ABSTRACT

International Public Sector Accounting Standards (IPSAS) has become one of the popular tools implemented by governments to ensure greater transparency and accountability globally. This research assesses the impact of IPSAS adoption on transparency and accountability in the use of public funds in Liberia. A survey design using five-point Likert scale questionnaire was employed for collecting the data. Questionnaires were administered to accountants, auditors (private and state-owned), government departments and related public sector bodies within the Montserrado County of Liberia. The valid questionnaires were then analysed using descriptive statistics. The hypotheses were formulated and tested by means of analysis of variance (ANOVA) at a 5% significant level with the aid of Microsoft Excel 2013. The study finds that IPSAS adoption increases the level of transparency and accountability in the use of government funds. It further establishes that revenue leakage and inadequate disclosure of public expenditure impedes government commitment to ensure a transparent and accountable management of public funds in the country. Hence, the paper recommends that governments in developing counties should hasten in their transition to the accrual basis IPSAS.

Key words: Accountability, international public sector accounting standards (IPSAS), public funds, transparency, Liberia.

Hardly does a day pass without issues pertaining to massive public sector corruption being cited in the press. This is predominantly the case in developing countries. The West African sub-region in particular, has recorded many cases of reported massive misappropriation of public funds in recent times. Latest instances of reported public sector corruption include: The fraud involving over N40 billion (about US$308 million) pension scam in Nigeria, the Police Pension scandal in Nigeria, and the $1.6 million bullet proof BMW car fraud involving the Nigerian Aviation Ministry (Ademola et al., 2017); the failure of the state to account for a third of 84 billion Leones (about £12 million) set aside to fight the deadly Ebola virus in Sierra Leone (O'Carroll, 2015); and the

loss of GHS347 million Ghana Cedis (about US$77 million) from national Consolidated Fund due to corrupt and treasury mismanagement by government officials in Ghana (Auditor General Report, 2012).

The situation in Liberia before, during, and after the civil war ending 2006 has not been fundamentally different. According to statistics provided by the European Commission (2004), Liberia’s total indebtedness was $2.9 billion as at the end of 2003, approximately half of that was owed to the International Monetary Fund (IMF). Despite this huge accumulated public debt, the report noted that taxes and other revenues accruing to the Government of Liberia were generally believed to be lining the pockets of then President Charles Taylor, the warlord and few persons within his inner circles (Clark, 2008). As a result, the United Nations Security Council placed sanctions on sales of Liberia’s diamonds, timber and as well placed arms embargo together with a travel ban on individuals considered a threat to Liberia’s peace process (United Nations Security Council, 2003). These were the immediate measures instituted to halt corruption and mismanagement then prevalent in the country before the end of the civil war.

Similarly, in President Sirleaf’s inaugural speech after the war, she reckoned massive corruption, mis-management, and misapplication of public funds as the primary canker that had permeated the little nation before and during the war (Sirleaf, 2006). She opined that such fraudulent practices did not only deplete the country’s coffers but also eroded the little faith that members of both local and international community had in the Liberian economy. Given that the Government of Liberia had to continue its extensive reliance on support from external development partners after the fourteen years of civil war to fund the emergency infrastructural needs, it was imperative that President Sirleaf’s government, like many other countries emerging from war exhibited an appreciable level of transparency, stewardship, and accountability in the use of financial resources. This required providing clear and comprehensive financial information regarding the sources and uses of public funds in a form satisfactory to the relevant stakeholders who included Liberia’s taxpayers and development partners. Consequently, the government of Liberia like most other emerging countries around the world resolved to adopt the Accrual Basis International Public Sector Accounting Standard; starting however, initially with Cash Basis IPSAS as a major policy reform to reinforce transparency, stewardship, and accountability in the management of public finances.

This paper seeks to establish that, the adoption of IPSAS does contribute to governments’ effort at ensuring transparency, stewardship, and accountability in the management of public funds in developing. The main objective of this research, therefore, is to assess the impact of IPSAS adoption on transparency and accountability in managing public funds in a developing country such as Liberia. The paper relies on a five-point Likert scale survey questionnaire to obtain data for conducting analysis of variance (ANOVA). Descriptive statistical analyses were carried out with the aid of Microsoft Excel 2013.

Statement of the problem

IPSAS was introduced by the International Federation of Accountants (IFAC, 2012; 2014) through one of its standard setting boards: the International Public Sector Accounting Standard Board (IPSASB) in response to increasing calls for greater transparency and accountability in the management of public funds in the wake of the global financial crises (Ademola et al., 2017; Bello, 2001, IFAC, 2017, Schaik, 2018). Thus, the core motivation for embracing IPSAS by the government of Liberia as part of the financial management reforms was to overturn the existing weakness hampering accountability and transparency in the country.

Similar to many other financial management reforms in developing countries, IPSAS was initiated in Liberia to improve budgeting and expenditure management, augment effective processes that control corruption, improve procurement practices, and enhance accountability in the overall use of government funds. Chan (2006) for example indicated that appropriate application of IPSAS in developing countries plays a leading role in keeping high standards in the use of public funds. He stressed that IPSAS will remain a leading catalyst for the preparation and submission of sound and transparent financial reports to various user groups. This could ultimately enrich operational performance, allocation efficiency, and ensure greater accountability of public funds. Similarly, Ademola et al. (2017) maintained that appropriate application of IPSAS did facilitate good financial management practices in many countries because of its tendency to comprehensively disclose all material transactions and thus highlight financial irregularities that exist within public sector institutions.

The Ministry of Finance and Development Planning plays a pivotal role in upholding a transparent and accountable public financial management system for Liberia. Prior to the end of the civil war in 2006, the government accounting system was characterized by multiple bank accounts scattered across various government ministries, departments, and agencies. Different investigations confirmed that disbursements were made from multiple bank accounts spread across various government ministries, departments, and agencies, and this presented fertile breeding grounds for misapplication and mismanagement of public funds and other corrupt practices (Clark, 2008). To eliminate this corrupt prone environment, where processing of many transactions was initiated and completed without proper authorization from appropriate government of Liberia officials, many important public financial management reforms were introduced. Among the financial management reforms initiated by the government of Liberia include the promulgation of the Public Finance Management Act of 2009, acquisition and installation of the Integrated Financial Management Information System (IFMIS) through a three million and seven hundred thousand American dollars (USD 3.7 million) grant secured from the World Bank on December 12, 2008. To further facilitate a holistic and timely reporting of the government financial transactions and position, the government decided to introduce the Cash Basis IPSAS with the view to achieving the perceived benefits acclaimed by a number of implementing nations.

Consequently, on November 9, 2009, the government through the Ministry of Finance (now the Ministry of Finance and Development Planning) adopted the Cash Basis IPSAS. The Cash Basis IPSAS has since become the prescribed accounting standard for reporting all government of Liberia financial transactions. In announcing the adoption of the Cash Basis IPSAS, then Minister of Finance, the Honorable Augustine Ngafuan, indicated that the government's long-term objective was to migrate into the Accrual Basis IPSAS over a period of five years starting from 2010 (Ngafuan, 2009).

It is worth noting that immediately after the end of the global economic crises, IPSAS recorded a spree of worldwide adoption by many governments and NGOs for varied reasons. Many scholars and practitioners including Han and Hong (2019) and Vokshi (2016) regard the implementation of IPSAS as the panacea for curtailing massive agitations for greater transparency and financial accountability. Whether the implementation of IPSAS contributed to transparency, stewardship, and accountability in the management of public finances in Liberia, is a question yet to be established scientifically. It is this question that motivates this study.

Objectives of the study

The main objective of this study is to assess and ascertain the impact of IPSAS adoption and implementation on transparency and accountability in managing financial resources or public funds by the government of Liberia. The research objective was accomplished by examining the following research question:

“Does the adoption of the Cash Basis International Public Sector Accounting Standard improve greater transparency and accountability in the use of public funds in Liberia?”

Hypotheses of the study

The research was carried out based on the following null and alternative hypotheses:

H01: Adoption of the Cash Basis International Public Sector Accounting standard does not significantly promote greater transparency and accountability in the use of public funds in Liberia.

Ha1: Adoption of the Cash Basis International Public Sector Accounting standard does significantly promote greater transparency and accountability in the use of public funds in Liberia.

Conceptual issues

Conceptual framework of IPSAS

It is imperative that every government works towards establishing trust with its several publics and constituencies. Establishing trust is done through effective information sharing. Governments must present accurate and complete information on their revenue, expenditures and other transactions, as a way of showing greater accountability and stewardship and thereby court trust from its publics and constituents. In other words, governments must present clear and comprehensive information about the financial consequences of their political, economic, and social decisions to all of its stakeholders.

Prior to the introduction of IPSAS, there were no recognized international reporting standards specifically designed to guide reporting on the use of public funds by governments to interested parties (Brown, 2013; Ijeoma and Oghoghomeh, 2014; Nkwagu et al., 2016). IPSASs were therefore developed to address issues which were hitherto either not addressed by existing International Financial Reporting Standards (IFRS) or for which no IFRS had been developed (Achua, 2009 as cited in Ademola et al., 2017). The absence of a recognized credible high-quality international reporting framework for the public sector led to many reported cases of sovereign write-downs and debt defaults. For example, as many as 25 sovereign debt restructurings were reported between 1990 and 2011 (IFAC, 2012, Pricewaterhouse Coopers PwC, 2018). Regrettably, most of these sovereign debt crises were induced by the lack of a transparent and accountable resource governance, ineffective public finance management, and deficient institutional fiscal arrangements and poor public sector financial reporting practices in many countries. The fact that most of these public institutions do not create the needed incentives or restrictions for governments to manage their finances means that the interest of investors and the public at large may not be protected.

Accordingly, the development of the IPSASs by IPSASB signified the conception of practical efforts by the accounting profession to provide accounting tools that represent real progression towards increasing transparency and accountability by governments and related agencies in managing public funds through a high-quality and standardized financial reporting framework. As stated by Ademola et al. (2017), the IPSASB which serves as an independent standard-setting board, with the support of IFAC, issued one Cash Basis IPSAS and several other IPSASs built on the accrual basis of accounting similar to the IFRS. It must be noted that many measures have been instituted in the past by IPSASB to improve public sector financial reporting. One of such initiatives, according to IFAC (2014) was the accrual basis conceptual framework for General Purpose Financial Reporting (GPFR) for public sector entities targeted at improving governments’ stewardship, transparency, and accountability. The conceptual framework similarly has applicability for the cash basis accounting as it does for accrual basis accounting. This conceptual framework requires that government financial statements, whether based on cash accounting or accrual accounting should provide information that is relevant, faithfully representing of transactions purported to be reported, comparable, verifiable, timely and understandable. The conceptual framework also requires that government financial transactions be recognized and measured on sound objective basis in order to be relevant. It is therefore the expectation of IPSASB that all public sector institutions comprising of national governments, regional governments, local governments, and other related government entities (boards, agencies, commissions, and enterprises) apply the specified general purpose financial reports (GPFRs) and recommended practice guidelines (RPGs) to account for sources and uses of public resources. Thus, in the view of IPSASB, using the accrual basis of accounting will serve stakeholders with clear and comprehensive information about the various elements of the public sector financial statements and their financial consequences on economic, social, and political decisions; thereby promoting trust in governments.

IPSASs adoption on transparency and accountability

Rapid developments of global events necessitate that both private and public sector institutions address critical issues relating to transparency and accountability. Indeed, transparency and accountability in the public sector imply government answerability to taxpayers, lenders, donors, and other resource providers who have invested their resources, trust, and confidence to persons assigned to appointed or elected positions. According to IFAC (2012), IPSAS represents a unique institutional arrangement through which governments all over the world can and must rely on to protect the general public and other investors in the use of resources entrusted to them. In view of that, the adoption of IPSAS and the application of the associated guidelines and other resources issued by IPSASB have witnessed a rapid global insurgency since its introduction. IPSAS compliant financial reports are said to provide information that facilitates good governance by ensuring greater transparency and accountability in sourcing and utilizing public funds (Babatunde, 2017; IFAC, 2012). The question then is what is accountability and transparency?

According to Adegite (2010), accountability is the obligation on the part of the assigned officer to demonstrate that a specific duty has been done according to agreed standards and rules and that the reports provided reflect fairly and accurately on actual performance in relation to mandated roles and plans. Rondinelli (2007) on the other hand is of the view that accountability occurs once decision-makers in government, civil society organizations, private sector actors as well as institutional stakeholders are answerable to the public. Ofoegbu (2014) similarly termed accountability as the act of being responsible for one’s decisions or/and actions and providing explanations as and when asked to do. The general assertion is that accountability is made up of three main dimensions: political, financial, and administrative (Cheema, 2007; IFAC, 2012). Among these three dimensions, financial accountability, the focus of this research is defined by Cheema (2007) as an obligation placed on the person(s) handling resources or holding public position or any other position of trust, to report on the actual or intended use of the assigned resources. Accountability is high on the agenda in the corporate business world and managers of resources have a well-established idea as to what to account for and whom they are accountable to. Inevitably, in the public sector where government officials are the custodians of the taxpayers’ money, the need for accountability not only has to be even on a higher pedigree but also need to be much more rigorous. Public sector financial accountability is thus expected to be more transparent in the eyes of the general public to satisfy a necessary but not sufficient condition of good governance. Accountability is closely related to transparency.

Murphy and Sagar (2009) explain that financial transparency manifests in four ways: reporting entities accurately and fully disclosing all transactions including disclosures of stakeholders who have beneficial ownership in the entities, the management and shareholding structure of the entities; reporting entities and the substance of their transactions in accordance with internationally recognised accounting standards; regulatory authorities having access to every and all information that they may require from the published financial statements; and there being no exceptions to the above three except in cases of national security. Lowenstein (1996) asserts that transparency manifests itself through insistence of open hearings of government transactions throughout the entire structures of government, opening up for public scrutiny and not covering up transactions under the guise of confidentiality, requiring all public officers file returns of all their business dealings. He maintains that transparency is essential because, citizens have a right to know, comprehensively, the way their resources are being managed. McCarthy (2007) maintains that transparency is rooted in a visible commitment to be held accountable. The implication of the above arguments is that transparency requires participation by the citizenry or their elected representatives in the financial management process and accountability is submission to the citizens by managers of public funds, the two are thus closely linked and inseparable. Accountability and transparency are therefore twin concepts which are fundamentally a key part of good governance.

Given the extensive and rigorous need for government accountability, Rizvi (2007) suggests that public sector accountability is spread through different layers of players including parliament, ministries, departments, and agencies. Responsibility for financial management has to be distributed among these stakeholders as a way of division of labour and checks and balance mechanism. Rizvi (2007) noted that such segregation of duties will lend more credence to the transparent use of public funds. The use of both cash basis and accrual basis IPSAS enhances accountability and transparency. Ofoegbu (2014), however, believes that the use of accrual basis of accounting in the public sector as a framework for reporting is best suited to serve the information needs of its user, concluding that governments implementing accrual basis IPSASs stand a better chance to achieve increased transparency and accountability expected of a good governance system compared to their counterparts reporting on the cash basis accrual system.

The free flow of financial information has thus become the cornerstone of transparent governance systems. To improve transparency, Rondinelli (2007) insisted that all government processes, institutions, and information must be directly accessible to persons connected to them and that there should be enough information on these processes and institutions to aid understanding and monitoring. In this regard, IFAC (2012) proposed that reporting entities should submit high-quality public sector financial statements to intended users timely. The report explained further that as systems develop, governments must strive to make information publicly available preferably on monthly basis. This implies that IPSAS as a transparent system must be capable of promoting openness through a comprehensive reporting. IPSAS is thus perceived as the principal public sector accounting tool employed by most governments to gather, record, classify and summarize fiscal and financial activities of government transactions into information for use by interested stakeholders (Chinedu et al., 2016).

There is also a suggestion that the public interest is best served when government financial statements are presented in a format that is understandable, reliable, and comparable to financial statements prepared by other public sector entities elsewhere. This clearly, is only feasible if an internationally recognised reporting framework like IPSAS is used as basis for financial reporting by all governments (IFAC, 2014; Legenkova, 2016; Mack and Ryan, 2006). IPSAS based reports encourage adequate disclosure of the financial position and performance of governments in comparison with respective budgets. Such budget comparison information helps to determine compliance with parliamentary approval limits and arms Parliamentarians as critical users of public sector financial statements with a base for assessing the extent to which authorisation limits have been breached by government officials.

Additionally, IPSAS based reports provide clear information to citizens regarding the extent to which government officials comply with the appropriations authorised by their elected representatives. This means that stakeholders including citizens are encouraged to actively participate in ensuring accountable governance through questioning non-compliance behaviours of government officials. Cheema (2007) claimed that the more informed the citizens are, the more likely they will be willing to contribute meaningfully during dialogue with the government and with each other; which could enhance economic growth and development.

Another point is that IPSAS based reporting serves as an effective instrument for promoting transparent governance systems, facilitating the combat of fraudulent and corrupt practices that have permeated the public sector in many countries. Chen (2012) found that the number of reported cases of institutional fraud and irregularities including falsification of financial transactions, leakage of government revenues, assets embezzlement, and other irregular transactions have significantly dropped in countries that have adopted IPSAS compared to those countries yet to do. Given the level of financial discipline that have been associated with countries that have adopted IPSAS as part of transparent and accountable governance, Babatunde (2017) and Transparency International (2016) in their respective studies called on developing countries to embrace IPSAS in order to accelerate their respective levels of economic growth and development through increased financial discipline.

It is worth noting that accrual based IPSASs have become the centre of attention for most countries that intend to adopt IPSAS. It has long been established that many countries prefer Accrual Basis IPSASs to the Cash Basis IPSAS because of its ability to improve transparency and accountability of many public sector institutions across the world (Aliyu and Balaraba, 2015). The World Health Organization’s migration from the Cash Basis IPSAS reporting to the Accrual Basis IPSASs is attributable to the latter’s ability to: show a comprehensive reporting of assets and liabilities, display a snapshot of comparison between financial periods as well as providing adequate representation of the entity’s overall financial position (World Health Organization, 2013).

Also, the conceptual framework developed and approved by IPSASB in 2014 for preparing General Purpose Financial Statements (GPFS) by public sector entities encourages the disclosure of individual items within an element as well as aggregations of items in order to enhance the ability of the public sector financial statements. According to IFAC (2014), accrual-based reporting requirements not only calls for adequate disclosure of revenue and expenses but also imposes an obligation to disclose all material national assets and liabilities. Such disclosure has a significant influence on future decisions of creditors, lenders, donors and other providers of resources to have the motivation to commit more resources to support current and future activities of government and related entities. Such adequate disclosure required by accrual basis of reporting further reinforces the relationship between government institutions and other stakeholders including taxpayers, creditors, suppliers, taxpayers, public sector employees as well as the media. Although the Accrual Basis IPSASs are superior and therefore preferable, a number of PFM scholars have counselled that countries with less developed accounting systems may start with the Cash Basis IPSAS as a stepping stone towards migration to full Accrual Basis IPSAS (Bergmann, 2011; Chan, 2006; van Der Hoek, 2005). It is in this regard that the Government of Liberia started with the adoption of the Cash Basis IPSAS in 2009 with the plan to migrate to full Accrual Basis IPSAS by 2015.

Reforms towards achieving transparency and accountability in Liberia

A very active and favourable environment must exist for the effective implementation of IPSAS. Prior to IPSAS adoption by the government of Liberia, there were legislative provisions that sought to protect the public purse. General Auditing Commission (GAC) Act 2005 is one of such important enactments which empower the Auditor General to provide his opinion on government financial statements and the transactions they report on, and in certain circumstances probe the financial transactions of government as the GAC deems necessary. In order to execute its mandate as a pillar of transparency, accountability, and fiscal probity within the public sector, section 53 of the GAC Act empowers the Auditor General to audit the public accounts of the Republic of Liberia and of all other public offices. In addition, Section 37 sub-section 2 of the Public Finance Management (PFM) Act, 2009 mandates the Minister of Finance to submit unaudited final accounts in accordance with the content and classifications of the national budget to the Auditor General not later than four (4) months following the end of the fiscal year to which the statements relate for audit. Furthermore, section 37 sub-section 5 of the PFM Act, 2009, obliges the Auditor General to review the final accounts of the national budget produced by the Minister of Finance and Development Planning and submit his report, along with the audited final accounts, including responses and clarifications provided by the Minister of Finance and Development Planning (if any) on the observations and comments raised by the Auditor General, to the national Legislature not later than four (4) months after receipt of the unaudited final accounts from the Minister. These existing legislative provisions enable user groups to compare financial outcomes with the budget, and thus aid proper assessment of the extent to which the government is living up to its financial obligations. These provisions also clearly establish the need for accountability by government officials and the basis for transparency in managing public funds as audit by the Auditor General is constitutionally mandatory.

In practice, to expedite efficient financial oversight over the financial activities of the government, the Liberia Senate and House of Representatives have created a Joint Public Accounts Committee (JPAC). It functions as a Committee of the national Legislature of the country. The JPAC is mandated to review audit reports submitted by the General Auditing Commission (GAC), conducts investigations on the application of public funds, and investigate any irregularities and other issues raised by the GAC. The JPAC is further tasked with developing recommendations on government financial administration, ex-post scrutiny of the budget execution process, all with a view to ensuring transparency, accountability and value for money within the public sector. It is therefore expected that effective implementation of IPSAS should help generate the appropriate financial reports that will facilitate the work of both the GAC and the JPAC. The next section, discusses the theoretical framework upon which this study is rooted.

Theoretical framework

The collective resources citizens in organized democracies are generally usually entrusted to the governments to administer on behalf of the citizens. In order for governments to effectively manage the resources entrusted to their care, they are not only granted legal access to those resources but also the command over their use for the benefit of the public. Hence, the need for accountable governance by governments arising from the right to command how state resources are deployed. This study is therefore anchored on two main theories: the governance theory and commander theory. The word governance has been defined differently by different authors. According to Ruggie (2014), governance refers to the systems of authoritative rules, norms, institutions, and practices through which nations manage their affairs either locally or globally. It should be noted that the term governance represents an indubitable vocabulary in advanced countries including Britain and the United States of America. However, in developing countries, governance is more of a policy reform forced through the throats of many regimes by bilateral and multilateral institutions with the view to committing them to an efficient and accountable government (Stoker, 1998).

As such, Stoker (1998) sees governance as an autonomous self-governing of a network of actors which are required to identify the blurring boundaries and responsibilities essential to tackling economic and social issues. In other words, governments must pursue policies that guarantee sensible and effective use of state resources. Chhotray and Stoker (2009) stated that “governance is about the rules of collective decision-making in settings where there is a plurality of actors or organizations and where no formal control system can dictate the terms of the relationship between these actors and organizations” (p. 3). They posit that governance theory relates to collective decision making processes and deals with how the multi-dimensional construct of governance brings about development by facilitating delegation of state authority to some elected or appointed individuals to make choices on behalf of those they represent, responsibly deploy the collective resources of the state for the benefit of citizens in a transparent manner and account to the citizens by explaining how resources were obtained and used. Hupe and Hill (2007) in their paper titled street level bureaucracy and public accountability affirm the main tenet of governance theory as being at the foundation of explaining how bureaucrats at the different multiple layers of the governance structures are held to account to their superiors for responsibilities delegated in democratic societies. The clearest application of governance theory to financial accountability is the World Bank’s restricted economic view of good governance as holding government officials accountable for use of resources; clear structure of rules that provide clarity and predictability of engagements between government and citizens; governments making available information about economic conditions, budgets and transparency in use of public resources through citizens’ participation in governance processes and reduced corruption (Kaufmann et al., 1999; Leftwich, 1994; World Bank, 1992, 1994).

These assertions converge with the views by several other governance scholars that governance theory requires governments to clearly exhibit accountability and transparency over the use of public funds (Baland et al., 2010; Hill and Hupe, 2014; Hupe and Hill, 2007; Kooiman, 1993; Michael and Hill, 2002; Nanda, 2006). Hood (1991) thus laid emphasis on the need for governments to make sensible and effective use of scarce resources beyond the direct provision of services. This means that persons entrusted with resources by the governed must make active and sensible deployment of these funds and render accurate accounts to the citizens regarding how resources have been so deployed. It is, therefore, necessary that the government as the trustee of state resources is vested with the needed power to direct how these resources are utilized, hence the commander theory. The present study therefore finds strong scholarly roots in the governance literature. The commander theory is also relevant for the study.

The commander theory propounded by Louis Goldberg in 1965 titled “Inquiry into the Nature of Accounting” in Australia represents a fundamental strategic platform for financial statement disclosure activities. It represents a theoretical foundation and basis whereupon analyses of the possible outcomes of cross-sector transfer of accounting principles as well as rules to the public sector are grounded. According to Goldberg (1965), the commander theory assumes that owner(s) of resources may well be the controllers or directors of those resources, however, in some cases, a separation between ownership and control is essential and must prevail. This theory, similar to principal and agent relationship (Jensen and Meckling, 1976), focuses on situations where separation exists between the control and ownership of resources. In such instances, command remains with the controller who must direct the affairs of the institution given the power and authority bestowed on the individual while the owner(s) in return, will demand reports and accountability from the controller.

The Commander theory used in the context of government regards top public office holders including ministers, permanent secretaries, and special advisers as commanders. These persons are seen as individuals occupying the top level in a hierarchy of command and ought to be accountable to the state for every resource entrusted to their control through periodic financial statements. Similarly, departmental heads and directors who discharge their duties upon the directives of ministers in their respective departments must also be accountable to the relevant authorities, for the resources at their disposal. As such governments, must conduct due diligence as trustees of national resources and also make available to all stakeholders comprehensive financial statements, at periodic intervals, to permit informed judgments by users. The commander theory has thus become essentially relevant, given that IPSASs advocate for full disclosure of every material financial information to enable stakeholders to make informed judgments. Full compliance with the commander theory requires full disclosure of public sector financial transactions, thus paving way for the production of credible and comparable government financial reports which will result in transparent and accountable governance.

This study employed the purposive sample selection technique to pick the respondents for the investigation. The respondents are made up of auditors and accountants from the General Auditing Commission (state-owned), private audit firms, and the accounting departments of selected government ministries within the Montserrado County in Liberia. The population represents not less than 99% of persons (practitioners) in Liberia with the requisite training and practical experience on what IPSAS seeks to achieve. The sampling technique adopted is quite similar to the mode of selection of participants for assessing the rationale, benefits and challenges on International Financial Reporting Standards (IFRS) Adoption in Ghana by Boateng et al. (2014). This sample selection technique guaranteed that persons with the requisite experience and insights into IPSAS application were selected for the conduct of the study.

Montserrado County, the main focus of the study is located north-western of the West African country of Liberia. The researchers selected Montserrado County because it represents the largest market in the entire Liberia economy (Market Review Liberia, 2007). Most significantly, the General Auditing Commission, all the public accounting and audit firms as well as ministries selected for the examination have their head offices and core staffs based in this county. Moreover, staff personnel with requisite knowledge of the relevant provisions and operations of IPSAS are all in the offices headquartered in this County.

Accountants, internal and external auditors represent the elements of the population under study. A questionnaire instrument outlining a five-point Likert scale was adopted. Responses to the questions ranged from strongly agree, agree, unsure, disagree, to strongly disagree. The paper adopted the research instrument used by earlier researchers (Ijeoma and Oghoghomeh, 2014; Yin, 2003). The content of the research instrument formulated by the researchers was validated by a renowned international IPSAS consultant who is also a Senior Lecturer and holds a Ph.D. qualification in accounting. These procedures were initiated to ensure that the five-point Likert scale instrument measures the variables it envisioned to investigate.

The five-point Likert scale questionnaire consisted of three primary segments. Section one contained the demographic data of the research participants. Besides, closed-ended questions were created in the second section of the questionnaire to enable the researchers to gather the relevant data from the respondents on how IPSAS implementation influence transparency and accountability of the public sector financial management system in Liberia. In addition, open-ended questions were drawn in the third segments to allow participants that are expert-practitioners in their respective fields to provide any additional comments. The aim is to allow the experts list how or what can be done to ensure that IPSAS contributes significantly to the attainment of the agenda on transparency and accountability in public financial management systems.

To achieve this goal, one hundred participants were drawn from a population size of hundred and fifty by means of the Taro Yamane sample size determination technique at 95% confidence level (Yamane, 1967). The reliability test was conducted by means of Cronbach's alpha test. A Cronbach's alpha of 0.76 was registered (considered higher than the conventional standard of 0.70). According to Hejase and Hejase (2013: 570), “the generally agreed upon lower limit for Cronbach’s alpha is 0.70, although it may decrease to 0.60 in exploratory research.” As a result, the findings of the investigation conducted were deemed to be reliable.

The ensuing section provides an analysis of responses through descriptive statistics and analysis of variance (One-Way ANOVA).

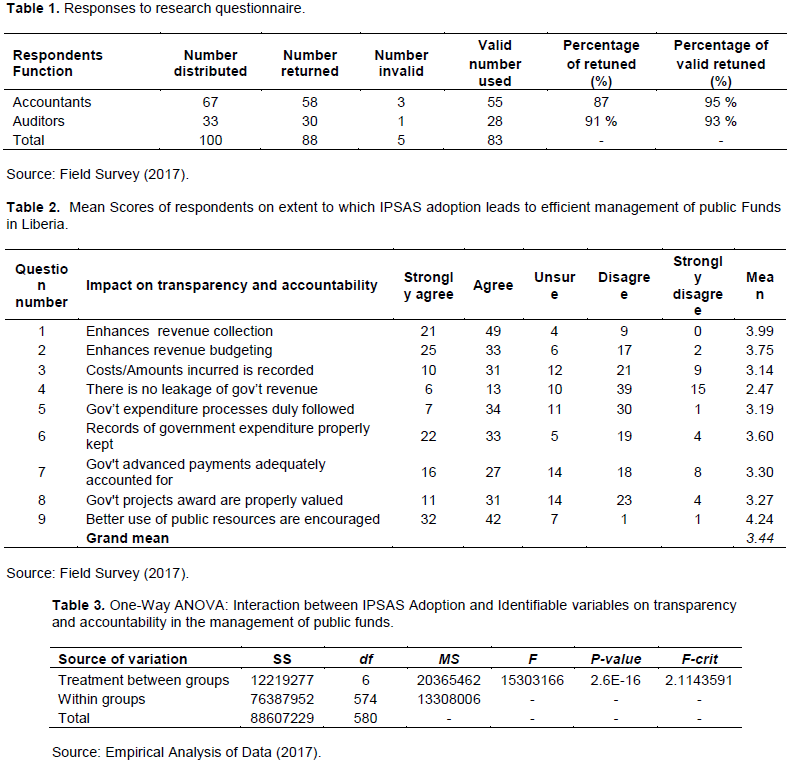

The data produced from the research questionnaire were analysed by means of descriptive statistics depicted in Tables 1 to 3. Table 1, for example, display the breakdown of responses assembled from the respondents. It can be observed from Table 1 that out of the 100 questionnaires distributed, only 88 were returned. Whilst, 12 of the administered questionnaires representing 12% could not be retrieved. The breakdown of the returned questionnaire comprises 58 from accountants and 30 from auditors representing 87 and 91%, respectively of the total number administered. Only 95 and 93% of the retrieved questionnaires from the accountants and auditors respectively were deemed valid and were accordingly used for the analysis. However, the overall response rate is 83%. Five of the returned questionnaires representing 6% were incomplete and categorized as invalid and were therefore excluded from the final analyses. Table 2 depicts the mean scores of respondents on the extent to which IPSAS adoption has resulted in efficient management of public funds in Liberia.

The results presented in Table 2 indicate that the respondents agree with items 1, 2, 6, and 9 with respective mean scores of 3.99, 3.75, 3.60, and 4.24. The respondents, however, disagree with item 4 with a mean score of 2.47. Also, respondents were unsure about items 3, 5, 7, 8 with mean scores of 3.14, 3.19, 3.30, and 3.27, respectively. Hence, the general consensus by these practitioners is that IPSAS implementation has not only deepened the enthusiasm of government to budget for the amounts of revenue it anticipates to generate yearly, but also encourages Liberia Revenue Authority to collect budgeted amounts from targeted sources. Given proper projections of government’s yearly cash expectation, with the introduction of IPSAS, the expectation is that national priorities could effectively be aligned with these scarce resources.

Consequently, this results in fiscal discipline as the government spends what it can generate. This line of argument is confirmed by the responses to question 9 in Table 2, that IPSAS implementation has had a positive influence on accountability and transparency through better deployment of economic resources. Similarly, the experts’ general response to question 6 reveals that proper record keeping on government expenditure is enhanced through IPSAS implementation.

However, the respondents strongly believe that more effort is still required to completely eliminate the leakage of government revenue in the country. The result from the survey also indicates that IPSAS implementation is yet to guarantee the determination of exact amounts of expenditure incurred by the government each year. The respondents could neither confirm nor dispel the assertion that due processes instituted by the government of Liberia regarding expenditure are fully followed, following IPSAS adoption. This means that additional internal control procedures must be introduced to ensure that every expenditure item is fully reported. Finally, the respondents were not too certain as to the impact of IPSAS implementation on proper accountability of government advances and accurate valuation of government projects awarded to constructors and consultants.

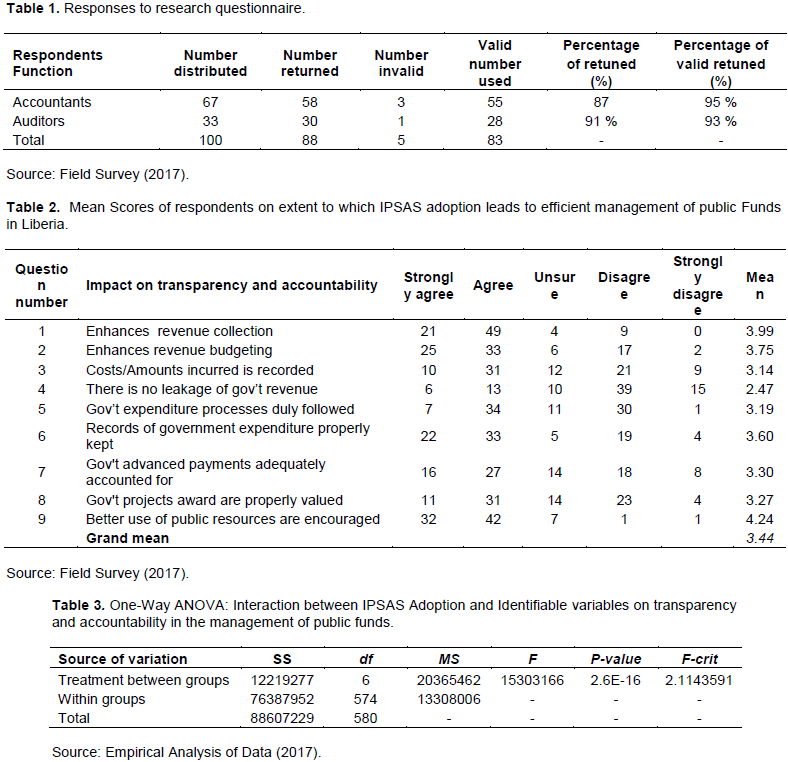

In answering the research question, “Does the adoption of the Cash Basis International Public Sector Accounting Standard ensure greater transparency and accountability of public funds in Liberia?” The research question was tested using the following hypothesis through One-Way ANOVA:

H0: µ1=µ2....=µk

HA: µ1≠µ2…=µk

H01: Adoption of the Cash Basis International Public Sector Accounting Standard does not significantly improve greater transparency and accountability of public funds in Liberia.

Ha1: Adoption of the Cash Basis International Public Sector Accounting Standard does significantly improve greater transparency and accountability of public funds in Liberia.

At the significance Level (α): 0.05, the research results produced through ANOVA are presented in Table 3. The results from Table 3 show that p < 0.0001. Given that the p-value is less than the significance level of 0.05, we have sufficient evidence to reject the null hypothesis as the p-value falls within the rejection region. Besides, the F-ratio of 15.3032 with 6 degrees of freedom is larger than the critical F-value of 2.1144; hence we conclude that the result is statistically significant at 0.05 level of probability. Given that the test statistic is greater than the tabled (critical) value, the null hypothesis is rejected. Therefore, the F statistics result has effectively endorsed the finding obtained using the p-value. Accordingly, the alternate hypothesis which states that the adoption of the Cash Basis International Public Sector Accounting Standard does significantly improve greater transparency and accountability of public funds in Liberia was accepted. In brief, the result endorses the findings of Transparency International (2016) that IPSAS adoption and implementation has a significant positive influence on government accountability and transparency.

The paper further tries to solicit the views of the respondents (experts) on practical measures that could accelerate the attainment of the desired level of transparency and accountability in management of public funds using open ended questionnaire. According to the respondents, the government of Liberia ought to hasten the adoption of Accrual Basis IPSAS (the government long term objective). As experts, their general belief is that this move will deepen full disclosure of sources and uses of government resources; expected by relevant stakeholders. This suggestion supports the recommendation by IFAC (2014) that nations must make extra effort to implement the accrual basis of IPSAS so as to improve government stewardship, transparency, and accountability. The respondents are also of the view that the production of accrual basis IPSAS compliant reports by ministries, departments, and agencies should be made mandatory and that any subsequent allotments to public sector entities must be contingent upon obtaining a clean audit report on previous allotments.

Majority of the respondents also called for a timely audit of the financial transactions of government ministries, departments, and agencies to ensure well-timed detection of any existing fraud and corruption. In the same manner, it was recommended that any suspected case of fraud must be investigated in a timely manner and that offender of the financial rules and regulations must be prosecuted without fear or favour. Some also demanded the passage of a whistle-blowers Act along with adequate protection granted to whistle-blowers.

Besides, it was suggested that the autonomous reform institutions established to fight corruption in the country including the General Auditing Commission, Liberia Anti-Corruption Commission, and Internal Audit Agency should not only be independent on paper, but in practice also. This important recommendation could be realised if the security of tenure and remuneration package of the key staff of these institutions among other factors are guaranteed.

CONCLUSION AND RECOMMENDATIONS

This study evaluated the impact of the adoption of the Cash Basis IPSAS on transparency and accountability in managing public funds in Liberia. This research expanded the current literature on the impact of IPSAS adoption on public sector transparency and accountability regarding the use of public funds, especially in developing countries such as Liberia. In addition, the methodology employed to obtain the empirical evidence is scholarly and could be used by other researchers in future assignments. The study revealed that IPSAS adoption increases the level of transparency and accountability in the use of government funds. Yet, the research established that revenue leakage and inadequate reporting of government expenditure were impediment to ensuring a transparent and accountable management of public funds in the country. Therefore, based on the hypothesis, the paper concludes that IPSAS implementation do significantly improve greater transparency and accountability in the use of public funds in Liberia. This is expected to strengthen the relationship between the government and the governed. Based on the research conclusions, the following policy recommendations are regarded very useful for policymakers:

(i) A monitoring and evaluation team consisting of committed experts be set up to ensure that intended outcome for all reforms, particularly, PFM reforms are achieved.

(ii) Governments must consider enacting relevant legislations that seek to protect and allow whistle-blowers and these laws must be backed by appropriate sanctions to ensure full compliance.

(iii) Investigative institutions including the GAC, the Liberia Anti-Corruption Commission (LACC), and Internal Audit Agency must be well resourced to conduct timely inquiries when the need arises. In addition, the personnel of these institutions must be guaranteed security of tenure and attractive remuneration packages to keep them motivated.

(iv) Governments should institute plans for smooth and quick migration to full accrual-based IPSAS so as to maximize the perceived benefits associated with accrual basis IPSAS.

The authors have not declared any conflict of interests.

REFERENCES

|

Achua JK (2009). Reinventing governmental accounting for accountability assurance in Nigeria. Nigerian Research Journal of Accounting 1(1):1-16.

|

|

|

|

Adegite EO (2010). Accounting, accountability and national development. Nigerian Accounting 43(1):56-64.

|

|

|

|

|

Ademola OA, Adegoke AK, Oyeleye AO (2017). Impact of international public sector accounting standards (IPSAS) adoption on financial accountability in selected local governments of Oyo State, Nigeria. Asian Journal of Economics Business and Accounting 3(2):1-9.

Crossref

|

|

|

|

|

Aliyu A, Balaraba A (2015). IPSASs and financial and financial reporting in Nigeria: Answer to implementation questions. Journal of Economics and Finance 6(6):28-32.

|

|

|

|

|

Auditor General Report (2012). Report of the Auditor-General on the

|

|

|

|

|

Auditor General Report (2012). Report of the Auditor-General on the Public Accounts of Ghana (Consolidated Fund) for the year ended 31 December 2012. Accra: Ghana Audit Service. Available at:

View.

|

|

|

|

|

Babatunde SA (2017). Implementing international public sector accounting standards in Nigeria: issues and challenges. International Journal of Business Economics and Law 12(1):52-61.

|

|

|

|

|

Baland JM, Moene KO, Robinson JA (2010). Governance and development. Handbook of Development Economics 5:4597-4656.

Crossref

|

|

|

|

|

Bello S (2001). Fraud prevention and control in Nigerian public service: The need for a dimensional approach. Journal of Business Administration 1(2):118-133.

|

|

|

|

|

Bergmann A (2011). Improving public sector financial management through the use of IPSAS'. Available at:

View

|

|

|

|

|

Boateng AA, Arhin AB, Aful V (2014). International Financial Reporting Standard's (IFRS) adoption in Ghana: Rationale, benefits and challenges. Journal of Advocacy Research and Education 1(1):27-32.

Crossref

|

|

|

|

|

Brown P (2013). Some observations on research on the benefits of nations adopting IFRS. The Japanese Accounting Review 3:1-19.

Crossref

|

|

|

|

|

Chan JL (2006). IPSAS and government accounting reform in developing countries. Accounting reforms in the public sector: Mimicry, fiduciary or necessity. pp. 31-42.

|

|

|

|

|

Cheema GS (2007). Linking Governments and Citizens through Democratic Governance. Public Administration and Democratic Governance: Governments Serving Citizens. 7th Global Forum on Reinventing Government. 26-29 June, Vienna, Austria. UN Publication No.: ST/ESA/PAD/SER.E/

|

|

|

|

|

Chen MC (2012). The Influence of workplace spirituality on motivations for earnings management: A Study in Taiwan's hospitality industry. Journal of Hospitality Management and Tourism 3(1):1-11.

Crossref

|

|

|

|

|

Chinedu NL, Okoye GO, Nkwagu CC (2016). International public sector accounting standards adoption and financial transparency in the Nigerian South Eastern states public sector: A case of Ebonyi and Enugu states. IOSR Journal of Humanities and Social Science 21(4):40-51.

|

|

|

|

|

Chhotray V, Stoker G (2009). Governance: From Theory to Practice. In Governance Theory and Practice. Palgrave Macmillan, London. pp. 214-247.

Crossref

|

|

|

|

|

Clark MA (2008). Combating corruption in Liberia: assessing the impact of the governance and economic management assistance program (GEMAP). Journal of Development Social Transformation 5:25-32.

|

|

|

|

|

European Commission (2004). Liberia: Country Strategy Paper and National Indicative Program 2004-2007. Available at:

View

|

|

|

|

|

Goldberg L (1965). An Inquiry into the Nature of Accounting. American Accounting Association. Available at:

View

|

|

|

|

|

Han Y, Hong S (2019). The Impact of Accountability on Organizational Performance in the U.S. Federal Government: The Moderating Role of Autonomy. Review of Public Personnel Administration 39(1):3-23.

Crossref

|

|

|

|

|

Hejase A, Hejase HJ (2013). Research Methods: A Practical Approach for Business Students (2nd edition). Philadelphia, PA, USA: Masadir Inc.

|

|

|

|

|

Hill MJ, Hupe PL (2014). Implementing Public Policy: An Introduction to the Study of Operational Governance, 3rd ed. London, UK: Sage.

|

|

|

|

|

Hood C (1991). A public management for all seasons. Public Administration 69:3-19.

Crossref

|

|

|

|

|

Hupe PL, Hill MJ (2007). Streetâ€Level bureaucracy and public accountability. Public Administration 85(2):279-299.

Crossref

|

|

|

|

|

Ijeoma NB, Oghoghomeh GN (2014). Adoption of IPSAS in Nigeria: expectations, benefits and challenges, problems. Journal of Investment and Management 3(1):21-29.

Crossref

|

|

|

|

|

International Federation of Accountants (IFAC) (2012). Public sector financial management transparency and accountability: The use of international public sector accounting standards. IFAC Policy Position 4:1-6. Available at:

View

|

|

|

|

|

International Federation of Accountants (IFAC) (2014). The Conceptual Framework for General Purpose Financial Reporting by Public Sector Entities. Available at: View

|

|

|

|

|

International Federation of Accountants (IFAC) (2017). Accrual Practices and Reform Expectations in the Caribbean. Public Sector Financial Accountability Survey Findings.

|

|

|

|

|

Jensen MC, Meckling WH (1976). Theory of the firm: Managerial behavior, agency costs and ownership structure. Journal of Financial Economics 3(4):305-360.

Crossref

|

|

|

|

|

Kaufmann D, Kraay A, Zoido-Lobaton P (1999). Governance matters (World Bank Policy Research Working Paper No. 2196). Washington, DC: World Bank.

|

|

|

|

|

Kooiman J (1993). Modern Governance: New Government Society Interactions, ed. Jan Kooiman: London: Sage pp. 249-262.

|

|

|

|

|

Leftwich A (1994). Governance, the State and the politics of development. Development and Change 25(2):363-386.

Crossref

|

|

|

|

|

Legenkova M (2016). International public sector accounting standards implementation in the Russian Federation. International Journal of Economics and Financial Issues 6(4):1304-1309.

|

|

|

|

|

Lowenstein L (1996). Financial transparency and corporate governance: you manage what you measure. Columbia Law Review 96(5):1335-1362.

Crossref

|

|

|

|

|

Mack J, Ryan C (2006). Reflections on the theoretical underpinnings of the general- purpose financial reports of Australian government departments. Accounting, Auditing and Accounting Journal 19(4):592-612.

Crossref

|

|

|

|

|

Market Review Liberia (2007). The Republic of Liberia. July Edition. Available at:

View

|

|

|

|

|

McCarthy J (2007). The ingredients of financial transparency. Nonprofit and Voluntary Sector Quarterly 36(1):156-164.

Crossref

|

|

|

|

|

Michael J, Hill A (2002). Implementing Public Policy: Governance in Theory and Practice. London: Sage.

|

|

|

|

|

Murphy R, Sagar P (2009). What is financial transparency? Mapping the Faultlines series, tax justice network. Available at:

View

|

|

|

|

|

Nanda VP (2006). The "good governance" concept revisited. The annals of the American. Academy of Political and Social Science 603(1):269-283.

Crossref

|

|

|

|

|

Ngafuan AK (2009). International Public Sector Accounting Standards. Available at:

View

|

|

|

|

|

Nkwagu LC, Uguru LC, Nkwede FE (2016). Implications of International Public Sector Accounting Standards on financial accountability in the Nigerian Public Sector: A Study of South Eastern States. IOSR Journal of Business and Management 18(7):105-118.

|

|

|

|

|

O'Carroll L (2015). A third of Sierra Leone's Ebola budget unaccounted for, says report. The Guardian. February 15, 2015. Available at:

View

|

|

|

|

|

Ofoegbu GN (2014). New public management and accrual accounting basis for transparency and accountability in the Nigerian public sector. IOSR Journal of Business and Management 16(7):104-113.

Crossref

|

|

|

|

|

PricewaterhouseCoopers (PwC) (2018). IPSAS: An enabler for better public financial management. Available at:

View

|

|

|

|

|

Rizvi G (2007). Reinventing Government: Putting Democracy and Social Justice Back into the Discourse. Public Administration and Democratic Governance: Governments Serving Citizens. 7th Global Forum on Reinventing Government. 26-29 June 2007, Vienna, Austria. Available at:

View

|

|

|

|

|

Rondinelli DA (2007). Governments Serving People: The Changing Roles of Public Administration in Democratic Governance. Public Administration and Democratic Governance: Governments Serving Citizens. 7th Global Forum on Reinventing Government. 26-29 June, Vienna, Austria. UN Publication No.: ST/ESA/PAD/SER.E/.

|

|

|

|

|

Ruggie JG (2014). Global governance and new governance theory: Lessons from business and human rights. Global Governance 20:5-17.

Crossref

|

|

|

|

|

Schaik FV (2018). IPSAS in your pocket (2018 Edition): Deloitte: Rotterdam.

|

|

|

|

|

Sirleaf E (2006). Inaugural address of H.E. Ellen Johnson Sirleaf. Available at:

View

|

|

|

|

|

Stoker G (1998). Governance as theory: Five propositions. International Social Science Journal 50(155):17-28.

Crossref

|

|

|

|

|

Transparency International (2016). Corruption Perception Index 2016. Available at:

View

|

|

|

|

|

United Nations Security Council (2003). Security Council Committee Established Pursuant to Resolution 1521(2003) Concerning Liberia. Available at: View

|

|

|

|

|

van der Hoek MP (2005). From cash to accrual budgeting and accounting in the public sector: The Dutch experience. Public Budgeting and Finance 25(1):32-45.

Crossref

|

|

|

|

|

Vokshi B (2016). Transparency in management of public funds. International Journal of Economics, Commerce and Management 4(1):533-559.

|

|

|

|

|

World Bank (1992). Governance and Development (Washington DC: World Bank). Available at:

View

|

|

|

|

|

World Bank (1994). Governance: The World Bank's Experience (Washington DC: World Bank). Available at:

View

|

|

|

|

|

World Health Organization (WHO) (2013). IPSAS benefit to WHO. WHO Document Production Services, Geneva: Switzerland? Available at:

View

|

|

|

|

|

Yamane T (1967). Statistics: An Introductory Analysis. 2nd Ed., New York: Harper and Row.

|

|

|

|

|

Yin RK (2003). Case Study Research: Design and Methods (3rd Ed.). Thousand Oaks, CA: Sage.

|

|