise the operations of middle managers, the organisation’s transactions could be manipulated without any notice until the fraud escalates (Grant and Visconti, 2006).

Weak governance and management controls

This is among the major problems which occur in controls and management systems of corporations that sometimes lead to corporate fraud. Krummeck (2000) claimed that fraud prevails when there are opportunities for fraud to occur and that for corporations to prevent such opportunities adequate control mechanisms must be in place. For example, controls that take adequate account of risk (risk management). Krummeck further asserts that an important way of minimizing fraud is to institute risk management procedures that involve external and internal audit teams and all employees in the organisation and not just management. Luo (2005) also asserted that the structure by which jobs are allocated and apportioned could either enhance or inhibit the detection of employees’ misbehaviours. Luo further claimed that structuring responsibilities formally and clearly could increase the integrity of mangers, which gives a clear direction of each manager’s responsibility and role.

Culture

According to Willcoxson and Millet (2000), culture develops over time as organisations create patterns of behaviour and beliefs that are adequate for interactions within and outside an organisation. Krummeck (2000) claimed that for an organisation to prevent fraud a culture of zero tolerance on fraud should be introduced by those administering the affairs of organisations by working openly and honestly. Most corporate businesses do not exhibit a culture that prevents fraud rather a culture of cost reduction and profitmaking is introduced. Grant and Visconti (2006) suggest that inappropriate strategies may lead to top management aspirations rather than business reality. This happens when overambitious growth targets and lack of clear strategic directions are established.

The employees

Grant and Visconti (2006) claimed that the combination of an individual’s greed and moral negligence is assumed one of the reasons why corporate resources are plundered for private gain in a way of manipulating earnings to increase bonuses and stock options. According to Grant and Visconti (2006), Andrew Fastow at Enron and Tanzis at Parmalat are examples of employees who manipulated earnings to achieve personal gains. The above statement leads to the issue of employing ethical individuals in an organisation. The fraudulent cases for this report indicate that individuals are the source of corporate plundering.

Corporate governance reforms

According to Vera-Muñoz (2005), the numerous corporate scandals have made regulators to redefine, re-examine and reemphasize the roles of participants in an organisation’s corporate reporting procedures. In addition, responses to accounting fraud have made regulators institute regulatory measures both in the US and Europe and Nigeria has come up similarly. These regulatory measures define the duties and roles of corporate officers, reforming procedures of corporate governance, reporting and oversight establishing penalties for incompetence and opportunistic behaviour (Grant and Visconti, 2006).

The reforms are focused on (1) Audit committees; their roles are enhanced as supervisors, protectors of investors’ interest; ensuring boards complies with regulations, external and internal auditors (Vera-Muñoz 2005). Vera-Muñoz identified the benefits inherent in organisations when there are audit committees, that there is more time available for directors to deliberate and evaluate financial statements rigorously, which can lead to increased reliability of financial reports. (2) By classifying directors into executives and independent non-executive directors performing oversight functions and relating with company’s shareholders. (3) The development of modern business reporting by integrating corporate social responsibility reports as part of the traditional financial accounting reporting (Elson and Gyves, 2003).

New corporate regulations tend to minimize fraud in the future by reviewing corporate governance codes for example, SOX 2002 requiring executives, boards of directors and external auditors to ensure accountability and transparency in financial reporting. Other code reforms are on the audit committee to reduce financial fraud. However, few empirical results have shown that there is no relationship between the number of independent directors and good performance although it reduces failure and fraud. Grant and Visconti (2006) argued that the recent corporate reforms might boost effective corporate governance in a little way. It is also argued that, there are no or little evidence to show how the corporate governance reforms have affected performances of companies positively in the last few years (Benkel et al., 2006).

Corporate governance codes in Nigeria

The objective of corporate governance (CG) is to aid effective, entrepreneurial and prudent management that can produce long-term success for corporate entities. Demsetz and Lehn (1985) suggest that the primary objective of corporate governance is not to improve financial performance directly. It could consider, but it tries to curb or minimise agency problems by aligning managers’ interest with those of shareholders as nearly as possible. Corporate governance codes have developed over the years in the world and Nigeria. They are guide to a number of key components of effective board practices which are based on the principles of accountability, transparency, probity, and focus on the sustainable success of companies over a long-term period (Council, 2010). However, Benkel et al. (2006) argued that corporate governance codes established to monitor organisation’s financial transactions should effectively improve financial reporting by preventing or reducing fraudulent activities even though, it is not its primary aim.

Aguilera and Cuervoâ€Cazurra (2009) claimed that corporate governance codes have generally enhanced corporate governance by instituting roles that improve leadership, culture and controls of company’s affairs all over the world and Nigeria is not an exception. However, there is a need to enhance the codes further because of the need to prevent unnecessary accounting scandals in the future.

Boards of directors

This is one of the corporate governance mechanism contained in the Nigerian code of 2011. The board of directors is regarded as the first defence of shareholders’ interest against opportunistic managers; it comprises executive and non-executive directors. The non-executive directors are also known as independent and outside directors (Chen et al., 2007). Independent directors perform monitory and supervisory roles on the board of directors. Although their roles are not restricted to monitoring alone, they also work with executive directors in order to achieve corporate, legal and ethical compliance. They are more vigilant and able to mitigate the conflicts between shareholders and managers than the executive directors who perform the day-to-day dealings of the company. The findings of Beasley (1996) and Persons (2006) suggest that there is a relationship between the board of director’s independence and the financial reporting quality of a company. However, when the independent director’s expertise and experience could not reduce or prevent earnings manipulations, then, stakeholders tend to believe that independent directors do not perform their roles properly as supervisors and monitors (Weir et al, 2002).

External auditors

External auditors have the responsibility of complying with professional standards while planning and performing the audit of an organization’s financial statements. They perform this in order for them to obtain reasonable assurance whether the financial statements are free from material misstatements and to state whether the misstatements were caused by error or fraud if there is any. Whenever the external auditors have perceived that there is an evidence that fraud exists, the external auditor’s professional standards typically requires that the matter be brought to the attention of an appropriate level of management (Haugen and Selin, 1999). The external auditor usually reports fraud involving senior management directly to those charged with governance, for example, the audit committee. This suggests that auditing has a role to play in controlling and preventing fraud even though that is not their primary duty.

Audit committees

An audit committee, according to Chen and Zhang (2014), is a delegated body of board of directors that is mandated with the responsibility of defending and protecting the interest of shareholders. The audit committee comprises independent directors; hence, the committee is used as a supervisory model that reduces the agency problem that often arises from the relationship between shareholders and managers of companies. The audit committee primarily oversees the firm’s financial reporting process. It meets regularly with the firm’s outside/external auditors and internal financial managers to review the corporation’s financial statements, audit process, and internal accounting controls (Klein, 2002).

From the literature above, one could say that corporate governance best practices generally improve the performance of companies by reducing managers’ opportunistic behaviour. Therefore, it could be argued that the corporate governance mechanisms, especially the roles of independent directors on boards of directors and audit committees have reduced earnings manipulations. This is as a result of the monitoring roles delegated to independent directors and audit committees stated in the CG codes.

A number of authors have focused on researching the relationship between corporate governance and fraudulent activities but with little reference to Nigeria (Dedman, 2002; Peasnell et al., 2000, 2005). This has created a gap in the literature, even though some research was done on accounting fraud itself (Kehinde, 2015; Akeem, 2015). Hence, this study aims to reduce this gap by conducting a research on Nigerian companies listed on the stock exchange between the periods of 2011-2016.

This study specifically focuses on the independence of the board of directors and the independent directors in audit committees. The following hypotheses are to be tested for this study.

H1: Companies with higher number of independent directors on boards are associated with less fraudulent activities.

H2: Companies with audit committees comprising independent directors are associated with less fraudulent activities.

To investigate and ascertain the effects of corporate governance mechanisms on fraudulent activities in private companies, a sample of 20 non-financial companies listed on the Nigerian Stock Exchange during the periods of 2011-2014 with fiscal year ending 31st December were ascertained. Financial companies were excluded because they have distinctive features compared to non-financial companies. This study uses the Nigerian Corporate Governance Code of 2011 as a guide for determining the corporate governance variables. The data for fraudulent activities or manipulated earnings (financial data) will be extracted from the company’s financial statements as shown on the financial reports of the sampled companies, whilst the corporate governance mechanisms data are sourced from the company’s annual reports.

Fraudulent activities model

Fraudulent activities, termed as manipulated earnings, are used as the dependent variable in this study. Although a number of models have been developed to estimate discretionary accruals which they use as a measure for manipulated earnings (Becker, Connie L., Mark L. DeFond, James Jiambalvo, and K. R. Subramanyam. "The effect of audit quality on earnings management." Contemporary accounting research 15, no. 1 (1998): 1-24.), there is no perfect measure for manipulated earnings. Therefore, this research uses the Modified Jones Model (MJM), which Dechow et al. (1995) described as the most powerful model for measuring discretionary accruals. The model requires industry classification on the companies used and data over a lengthy time series; however, it does not require large sample size. The modified cross sectional Jones model described by Dechow et al. (1995) is estimated for each industry or sector across the study period (2011-2016) using the following expression. The formula for total accruals is stated as:

TAC i, t = α1 (1 / TA it -1) + a2 (Δ REV it / TA it -1) + a3 (PPE it / TA it -1) + ε i, t… (1)

Where: For fiscal year t-1 and firm i, TAC represents total accruals; it is also calculated as:

TAC =NI –CFO. Where TAC = total accruals, NI= net income/net profit after tax and CFO= cash flow from operations taken from the cash flow statements of the company.

TAt-1 = total assets from previous fiscal year (t-1).

Δ REV i, t =the change in revenue from the previous year

a1, a2, a3= firm-specific parameters, the estimates of a1, a2, a3 that are calculated by ordinary least square regression (OLS).

PPE i, t = gross property plant and equipment in year t

Æ i, t = the measurement error in the year t

This model, according to Dechow et al. (1995), introduces the change in revenue and the level of gross property, plant and equipment to capture the economic condition of the company. The model was originally introduced as a time series model (Jones model). However, DeFond and Jiambalvo (1994) introduced the cross-sectional discretionary accruals model, which was used in previous studies (Klein, 2002; Xie et al., 2003). After calculating the total accruals of a company, as stated in Equation 1, the coefficient estimates from Equation 1 are then used to estimate the company’s specific non-discretionary accruals (NDA) for the sampled companies by using the formula,

NDA i, t = a1 (1 / TA it -1) + a2 (Δ REV it - Δ REC it) / TA it -1) + a3 (PPE it / TA it -1) … (2)

Where: NDA i, t= non-discretionary accruals in year t, company (i) scaled by total assets in t-1 year; ΔREC i, t = the change in account receivables from the previous year.

When the amount of the non-discretionary accruals value is determined from Equation 2, then the amount of discretionary accruals is determined for the sampled companies (i) in year (t) by substituting the values of total accruals and non-discretionary accruals into the following equation:

DA i, t = TAC i, t / TA i, t – NDA i, t (3)

Where, DA = discretionary accruals, TAC =total accruals, TA=total assets and NA=non-discretionary accruals. A positive (DA) means the existence of fraudulent practices, whilst a negative (DA) means that there is no fraudulent practice in a company. Therefore, the value (1) is used to represent negative (DA) and (0) otherwise.

Corporate governance mechanisms

The corporate governance mechanism is measured as the independent variable in this study by the following specific variables: independent directors and audit committee. These corporate governance variables will be used to test the hypothesis formulated in this study.

Independent variables

The variable (INDDIR) is defined as the number of independent directors on boards of directors divided by the total number of directors on the board (Chen et al., 2007). Independent directors are also known as non-executive directors; they are the management team that supervises the executive managers (Shakir, 2008). Two variables are introduced to capture the effectiveness of audit committees. Firstly, the variable (AUDCOM) reflects the role of an audit committee in controlling fraudulent activities. Hence, the value (1) is used to indicate if a company has established an audit committee and (0) otherwise. Secondly, the variable (INDAUD) is used to identify the number of independent directors in an audit committee.

Control variables

In line with existing literature, in order to investigate and capture a company’s specific factors on fraudulent activities and to capture a company’s corporate governance characteristics, the following control variables are built into the regression model aimed at testing the research hypotheses.

The variable (BRDSIZE) is used to represent the board size and is defined as the total number of directors on boards, and the variable (CFO), which is referred to as the cash flow from operations, is included as a control variable. It is used as a control for accruals management in a company (Dechow et al., 1995; Peasnell et al., 2000). These variables are included into the regression model as explanatory variables because they can potentially affect the independent variables and dependent variable. Therefore, if they are not included, the result of the study may suffer from omitted variable bias.

The regression model

A regression model is constructed to test the hypotheses formulated. It is used to establish whether the corporate governance mechanisms (independent directors and audit committees) are associated with reduced levels of fraudulent activities using the sampled companies. The Pearson’s correlation coefficient will be used to test for the relationship between the variables and any indication of multicollinearity will be discussed. The word multicollinearity is often used to refer as a phenomenon that affects a study’s results when there is an indication that two or more variables are highly correlated in a multiple regression model. The dependent variable is manipulated earnings measured by discretionary accruals (DA), whilst the independent variables are the corporate governance mechanisms, which are INDDIR, AUDCOM and INDAUD. The control variables are BRDSIZE and CFO, the overall regression model is formulated as:

DAi,t =β0 +β1INDDIRi,t + β2AUDCOMi,t + β3INDAUDi,t + β4BRDSIZEi,t + β5CFOi,t + Æi,t.

The aim of this study is to:

1). Ascertain whether a higher number of independent directors on boards of directors are associated with less fraudulent activities.

2). Investigate whether audit committees comprising independent directors are associated with less fraudulent activities.

This study applied data from the Nigerian stock exchange (NSE) for 20 sampled companies in the periods of 2011 to 2016. The results of the descriptive and regression statistics are discussed as follows.

Descriptive statistics

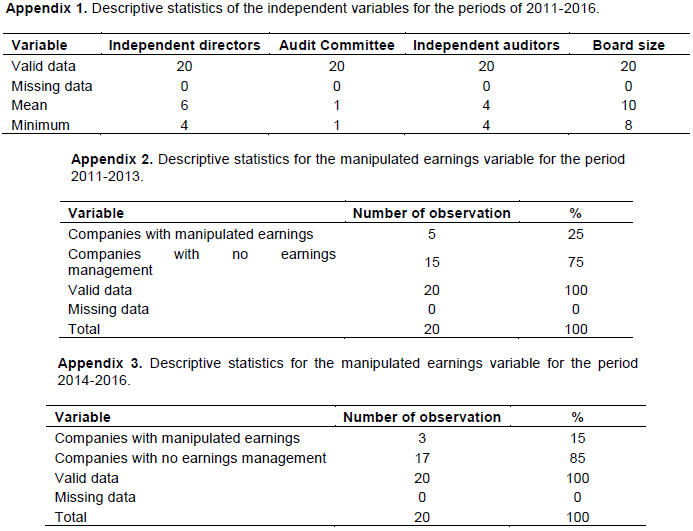

The descriptive statistics for the independent directors, audit committees and board size variables are presented in Appendix Table 1 for the periods 2011-2016. For the six years (2011-2016) in each company the average board of directors contained 11 directors, 6 of whom are independent directors and all the companies in the period have audit committees with an average number of 4 and a minimum of 2 members. This shows that the companies are following the corporate governance codes that state that every company must have more independent directors on the board of directors and must establish an audit committee with at least one independent director as a member.

Discretionary accruals

The discretionary accrual figures were used to represent and measure the level of fraudulent practices, that is, manipulated earnings. The discretionary accruals for each company were coded value (1) for companies with negative figures and (0) for companies with positive figures. Appendices Tables 2 and 3 show the descriptive statistics of the periods of the discretionary accruals variable. From the observation, about 25% of the firms practiced manipulated earnings in the early years of 2011-2013, whilst, it was only 15% in the later years (2014-2016). Therefore, companies without manipulated earnings practices increased from 75 to 85% in the years of observation.

Regression statistics

The independent variables were used to correlate the dependent variables in order to determine the association/relationship between the corporate governance mechanisms and manipulated earnings.

Results of hypothesis testing

Independent directors on board’s result

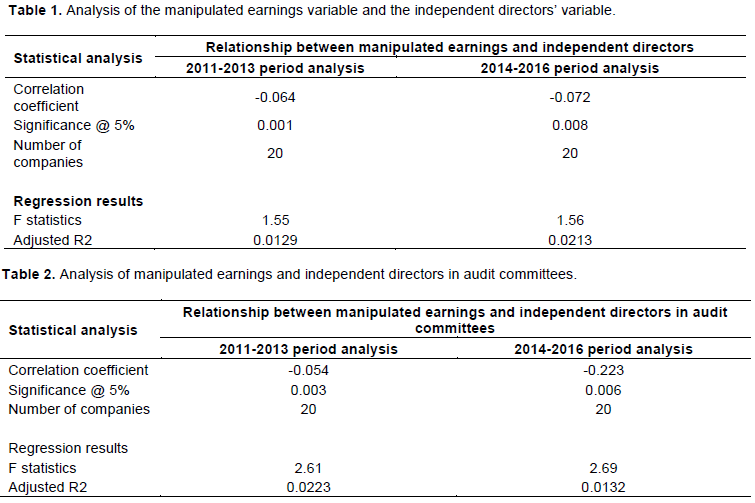

The first hypothesis (H1), which stated that companies with higher number of independent directors on boards are associated with less fraudulent activities, was supported. From the findings, the Pearson correlation of the independent directors and manipulated earnings variables were negative and significant at .001, which is below the 5% significant level. The Pearson correlation indicated a perfect negative correlation between the manipulated earnings and the independent directors’ variable (Table 1). The regression result gave an f statistic of 1.55 and an adjusted R2 0f 0.0129 for 2011-2013 periods and an f statistic of 1.56 and an adjusted R2 of 0.0213 for the years 2014-2016. The f statistics and the adjusted R2 are higher than the 5% significant level set for this study. Therefore, the result does not occur by chance and it supports the hypothesis. The result also shows that the variables of this study have fitted into the regression line and the results do not occur by chance.

Audit Committee result

The results supported hypothesis 2 (H2), which stated that companies with audit committees comprising independent directors are associated with less fraudulent activities (Table 2). The Pearson correlation (correlation coefficient) result for the 2011-2013 period as regard the number of independent directors in audit committees revealed an f statistic of 2.61 and an adjusted R2 of 0.0223 and an f statistic of 2.69 and an adjusted R2 of 0.0132 for 2014-2016 periods. The f statistics and the adjusted R2 are higher than the significant level of 0.003 and 0.006. The coefficient of the independent directors on audit committees’ variable is negative and lower than the 5% significant level set for this study; which means that the correlation is significant. Therefore, the result does not occur by chance, it provides evidence supporting hypothesis 2.

CONCLUSION AND RECOMMENDATIONS

From the findings, it is clear that the independence of directors on boards, the establishment of Audit Committees with independent directors as members, through their monitory/supervisory roles have effectively reduced fraudulent activities used in this study as manipulated earnings practices. Moreover, the normal boards of directors and audit committees established in companies without the supervisory roles of independent directors could reduce manipulated earnings, but the presence of independent directors could enhance the roles of boards and audit committees further. Therefore, the practice of manipulated earnings could be highly minimized when companies have effectively implemented the Corporate Governance mechanisms as contained in the code. This was evidenced in the case of the companies used for this study especially when the newer codes were enacted.

The study therefore recommends that:

(1) Corporate governance codes should be reviewed by governing bodies of a country to include the issue of manipulated earnings so that these manipulations and other financial irregularities could be reduced, controlled and prevented.

(2) It may be useful for further research to examine the relationship between manipulated earnings and executive directors on the board of directors, instead of non-executive (independent) directors on boards. This will reveal the role of executive directors in reducing fraudulent activities.

Limitation of the study

The first problem that is associated with this research is not having sufficient access to accurate financial reports that will reveal the true financial and corporate governance status of the sampled companies. It is also possible that some specific information needed in terms of the company’s board arrangements (corporate governance data) may not be available due to the sensitive nature of the information and the companies might present inaccurate and incomplete data on the (internet) database. Another factor that limits this study is time, as the time given for this research is limited. These factors might limit the credibility of the research by providing invalid results.

The authors have not declared any conflict of interests.

REFERENCES

|

Aguilera RV, Cuervoâ€Cazurra A (2009). Codes of good governance. Corporate Governance: An International Review 17(3):376-387.

Crossref

|

|

|

|

Akeem LB (2015). The impact of auditing in controlling fraud and other financial irregularities. International Journal of Empirical Finance 4(3):147-164.

|

|

|

|

|

Beasley MS (1996). An empirical analysis of the relation between the board of director composition and financial statement fraud. Accounting Review 71:443-465.

|

|

|

|

|

Benkel M, Mather P, Ramsay A (2006). The association between corporate governance and earnings management: The role of independent directors. Corporate Ownership and Control 3(4):65-75.

Crossref

|

|

|

|

|

Bhasin LM (2016). Fraudulent Financial Reporting Practices: Case Study of Satyam Computer Limited. The Journal of Economics, Marketing and Management 4(3):12-24.

|

|

|

|

|

Cadbury A (1992). Cadbury report: The financial aspects of corporate governance. Technical Report, HMG, London, UK pp. 1-10.

|

|

|

|

|

Chen JJ, Zhang H (2014). The impact of the corporate governance code on earnings management-evidence from Chinese listed companies. European financial management 20(3):596-632.

Crossref

|

|

|

|

|

Chen KY, Elder RJ, Hsieh YM (2007). Corporate governance and earnings management: The implications of corporate governance best-practice principles for Taiwanese listed companies. Journal of Contemporary Accounting and Economics 3(2):73-105.

Crossref

|

|

|

|

|

Council FR (2010). The UK corporate governance code'. London: Financial Reporting Council pp. 1-40.

|

|

|

|

|

Dechow PM, Sloan RG, Sweeney AP (1995). Causes and consequences of earnings manipulation: An analysis of firms subject to enforcement actions by the SEC. Contemporary Accounting Research 13(1):1-36.

Crossref

|

|

|

|

|

Dedman E (2002). The Cadbury Committee Recommendations on Corporate Governance–A review of compliance and performance impacts. International Journal of Management Reviews 4(4):335-352.

Crossref

|

|

|

|

|

DeFond ML, Jiambalvo J (1994). Debt covenant violation and manipulation of accruals. Journal of Accounting and Economics 17(1):145-176.

Crossref

|

|

|

|

|

Demsetz H, Lehn K (1985). The structure of corporate ownership: Causes and consequences. The Journal of Political Economy 93(6):1155-1177.

Crossref

|

|

|

|

|

Elson CM, Gyves CJ (2003). Enron Failure and Corporate Governance Reform. Wake Forest Land Review 38:855.

|

|

|

|

|

Grant RM, Visconti M (2006). The strategic background to corporate accounting scandals. Long Range Planning 39(4):361-383.

Crossref

|

|

|

|

|

Honda A (2015). Analysis of agency relationships in the design and implementation process of the equity fund in Madagascar. BMC Research Notes 8:31.

Crossref

|

|

|

|

|

Haugen S, Selin JR (1999). Identifying and controlling computer crime and employee fraud. Industrial Management and Data Systems 99(8):340-344.

Crossref

|

|

|

|

|

Kehinde JS (2015). Asset Protection and Financial Statement Fraud: The Audit and Management Function in Nigeria Business Organisation. Journal of Policy and Development Studies 9(3):166-175.

Crossref

|

|

|

|

|

Klein A (2002). Audit committee, board of director characteristics, and earnings management. Journal of Accounting and Economics 33(3):375-400.

Crossref

|

|

|

|

|

Krummeck S (2000). The role of ethics in fraud prevention: a practitioner's perspective. Business Ethics: A European Review 9(4):268-272.

Crossref

|

|

|

|

|

Luo Y (2005). An organisational perspective of corruption. Management and Organisation Review 1(1):19-154.

Crossref

|

|

|

|

|

Peasnell KV, Pope PF, Young S (2000). Accrual management to meet earnings targets: UK evidence pre and post Cadbury'. British Accounting Review 32(1):15-45.

Crossref

|

|

|

|

|

Peasnell KV, Pope PF, Young S (2005). Board monitoring and earnings management: do outside directors influence abnormal accruals? Journal of Business Finance and Accounting 32(7â€8):1311-1346.

Crossref

|

|

|

|

|

Persons OS (2006). Corporate governance and non-financial reporting fraud. The Journal of Business and Economic Studies 12(1):27-41.

|

|

|

|

|

Reurink A (2016). Financial Fraud: A Literature Review. Discussion Paper 16/5. May, Max Planck Institute for the Study of Societies, Cologne, 21.

|

|

|

|

|

Rezaee Z (2002). Financial Statement Fraud Prevention and Detection, John Wiley and Sons, Inc. pp. 6-10.

|

|

|

|

|

Rezaee Z (2005). Causes, consequences and deterrence of financial statement fraud. Critical Perspective on Accounting 16(1):277-298.

Crossref

|

|

|

|

|

Shakir R (2008). Board Size, Board Composition and Property Firm Performance. Pacific Rim Property Research Journal 14(1):1-16.

Crossref

|

|

|

|

|

Uwuigbe U, Peter DS, Oyeniyi A (2014). The effects of corporate governance mechanisms on earnings management of listed firms in Nigeria. Accounting and Management Information Systems 13(1):159-174.

|

|

|

|

|

Vera-Mu-oz SC (2005). Corporate governance reforms: Redefined expectations of audit committee responsibilities and effectiveness. Journal of Business Ethics 62(2):115-127.

Crossref

|

|

|

|

|

Watts RL, Zimmerman JL (1978). Towards a positive theory of the determination of accounting standards. Accounting Review 53(1):112-134.

|

|

|

|

|

Weir C, Laing D, McKnight PJ (2002). Internal and external governance: their impact on the performance of large UK public companies. Journal of Business Finance and Accounting 29(5â€6):579-611.

Crossref

|

|

|

|

|

Willcoxson L, Millett B (2000). The management of organisational culture. Australian Journal of Management and Organisational Behaviour 3(2):91-99.

|

|

|

|

|

Xie B, Davidson WN, DaDalt PJ (2003). Earnings management and corporate governance: the role of the board and the audit committee. Journal of Corporate Finance 9(3):295-316.

Crossref

|

|

|

|

|

Young MR (2002). Accounting Irregularities and Financial Fraud, a Corporate Governance Guide. Journal of Law and Business 2(1):7-10.

|

|

|

|

|

Zahra SA, Priem RL, Rasheed AA (2005). The antecedents and consequences of top management fraud. Journal of Management 31(6):803-828.

Crossref

|

|