ABSTRACT

Organizations that oversee education institutes contribute to the quality of education. Audit as a tool can support the optimization of processes for these organizations. However, literature was scarce regarding audit in educational monitoring organizations. This research attempts to understand the position that audit holds in educational monitoring and how it optimizes their processes. A questionnaire based on audit literature was prepared with the aid of experts to fill in the gaps regarding education. A total of 199 responses were collected from senior executives of educational monitoring organizations. The data were analyzed through SPSS and a factor analysis was initially used. The correlations between the factors were discerned using a regression analysis. The research produced 4 factors that measure the process optimization, ability to support external audits, support given by audit and the reorganization of processes after the audit. The results showed that audit is used supportively and not proactively. The interesting finding is in reorganization caused by the need of optimization before the audit's execution. Audit is thus not only considered a tool for optimizing processes, but as a means of stimulation. Therefore, its healing properties are not fully utilized, despite the perceived importance of audit to organizations and states.

Key words: Internal audit, education, educational institutes, educational monitoring organizations, public sector.

The science of Auditing has proven in recent years its importance in the efficiency of processes and improvements of results, both in the private and public sector. Through audit, companies and organizations can identify and rectify issues, impossible to determine otherwise due to the speed of their daily processes. At

the same time, the inclusion of an internal audit department is increasingly applied for faster detection of problematic activities and incidents (Papastathis, 2014).

In educational organizations, quality, resource management and operational improvements are profound factors for losses prevention and reduction; improve efficiency and achieve teaching quality. There is a growing need to apply optimal management practices in both private and public education (Sorros et al., 2017). Regardless of the country, educational institutions are subject of public organizations that promote knowledge, research and innovation. The latter bodies are responsible for proper conduct of training, and provision of support for students, faculty and employees of educational institutions. Through proper management exercised by these educational monitoring organizations, evolution and renewal of educational processes is promoted; as well as the knowledge acquired by new students or pupils. It should be mentioned that monitoring, management and consulting services are provided to both private and public educational institutions, regardless of level (primary, secondary or higher education).

Due to its complexity, as well as importance of the educational system of institutions they supervise, public bodies are in need of occasional reorganizations. This change in activities, procedures and resources must be thorough and made through careful planning (Aikins, 2011; Badara and Saidin, 2012; Enofe et al., 2013). The importance of audit is crucial regarding successful amendments in organizational charts as well as changes in activities (Drogalas et al., 2020).

The changes can have a direct impact on swiftness and efficiency of affairs performed by educational institutions. At the same time, through their modern and improved operation, educational support organizations can focus on goals of renewal and implementation of innovations in the educational process (Sorros et al., 2017).

The consulting significance of internal audit in the management of educational organizations is found in strategies of effectiveness, efficiency, quality and transparency. This paper treats internal audit as an operational management implementation tool in educational organizations. Beyond its contribution to existing studies, it highlights the relationship between internal and external audit with educational supportive institutions. At the same time, a scarcity of in-depth analyses in the literature, regarding internal audit in education and its support services was evident. Educational supporting organizations and as a result educational institutions can achieve added value from their activities (Aikins, 2011; Badara and Saidin, 2012; Enofe et al., 2013).

The main objective of the research is to create a research tool that will identify the causal relationships of a theoretical model, reflecting the factors that influence management of operations. The model implements quality, effectiveness and efficiency of educational organizations in relation to internal audit. The theoretical model incorporates factors based on information from the relevant literature and from interviews with accounting experts. The model was composed with the aid of a questionnaire that reflects the interactions of internal audit-related tool applied to educational organizations.

Internal audit

According to the Institute of Internal Audit, internal audit as an independent, reassuring and consulting activity is designed to add value and improve operations (Badara and Saidin, 2012; Vassiliou et al., 2017). A broader definition defines it "as the Administration Consultant" not limited to the traditional financial audit based on financial statements. Internal audit integrates audit principles to an entity’s philosophy and practices. With the absence of obstacles or constraints, internal audit works as a tool to heighten perception (Papastathis, 2014).

The basic principles of internal audit provide a framework that implements and organizes the basis for evaluating the performance of internal audit and promotes improved organizational processes (Papastathis, 2014; Dascalu et al., 2016). Independence and objectivity are key elements of a successful internal audit department. Furthermore, the close collaboration between management and internal audit department leaders must not undermine the objectivity of this relationship. Auditors should be able to execute their projects professionally, while at the same time, audit executives ought to maintain an assurance of quality improvements (Vassiliou et al., 2017).

Additionally, effective internal audit management should aim for proper evaluation and contribute to improved processes adopting systematic and prudent approaches. To that extent, the ability of an internal auditor to understand and improve the design of each project is of grave importance. Translating objectives, scopes, timing and allocation of resources into a set of activities is audit’s main long term goal in order to facilitate an organization’s performance (Dascalu et al., 2016; Morrish and Sauntson, 2016).

For that reason, the internal auditor processes and evaluates available information. The data that would reach audit departments undergo analysis and are recorded to achieve the various objectives of a project. The proper communication of results to upper management levels is vital for the regularization and integration of these results into everyday business activities (Vassiliou et al., 2017; Drent, 2002).

Public organizations and the principles of modern management

For most educational systems, primary and secondary education is the first two mandatory educational stages. In these two levels of education, the division of duties, domains and responsibilities for employees and staff, present a hierarchical structure. It is a bureaucratic system that aims to ensure uniformity in the implementation of educational policies and processes. Primary and secondary education management frameworks, for both public and private sectors, pursue effective coordination and a certain degree of control by local or state monitoring organizations. Different rules or responsibilities apply depending on country or state; however, the organizational structure and function, administration, supervision and educative guidance of primary and secondary education are determined by the decisions of the state. In Greece, the Ministry of Education have a set of detailed laws and decrees that covers all aspects of the educational process (Katsaros, 2008).

The current goal of management is to implement principles of efficiency, productivity and effectiveness. To these principle’s quality and economy are interpreted as a continuous effort to optimize the organization’s production and offer of services. Operational management, recognizing complexity of activities, highlights the importance of human relationships. Also, human resources within organizations should be treated as separate social groups (Garza, 2013).

The need for administrative reform is strongly expressed by many scientific institutions and organizations. Today, outdated bureaucratic and inefficient public administration is met with cutting-edge technological developments. Furthermore, the globalization of economy brought increased requirements of students and scholars for better quality in educational services. The fast pace of life and the rapid developments disrupted by unexpected fiscal deficiencies make the need for the appliance of modern public management principles in educational organizations (Borins, 1995; Ferlie et al., 2011).

Modern public management consist of substantial administration reforms of public services. It emphasizes on effective management of human and material resources. Through modern public management, states aim to achieve quality objectives through the design, redesign and implementation of long-term strategies (Ferlie et al., 2011). Modern public management is the evolution of public administration, with a marked differentiation from current situations (Aikins, 2011; Badara and Saidin, 2012; Enofe et al., 2013).

The management of educational organizations, under the new circumstances brought substantial objective related differentiations. It incorporates elements of administrative practices that favor efficiency, flexibility, and the ability to achieve predetermined goals. Furthermore, it introduces productivity, effectiveness and better conditions of a working environment, into the public sector (Vischer, 2003). However, given the requirement for more cost-effective results, emphasis is placed on the need for more rational management of resources. In addition, risks and shortcomings become more obvious in the event of economic deficiencies such as in 2009 brought by banking crisis or in 2020 due to Corona virus. For these probabilities, the need to apply principles of modern public management is maximized (Karagiorgos et al., 2019).

According to Fanariotis (1999), “Public management as a functioning system of modern public administration and techniques, is wide and covers a great range of activities. The latter are carried out in the field of public administration, while at the same time required to bring significant results from the application of specialized methods. Aikins (2011) examined internal audit and its possible improvements in a country’s financial performance. Furthermore, public management has been successfully implemented in many EU Members State administrations. It was found that it carries the potential to achieve objectives such as enhancing efficiency and effectiveness of public services. Public management utilizes specialized practices in line with current administrative frameworks implemented in the private sector. Furthermore, it allows when possible to reconstruct public administration through radical administrative reforms aimed at efficiency and effectiveness. It is interesting that this rationalization of management, focuses on results and performance, rather that plain reconstruction of procedures (Pierre, 2012; Dascalu et al., 2016). The necessity of implementing modern public management is imperative. With administrative reforms adapted to the theoretical foundations and principles of modern operational management, the public sector is in need of a tool capable of designing and controlling the potential changes.

Implementation of internal audit in educational organizations

One of the major challenges of this study was the scarcity of available literature focused on internal audit implementation regarding educational institutes. However, internal audit has made a significant impact in various governmental activities and in the public sector (Enofe et al., 2013). Internal audit proves to be a necessary tool of modern administration in educational organizations. In order for the public sector, to provide high quality specialized services and formulate strategies for educational purposes, audit is necessary. However, the structural barriers of public administration described previously should be successfully addressed.

The inspiration for the administrative transformation of the public sector has been operational management and its success in private companies. Application of business administration principles to public sector has upgraded the level of services provided (Morrish and Sauntson, 2016). It evolved the traditional bureaucratic educational system. For example, in an Italian university, a survey by Arena (2013) argues that internal audit in higher education institutes aided in discerning certain patterns and characteristics. Prior to the latter’s research, Arena and Azzone (2007) argued that there is a limited diffusion of internal audit as well as a trend for development similar to that of the private sector. In private sector, internal audit focuses on financial auditing and compliance. It gradually broadens to operational auditing, risk management and corporate governance (Fernándezâ€Laviada, 2007; Arena et al., 2006; Spira and Page, 2003). In educational institutes, modern management should take into consideration these patterns in order to predict successfully differences in results from private sector companies (Sorros et al., 2017). Similar conclusions can be drawn from Fischer and Montondon (2005), in their research for qualifications and diversities found in the workplace. They examined cases of Higher Education institutes and found the importance of the internal audit departments as regards promoting academic goals. Farahsa and Tabrizi (2015) argue how audit can be implemented and aid educational organizations in terms of evaluating frameworks and procedures. According to Papastathis (2014), in order for internal audit to successfully fulfill its role, an organization must first reach an adequate level of managing its operations. It is understandable that for internal audit to be used as a strategy of control, it must be accepted and supported from management and staff. Thus, an approved operating regulation can be drawn and implemented.

It goes without saying that in the case of education related institutions and organizations, internal audit should be in line with the lifelong learning philosophy, training and development of its employees. As in traditional auditing, a better understanding of the organization's processes, activities and culture is good management practice. After the common understanding between audit and education has been met, the necessary resources should be secured (e.g. human resources, equipment, and infrastructure) (Morrish and Sauntson, 2016). Finally, in audit, its value is not found in controlling running costs and activities, but in the additional value given to an organization (Papastathis, 2014).

Disadvantages, weaknesses and malfunctions in the management of educational organizations

In introducing audit in educational institutes and education related organizations, certain issues can arise that could lead to inefficiency. Education could be managed by centralized decision-making, or present a large number of different administrative bodies and services (Papastathis, 2014; Sorros et al., 2017). The possibility of inefficient administrative functions, poor quality of services offered to citizens and students could present a challenging situation for audit. It is expected that when applied in education, two of audit’s goals related to i) the organizations necessity for contributions to society and ii) managing resources to be of critical importance are difficult to ignore. Furthermore, internal audit does not always achieve the desired results in the absence or inefficiency of an existing strategic plan. If the audit is self-centered or does not seek substantive examination, the auditors’ relationship with the organization under audit may hinder the expected results. It goes without saying that the unreliability of audits due to the poor quality of services and lack of support from the administration would lead to a pointless disruption of activities.

Despite its disadvantages, weaknesses or possible malfunctions, audit as part of administrative reforms in educational institutions have been satisfactory. However, as in private sector audits, an educational audit should be carefully performed, especially in events of external fiscal deficiencies and sociological pressure (Papastathis, 2014).

The study adopted a mixed method approach of qualitative and quantitative techniques. By combining quantitative and qualitative models, the research aims at a comprehensive understanding of the research problem, since the findings are based on more than one research approaches (Creswell, 2009). The aim was to develop and validate a multi-item scale to measure the proposed theoretical framework and investigate the causal relationships between empirically tested theoretical constructs (Churchill, 1979; Hinkin, 1995; DeVellis, 2003).

The first stage of scale construction includes the item generation process and the scale purification. In the second and main stage, stratified random sampling was used in selecting respondents and to distribute web-based questionnaires. In scale validation, initially exploratory and then confirmatory analysis was employed to identify the factor structure of the measurement items (construct validity). The last stage proposes a conceptual model which depicts the theoretical causal relationships among variables and the derived hypothesis. Statistical procedures and analysis were conducted with the use of SPSS.

Deductive item generation for the questionnaire

In this study, the items generation is driven by the deductive approach to analyze and organize information and data. Template thematic analysis was used to systematically identify, organize, and offer an insight into patterns across a data set. Template analysis balances a relatively high degree of structure in the process of analyzing textual data with the flexibility to adapt it to needs of a particular study (Braun and Clark, 2012). It is widely used for interview transcripts (King, 2012).

For generating the items, the first step was to create a pool of items that would characterize the theoretical constructs. Items can be drawn either inductively (eg. interviews, focus groups) due to lack of available theories or deductively based on literature review and on existing instruments (Hinkin, 1995).

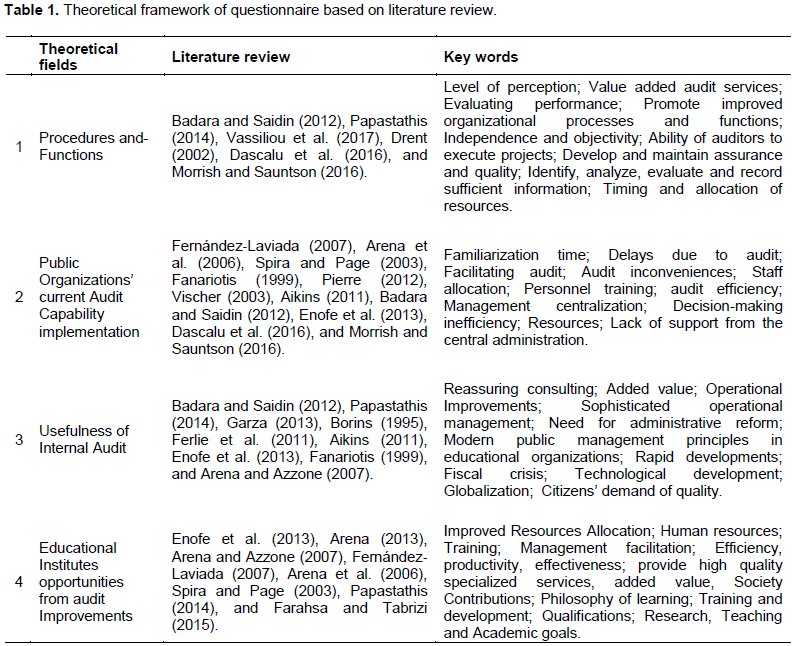

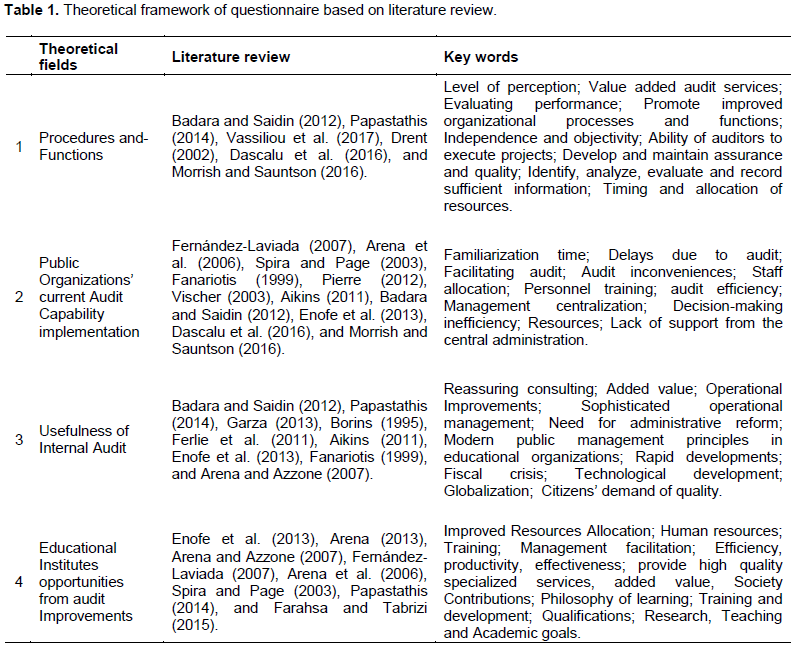

The absence of pre-existing validated instruments about the audit in educational institutes directed the researchers toward available theoretical frameworks related to audit, public organizations and educational efficiency. At this point, a sample of 40 items was created reflecting four theoretical constructs derived from literature. The second step involved the effort to refine the theoretical constructs through semi-structured interviews from 9 experts in the field (Heads of accounting departments; Accounting or audit scholars, Auditors). The process of interviewing was based on Minichiello et al. (1995) combining the “funnel” and “story telling” methods. The interviews were guided by a list of 10 prepared questions that adhered to the themes of the identified theoretical constructs. In order to analyze information from the interviews, a template of themes and codes (conceptual labels) was prepared. The data collected from interviews combined with the information gathered from literature, was used in constructing a list of 35 measurement items which is assumed to represent a sound proxy of the four theoretical constructs depicted in Table 1.

To establish item validity, the developed questionnaire was subject to expert assessments. Five experts from high education institutes and audit organizations assessed the relevance of the items to the theoretical constructs and provided suggestions on comprehension, clarity and simplicity. Their remarks contributed to the purification of the items and resulted in a set of 32 items measured on a five-point scale (1= “strongly disagree”; 5= “strongly agree”).

Sampling and questionnaire composition

The target population was administrators, educators and executives who hold positions of responsibility in public educational monitoring services (N= 2.381). The survey’s sample frame was made up of the 500 educational personnel. Α proportionate stratified random sample procedure was used according to the type of employee. An invitation e-mail was sent to the 500 educational organizations with a direct link to the web-based questionnaire. A consent form and information was included stating the reasons and goals of this research. After two e-email reminders to non-responders, a total of 199 completed questionnaires was returned (39.8% response rate) which was deemed adequate. Educational systems may differ regarding countries. However, educational and audit standards demonstrate great similarities regarding their control procedures.

The questionnaire was divided into 5 sections. Four sections depicted the theoretical model and the 32 items while the last section contains six demographic questions. The analysis of the findings was based on the "inferential logic for discovering and confirming a set of probabilistic causal laws, for predicting general patterns of human activity" (Neuman, 2003).

Scale validation

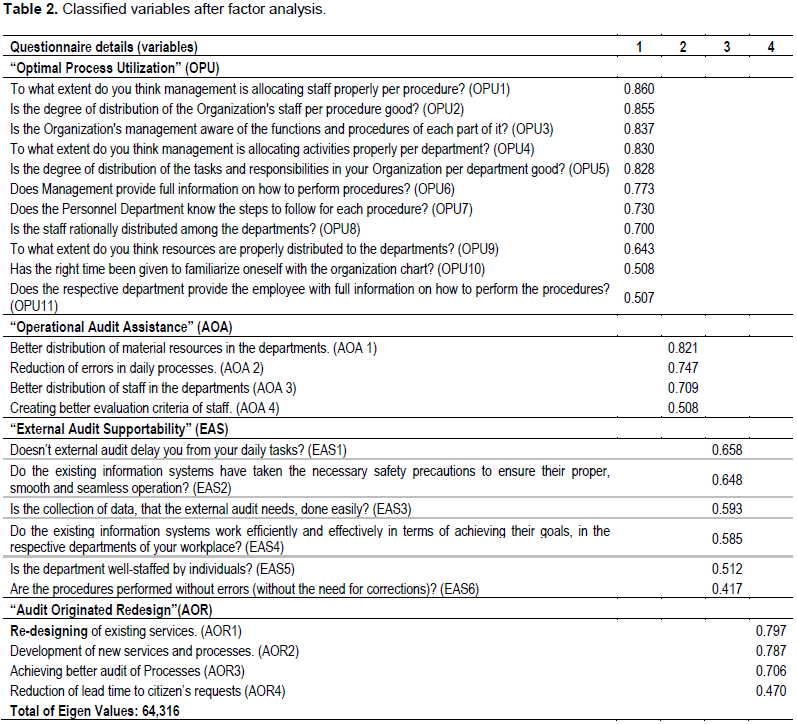

Investigative factor analysis (IFA) was used to determine the latent structure of the data set. Pearson product- moment correlation coefficients were estimated to detect uncorrelated items. Twenty five items exhibited correlations above 0.40 and were deemed acceptable for further analysis. Seven (7) items of the questionnaire were excluded from the factors as they did not show factor loadings with values ​​above 0.4.

The principal factor analysis with varimax rotation suggested 4 factors (with eigen values >1) which explained 64.31% of the total variance. The chosen items (variables) retained in the factors since their loadings were found to be greater or equal to 0.4 (Hair et al., 1998). An inspection of the scree plot also maintained a four-factor structure. Table 2 contains the items of the four factors, their loadings and the associated statistics of factor analysis.

After identification of the factors, the items that they are composed of aided the labeling process. Eleven items formed the first factor related to the “Optimal Process Utilization” (OPU) that explains the organizations’ ability to distribute its resources or facilitate its procedure. Generally, the factor measures the current managerial and operational capability of an organization. It demonstrated the successful allocation of different resources in the various departments and activities. It is the ability of organization to use efficiently and perform its basic and everyday operations.

The second factor was named “Audit’s Operational Assistance” (AOA) in order to measure the part audit plays in the organization. This four-item factor explains how audit can help improve management reduction of errors in its everyday activities, allocate resources efficiently and properly evaluate employees. The third factor was formed by six items. It was named “External Audit Supportability” (EAS) and explains external audit’s ability to locate problematic areas and issues within the organization without hindrances to the everyday activities and performance. The last factor, "Audit Originated Redesign" (AOR) was formed by four items, measuring necessary and possible implementations. These changes may refer to existing activities or the redesign of services. It explains the effort the organization puts to improve quality of work and the services offered.

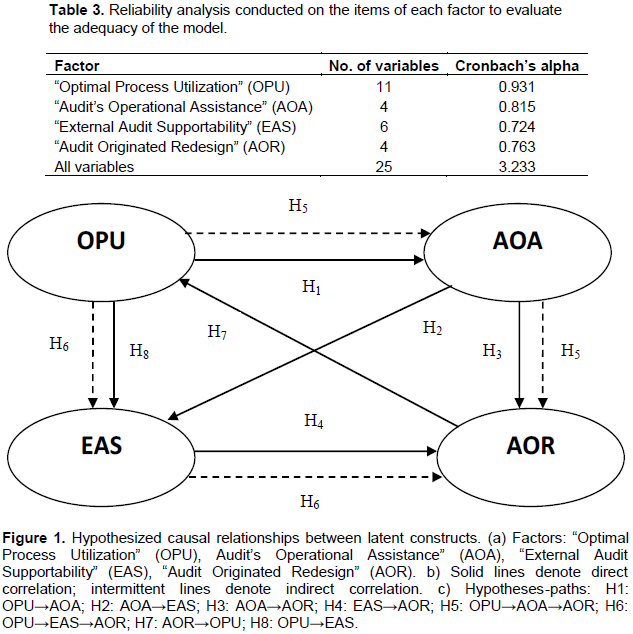

All individual items loaded onto their identified latent variables had significant (p<0.01) regression weights. Moreover, the estimated values of the employed goodness-of-fit indices indicated that the data provided a good fit to the model. To further evaluate the adequacy of the model, a reliability analysis was conducted on the items of each factor. Cronbach’s alpha coefficients for the four factors were found to be above the recommended standard value of 0.70 (Hair et al., 1998) as seen in Table 3.

Following literature and interviews, a theoretical model is specified. Figure 1 depicts the proposed model, which describes the relationships among the theoretical concepts derived from the questionnaire. The model posits that the external and internal audit will impact optimization. It is expected that three independent variables may interact with each other. Consequently, it is left to the regression analysis to investigate and capture pathways among the three variables.

Conceptual model and research hypothesis

Based on the results of the conceptual reasoning, the interviews and literature review of a conceptual model was created that proposed hypothesized relationships, through its latent variables. The model was conceptualized so that the External Audit Supportability, Audit Operational Assistance and External Audit Supportability would work as predictors of the Optimal Process Utilization. Figure 1 demonstrates the conceptual model with the associated hypothesized causal relationships.

The first hypothesized relationship (H1) was that “Optimal Process Utilization” (OPU) would directly affect “Audit’s Operational Assistance” (AOA). The hypothesis was based on the facilitation of internal audits offered by an optimized or properly organized set of activities within an organization.

Thereafter, the model hypothesizes (H2) that AOA should also demonstrate a direct relationship and affect “External Audit Supportability” (EAS), since the ability of an internal audit’s department can significantly facilitate procedures and investigations performed by external auditors.

The third hypothesis (H3) states that AOA should also have a similar and direct relationship with “Audit Originated Redesign” (AOR). Similarly, it is expected for EAS to also affect directly AOR (H4). However, by using EAS and AOA as mediators, OPU could also indirectly affect AOR through these two paths (H5 and Η6). The latter two hypotheses are based on literature’s solid expectations that an audit department (either external or internal) consults an organization regarding its decision making. Furthermore, audit offers possible redesigns of procedures in order to increase effectiveness and discern added value activities.

The fifth Hypothesis (H7) involved the expected relationship between AOR and OPU, since suggested redesigns and improvements offered by auditors should aim into the organization’s optimization of processes and activities.

The last Hypothesis (H8) was a possible relationship between OPU affecting EAS in order to cover the possibility of an organization lacking an autonomous internal auditing department. This relationship explains the possible results of an interaction between an organization and an external auditor as the sole audit mechanism. Figure 1 depicts the proposed conceptual model with the associated hypothesized causal relation-ships among variables. The five hypotheses deriving from the conceptual model are listed semantically below:

Η1: “Optimal Process Utilization” (OPU) directly affects “Audit’s Operational Assistance” (AOA); Η1: OPU→AOA.

H2: “Audit’s Operational Assistance” (AOA) directly affects “External Audit Supportability” (EAS); H2: ΑΟΑ→EAS.

H3: “Audit’s Operational Assistance” (AOA) directly affects “Audit Originated Redesign” (AOR); H3: AOA→AOR.

H4: “External Audit Supportability” (EAS) directly affects “Audit Originated Redesign” (AOR); H4: EAS→AOR.

H5: “Optimal Process Utilization” (OPU) indirectly affects “Audit Originated Redesign” (AOR) through “Audit’s Operational Assistance” (AOA); H5: OPU→AOA→AOR. H6: “Optimal Process Utilization” (OPU) indirectly affects “Audit Originated Redesign” (AOR) through “External Audit Supportability” (EAS); H6: OPU→EAS→AOR.

H7: “Audit Originated Redesign” (AOR) directly affects Optimal Process Utilization” (OPU); H7: AOR→OPU.

H8: “Optimal Process Utilization” (OPU) directly affects “External Audit Supportability” (EAS); H8: OPU→EAS.

Validation of the conceptual model

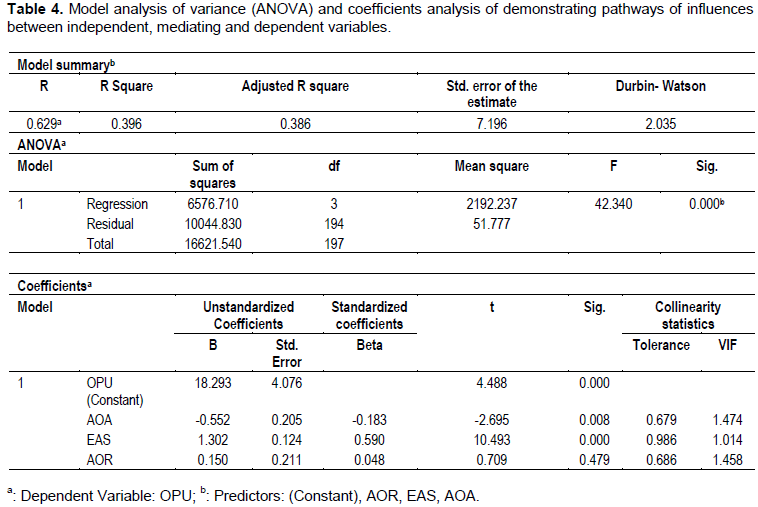

Having obtained a factors’ solution for the observed data, a regression analysis was employed to ensure the relationship between the dependent variable (OPU) and the three independent variables (AOA, EAS, AOR). In this case, the multiple regression function takes the following form:

Yi = α + β1 * Χ1 + β2 * Χ2 +……..+ βv * Χi

The correlation coefficient R2 shows the percentage of variance of the dependent variable explained by the independent variables. The model explains 39.6% of the total variability.

The value of adjusted R2 shows that the model can be generalized to the population. It is concluded that 38.6% of the variance of the OPU variable is explained by the independent variables. The value of Durbin-Watson is close to 2, so the errors are independent.

According to Table 4, the Analysis of Variance (ANOVA) gave an F-test with a value of 42.34, so the model is statistically highly significant, at the level of statistical significance α = 0.001. Based on the table of factors, the regression equation of the model is:

OPU = 18.293 – 0.552*AOA + 1.302*EAS + 0.150*AOR

The regression explains that when the AOA value increases by one unit, the OPU value will decrease by 0.552, whereas when the EAS and AOR values increase by one unit, the OPU value will increase by 1.302 and 0.150 respectively. The value of t indicates that EAS is the most important factor in the model, while the other two factors (AOA and AOR) are less important. It also appears that the tolerance values do not approach the value 0 and therefore there is no problem of multicollinearity in the model. This fact is also confirmed by the value of VIF, which in all cases is less than 10. Finally, from the normal probability plot, it appears that the distribution of residues is normal since the points are concentrated around the 45° line. Overall, the fit of the model to the data can be considered satisfactory.

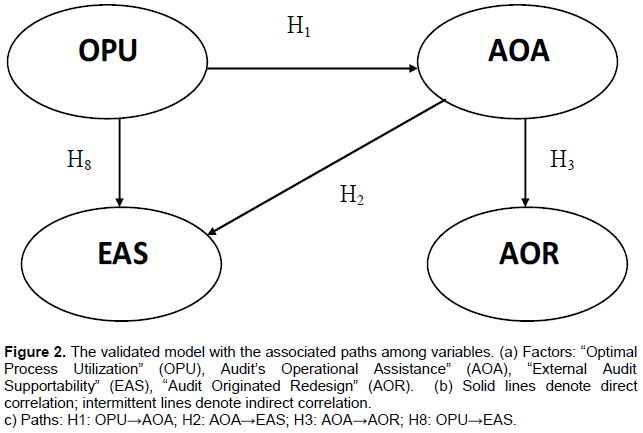

The results show that the proposed direct relationship between OPU and AOA is negative and significant, thus supporting hypothesis H1. On the other hand, OPU has a significant positive effect on EAS (H8). The path coefficients showing the influence of EAS to AOR and AOR to OPU were not significant (p>0.05) and therefore deleted from the model; as a result, hypotheses H4 and H7 are not supported. Furthermore, an indirect effect of OPU to AOR through AOA and EAS was not supported by results, thus H5 and H6 were not validated by the model. AOA has a significant positive impact on AOR (H3), and a significant but opposing effect on EAS (H2).

Furthermore, the supported hypotheses and the relationships between the factors deriving from the validated model are shown in Figure 2 and listed semantically below:

Η1: “Optimal Process Utilization” (OPU) has a direct negative effect on Audit’s Operational Assistance” (AOA); (EAS); Η1: OPU→AOA.

H2: “Audit’s Operational Assistance” (AOA) has a direct opposing effect on “External Audit Supportability” (EAS); H2: ΑΟΑ→EAS.

H3: “Audit’s Operational Assistance” (AOA) directly affects “Audit Originated Redesign” (AOR); H3: AOA→AOR.

H8: “Optimal Process Utilization” (OPU) directly and positively affects “External Audit Supportability” (EAS); H8: OPU→EAS.

Some correlations between factors normally interpreted by literature were not found significant. The hypotheses related to these paths cannot be supported. Education is a field of interesting exemptions regarding the appliance of traditional management principles. Administrations for both educational institutions and monitoring organizations require quality and careful planning of procedures (Morrish and Sauntson, 2016). It is understood that auditing should likewise be applied to educational subjects with caution. Primarily, the results and procedures of an audit should be provided with the aim of promoting educational purposes (Dascalu et al., 2016; Morrish and Sauntson, 2016). On the one hand, institutions manage a valuable intangible asset and ensure the quality of education's transmission to students. On the other hand, indiscriminate audits and hasty changes in procedures can disrupt the quality of education offered (Papastathis, 2014). Unlike industrial sectors or other markets, results of miscalculated strategies in education are difficult to trace and evaluate, before a reasonable period of time.

The present research uses education in the light of educational organizations' supervisory bodies. It is therefore understood that the public sector and the peculiarities that distinguish it must be taken into account in the implementation of audit as an optimization tool. For this type of organizations, competitiveness and profitability are not immediate goals (Sorros et al., 2017). Thus, the same swiftness and procedures used in the private sector should not be used as measures of comparison.

The importance of this research is decided in its research hypotheses. The absence of estimated correlations of factors from four hypotheses can be traced as part of the specificity of the public sector. At the same time, education's specific features can differentiate normalcy, when applying audit mechanisms.

Initially, the fourth hypothesis (H4) concerned the processes and activities of an organization. It was expected that they should comply with external audits that eventually would lead to redesigns. On the contrary, redesign seems to be directly affected only by those procedures performed by the organization to support the subsequent audit. In fact, there is difficulty in distinguishing between external and internal audit in the answers of the respondents. The latter is explained as external audits of educational and monitoring organizations are executed by the public body to which they are subject. The state from time to time appears not as an external auditor but as a higher administrative stage of the same organization. At the same time, the audit does not seem to be cathartic or bring about significant redesigns.

The latter can be confirmed by the first hypothesis (H1), where "Optimal Process Utilization" (OPU) directly affects "Audit’s Operational Assistance" (AOA), which proved to be true. Nevertheless, the effect was negative. So in public education support organizations, audit related procedures are abandoned when an organization’s activities are optimal. Therefore, there is a high possibility audit is used as a provisional practice. At the same time, audit seems to propose redesigns only when the organization can support an audit.

The third hypothesis (H3) is where “Audit’s Operational Assistance” (AOA) directly affects “Audit Originated Redesign” (AOR). Given that the education monitoring organizations belong to the public sector, it is the state that has to decide on reorganization. Practically, the usefulness of audit can be found where the state allows it and when the quality of procedures has been significantly reduced. At the same time, the second hypothesis (H2) states that "Audit's Operational Assistance" (AOA) has a direct and opposing effect on "External Audit Supportability" (EAS). This confirms the above conclusions. External audit performed to educational and educational-monitoring institutions remains as a part of the general public sector's performance

Nevertheless, external audit seems to be positively affected by the optimization of operations and procedures. This is implied in H8 where, “Optimal Process Utilization” (OPU) directly and positively affects “External Audit Supportability” (EAS). So the increase in functionality of an organization increases its ability to support an external audit. This assumption is logical and expected. Nevertheless, questions arise as to the timing and criteria on the basis of which the external audit is decided. At the same time, more questions are raised as to whether the external audit works as a correction or mainly as a confirmatory tool for the already sufficient functionality of organizations. These questions intensify since the expected correlation of the proposed redesign of processes from audit and its assistance in process optimization has not been confirmed.

From this research it is understood that audit in education is deemed important by both state and educational institutions. Through the audit procedures, educational organizations strive to optimize their services. Nevertheless, data supports that audit be used partially, since it has little influence on the reorganization and optimization of operations. The first interesting finding of this research is that educational monitoring organizations consider the state as an external auditor. The factor measuring external auditing was found to be great. The second interesting finding concerns achieved process optimization and its effect on external audit. It is understood that public organizations that monitor education systems do not use audit proactively. Rather audits are performed after certain procedures have already been redesigned to a sufficient level. Namely, the reorganization of the departments and activities seems to originate from the support work the organizations have to do before and for the audit. It is possible that organizations and employees want to show good results in auditing. However, it seems that audit itself does not affect the procedures. It is an important tool for optimizing processes as a means of stimulation. This increases the likelihood that the healing properties of audit will not be fully utilized. This is despite the importance of audit given by both employees and organizations, as well as by the respective state.

This paper shows a very interesting aspect of the public sector and its differences in approach to audit. The existence of pre-audit preparations to aid the procedure is normal and expected. However, it was not expected that the reorganization would occur to such an extent from pre-audit support processes performed by the organization. This raises important questions about the philosophy of audit in the public sector as well as the educational organizations it oversees.

Existing literature was scarce as far as audit in educational institutions and educational monitoring organizations are concerned. For this reason, the opinion of audit experts from both the public and private sectors was vital. The questionnaire as a tool is expected to contain some elements of subjectivity. While finally, on researching an area with many peculiarities and a wide range of responsibilities, such as education, it is expected to yield results that need further analysis.

At a later time, from the questions raised in the conclusions about the time chosen and decisions of initiating an audit, new research is likely to emerge. In case external private sector auditors were used, which would be the factors and issues raised, it is evident that such decisions should be made with assurance that private external auditors have taken into account the objectives of an educational institution. Finally, the audit-public sector's relationship found in education could be transferred to other similar organizations or different levels of public administration.

The authors have not declared any conflict of interests.

REFERENCES

|

Aikins S (2011). An examination of government internal audits' role in improving financial performance. Public Finance and Management 11(4):306-337.

|

|

|

|

Arena M (2013). Internal audit in Italian universities: An empirical study. Procedia-Social and Behavioral Sciences 93:2000-2005.

Crossref

|

|

|

|

|

Arena M, Arnaboldi M, Azzone G (2006). Internal audit in Italian organizations. Managerial Auditing Journal 21(3-2006):275-292.

Crossref

|

|

|

|

|

Arena M, Azzone G (2007). Internal audit departments: adoption and characteristics in Italian companies. International Journal of Auditing 11(2):91-114.

Crossref

|

|

|

|

|

Badara MAS, Saidin SZ (2012). Improving the existing functions of internal audit at organizational level. International Journal of Arts and Commerce 1(6):36-46.

|

|

|

|

|

Braun V, Clark V (2012). Thematic analysis. In H. Cooper (Ed.), APA Handbook of Research Methods in Psychology: Vol. 2. Research Designs (57-71). Washington, DC: American Psychological Association.

Crossref

|

|

|

|

|

Borins S (1995). The New Public Management is here to stay. Canadian Public Administration 38(1):122-132.

Crossref

|

|

|

|

|

Churchill GA (1979). A paradigm for developing better measures of marketing constructs. Journal of Marketing Research 16:64-73.

Crossref

|

|

|

|

|

Creswell W John (2009). Mapping the Field of Mixed Methods Research 3(2):95-108.

Crossref

|

|

|

|

|

Dascalu ED, Marcu N, Hurjui I (2016). Performance management and monitoring of internal audit for the public sector in Romania. Amfiteatru Economic Journal 18(43):691-705.

|

|

|

|

|

Drent D (2002). The quest for increased relevance: Internal auditors who successfully communicate and balance their needs and those of their clients can increase their relevance to the organization. Internal Auditor 59(1):49-54.

|

|

|

|

|

DeVellis RF (2003). Scale Development Theory and Applications 2nd ed. Thousand Oaks, CA: Sage.

|

|

|

|

|

Drogalas G, Apostolakis A, Karagiorgos A, Garyfalakis A (2020). Evaluation of the contribution of Internal Audit Mechanisms in the Departments of Tourism of the Thirteen Districts of Greece, Interdisciplinary Journal of Economics and Business Law 9(1):115-139.

|

|

|

|

|

Enofe AO, Mgbame CJ, Osa-Erhabor VE, Ehiorobo AJ (2013). The role of internal audit in effective management in public sector. Research Journal of Finance and Accounting 4(6).

|

|

|

|

|

Fanariotis P (1999). Public Administration: Decentralisation and Self-Governance, Stamoulis Publishing (in Greek), Athens.

|

|

|

|

|

Farahsa S, Tabrizi JS (2015). How evaluation and audit is implemented in educational organizations? A systematic review. Research and Development in Medical Education 4(1):3-16.

Crossref

|

|

|

|

|

Fernándezâ€Laviada A (2007). Internal audit function role in operational risk management. Journal of Financial Regulation and Compliance 15(2):143-155.

Crossref

|

|

|

|

|

Ferlie E, Lynn L, Pollitt C (2011). The Oxford Handbook of Public Management New York: Oxford University Press pp. 33-76.

|

|

|

|

|

Fischer M, Montondon L (2005). Qualifications, Diversity and workplace practices: An Investigation of Higher Education Internal Audit Departments. Journal of Public Budgeting, Accounting and Financial Management 17(4):488-522.

|

|

|

|

|

Garza FA (2013). A framework for strategic sustainability in organizations: A three pronged approach. Journal of Comparative International Management 16(1):23-36.

|

|

|

|

|

Hinkin T (1995). A Review of Scale Development Practices in the Study of Organizations. Journal of management 1(5):967-988.

Crossref

|

|

|

|

|

Karagiorgos A, Stamatis S, Plioska P, Koutri O (2019). Audit in the service of revenue increase: A tool for boards and committees of local authorities. Corporate Board: Role, Duties and Composition 15(2):8-17.

Crossref

|

|

|

|

|

Katsaros I (2008). Organization and Management of Education. Ministry of Education, Institute of Education, Athens.

|

|

|

|

|

King N (2012). Doing Template Analysis. In Symon G, Cassel G (eds), Qualitative Organizational Research, Core Methods and Current Challenges, Sage pp.426-50.

Crossref

|

|

|

|

|

Minichiello V, Aroni R, Timwell E, Alexander L (1995). Interview Processes. In: In-Depth Interviewing 2nd ed, Chapter 5, Melbourne: Longman.

|

|

|

|

|

Morrish L, Sauntson H (2016). Performance management and the stifling of academic freedom and knowledge production. Journal of Historical Sociology 29(1):42-64.

Crossref

|

|

|

|

|

Neuman SB (2003). From rhetoric to reality: The case for high-quality compensatory prekindergarten programs. Phi Delta Kappan 85(4):286-291.

Crossref

|

|

|

|

|

Papastathis P (2014). Modern Internal Audit and its Practical Implementation, Printfair Publications, Athens.

|

|

|

|

|

Pierre J (2012). The SAGE Handbook of Public Administration, London: Sage Publications pp. 17-32.

|

|

|

|

|

Spira LF, Page M (2003). Risk management: the reinvention of internal control and the changing role of internal audit. Accounting, Auditing and Accountability Journal 16:640-661.

Crossref

|

|

|

|

|

Sorros J, Karagiorgos A, Mpelesis N (2017). Adoption of Activity-Based Costing: A Survey of the Education Sector of Greece. International Advances in Economic Research 23(3):309-320.

Crossref

|

|

|

|

|

Vassiliou D, Heriotis N, Menexiadis M, Balios D (2017) Internal Audit for Businesses and Organizations, Rosili publications, Athens.

|

|

|

|

|

Vischer JC (2003). Designing the work environment for worker health and productivity. In Proceedings of the 3rd international conference on design and health pp. 85-93.

|

|