Full Length Research Paper

ABSTRACT

The study examines the effect of two instructional design formats on performance scores in introductory accounting when learning the accounting equation. The conventional split-source instructional design and the integrated instructional design were used in an experiment administered to two groups of students. Sixty-four students enrolled in introductory accounting participated in the study. Results of performance scores in recall and transfer test items suggests that instructors can enhance students understanding of introductory accounting by integrating text and diagrams in introductory accounting. Instructors require evidence of teaching and learning activities that enhances students learning during the study of introductory accounting and the study shows that a redesign of accounting instructional material improves students’ performance and learning experience.

Key words: Accounting education, integrated, instructional format, introductory accounting, split-attention.

INTRODUCTION

Most undergraduate financial accounting instructional material begins with an an explanation about accounting equation, followed by a formula and diagram explaining the accounting equation. Such instructional format has been found to have a negative effect on learning (Agostinho et al., 2012; Mostyn, 2012). There are a variety of ways information may be presented. Choosing alternative ways may not be easy. For example formulas may be presented in textbooks accompanying text explaining the formulas. A diagrammatic presentation or a formula presented with text above, below or on the side often present an unnecessary load for the student who may be required to search the text for the corresponding part of the formula or diagram.

If students spend most of their time searching and matching, then their learning may not be enhanced. One way to enhance students’ learning experience is to carefully redesign accounting instructional material that can be used to assist students as they try to understand difficult principles in accounting. The initial step involves identifying instructional material that is presented in a way that splits attention, for example separate diagram and text or separate formula and text. This is followed by restructuring the material in a manner that brings the text as close as possible to the relevant parts of a diagram or formula. Such a reorganization of text and diagrams would reduce the need to search the solution steps within the text and match them with corresponding parts of the diagram. This frees up mental resources that would focus on the learning process.

This paper examines the use of such integrated instructional materials as an alternative to the separate diagram and text, often referred to as split-attention materials. The integrated instructions may enhance students’ learning in the classroom. Significant research exists in mobile learning environments, educational psychology and mathematics advocating the use of integrated instructional material (Liu et al., 2012; Roodenrys et al., 2012). Results of experiments involving reorganization of instructional material in these disciplines have demonstrated improved learning. However, for example, in the research of Mostyn (2012), integrating instructional material is very sparse in accounting. The next section reviews the literature on integration of instructional material, followed by a section on ways to effectively integrate split attention material into the accounting curriculum. The result is presented from an experiment examining the effectiveness of split attention involving the accounting equation. The final section presents the concluding remarks.

INTRODUCTION

Most undergraduate financial accounting instructional material begins with an an explanation about accounting equation, followed by a formula and diagram explaining the accounting equation. Such instructional format has been found to have a negative effect on learning (Agostinho et al., 2012; Mostyn, 2012). There are a variety of ways information may be presented. Choosing alternative ways may not be easy. For example formulas may be presented in textbooks accompanying text explaining the formulas. A diagrammatic presentation or a formula presented with text above, below or on the side often present an unnecessary load for the student who may be required to search the text for the corresponding part of the formula or diagram.

If students spend most of their time searching and matching, then their learning may not be enhanced. One way to enhance students’ learning experience is to carefully redesign accounting instructional material that can be used to assist students as they try to understand difficult principles in accounting. The initial step involves identifying instructional material that is presented in a way that splits attention, for example separate diagram and text or separate formula and text. This is followed by restructuring the material in a manner that brings the text as close as possible to the relevant parts of a diagram or formula. Such a reorganization of text and diagrams would reduce the need to search the solution steps within the text and match them with corresponding parts of the diagram. This frees up mental resources that would focus on the learning process.

This paper examines the use of such integrated instructional materials as an alternative to the separate diagram and text, often referred to as split-attention materials. The integrated instructions may enhance students’ learning in the classroom. Significant research exists in mobile learning environments, educational psychology and mathematics advocating the use of integrated instructional material (Liu et al., 2012; Roodenrys et al., 2012). Results of experiments involving reorganization of instructional material in these disciplines have demonstrated improved learning. However, for example, in the research of Mostyn (2012), integrating instructional material is very sparse in accounting. The next section reviews the literature on integration of instructional material, followed by a section on ways to effectively integrate split attention material into the accounting curriculum. The result is presented from an experiment examining the effectiveness of split attention involving the accounting equation. The final section presents the concluding remarks.

LITERATURE REVIEW

This section provides a brief discussion of the split attention effect. It also provides an overview of salient literature on an instructional technique that can be used to reduce working-memory load thereby enhance students learning performance.

The split-attention effect occurs when learners are required to process and integrate multiple and separated Learning instructions involving text and diagrams that need to be integrated mentally inorder to be understood must be reorganised into physically integrated formats (Austin, 2009; Ayres and Sweller, 2005; Cierniak et al., 2009; Florax and Ploetzner, 2010; Kester et al., 2005; Pociask and Morrison, 2008). Currently, the known, most effective technique for dealing with split-attention is by way of integrated instructional materials. The strategy demands the instructor to manipulate the instructional content and is a type of instructor-managed influence over cognitive load (Paas et al., 2010).

According to Sweller (2015), a large number of instructional techniques can be used to reduce working-memory load. Integration is one such technique (Sweller et al., 2011). Instrcutional material in the form of worked examples may comprise several sources of mutually referring information. An example could be diagrams and a set of explanatory text below, above or on the side. The diagram in isolation is meaningless while little value may be obtained from the text. To learn from such examples, students must focus their attention on mentally integra-ting the multiple sources of information, since they are unintelligible in isolation. The integration would require searching for refering information on the diagram and matching it with the text. The process of searching can have deleterious effect on learning. The activities of searching and matching, although they are precursors to learning, are in themselves unrelated to learning (Paas et al., 2010).

Presenting novice students with separate text and diagrams demands effort to mentally reorganise the instructional material (Paas et al., 2003). Often, this type of presentation is found in accounting textbooks. Accounting instructors have an option to restructure some of the instructional material for learners as it will provide an important step to reduce the load in working memory and enhance learning. Some accounting textbook publishers present information in an integrated format eliminating the requirement for students to mentally integrate the two or more sources of information, which draws considerable cognitive resources from the learner, contributing to learning difficulty. Such integrated examples enhance learning since it guides the learner through the steps of a worked example (Ayres and Sweller, 2005; Ginns, 2006; Mayer, 2009).

As explained earlier, a meta-analysis of this effect has shown that integrated instructional material reduce the load on the working memory and has a positive effect on learning (Ginns, 2006). Replacing various sources of information with a single, integrated source of information assists with more effective learning. (Clark and Mayer, 2008; Mayer, 2005).

METHODOLOGY

In this study students were assigned to two different instructional formats in order to investigate the effect of these formats on learning outcomes. In the first instructional format, the presentation was similar to that found in textbooks where diagrams are presented separately from the text. The second involved physically bringing together as close as possible text and associated diagrams, which is refered to as the integrated.

The study sought to test whether learners in the integrated format would outperform students in the conventional format. Participants were randomly assigned to one of the two conditions. Random assignment was achieved by computerised creation of random numbers and assignment to students based on the numbers. The first 32 students were allocated to the first group and the other 32 students were allocated to the integrated group.

The task differentiations across the two groups were as follows:

1. Conventional group format instructional materials (Group 1).

The material for this group was presented on A3 sheets of paper. The students could see all the respective parts of the material from one sheet of paper. The conventional format is similar to that found in textbooks.

2. Integrated instructional format materials (Group 2).

The content was reformatted by bringing the text as close as possible to the diagram (integrating). The integrated instructional material was developed after reviewing the research relating to split-attention and then formatting the instructional material (Agostinho et al., 2013; Ayres and Sweller, 2005; Florax and Ploetzner, 2010; Roodenrys et al., 2012; Tindall-Ford et al., 2015).

Mental effort ratings

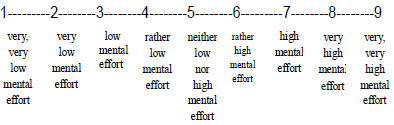

The method used to assess load in this study, and which seems to be the preferred method in most recent research, is to use subjective rating scales (Paas 1992;

Paas et al.,2003; Gog and Paas 2008). Learners were asked to rate the amount of mental effort they invested in completing a task on a 9-point Likert scale, ranging from “very, very low mental effort” to “very, very high mental effort. The scale’s (Paas, 1992) reliability (alpha > .8) and convergent, construct, and discriminate validity have been demonstrated (Gimino, 2000).

For the test phase, repeatedly after every test question, students had to rate how much mental effort they invested.

The participants in the experiment were 64 first-year undergraduate students from a Zimbabwean university. Participants were enrolled in a accounting degree program. A pre-test questionnaire was used to collect information about each participant’s age, gender, language, and knowledge of accounting. In total, 55% males and 45% females students were randomly assigned to one of the two conditions. There were 32 students in the split-attention group (Group 1; 20 males and 12 females, M = 22 years old, SD = 2.87 ), 32 students in the integrated group (Group 2; 18 males and 14 females, M = 20 years old, SD = 2.0) who participated in the study at GZU. The participants’ gender homogeneity was apparent across the two groups.

Materials

The paper-and-pen based materials covering an introductory accounting topic as well as a pre-test questionnaire and A3 pages of learning materials which included a mental effort rating question at the end of the learning phase and each test question. There were two pages of recall and transfer questions to be answered used in the test phase, including a requirement to rate mental effort after answering every test question.The learning materials were actual teaching materials used in a realistic teaching and learning environment. The instructional materials were obtained from an accounting textbook but were adapted to meet the needs of the instructional formats (Weygandt et al., 2010).

The first set of instructional material was taken directly from the textbook without any changes. This constituted the material for Group 1, the conventional format group. The second set of material combined text and diagrams (Group 2 - the integrated format group).

Pre-test of Age and Knowledge of Accounting

Students' understanding of the area being tested covered two categories:

(a) describing their knowledge of accounting on a rating scale from very poor to expert. The question testing accounting knowledge was: How would you describe your knowledge of accounting?

1--------------2-------------3-------------4---------------5

Very poor Poor Fair Good Expert

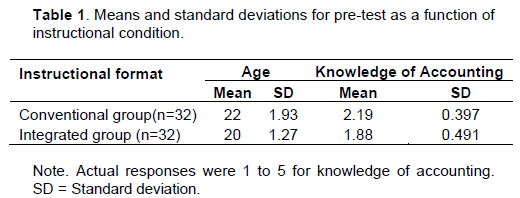

The means and standard deviations of these responses are shown in Table 1. There was a follow up question to ask participants whether they had ever learned the accounting equation before; and if so, to briefly explain what they knew about the accounting equation.

A one-way analysis of variance (ANOVA) was conducted on pre-test responses of age and basic knowledge of accounting to explore differences across the two groups participating in the experiment. The respective means and standard deviations of the pre-test responses are shown in Table 1.

The one-way ANOVAs for pre-test questions demonstrate no significant main effect of group for age (F (1,62) = 3.363, p = .071) and knowledge of accounting (F (1,62) = .205, p = .653), thus enhancing the likelihood that any statistically significant differences detected later are more likely due to the different treatment conditions.

The study had the approval of the Human Research Ethics Committee at a Zimbabwean University. A consent form was provided to each participant with information concerning the procedures, description, purpose and confidentiality conditions. The participation of students in the study was voluntary. Participants were given participant information sheets and signed the form as an indication of agreeing to participate in the study. Completion of the consent form took 10 min.

Note. Actual mental effort ratings were 0 to 9 for mental effort.

The study included three phases which were conducted during the teaching of accounting to undergraduate students. During the first phase participants provided information about their gender, age, language, and knowledge of accounting. This took ten minutes. In the learning phase, the participants were given 15 min to review the learning materials provided to them. In the final phase, the test was administered. The test consisted of recall and transfer items. The students participating in the study were given 45 min to complete the test.

The time given to complete the test was strictly controlled to avoid the possibility of a systematic difference in processing time across the two groups. Research has demonstrated that processing time is positively related to recall (Barrouillet et al., 2007).

Examples of a recall question in the test phase required students to state the accounting equation formula or stating the liquidity ratios. Recall questions required a student to retrieve information that has been learned (Carpenter, 2012). An example of a transfer question required students to classify certain expenditures as either assets or liabilities. The transfer questions tested the ability to transfer acquired knowledge, and the demands of the questions were higher than recall questions. Transfer questions require a student to apply what has been learned during instruction to a novel situation (Carpenter, 2012).

Participants reported their mental effort ratings after the learning phase and after answering each question. Participants wrote answers and any comments they wished to provide on the blank spaces immediately below the questions. The researcher collected all the test booklets soon after the students completed the tasks.

ANALYSIS AND DISCUSSION

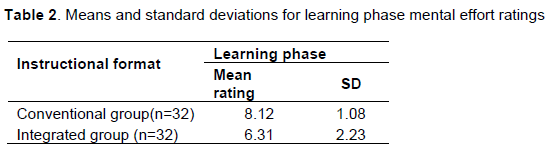

Results from the one-way ANOVA for mental effort invested in the learning phase are shown in Table 2. They indicate significant differences across the two formats, (F(1, 62) = 17.486, p < 0.05, effect size (partial η² = 0.46)). Consistent with predictions, there were signifi-cant between-group differences on mean mental effort rating on performance results. The ratings showed that the integrated group reported lower levels of load than the conventional group (6.31 rating, p < 0.05), d = 1.05.

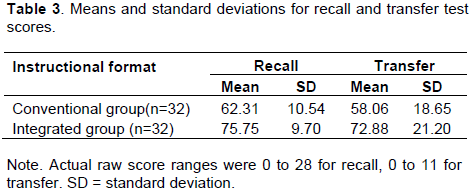

A one-way analysis of variance (ANOVA) was conducted on test performance scores to investigate the differences across the two groups involved in the study. Means and standard deviations are shown in Table 3. Recall scores showed a statistically significant main effect for the recall test items (F(1, 62) = 28.125, p < 0.05, effect size (partial η² = 0.55)). The mean recall scores showed that the integrated group had higher scores than the conventional split-attention group. The integrated group performed significantly better on the test items within the recall category, d = 1.32 indicating a large effect size (Cohen, 1988).

The one-way ANOVA for transfer questions also demonstrated a significant main effect of group (F(1, 62) = 8.803, p < 0.05, and effect size (partial η² = 0.347)). The integrated format group performed

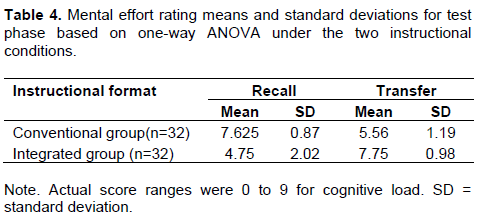

Besides rating mental effort during the the learning phase, students were also asked to rate their mental effort during the test phase. A one-way ANOVA was conducted on the instructional rating (of mental effort) that the participants recorded. Table 4 shows the mean ratings and standard deviations for the ratings of the test phase. There were significant between-group differences on mean mental effort results (F(1, 62) = 54.846, p < 0.05, effect size (partial η² = 0.679)).

Transfer items also revealed a significant effect between-groups (F(1,62) = 8.865, p < 0.05, effect size (partial η² = 0.348)). Mean recall and transfer ratings showed that the self-managed group reported lower levels of cognitive load than the integrated group. The perceived amount of mental effort invested with the split-attention format (5.56 rating, p < 0.05) was higher than that invested with the integrated format integrated format group (4.75 rating, p < 0.05), d = .74

GENERAL DISCUSSION

The finding of significantly higher transfer performance scores by students in the integrated group compared to those in the conventional split-attention group was clearly evident. The results of performance scores on transfer items are similar to those found in other disciplines, for example by Florax and Ploetzner (2010), Roodenrys et al. (2012) and Tindall-Ford et al. (2015).

The study showed a strong performance by the integrated group in the recall and transfer test items. This strongly suggest that providing students with integrated instructional material which has been reorganised by ensuring that the text is in close proximity with diagrams prior to learning new content would result in effective learning.

The main finding concerns the integration of instruc-tional material that requires students to split their attention between diagram and text. This study shows that when split split attention is managed by students by integrating text and diagrams they consistently outper-formed those in the split-attention and integrated groups (Mayer and Moreno, 2002; van Bruggen et al., 2002).

With regard to cognitive load, students in the integrated group exerted less mental effort than students in the split-attention group. This is in line with studies by Agostinho et al. (2014), Roodenrys et al. (2012) and Tindall-Ford et al. (2015). Overall, the results from the study showed that the split attention group had relatively low cognitive load and higher performance whilst the split-attention had higher cognitive load and lower performance. This suggests that the presence of split-attention has a negative effect on learning.

CONCLUSION

The ultimate purpose of instructional design is not only to make an efficient use of the available cognitive capacity but also to achieve superior performance. The study provides evidence in the discipline of acounting by yielding a significantly better performance in the integrated group. The implications of this are numerous including that instruction with emphasis on integration is an appropriate alternative to other ways of mediating the undesirable consequences of split-attention.

Many of the learning activities that novice under-graduate accounting students engage with in the classroom, whether related to reading, calculations, or other areas of studying accounting, impose considerable burdens on the limited capacity of working memory because they split the attention of the student. These activities often require a student to hold in mind some information (for example, a text) while attempting to match with relevant parts of a diagram. This is something that this study argues is mentally challenging and may impede learning. Therefore instructors need to design instructional material that is already integrated.

The major implication of this study is that integration appears to enhance learning. The results support most prior studies in suggesting that material needs to be integrated before any meaningful learning can occur. It seems that there is a need for more studies in other accounting related subjects such as taxation and finance.

REFERENCES

|

Agostinho S, Tindall-Ford S, Bokosmaty S (2014). Adaptive diagrams: a research agenda to explore how learners can manipulate online diagrams to self-manage cognitive load. In: Handbook of human centric visualization, Springer, New York pp.529-550. |

|

|

Ayres P, Sweller J (2005). The split-attention principle in multimedia learning, In: R.E. Mayer (Ed.), The cambridge handbook of multi-media learning, New York: Cambridge University Press pp. 135-146. |

|

|

Carlson R, Chandler P, Sweller J (2003). Learning and understanding science instructional material, Journal of educational psychology, 95(3):629-640. |

|

|

Clark RC, Mayer RE (2008). E-Learning and the science of instruction. San Francisco, CA: Pfeiffer. |

|

|

Florax M, Ploetzner R (2010). What contributes to the split-attention effect? The role of text segmentation, picture labelling, and spatial proximity, Learn. Instruction 20(3):216- 224. |

|

|

Ginns P (2006). Integrating information: a meta-analysis of the spatial contiguity and temporal contiguity effects, Learn. Instruct. 16:511–525. |

|

|

Liu TC, Lin YC, Tsai MJ, Paas F (2012). Split-attention and redundancy effects on mobile learning in physical environments, Comput. Edu. 58(1):172-180. |

|

|

Mayer RE (2009). Multimedia learning, Cambridge university press. |

|

|

Mayer RE (2005). Principles for managing essential processing in multimedia learning: segmenting, pre-training, and modality, In: R.E. Mayer (Ed.), Cambridge handbook of multimedia learning New York: Cambridge University Press, pp.169-182. |

|

|

Mayer RE, Moreno R (2002). Aids to computer-based multimedia learning, Learn. Instr. 12(1):107-119. |

|

|

Mostyn GR (2012). Cognitive load theory: What it is, Why its important for accounting instruction and research, Issues Account. Educ. 27(1):227-245. |

|

|

Paas F, Renkl A, Sweller J (2003). Cognitive load theory and instructional design: Recent developments, Edu. Psychol., 38(1):1-4. |

|

|

Paas F, Van Gog T, Sweller J (2010). Cognitive load theory: New conceptualizations, specifications, and integrated research perspectives, Educ. Psychol. Rev.22:115-121. |

|

|

Roodenrys K, Agostinho S, Roodenrys S, Chandler P (2012). Managing one's own cognitive load when evidence of split-attention is present, Appl. Cognit. Psychol. 26(6):878-886. |

|

|

Sweller J (2015). In Academe, What Is Learned, and How Is It Learned?, Current Directions In Psychological Science (Sage Publications Inc.), 24(3):190-194. |

|

|

Sweller J, Ayres P, Kalyuga S (2011). Cognitive load theory. New York:Springer. |

|

|

Tindall-Ford S, Agostinho S, Bokosmaty S, Paas F, Chandler P (2015). Computer-based learning of mathematical concepts by studying instructor-managed or self- managed split-attention materials, Education Technology and Society (Online). |

|

|

Van Bruggen JM, Kirschner PA, Jochems W (2002). External representation of argumentation in CSCL and the management of cognitive load, Learn. Instruct., 12(1):121-138. |

|

|

Weygandt, JJ, Chalmers K, Mitrione L, Fyfe M, Kieso DE, Kimmel PD (2010). Principles of financial accounting. Australia: John Wiley & Sons Australia Ltd. |

|

Copyright © 2024 Author(s) retain the copyright of this article.

This article is published under the terms of the Creative Commons Attribution License 4.0