Full Length Research Paper

ABSTRACT

Many countries have adopted a taxpayer charter or equivalent, which governs the relationship between taxpayers and tax authorities. However, little is known about the extent to which these charters are constructed in accordance with widely accepted fairness dimensions, as well as the relative importance of taxpayer charter rights within each fairness dimension. This research investigates the Canadian taxpayer charter (the Taxpayer Bill of Rights) using a trio of fairness dimensions that are known to influence tax compliance and the tax assessment process: procedural fairness, interpersonal fairness, and informational fairness. Rights classified as interpersonal or informational fairness were significantly underweight relative to procedural fairness. Furthermore, taxpayers rated data privacy, tax authority’s accountability, and comprehensive communication of information as the most important aspects of their service relationship with the tax authority. Implications for tax policy makers and tax researchers are discussed.

Key words: Fairness, tax compliance, charter.

INTRODUCTION

Taxpayer charters summarize taxpayers’ rights and obligations pertaining to their tax affairs and dealings with tax authorities. The Organisation for Economic Co-operation and Development (OECD), which is an international economic organization with a focus on the role and importance of tax policies, and informal world tax authority, has suggested that tax authorities issue a taxpayers’ charter, and that a taxpayers’ charter should cover basic taxpayers’ rights and obligations (OECD, 1990). The United Kingdom was the first to adopt a taxpayers’ charter, in 1986. A number of countries have subsequently adopted taxpayer charters, including Australia, Canada, France, India, Italy, Ireland, New Zealand, South Africa, Pakistan, the Philippines, Russia, Spain, Uganda, and the United States (CIOT, 2008).

Taxpayer charters, or equivalents, such as a Taxpayer Bill of Rights, may improve taxpayers’ trust and confidence in tax authorities, which in turn may improve tax morale, and subsequently tax compliance. A taxpayer charter symbolizes the partnership between taxpayers and tax authorities, which helps to address the unequal balance of power between these parties, and may instil trust in taxpayers (Unger, 2014). There is also a wide literature on the association between fairness and compliance (Verboon and Goslinga, 2009), which supports the premise that taxpayers who perceive a tax authority to be fair are more likely to be compliant. A taxpayer charter is a way for a tax authority to establish fairness in its dealings with taxpayers, and as such, may be one way for tax authorities to improve compliance through fairness. Alm and Torgler (2011) contend that a “full house” of compliance strategies is needed to combat tax evasion, which includes deterrence activities such as audits and penalties, but also a more service-oriented administrative focus, which includes fairness-based approaches.

Although tax research has examined the historical development of the content of some taxpayer charters (Doern, 1993; McLennan, 2003), the suitability of taxpayer charters as a dispute resolution mechanism (Mookhey, 2013), the legal status of taxpayer charters (Dawe, 2014), and a comparative analysis of different countries’ charters (Unger, 2014), there is a dearth of theoretically based empirical research regarding the propriety of the contents of taxpayer charters. The purpose of this research is twofold. First, it will analyze the contents of the taxpayer charter in Canada – the Taxpayer Bill of Rights – using Colquitt’s (2001) theoretical fairness framework, which encompasses procedural fairness, interpersonal fairness, and informational fairness, to determine the extent to which different aspects of fairness are present in the taxpayer charter. Second, it will identify taxpayer’s preferences for the contents in this charter according to each fairness dimension. By recognizing which aspects of each dimension of fairness are most important to taxpayers, tax authorities may be able to refine their compliance strategies, and tax researchers may be able to focus their research on previously unexplored aspects of fairness and com-pliance. Canada was chosen, as its taxpayer charter has received minimal attention in the tax literature (Li, 1998), and its charter has undergone several major revisions, making it a timely case study.

The Canadian Taxpayer Bill of Rights contains sixteen items. These items were classified as procedural fairness, interpersonal fairness, and informational fairness (Colquitt, 2001). The item classification was validated by an expert panel. A survey was administered to a sample of 606 Canadian taxpayers, who ranked each right according to order of importance for each fairness category. Statis-tical analysis was then performed on the ranked data. Results indicated that items comprising interpersonal fairness and informational fairness were decidedly underweight relative to procedural fairness. The most important procedural fairness item was, The right to privacy and confidentiality, whereas the most important informational fairness right was, The right to complete, accurate, clear, and timely information. No interpersonal fairness items were significantly preferred over each other.

The remainder of this paper is structured as follows. In the next section, Colquitt’s (2001) framework is presented, along with empirical evidence on the association between each fairness dimension and compliance. Next is a brief overview of the Canadian Taxpayer Bill of Rights, followed by the research methodology and results. The paper concludes with a discussion of the implications for tax researchers and tax authorities.

Tax fairness and tax compliance

Fairness is a judgment arising from actual or imagined comparisons involving oneself or oneself and others. Fairness was initially conceptualized as distributive fairness, which is concerned with outcome allocations. Later, the conceptual understanding of fairness was broadened to include procedural fairness, which is the fairness of procedures that lead to decision outcomes, and interactional fairness, which is concerned with the quality of the treatment individuals receive when procedures are enacted. Subsequently, interactional fairness was split into two distinct elements: interpersonal fairness and informational fairness. Interpersonal fairness refers to sensitivity and respectful treatment shown during decision processes, whereas informational fairness refers to the adequacy of explanations given during decision processes. The fairness literature thus recognizes these four distinct but related categories of fairness: distributive, procedural, interpersonal, and informational (Colquitt, 2001).

These four factors are generalizable to contexts where authority figures make decisions that impact one or more members of a collective (Colquitt et al., 2005). Therefore, applying this framework to the tax context is appropriate, since in the tax context tax authorities make decisions that impact individual taxpayers (a collective). The focus of this paper is on procedural, interpersonal, and informational fairness, since this trio encompasses the fairness of the tax assessment process, which is informally governed by taxpayer charters. In the tax context, procedural fairness is concerned with administrative protocol leading to taxpayer outcomes (Wenzel, 2002); interpersonal fairness refers to the relational aspects of the tax authority-taxpayer relation-ship; and informational fairness refers to the adequacy of explanations given to taxpayers by tax authorities (Wenzel, 2006). Situations involving an interaction between taxpayers and a tax authority, such as a taxpayer inquiry, or a taxpayer-tax authority dispute, will have all three dimensions of fairness present con-currently, since the tax authority has procedures to follow, the taxpayer will have a relational encounter with a tax authority through a tax agent or other channel, and the tax authority will provide some degree of explanation during the encounter. What remains to be discovered is the degree to which taxpayer charters comprise each of these three dimensions of fairness, and within each dimension, which taxpayer rights are most important to taxpayers, and therefore might be most relevant for compliance.

There is a significant body of literature that documents a significant and positive association between each of procedural fairness, interpersonal fairness, and informational fairness, on tax compliance (Farrar et al., 2015). However, only a few studies are able to provide insights into the nuances of each type of fairness, and how these nuances influence tax compliance. Regarding procedural fairness, Worsham (1996) investigated accuracy and consistency of tax procedures on tax compliance, and Hogan et al. (2013) investigated the effect of taxpayer voice on tax compliance. Wenzel and Taylor (2004), Wenzel (2006), and Doyle et al. (2009) investigated the respectful tone of tax authority letters, and the information quality of tax authority letters. Van Dijke and Verboon (2010) investigated how the clarity of explanation impacted tax compliance. By classifying taxpayer charters according to each dimension of fairness, and subsequently identifying the items that are most relevant to taxpayers, tax researchers may be able to identify additional nuances of fairness that are likely to impact compliance, which tax researchers could further investigate, thereby extending the tax fairness-tax compliance literature. There are also tax policy implications arising from this classification and ranking, since by knowing which aspects of each type of fairness are most important to taxpayers, tax authorities can better focus their service delivery strategies to ensure the needs of taxpayers are met, which may in turn improve compliance.

OVERVIEW OF CANADA?S TAXPAYER BILL OF RIGHTS

The genesis of the Canadian Taxpayer Bill of Rights began in 1984, when a task force issued a report with 76 recommendations as to how Canada’s tax authority (the Canada Revenue Agency; CRA) could improve service to taxpayers. The following year, a Declaration of Taxpayer Rights was issued, containing eight rights taxpayers had in their dealings with the CRA (Li 1998). It was not until 2007 that an official Taxpayer Bill of Rights was introduced in Canada, which contained fifteen rights. Also in 2007, the Office of the Taxpayers’ Ombudsman was created, with a mandate to uphold the rights in the Taxpayer Bill of Rights, and assist taxpayers who have grievances about their dealings with the CRA. A sixteenth right was included in 2013 (CRA 2013).

RESEARCH METHODOLOGY

The research method consists of three steps. First, the sixteen rights were classified according to whether each was related to procedural fairness, interpersonal fairness, or informational fairness. This classification was validated with an expert panel of tax academics and tax practitioners. Second, a survey was administered to a large sample of taxpayers, in which they ranked each right in order of importance, across each dimension of fairness. Third, statistical analysis was performed on the data to determine if and where there were significant differences in preferences for each right within each dimension of fairness.

Step 1: Classification of rights

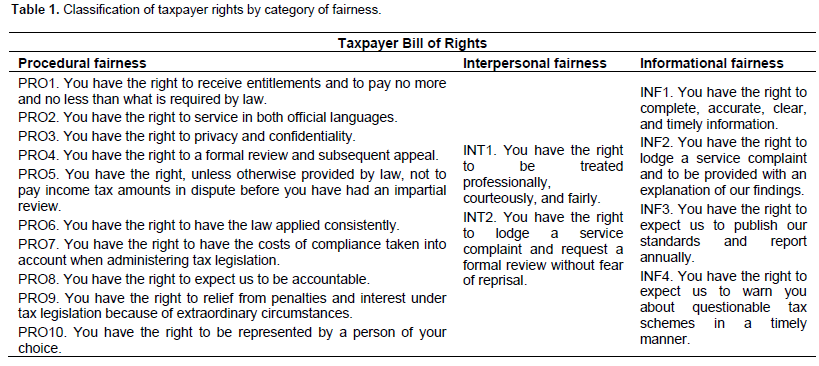

All sixteen rights were classified according to whether each was related to procedural fairness, interpersonal fairness, and informational fairness. This classification is contained in Table 1. Each are listed in the order in which they appear in the Taxpayer Bill of Rights, and are labelled as ‘PRO’ (procedural fairness), ‘INT’ (interpersonal fairness), or ‘INF’ (informational fairness).

In most cases, the wording of each right was clear and unambiguous. For example, a clearly worded right is, You have the right to have the law applied consistently. Consistency was the only focus of this particular right. Other rights were somewhat ambiguous, since they contained elements that could have spanned multiple fairness dimensions. For example, an ambiguous right is, You have the right to complete, accurate, clear, and timely information. The notion of timeliness could be procedural, since a delay in the execution of a procedure could relate to procedural fairness, or it could relate to the adequacy of explanations (informational fairness). Since the overall context of this right was about the provision of information to taxpayers, it was classified as relating to informational fairness.

Three of the rights had similar language, but each captured a different dimension of fairness. The right, You have the right to a formal review and subsequent appeal, relates to a tax procedure. The right, You have the right to lodge a service complaint and request a formal review without fear of reprisal, relates to interpersonal treatment following the procedure. The right, You have the right to lodge a service complaint and to be provided with an explanation of our findings, relates to informational fairness. No other right used language that had cross-similarities.

The expert panel consisted of four tax academics and two tax practitioners. Members of the panel were given the definitions for each dimension of fairness, and were asked for input on the classifications, and whether they would suggest any changes. There were no changes to the initial classifications, nor did any member of the panel disagree with the underlying classification itself.[1]

Step 2: Administration of survey

Participants were Canadian taxpayers recruited from a consumer research firm that has a database of 200,000 Canadians. To be representative of a typical taxpayer population, participants were randomly selected using two parameters: gender and age. The sample was restricted to taxpayers between the ages of 25 to 80, and was evenly distributed across age groups and gender. 637 respondents completed the survey, at which point the data collection was terminated. Of these, 31 contained missing data and were deleted, leaving 606 usable responses.

Potential participants received an email invitation from the firm to participate in a questionnaire about income taxes. Individuals willing to complete the survey clicked on a web link, and were directed to the survey. Respondents had a unique user ID and password provided by the firm, which ensured that they could not respond to a survey more than once. Participants were incentivized using a point system specific to the firm.

Participants read an introductory screen, which provided a brief overview of the Taxpayer Bill of Rights. They were told that on the following three screens, they would see these rights listed, and would be asked to rank them in order of their importance. To minimize order effects, i.e., the tendency for respondents to rank the first item in the list as the most important, etc., the lists of rights were randomly ordered for each participant. Demographic information was collected at the end of the survey, and included gender, age, income, education, tax preparer, whether the respondent had ever had an unpleasant encounter with the tax authority, and whether the respondent had ever had a tax dispute with the tax authority. Demographic data are reported in Table 2.

Step 3: Statistical Analysis

To perform statistical analysis on the sample, statistical tests were conducted to determine if there were any significant differences in the rankings within each fairness dimension. Then, if a test result was significant, further post-hoc statistical tests were conducted to understand and isolate where the significant differences in rankings occurred within each dimension.

One member of the panel commented that the right, You have the right to expect us to be accountable, which was classified as relating to procedural fairness, could be an item relating to informational fairness, since by providing information to taxpayers, a tax authority is being accountable. Nevertheless, informational fairness in the tax context relates to the adequacy of explanations, rather than a tax authority’s willingness to make an explanation, which is more of a procedural concern. By providing an explanation, regardless of its adequacy, the tax authority is being accountable. Therefore, since the notion of accountability is broader than just the adequacy of an explanation, it was retained as relating to procedural fairness.

According to the most recent Canadian income statistics published by Statistics Canada (http://www.statcan.gc.ca/tables-tableaux/sum-som/l01/cst01/famil105a-eng.htm), the sample was similarly weighted to that of the Canadian population with respect to income, except that the income category below $25,000 was underweight (by about 15%), and the income categories above $50,000 and $75,000 were overweight by 6% and 4%, respectively. Furthermore, 8.4% of the sample chose not to disclose their income, which may have been the lowest income respondents. Although the sample might be slightly less representative of the lowest income Canadians, given that the population of the income category below $25,000 is the one least likely to pay tax, the sample is likely to be representative of the broader population of Canadian taxpayers. The median age of the sample was 51, which compares favorably with the median age in Canada in the 25 to 80 age group (http://www.statcan.gc.ca/pub/91-215-x/2012000/part-partie2-eng.htm).

.png)

Testing for overall differences in the rankings within each fairness category

The first test requires testing for significant differences in the rankings for each fairness dimension. The Friedman test was used, which is appropriate for testing differences in ranked data between conditions when there are more than two conditions and the same participants have been used in all conditions (Field, 2009). Since one fairness category (interpersonal fairness) had two conditions, the Friedman test cannot be used. In this instance, the binomial test is appropriate (Field, 2009). A significant test result indicates that there are significant differences in rankings of the rights within a fairness category, but it cannot identify where the differences occur.

Results are as follows. For the ten rights pertaining to procedural fairness, the test result was significant (χ2 = 786.69, p<0.001), which indicates that there were significant differences in terms of how these 10 rights were ranked. For the two rights pertaining to interpersonal fairness, the test result was not significant (Pbinomial=0.49), which indicates respondents did not prefer one right over another. For the four rights pertaining to informational fairness, the test result was significant (χ2 = 450.65, p<0.001), which also indicates that there were significant differences in terms of how these four rights were ranked. Thus, there were significant differences in rankings within the procedural fairness and informational fairness dimensions. Subsequent statistical analysis can isolate which rights are ranked significantly different from each other, within each of these two categories.

Understanding the differences in rankings within each fairness category

Since there were two significant test results, it is necessary to do further statistical analysis to determine which rights were ranked significantly different from each other. The Wilcoxon signed-rank test (Field, 2009) is appropriate for this purpose. One-tailed tests are used, since the test is whether one mean is higher than another. A Bonferroni correction is applied to the significance level, according to the number of pairwise comparisons (Field, 2009).

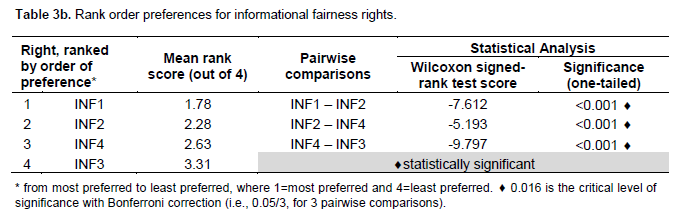

Within procedural fairness and informational fairness, the rights were ranked according to their mean rank, in order of preference, beginning with the most preferred right. Wilcoxon signed-rank tests were performed on each pair of rights to determine if the order of preferences differed significantly. Table 3a reports the results for the rights classified as

.png)

procedural fairness, and Table 3b reports the results for the rights classified as informational fairness. Each table shows the rights ranked in order of preference, beginning with the most preferred right, the mean rank of each right, and the results of the Wilcoxon signed-rank test.

Results are as follows. Of the ten procedural fairness rights, the most preferred right was PRO3, You have the right to privacy and confidentiality, with a mean rank of 4.09 out of 10, followed by PRO8, You have the right to expect us to be accountable, with a mean rank of 4.28 out of 10. Although these two rights were not ranked significantly different from each other (Z=-1.208, p=0.114), the rank scores of PRO8 and the next-highest ranked right (PRO1; mean score of 4.90 out of 10) were significantly different (Z=-3.881, p<0.001), which indicates that the two highest-ranked rights were significantly more preferred than any other procedural right.

There were no other significant differences in mean rank scores, except for the two least-preferred rights, PRO10, You have the right to be represented by a person of your choice, with a mean rank of 6.34 out of 10, and PRO2, You have the right to service in both official languages, with a mean rank of 8.16 out of 10. PRO10 was significantly different than the right ranked next in highest importance to it, PRO7 (Z=-3.167, p=0.001), and PRO2 was ranked significantly different than PRO10 (Z=-10.987, p<0.001). Thus, respondents made a significant distinction between their two least-preferred procedural fairness rights, and also made a significant distinction between their two least-preferred procedural fairness rights and all other procedural fairness rights. Respondents did not make a significantly different distinction in preference rankings amongst the remaining six procedural fairness rights.

Of the four rights associated with informational fairness, there was a clear distinction in preferences for each right, since all of the statistical test scores were statistically significant. The most preferred right was INF1, You have the right to complete, accurate, clear, and timely information (mean rank of 1.78 out of 4), followed by INF2, You have the right to lodge a service complaint and to be provided with an explanation of our findings (mean rank 2.28 out of 4), followed by INF4, You have the right to expect us to warn you about questionable tax schemes in a timely manner (mean rank 2.63 out of 4), and finally the least-preferred right, INF3, You have the right to expect us to publish our service standards and report annually (mean rank 3.31 out of 4).

Sensitivity analysis

Although not tabulated, sensitivity analysis was conducted on each mean rank score. Differences in rank scores across dichotomous demographic variables (gender, whether the respondent had ever had an unpleasant encounter with the tax authority, and whether the respondent had ever had a tax dispute with the tax authority) were analyzed using two-tailed Mann-Whitney tests (Field, 2009). Although there were a few significant differences in rank score by gender and whether the respondent had ever had a tax dispute, the overall rankings of preferences within fairness dimensions did not change, nor their statistical significance relative to each other. Consequently, respondents’ gender, having had an unpleasant encounter with the tax authority, and having had a tax dispute with the tax authority do not appear to influence overall preferences for taxpayer rights.

Differences in ranked scores across demographic variables with more than two conditions (education, income, tax preparer) were analyzed using Kruskal-Wallis tests (Field, 2009). Although there were a few significant differences for income and tax preparer, the overall rankings of preferences within fairness dimensions did not change, nor their statistical significance relative to each other. Consequently, respondents’ education, income, and choice of tax preparer do not appear to influence overall preferences for taxpayer rights.

The sensitivity analysis suggests that the overall preference rankings within fairness categories appear to be robust, even after considering the influence of demographic variables.

IMPLICATIONS AND CONCLUSION

Although it is not publicly documented how the contents of the Taxpayer Bill of Rights were chosen, it is unlikely that a theoretically based fairness framework was explicitly or implicitly considered. Given the importance of fairness to taxpayers’ compliance, it is useful to consider rights under a taxpayer charter with respect to fairness. One broad finding that emerges from this study is the unequal distribution of rights according to dimensions of fairness, since ten of the sixteen rights were related to procedural fairness, four were related to informational fairness, and only two were related to interpersonal fairness. The emphasis on procedural fairness may not be misplaced, since there are likely to be more nuances with respect to administrative procedures rather than how information is conveyed to taxpayers, or with respect to the relational aspects of the taxpayer-tax authority encounter. Nevertheless, it is likely that the interpersonal and informational aspects of the taxpayer-tax authority relationship deserve greater emphasis, especially given the empirical findings with respect to their positive impact on tax compliance. Thus, these results suggest that policy makers should give greater consideration to interpersonal and informational fairness when crafting or revising taxpayer charters. Future research could also consider the extent to which other countries’ taxpayer charters have an unequal distribution of fairness dimensions.

While academic research has suggested revisions to existing taxpayer charters (Unger, 2014), and while professional tax bodies have developed model taxpayer charters (CFE, 2014; OECD, 1990), the underlying fairness dimensions have not been explicitly considered in the construction of these charters. Given that procedural fairness, interpersonal fairness, and infor-mational fairness occur concurrently in tax practice, tax policy makers could consider how their taxpayer charters reflect the multidimensionality of tax fairness.

Results from this study also have implications for tax authorities. Since there were two procedural fairness rights ranked significantly higher than all other procedural rights, it is possible that tax authorities should give greater attention to them, as they may be likely to influence compliance directly, or indirectly through trust. Future research could investigate these possibilities. Specifically, taxpayers’ right to privacy and confidentiality was the most preferred procedural fairness right, followed by the right for the tax authority to be accountable. Pragmatically, not only could the tax authority emphasize the confidentiality of taxpayer-tax authority transactions and its accountability to taxpayers on its websites, correspondence, and other channels of communication, but where breaches of privacy or confidentiality occur, or where there is a perception that the tax authority failed to be accountable, it may be especially important for tax authorities to take transparent and reparative actions, as subsequent compliance may be impacted.

Results from this study also suggest that information provided by tax authorities to taxpayers is important, especially as it relates to completeness, accuracy, clarity, and timeliness. Future research could consider how these elements impact compliance concurrently, or indirectly through trust. Given the low number of interpersonal fairness rights, it may not be surprising that one right was not significantly preferred over another, but this does not mean that interpersonal fairness is not important to taxpayers. The empirical research on the association between interpersonal fairness and compliance, cited earlier, suggests otherwise. However, future research could identify other aspects of interpersonal fairness that may be relevant to taxpayers with a view to understanding which aspect(s) is(are) most valued by taxpayers.

Implications of these results for tax researchers are that issues in the most preferred procedural and informational rights could be investigated further to determine their impact on tax compliance. Specifically, tax researchers could consider how privacy or confidentiality of taxpayer information, or lack thereof, impacts compliance; how accountability of tax authorities, or lack thereof, impacts compliance; and how the quality of the information provided to taxpayers with respect to accuracy, complete-ness, clarity, and delay, impacts compliance.

There are several limitations to this study. First, the results are tested on taxpayers from Canada, and although there is no reason to believe they would not generalize to taxpayers from other countries, results should be applied with care. Second, given the nature of the data and the categorization framework, it was not possible to assess the relative rankings of rights from one category with the rankings of rights from another category. It may be useful to know, for example, if the lowest ranked right from one dimension is ranked higher than the highest ranked right from another dimension. Future research could examine this possibility.

In Canada, approximately 5,400 complaints are received each year in Canada by the Office of the Taxpayers’ Ombudsman, and it conducts investigations on about 1,000 of these, pertaining to the Taxpayer Bill of Rights (OTO, 2013). Therefore, the rights under this taxpayers’ charter are of importance. Furthermore, the Canadian tax authority is planning to cut 3,100 full-time positions by 2017-18, and in 2013 closed payment and enquiry service counters in its Tax Services Offices across Canada (Fekete, 2013; Rankin, 2014). Thus, the quality of customer service has likely suffered and will likely suffer further. There has also been a recent series of Canadian cases where taxpayers alleged negligence by tax agents (Bevacqua, 2013). Consequently, under-standing key aspects of the tax authority-taxpayer service relationship should be important to tax authorities, who may be better able to channel their resources to prioritize a customer service focus on the attributes of the tax assessment process that are valued most by taxpayers, thereby improving compliance directly, or indirectly through other means, such as trust.

Globally, since tax authorities in advanced economies have been subject to significant budget cuts (OECD 2012), low-cost ways to improve compliance will only increase in importance, and taxpayer charters may be instrumental in ensuring smooth interactions between tax authorities and taxpayers. This research has highlighted several items relating to procedural fairness and informational fairness that appear especially important to taxpayers. This research also suggests that tax policy makers should give greater consideration to interpersonal fairness and informational fairness when constructing taxpayer charters, and in particular, identify other aspects of interpersonal fairness that could be incorporated into taxpayer charters.

CONFLICT OF INTERESTS

The author has not declared any conflict of interests.

REFERENCES

|

Alm J, Torgler B (2011). Do ethics matter? Tax compliance and morality. J. Bus. Ethics 101(4): 635-651. Crossref |

||||

| Bevacqua J (2013). Suing Canadian tax officials for negligence: An assessment of recent developments. Can. Tax J. 61(4):893-914. | ||||

| CFE (2013). A model taxpayer charter. Confederation Fiscale Européenne. | ||||

| CIOT (2008). A taxpayers' charter for the United Kingdom. Chartered Institute of Taxation. | ||||

|

Colquitt J (2001). On the dimensionality of organizational justice: A construct validation of a measure. J. App. Psych. 86(3):386-400. Crossref |

||||

| Colquitt J, Greenberg J, Scott B (2005). Organizational justice: Where do we stand? ("Handbook of organizational justice", Erlbaum Associates pp. 589-619). | ||||

| CRA (2013). Taxpayer Bill of Rights Guide: Understanding your rights as a taxpayer. Retrieved 30 April 2015, from: http://www.cra-arc.gc.ca/E/pub/tg/rc17/rc17-11-13e.pdf. | ||||

| Dawe R (2014). A legal duty to provide accurate information to the public? J. Parl. Pol. Law 8(1):187-208. | ||||

|

Doern G (1993). The UK Citizen's Charter: Origins and implementation in three agencies. Policy Politics 21(1):17-29. Crossref |

||||

| Doyle E, Gallery K, Coyle M (2009). Procedural justice principles and tax compliance in Ireland: A preliminary exploration in the context of reminder letters. J. Fin. Man. Publ. Serv. 8(1):49-62. | ||||

| Farrar J, Massey D, Thorne L (2015). Tax fairness and tax compliance: A literature review and tax fairness scale development study. Working paper. | ||||

| Fekete J (2013). Federal government plans to slash millions, hundreds of staff from Canada Revenue Agency compliance programs. Retrieved 30 April 2015, from: http://o.canada.com/business/federal-government-plans-to-slash-millions-hundreds-of-staff-from-canada-revenue-agency-compliance-programs/ | ||||

| Field A (2009). "Discovering Statistics Using SPSS". (3rd Edition), Sage Publications, Thousand Oaks, California. | ||||

|

Hogan B, Maroney J, Rupert T (2013). The relation among voice value, policy outcomes, and intensity of support on fairness assessments of tax legislation. J. Am. Tax. Assoc. 216(4):209-217. Crossref |

||||

| Li J (1998). Taxpayers' Rights in Canada. ("Taxpayers' Rights: An International Perspective", Queensland, Revenue Law Journal, School of Law, Bond University pp.89-137. | ||||

| McLennan M (2003). The principles and concepts in the development of the Taxpayers' Charter. Austr. Tax Rev. 32(1):22-50. | ||||

| Mookhey S (2013). Tax disputes system design. J. Tax Res. 11(1):79-96. | ||||

| OECD (1990). Taxpayers' rights and obligations – practice note. OECD Committee of Fiscal Affairs Forum on Tax Administration. | ||||

| OECD (2012). Working smarter in structuring the administration, in compliance, and through legislation. Forum on Tax Administration, Information note. | ||||

| OTO (2013). Annual Report. Office of the Taxpayers' Ombudsman. Retrieved 30 April 2015, from: http://www.oto-boc.gc.ca/rprts/nnl/rprt1213-eng.pdf | ||||

| Rankin M (2014). CRA Service Cuts. Retrieved 30 April 2015, from: http://murrayrankin.ndp.ca/changes-at-the-canada-revenue-agency. | ||||

| Unger K (2014). Ethics codes and taxpayer charters: Increasing tax morale to increase tax compliance. J. Tax Res. 12(2):483-498. | ||||

|

Van Dijke M, Verboon P (2010). Trust in authorities as a boundary condition to procedural fairness: effects on tax compliance. J. Econ. Psych. 31(1):80-91. Crossref |

||||

|

Verboon P, Goslinga S (2009). The role of fairness in tax compliance. Neth. J. Psych. 65(1):136-145. Crossref |

||||

|

Wenzel M (2002). The impact of outcome orientation and justice concerns on tax compliance: The role of taxpayers' identity. J. App. Psych. 87(4):629-645. Crossref |

||||

|

Wenzel M, Taylor N (2004). An experimental evaluation of tax-reporting schedules: a case of evidence-based tax administration. J. Pub. Econ. 88(12):2785-2799. Crossref |

||||

|

Wenzel M (2006). A letter from the tax office: Compliance effects of informational and interpersonal justice. Soc. Just. Res. 19(3):345-364. Crossref |

||||

| Worsham R (1996). The effect of tax authority behavior on taxpayer compliance: a procedural justice approach. J. Am. Tax. Assoc. 18(2):19-39. | ||||

Copyright © 2024 Author(s) retain the copyright of this article.

This article is published under the terms of the Creative Commons Attribution License 4.0