Full Length Research Paper

ABSTRACT

Compensation incentive schemes are mainly driven by the need to align owner-manager interests in the real corporate world of separation of ownership and control. We find that the role of taxes and its implication for employees’ compensation is, at best, evidently inconclusive in the compensation-taxation literature. Using a literature review/synthesis of the existing research approach, we begin by identifying three distinct forms of employees’ compensation. Then, we examine developing and current state of extant research in order to review the role of taxation and its implication in the corporate choice, and magnitude of remuneration packages. In particular, we highlight the units of investigation in those studies, contextualize their findings, identify gaps or areas that have not been accorded much research attention, and offer suggestions for future analysis and research in this area of taxation vis-à-vis compensation packages.

Key words: Employees’ compensation, taxes, incentive alignment.

INTRODUCTION

Compensation incentive schemes are mainly driven by the need to align owner-manager interests in the real corporate world of separation of ownership and control (Jensen and Meckling, 1976). While there is a long strand of research documenting positive earnings-compensation relation (Chan et. al., 2014), the role of taxes and its implications for employees’ compensation (i.e. compensation-taxation relation) is, at best, evidently inconclusive in the literature. An Increasing number of research in the empirical domain integrates agency theory into the investigation of corporate tax avoidance. Their findings however are inconclusive. Even taxed-based accounting research has consistently been providing mixed evidence in the literature as to the relevance of taxation to employees’ compensation. While some find taxes to play significant roles, others find no direct or demanding role or significant implication of taxation in the corporate choice or decision regarding employees’ compensation (Dechow et al., 2010). Therefore, the extent firms consider taxation as an input in their choices of compensation packages remains an empirical question, especially since at a macro level, Frydman and Molloy (2011) find “…no relationship between changes in tax rates and changes in pay” and that this lack of relationship or negligible effect of taxes on compensation dates back to 1980s.

At the top management level, it is not uncommon to find some forms of compensation packages that are tied to cost reduction. In fact, Ittner et al. (1997) report that some bonus contracts reward “cost reduction”. It can thus be argued that many executives may see tax expense (within a profit center) as a cost to be cut in their overall cost minimization strategy. Very recent studies such as Schmittdiel (2014) show that through compensation contracts, executives (CEOs in particular) are encouraged (“incentivized”) to engage in aggressive tax planning (avoidance) activities. In fact, Schmittdiel suggests that CEO’s bonuses should be tied directly to tax payments. Armstrong et al. (2012) also show that firms explicitly reward tax directors to incentivize them to “reduce the level of tax expense reported in the financial statements”. This suggests that firms use compensation to reward tax aggressiveness especially as it relates to GAAP effective tax rates. However, it must be noted that such a practice could backfire as such tax aggressiveness can invite increased scrutiny from tax authorities which may cost the firm future large cash outflow (in the form of back taxes, penalties and fines) when earlier tax positions cannot be sustained upon the Internal Revenue Service (IRS) audit. Schmittdiel writes, “shareholders reward income increase that comes from tax savings more strongly than other net income increases”, thereby concluding that CEOs are “incentivized” to pursue aggressive tax avoidance strategies for favorable compensation contracts. If this is true, then it extends research into the realm of reality that investors not only incentivize tax aggressiveness but also reward earnings management. Clearly more research is needed to ‘legitimize’ this assertion.

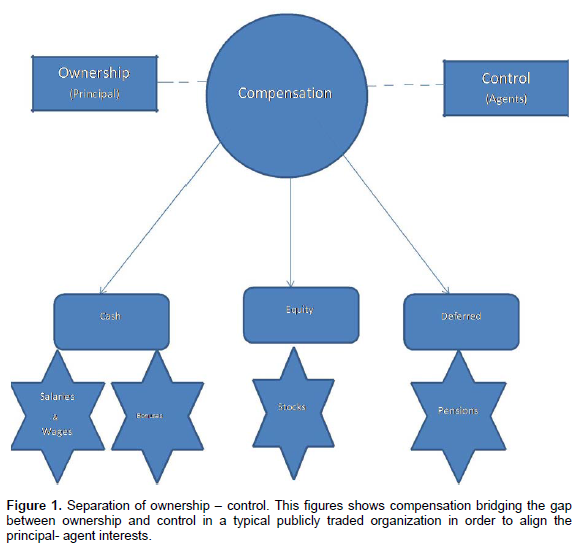

Researchers find that managers are less likely to manage compensations accounts for ‘contracting reasons’ because most compensation contracts are generally based on pretax earnings (Hanlon and Heitzman, 2010). In fact, Desai and Dharmapala (2008) report a negative relationship between equity-based compensation and book-tax difference (a proxy for tax avoidance). They also show that firms use ownership structures to minimize the effect of taxes on compensation. For example, partnership tax status in the U.S. allows preferential tax treatment on partner’s carried interest compensation as this is taxed at tax-favored capital gains tax rates and not ordinary income tax rates. We must note that this relates mostly to partners in private equity firms and not employees. It should be noted that employees’ compensation[1] can be cash-based, equity-based[2] or deferred. The cash-based compensation could be of many kinds which include, but not necessarily limited to, regular wages and salaries, and stock appreciation rights. On the other hand, stock-based compensation is primarily in the form of employees’ stock options, which can also include performance motivated stock appreciation rights[3]. Deferred compensations are mainly in the form of pensions or pensionable benefits.

The paper proceeds as follows: the methodology is presented in the next section. In section three, each of these employees’ compensation packages is discussed in sequence vis-à-vis the developing and current state of extant research reflecting on tax role and its implication in the corporate choice, and magnitude of these remunerations. Concluding comments are provided in the last section (Figure 1).

[1] Except otherwise stated, employees’ compensation is meant to include all employees (top management and CEOs inclusive). Although, the fact that stock-based compensation is commonly applied to CEOs and top management for strategic motivational/incentive reasons, middle or lower-level employees generally are seldom given such a booty especially in the form of stock appreciation rights. This is not an assertion!

[2] This categorization could be arbitrary in that stock-based compensation could be transformed into cash for employees even directly from the company in the form of stock appreciation right. Notwithstanding, a general purpose categorization could be made for intellectual curiosity.

[3] It should be noted that there is also Employee Stock Ownership Plans (ESOP). It is not considered in this discussion.

METHODOLOGY

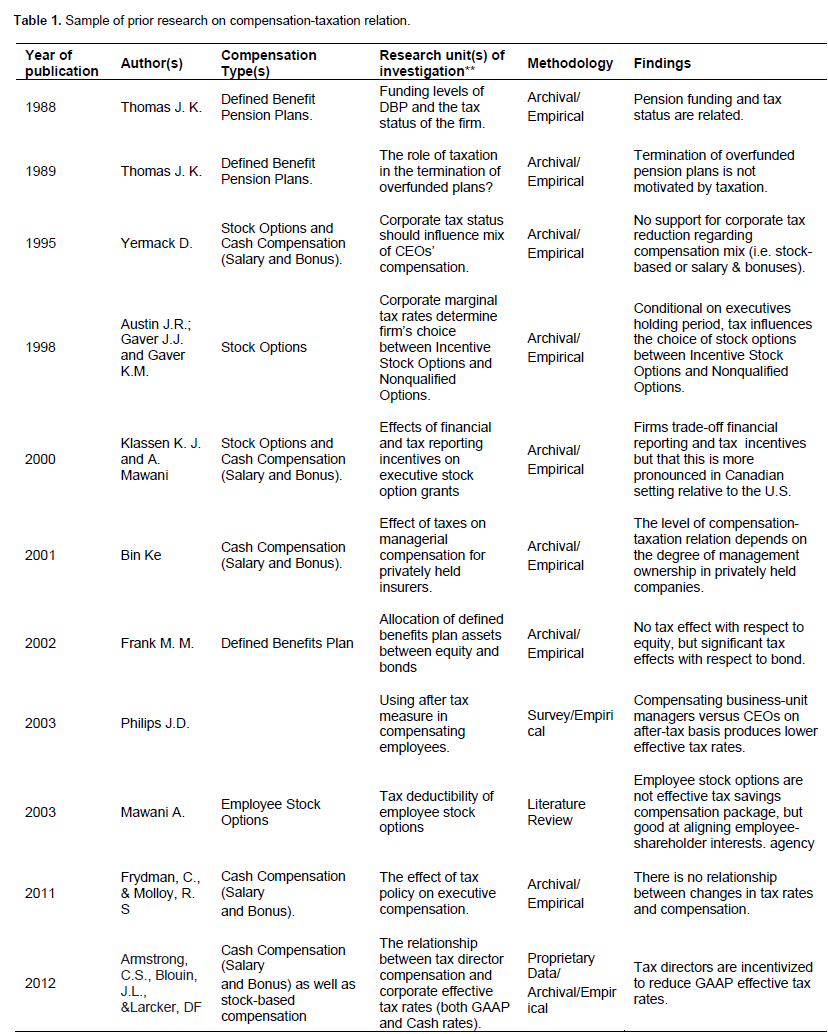

Due to the perceived importance of taxation and its ramifications on the dynamics of employees’ compensation, we provide a synopsis of a review and synthesize existing research on the compensation-taxation relation. A review of hundreds of identified papers that contextualize compensation-taxation relation was performed to examine the role (if any) that taxation plays in employee compensation. After extensive review of studies in this area, we identify studies that precisely examine corporate taxation and employee compensation (i.e. connecting compensation with taxation). The publication dates for these studies range between 1988 and 2014. The sample of the publications is tabulated below in terms of the units of investigation examined, methodologies employed, and findings obtained.

Each of the two researchers involved in the current review independently sampled and reviewed at least 100 academic publications in accounting, finance and related literatures. The articles reviewed focus on compensation-taxation relation vis-à-vis the three distinct forms of employees’ compensation (cash-based, equity-based, and deferred). After extensive review, both researchers mutually agreed on the identified units of investigation in the sampled studies and then evaluate their findings which produce the basis for further analysis in our study.

Within the compensation –taxation framework, the analysis constructively categorizes the forms of employees’ compensation packages into cash compensation, equity-based compensation and pension plans. Cash compensation primarily includes salaries and bonuses. Equity-based compensation focuses on stock options and the pension plans primarily examine defined benefit pension plans. The emerging issues for future academic studies are identified and discussed to advance knowledge in this important area of accounting and taxation research (Table 1).

RESULTS/DISCUSSIONS

Salaries and wages or other regular remunerations

This form of employee’s compensation is not expected to have direct impact on tax related corporate decisions when it comes to employee/executive compensation. Common opinion perceives this compensation expense as a given and that corporations’ commitment on meeting this obligation might be highly inflexible or involuntary. This translates to the fact that limited manipulations could be made for corporate tax-arbitrage.[1] It is therefore, not surprising that its consideration in the literature is almost nonexistent or at best passive with related studies consistently finding no or mixed results when it comes to its compensation-taxation relation. However, a study that can fit into this category is the one by Philips (2003) who investigates the effectiveness of corporate tax planning vis-à-vis the role of compensation-based incentives and firms’ choice to using pre or after-tax basis for employees’ compensation. He finds that “compensating business-unit managers, but not executive officers, on an after-tax basis leads to lower effective tax rates”.[2]

A different but related study by Ke (2001) documents that the interconnectivity between individual tax rates and corporate tax rates (within a time period) is capable of influencing the character of managerial compensation in terms of such compensation’s tax-deductibility. It is important to interpret the findings of the study in its context in that the study is based on privately held insurance companies. Therefore, the incentives for aggressive tax planning cum financial reporting strategies generally embarked upon by publicly quoted corporations are virtually nonexistent within the context of that study. Notwithstanding, the study is valuable in enhancing researchers’ appreciation of the tax planning opportunities and strategies pursuable in privately held organizations. Some research questions that require further exploration include the sensitivity of compensation packages to a firm’s foreign presence, leverage, and capital investment intensity. Schmittdiel (2014) explores those but only within the realm of bonus contracts and finds mixed or inconclusive results.

[1] This does not mean that this form of employees’ compensation is completely tax irrelevant. Usually, corporate tax arbitrage intentions might significantly impact the magnitude (and not the choice) of this form of compensation especially within the context of substitution dynamics.

[2] Without prejudice to the rigorous analysis methodologically displayed in the study, it is worthy to mention that this study is an empirical survey and so the findings need to be cautiously interpreted especially in term of its generalizability.

Unlike the form of compensation discussed above, stock-based employees’ compensation has enjoyed much (if not most) of researchers’ attention in tax-based accounting research (Hanlon and Heitzman, 2010). Some of the research outputs in this area are now reviewed to understand the developing state of the debate and the prospect for future academic development in this important area of tax and accounting research.

Individuals, firms, and even non-tax sensitive institutions engage in tax avoidance strategies because of its value-creation potentials. It is, therefore, expected that firms should be willing to compensate employees using after-tax remuneration incentives. Phillips (2003) finds results consistent with this proposition, but Desai et al. (2007) show that Phillips’ finding did not hold for equity-based remunerations.

Tax and non-tax factors as well as Pareto optimal considerations usually drive corporations’ decisions to employ this form of compensation (Thornton, 1999; Scholes et al., 1992). Therefore, it will not be out of place to reason that corporations will want to make voluntary stock-based employees’ compensation to minimize tax liability. While it is generally believed that taxes do play a significant role in the design, choice, and mechanics of stock-based compensation (Graham, 2008), the interesting conclusion regarding its (optimum) magnitude so far is inconclusive with mixed evidence in the literature as to the role or implication of taxation in this regard.

In what appears as a rather intellectual discomfort with the use of stock options as compensation for managers, Johnson (2003) believes that using stock options to compensate managers and CEOs could turn out inimical to the corporation’s strategic existence and thus run contrary to shareholders’ interests. For example, the author asserts “managers with significant options have an incentive to take the company into suicidal risks because option holders do not participate in the shareholders’ losses” (see also Akindayomi, 2006). It can be argued (in our opinion) that while the former part of the Johnson statement could be true, the latter part is much of a stretch. This is because employees/executives with substantial wealth tied to the company (i.e. ‘wealth specificity’) could face considerable erosion of wealth if stock prices significantly drop over a long period of time.

Our understanding of Johnson’s contention in this study is that stock options could be a bad corporate idea, not necessarily because it could not lead to minimization of corporate tax liability (i.e. it could be tax-relevant), but that their use could further precipitate agency problems as managers could selfishly engage in the pursuit of sub-optimal goal(s) which may deceptively signal corporate long-term prospects given its short-term success.[1] Similarly, compensating employees/executives with stocks instead of cash could further increase free cash flow available to managers. Jensen (1986) expresses concerns that such free cash flows are susceptible to diversion towards maximizing managers’ utility at the potential huge costs to shareholders.

It can be argued that Johnson’s ‘dislike’ for the use of stock options within a compensation package, as documented in the literature, offers vital opportunity for future empirical studies. Studies aimed at empirically documenting the relationship between corporate use of stock-based compensation and corporate failure will interestingly confirm or disconfirm

Johnson’s anxiety is this regard and shows if his contention is appropriately placed. This is important in that Klassen and Mawani (2000) provide statistics that stock options are increasingly becoming a significant part of executives’ compensation package both in Canada and the U.S. Yermack (1995) earlier raised concerns as to the high probability that stock options are being abused by managers who engage in “managerial self-interest, or rent-seeking behavior by senior management.”[2]

In what seems like contemporaneous study, Mawani (2003) portrays stock options in a more positive light claiming, for example, that instead of stock options widening the incentive asymmetry gap between managers and the shareholders, they can actually be used to align “the employees’ interests and long-term incentives with those of shareholders” thus potentially reducing agency costs. Klassen and Mawani (2000), in their study of option grants to Canadian CEOs, examine the relationships and interrelationships between financial reporting and tax reporting incentives vis-à-vis stock-based compensation.[3] They find that there is a significant relationship between their “proxies

[1] There are other implications and potent inferences that could be drawn from the Johnson study. For example, he sees stock options as flamboyant accounting terminology/technology to cosmetically give deceptive financial information. He vigorously asserts that stock options are not free.

[2] Yermack’s concern appears the same with Jensen’s concern. However, both concerns are different if one contextualizes the possible cause of the abuse. Jensen considers free cash flows while Yermack looks at no- free cash flow contexts, but still maintains that managers can still be self-seeking. Therefore, it is not tautological to mention both.

[3] This study has consistent objectives with similar studies like Yermack (1995) and Matsumaga (1995) in the U.S. except for the context differences between US and Canada, which of course is research sufficient for rich empirical investigations.

for short-run financial reporting incentives and the observed option grants.” Relatedly, they find evidence that “option granting behavior is correlated with proxies for tax incentives.” The significance of their study is that both financial reporting and tax reporting incentives impact the option granting behaviors of corporations. This finding is not that surprising in that given Canadian institutional tax context regarding option granting,[1] one would expect corporations to trade-off between both (financial versus tax) incentives compared to their counterparts in the U.S.

The Klassen and Mawani findings above are markedly in contrast with Yermack (1995)’s findings which, among others, do not find either financial reporting or tax status of corporations influencing their option granting behaviors. Matsunaga (1995) also contributed to the intellectual unease by showing that there is a positive relationship between a firm’s financial reporting costs and the likelihood of granting stock options to employees. In fact, apparently expressing frustrated satisfaction on the inconclusive or mixed evidence with respect to the role of taxes on stock options, Shackelford and Shevlin (2001) are forced to conclude (in their judgment) that taxes are not an important determinant of individual firm’s choice between Incentive Stock Options (ISOs) and Non-Qualified Stock Options (NQSOs).

In the current study’s assessment, the controversies appear not much to be on the use of stock options by corporations, but on what the mechanism should be such that corporation boards can effectively control managerial self-interest seeking or “rent” seeking behavior. This will “prevent wealth transfer from other shareholders to executives”; moreover that stock options bestow on executives or employees what Mawani termed ‘upside gains’ without any downside risks.

Prior to 2006, the complexity surrounding the use of stock options is somehow exacerbated by the decision of accounting standards not to recognize expensing options granted to employees which Mawani (2003) referred to as “technical valuation issues.” However, some scholars continue to argue in favor of expensing option grants to employees (Bodie et al., 2003). The sustained intellectual arguments surrounding this issue could have prompted the Financial Accounting Standard Board (FASB) to agree to the new expensing regime since 2006, and also the IASB’s intentions to sponsor global debate on the possibility of income-statementalizing stock option grants.[2] Furthermore, Mawani (2003), referring to the literature, documents the widening gap between book-tax conformity[3] in the U.S. such that it has attracted the legislative attention in the U.S. Congress. A bill sponsored by Levin-McCain in February 2002 is an important point of reference. The contention of Congress is that if corporations enjoy tax deductions with respect to option grants to employees, such an amount should be expensed in the financial statement with the consequence of reducing reported profits, thus impacting the stock market valuation of such corporation.[4] This non-conformity of the book-tax conformity is presently less of an issue in Canada.

Mawani (2003) argues that expensing stock options will “restore accounting neutrality” vis-à-vis option grants. Such could also enhance the competitiveness of the stock market as the disappearance of the financial accounting reporting benefits could cause more private placements of shares thus making the stock market more active. This is true since extant literature cannot conclusively find evidence in support of the capability of employees’ stock options to effectively and desirably align seemingly conflicting incentives between the employees and their shareholders.

However, the findings of Austin et al. (1998) call for cautious optimism as to the possibility of corporate reluctance to use option grants if there is tax-book conformity. Austin et al. document that despite the corporate tax disadvantage of ISOs, their sampled corporations use ISOs or a combination of both ISOs and NQSOs predominantly. This, therefore, suggests that CEOs and boards might not be deterred in their decision towards the continued use of stock options. This view is consistent with the conjecture of Austin et al. that “…option choice is made to minimize the executive’s tax burden, without regard for the corporate tax implications.” Therefore, future studies to empirically document whether

stock options actually reduce the effective marginal tax rates will valuably add to the literature as to whether or not stock options are actually a bad idea from the corporate tax point of view.

In what appears as an empirical documentation of Pareto methodology which is widely applied by Thornton (1999), Mawani (2003) investigated the cancellation of executive stock options in Canada vis-à-vis tax and accounting income considerations. He operationalized the trade-off between financial reporting costs and tax

costs in a multilateral framework using insider-trading data. He finds that tax benefits and reported income are taken into account by Canadian public corporations in their decisions of whether or not executive stock options should be cancelled. It is, however, not clear if the capital market will not see such a cancellation as a dis-appointment with its negative valuation impact. The validity of this thinking can be assessed if one considers the positive information value in

[1] For example, while in the U.S. the option benefits of Non-Qualified Options (NQSO) are tax deductible, in Canada, such benefits are not tax deductible.

[2] For further discussion on this, see “International Accounting Board Plans To Treat Options as Costs,” Wall Street Journal Europe’s edition of November 7, 2002. The real outcome and effect of such debates is yet to be measured.

[3] Shackelford and Shevlin (2001) note that “pensions are another form of compensation that has attracted book-tax analysis.” This is further explored in the proceeding section.

[4] While we are not particularly convinced of the value-relevance of this argument, we notwithstanding support it in the interest of fairness, in that all corporations will be assessed on an equal or equivalent level field by the market and not that option granting corporations, while eating their cake in the form of tax deductions, will still have it in the form of otherwise higher reported profits.

the form of expectations of future rise in earnings and thus stock price that the granting of the option had initially signaled to the market.[1] Such a market reaction can be captured by examining the abnormal returns of the stocks of such firms engaged in the cancellation around the cancellation announcement period.

Hitherto, the conceptual methodology gap in the study of stock options is the (near) accurate or approximate measure that could effectively capture the holding period’s behaviors of executives. For example, Austin et al. note that “consistency of our results with the joint tax minimization hypothesis requires that all executives of high tax firms have long holding periods. If there is diversity in executive preferences for holding stock (options), this situation will not hold.” This warning statement simply accentuates the importance for future research to find a proxy that can closely approximate this reality. Further, without a definite conclusion on the tax-efficiency status of the equity-based form of compensation, research in this area remains actively open.

Pension plans-based employees’ compensation

We must mention that there is a scarcity of theoretical and empirical literature relevant to pension plans especially within the domain of taxation. We see few studies on pension plans. We hope that our discussion in this review will fruitfully advance the state of research efforts in this form of deferred employee compensation.

Pensions are generally deferred employees’ compensation, which means that the values are cashable in the future. Therefore, given multi-period tax planning perspectives, one would expect taxation to play a prominent role in both corporate and employees’ attitudes towards the pension plans.[2] It is no wonder that the Internal Revenue Code (IRC) 409A imposes an election and documentation requirement on the firms using deferred compensation packages.

There appears to be less controversial evidence in the literature on pension plans and the role of taxation or its implication for those plans. Many studies, as cited in Thomas (1988), acknowledge the fact that tax arbitrage could be the reason for increasing existence and survival of defined benefit pension plans, hence its growing prominence in the corporate cycle. In fact, Thomas categorically states that the findings of his study “reject the view that pension funding and tax status are unrelated.” However, it is not yet clear in the literature as to the limit of tax arbitrage that corporations can engage in given other moderating and related issues of pension and non-pension shields. Notwithstanding, the reality-gap in Thomas’ finding begs the question as to why do tax-exempt institutions continue to use defined benefit plans? This suggests that there could be a bunch of nontax factors driving organizations’ preference for choice of pension plans. To further underscore the possible significance of nontax factors in the corporate operationalization of pension plans, Thomas (1989)’s study reveals that firms’ termination decision with respect to defined benefit plans could be driven primarily by factors other than taxation excepting in special cases which simply are difficult to empirically identify or justify.

One area that appears controversial with its indirect but potentially considerable effect on the employees and their eventual pension claims is the asset allocation vis-à-vis defined benefit plan and the impact of taxation in this corporate investment choice. Frank (2002) notes and contributes to this inconclusiveness in the literature. The findings of her study provide inconsistent flow to prior empirical work by documenting that “firms’ tax benefits are positively and significantly associated with the percentage of their pension assets invested in bonds.” In other words, tax is important in corporate allocation decision of assets from defined benefit plan to investment opportunities and alternatives.

[1] Alternatively, if granting stock options signaled positive information to the market as documented in the literature, then executives could grant options to take undue advantage of such an announcement to the market with an upfront knowledge of the intentions that the option will be cancelled and redeemed for cash. Therefore, what cash compensation cannot get from the market on its own, granting options and then converting it into cash by cancellation could. Insider trading on the market!

[2] For example, the significance of pension plans and management can be appreciated if one considers its strategic roles and continued mention of pensions in corporate reorganizations. Recent debates in Canada on Air Canada and General Motors in the U.S. regarding reorganization strategies readily come to mind.

CONCLUSION

Depending on the type of compensation package used by a company, the role of taxes remains painfully unclear. The theoretical and empirical research in taxation, accounting and finance on employees’ compensation is commendably intuitive, relevant and thought provoking. However, the commonality in those streams of research suggests inconclusive findings with regards to the role and implication of taxation in corporate choice of employees’ compensation as well as employees’ preference among alternative compensation packages. The discussions above project the fact that considerable research improvement is required to actually bring to the fore the desired commonality and conclusiveness. With cautious optimism, the current study hopes that such an intellectual congruence will occur, except for the fact that there will be continued refinements and improvements of research that will usually breed further dimensions for active need for more research. This can then enlarge the coast for intellectual prospects in this important area of financial accounting and taxation research. It is worthy to mention the possible role of methodologies and proxies for constructs in the empirical studies around the tax relevance of employees’ compensation packages. For example, while some studies have been unfortunately ‘forced’ to calculate corporate effective tax rates using information in the financial statements, others have used the simulated marginal tax rates. There is no doubt that methodological differences could un-intentionally drive research findings. For example, the sample periods may need to be longer than the ones widely used in many of the prior studies as the treatment may lag/lead the effects, that is, the effect of taxation on compensation may take years to manifest. In addition, the research contexts and databases used by many studies in this area of accounting and taxation research could limit the generalizability of findings. Therefore, in addition to highlights above, the current study calls for new and improved creative efforts to broaden the scope of investigations and methodological specifications in the domain of compensation-taxation research. This is particularly important if one considers the unique concerns of (reverse) causality, omitted variables and endogeneity issues that pervade tax-related compensation research.

[1] Alternatively, if granting stock options signaled positive information to the market as documented in the literature, then executives could grant options to take undue advantage of such an announcement to the market with an upfront knowledge of the intentions that the option will be cancelled and redeemed for cash. Therefore, what cash compensation cannot get from the market on its own, granting options and then converting it into cash by cancellation could. Insider trading on the market!

[1] For example, the significance of pension plans and management can be appreciated if one considers its strategic roles and continued mention of pensions in corporate reorganizations. Recent debates in Canada on Air Canada and General Motors in the U.S. regarding reorganization strategies readily come to mind.

CONFLICT OF INTERESTS

The author has not declared any conflict of interest.

REFERENCES

| Akindayomi A (2006). "An Empirical Investigation on the Impact of Executive Stock Options on Firm Valuation". Dissertation, University of Calgary (Alberta, Canada). | ||||

|

Armstrong CS, Blouin JL, Larcker DF (2012). The incentives for tax planning. J Account. Econ. 53(1):391-411. Crossref |

||||

| Austin JR, Gaver JJ, Gaver KM (1998) The choice of incentive stock options vs. nonqualified options: A marginal tax rate perspective". J Am. Tax. Assoc. 20(2):1-21. | ||||

| Bodie ZR, Kaplan S, Merton RC (2003). For the last time: stock options are an expense. Harvard Bus. Rev. 81(3):62-71. | ||||

|

Chan LH, Chen KC, Chen TY, Yu Y (2014). Substitution between Real and Accruals-Based Earnings Management after Voluntary Adoption of Compensation Clawback Provisions. Account. Rev. 90(1):147-174. Crossref |

||||

|

Dechow P, Ge W, Schrand C (2010). Understanding earnings quality: A review of the proxies, their determinants and their consequences. J Account. Econ. 50(2):344-401. Crossref |

||||

|

Desai MA, Dyck A, Zingales L (2007). Theft and taxes. J. Financ. Econ. 84(3):591-623. Crossref |

||||

| Desai M A, Dharmapala D (2008). Tax and corporate governance: An economic approach in tax and corporate governance. Springer Berlin Heidelberg. | ||||

|

Frank MM (2002). The impact of taxes on corporate defined benefit plan asset allocation. J Account. Res. 40(4):1163-90. Crossref |

||||

|

Frydman C, Molloy RS (2011). Does tax policy affect executive compensation? Evidence from postwar tax reforms. J Public Econ. 95(11):1425-1437. Crossref |

||||

|

Graham J (2008). Taxes and corporate finance. In: Eckbo, E. (Ed.), Handbook of Corporate Finance; Empirical Corporate Finance Amsterdam. Elsevier Science. Crossref |

||||

|

Hanlon M, Heitzman S (2010). A review of tax research. J Account. Econ. 50(2):127-178. Crossref |

||||

| Ittner CD, Larcker DF, Rajan MV (1997). The choice of performance measures in annual bonus contracts. Account. Rev. 72(2):231-255. | ||||

| Jensen M (1986). Agency costs of free cash flow, corporate finance and the market for take-overs. Am. Econ. Rev. 76(Papers & Proc.):323-328. | ||||

|

Jensen MC, Meckling WH (1976). Theory of the firm: Managerial behavior, agency costs and ownership structure. J. Financ. Econ. 3(4):305-360. Crossref |

||||

| Johnson CH (2003). Stock and Stock Option Compensation: A Bad Idea. Can. Tax J. 51(3):1259-90. | ||||

|

Ke B (2001). Taxes as a determinant of managerial compensation in privately held insurance companies. The Accounting Review. 76(4):655-74. Crossref |

||||

|

Klassen KJ, Mawani A (2000). The impact of financial and tax reporting incentives on option grants to Canadian CEOs. Contemp. Account. Res. 17(2):227-62. Crossref |

||||

| Matsunaga SR (1995). The effects of financial reporting costs on the use of employee stock options. Account. Rev. 70(1):1-26. | ||||

| Mawani A (2003). Tax Deductibility of Employee Stock Options. Can. Tax J. 51(3):1230-58. | ||||

|

Mawani A (2003). Cancellation of executive stock options: Tax and accounting income considerations. Contemp. Account. Res. 20(3):495-517. Crossref |

||||

|

Philips JD (2003). Corporate tax-planning effectiveness: The role of compensation-based incentives. Account. Rev. 78(3):847-874. Crossref |

||||

| Schmittdiel H (2014). Are CEOs incentivized to avoid Corporate Taxes?-Empirical Evidence on Managerial Bonus Contracts. Tinbergen Institute Discussion Paper. http://papers.ssrn.com/sol3/papers.cfm?abstract_id=2436101. | ||||

| Scholes M, Wolfson A, Erickson M, Maydew E, Shevlin T (1992). Taxes and business strategy: A planning approach. Prentice-Hall. New Jersey. | ||||

|

Shackelford DA, Shelvlin T (2001). Empirical tax research in accounting. J Account. Econ. 31(1):321-387. Crossref |

||||

|

Thomas JK (1988). Corporate taxes and defined benefit pension plans. J Account. Econ. 10(3):199-237. Crossref |

||||

|

Thomas JK (1989). Why do firms terminate their overfunded pension plans? J Account. Econ. 11(4):361-98. Crossref |

||||

| Thornton DB (1999). Managerial tax planning – A Canadian perspectives. Revised Second Edition. | ||||

|

Yermack D (1995). Do corporations award CEO stock options effectively? J. Financ. Econ. 39(2):449-476. Crossref |

||||

Copyright © 2024 Author(s) retain the copyright of this article.

This article is published under the terms of the Creative Commons Attribution License 4.0