Full Length Research Paper

ABSTRACT

Studies on economic growth have provided insights into why states grow at different rates over time. Most recently, endogenous growth economics asserts that government expenditure and taxation will have both temporary and permanent effects on economic growth. The debate on the effectiveness of taxes as a tool for promoting growth and development remains inconclusive. Against this background, this study sought to determine the effect of distortionary and non-distortionary taxes on the economic growth of sub-Saharan African countries. The ex-post facto research design was adopted which enabled the study to make use of secondary data of sub-Saharan African countries in a panel least squares. The hypotheses were linearly modelled while adopting the panel data estimation under the fixed-effect assumptions. Findings reveal that distortionary tax (a proportional tax on output at rate) has a negative and insignificant effect while non-distortionary tax has a positive and insignificant effect on the economic growth of sub-Saharan African countries. Given the positive but insignificant effect of non-distortionary taxes on economic growth, the study thus recommends that Governments of sub-Saharan African countries should improve on the mechanisms for the collection of non-distortionary taxes while deemphasizing the use of distortionary taxes for enhanced economic growth in the economies.

Key words: Distortionary taxes, non-distortionary taxes, economic growth rate, endogenous growth model, sub-Saharan Africa.

INTRODUCTION

The extent to which tax policies engender economic growth has continued to attract empirical debate especially in developing countries. Taxation is a tool by government in fashioning various aspects of economic growth. According to Tosun and Abizadeh (2005) taxes are instrument of fiscal policy. They outlined five possible mechanisms by which taxes can affect economic growth. First, taxes can inhibit investment rate through such taxes as corporate and personal income, capital gains taxes. Second, taxes can slow down growth in labour supply by distorting labour-leisure choice in favour of leisure. Third, tax policy can affect productivity growth through its discouraging effect on research and development expenditures. Fourth, in a Harbenger framework, taxes can lead to a flow of resources to other sectors that may have lower productivity. Finally, high taxes on labour supply can distort the efficient use of human capital high tax burdens even though they have high social productivity.

Engen and Skinner (1996) suggest that a number of recent theoretical studies have used endogenous growth models to stimulate the effects of a fundamental tax reform on economic growth. All of these studies conclude that reducing the distorting effects of the current tax structure would permanently increase growth. Anyanwu (1997) opines that in practice, it is difficult to distinguish between the effects of tax policy on levels and on growth rates of GDP. This is because transitional growth may be long-lasting and so it has not proved possible to distinguish effects on long-run growth from transitional growth. For instance, it is possible that tax changes that encourage innovation and entrepreneurship may have persistent long-run growth effects, while those that affect investment also can have long lasting effects on growth that fade out in the long run.

Non-distortionary taxes (taxes that do not affect the private sector’s incentive to invest in the input good, this reflects indirect taxation) do not affect the private sector’s incentive to invest in the input good, whereas the distortionary (direct taxation on property and income) taxes on output do. Governments of western African countries are grappling seriously with the bureaucratic management of fiscal policy especially in the area of distortionary and non-distortionary taxes which may have the incentive of negating peoples’ attitude towards working and paying higher taxes while affecting private sector’s incentive to invest in input goods. This study sets to determine if distortionary and non-distortionary taxes negatively and significantly affect the economic growth of sub-Saharan African Countries. Basically, thus study seeks answers to the extent in which distortionary and non- distortionary taxes affect the economic growth of sub-Saharan African countries. The study thus hypo-thesized that distortionary and non-distortionary taxes does not have a positive and significant effect on the economic growth of sub-Saharan African countries.

Given that the United Nations subdivided the African continent into five regions of Eastern Africa, Middle Africa, Northern Africa, Southern Africa, and Western Africa, this study in terms of geographical location was limited to countries of sub-Saharan Africa with agriculture based on cash crops for exports. The scope is also determined by the availability of data for the countries of sub-Saharan Africa. Countries involved in the study include: Benin, Botswana, Burkina Faso, Burundi, Cameroun, Cape Verde, Central African Republic, Liberia, Kenya, Equatorial Guinea, Lesotho, Madagascar, Malawi Namibia, Nigeria, Seychelles, Sierra Leone, and South Africa. In terms of time, the annual dataset for this study covered sub-Saharan Africa countries and for various periods during 1990-2011, from two sources IMF World Economic outlook and World Bank databank. Following this introduction is the review of related literature followed by methodological framework, findings and discussion as well as the conclusion.

REVIEW OF RELATED LITERATURE

The theoretical framework

The theoretical underpinning for this study is basically the endogenous growth theory. The endogenous growth theory advocates the stimulation of level and growth rate of per capita output through within the economic policies such as tax policies. The endogenous growth theory posits that the driver of economic growth is fundamentally the result of endogenous factors and not external factors (Roma, 1994). The endogenous growth theory posits that the growth of the economy in the long run primarily depends on policy measures which have grave implications on openness, competition, change and innovation (Fadera, 2010). The endogenous growth theory further argues that economic growth is generated from within a system as a direct result of internal workings of the system. Specifically, the theory notes that the enhancement of a nation's human capital will lead to economic growth by means of the development of new forms of technology and efficient and effective means of production which are not disrupted by taxes. Supporters of endogenous growth theory argue that the productivity and economies of today's industrialized countries compared to the same countries in pre-industrialized eras are evidence that growth was created and sustained from within the economy.

Since the mid-1980s the theoretical growth literature has above all tried to endogenize the growth rate of output in the long-run. As is well known, in the neoclassical growth model, if the incentives to save or to invest in new capital are affected by fiscal policy, this alters the equilibrium capital output ratio, and therefore the level of the output path, but not its slope (with transitional effects on growth as the economy moves onto its new path). The novel feature of the public-policy endogenous growth models of Barro (1990) and Barro and Sala-i-Martin (1992, 1995) is that fiscal policy (tax policy) can determine both the level of the output path and the steady-state growth rate. Endogenous growth theory pioneered by the work of Romer (1986), Barro (1990) among others, points out mechanisms by which policy variables cannot only affect the level of output, but also steady-state growth rates. Barro (1990) constitutes one of the first attempts at endogenizing the relationship between growth and fiscal policies. He distinguishes four categories of public finances: productive vs. non-productive expenditures and distortionary vs. non-distortionary taxation. Taxation is distortionary if it affects the investment decision, and hence output/growth. This is, above all, the case for direct income and profit taxation. Otherwise taxes, such as consumption taxes, are considered non-distortionary, except for the case when households face the endogenous choice of labour or leisure.

Empirical review

In general, studies of taxation using cross-country data suggest that higher taxes have a negative impact on output growth, although these results are not always robust to the tax measure used. Using reduced-form cross-section regressions, Koester and Kormendi (1989) estimated that the marginal tax rate—conditional on fixed average tax rates—has an independent, negative effect on output growth rates. Toshihiro (2001) investigated the effect of wealth taxation on economic growth using an endogenous growth model with the altruistic bequest motive while introducing intra-generational productivity differentials of human capital formation, resulting in differences of growth rates among individuals. Dividing the economy into two groups; those who leave bequests to physical capital investment and those who leave bequests to human capital investment, (Toshihiro, 2001) found that an increase in taxes on life cycle savings will reduce the intra-generational growth differences, while the effect of taxation on bequests, wage income, or consumption on intra-generational growth differences is ambiguous. Easterly and Rebelo (1993) described the empirical regularities relating fiscal policy variables, the level of development, and the rate of growth. Easterly and Rebelo (1993) employed historical data, recent cross-section data, and newly constructed public investment series on fiscal policy variables and the rate of growth and found it difficult to empirically isolate the effects of taxation on the rate of growth.

For studies using non-African level data, Pecorino (1994) noted that should the US have moved away from income taxes towards consumption taxes, economic growth could have increased significantly from an average of 1.53 to 2.56% per annum. Kim (1998) analysis shows that 35.0% of the differences between US and Korean economic growth can be explained by differences in the tax structure between the two countries in a comparison of economic growth and taxation. Dowrick (1992) also found a strong negative effect of personal income taxation, but no impact of corporate taxes, on output growth in a sample of Organization for Economic Co-operation and Development (OECD) countries between 1960 and 1985. Easterly and Rebelo (1993) found some measures of the tax distortion (such as an imputed measure of marginal tax rates) to be correlated negatively with output growth, although other measures of the tax distortion were insignificant in the growth equations. Using cross country data for 1970–85, Engen and Skinner (1996) found that an increase of 2.5 percentage points in the average tax burden (total taxes divided by GDP) is predicted to reduce long-term output growth rates by 0.18 percentage points, holding constant the supply of investment and labor. Wang and Yip (1992) in Chiumia and Simwaka (2012) while showing that the proportion in which taxes are collected is more important than the level of taxation in explaining economic growth in Taiwan from 1954 to 1986 empirically found negative impacts of specific taxes on economic growth and the effect of total taxation is not significant. Also, Stokey and Robelo (1995) in Chiumia and Simwaka (2012) found insignificant negative effects of taxation on economic growth employing the endogenous growth for developed economies. Lovell and Branson (2001) in Chiumia and Simwaka (2012) combined the use of data envelope analysis and a log quadratic equation to examine the impact of tax burden and tax mix on economic growth in New Zealand during the period of 1946 to 1995. Lovell and Branson (2001) noted that the tax burden in New Zealand had trended upwards from 23.0 to 35.0% and the ratio of direct taxes to indirect taxes had varied between 0.31 and 0.75 and these negatively affect economic growth in New Zealand.

For studies using African level data, Keho (2010) while arguing that a common limitation to most empirical studies is basically the adoption of linear models which fail to account for the nonlinearity in the tax-growth relationship applied a nonlinear estimation techniques to estimate optimal tax structure for Cote d Ivoire and found tax structure to have significant impact on growth. Marsden (1990) found that the low tax regimes grew at an average of 7.3% while the high tax group only averaged 1.1% in a group of less developed countries in Africa classified into high and low tax regimes. Koch et al. (2005) used data from 1960 to 2002 and a two-stage modeling technique to control for unobservable business cycle variables presented evidence about tax distortions in South Africa and found that decreased tax burdens are strongly associated with increased economic growth while decreased indirect taxation is strongly correlated with increased economic growth potential. Chiumia and Simwaka (2012), using data envelope analysis (DEA) and transcendental logarithm (Translog), examined the impact of tax policy and donor inflows on economic growth in Malawi from 1970 to 2010 and found that a 1.0% decrease in tax burden can raise economic growth by 0.8% in Malawi while a similar reduction in collection of taxes through expenditure can raise growth by 0.6%. Chiumia and Simwaka (2012) therefore note that reduction in tax burden is more potent in influencing economic growth than fine tuning the proportion in which income and consumption taxes are collected in Malawi. Chigbu et al. (2012) examined the causality between economic growth and taxation in Nigeria for the period 1970-2009 and concluded that taxation is a very important instrument of fiscal policy that contributes to economic growth of any country. Skinner (1988) used data from African countries to conclude that income, corporate, and import taxation led to greater reductions in output growth than average export and sales taxation.

Glaringly, the empirical literature search studies adopted variables including marginal tax rate, tax mix, tax regimes, tax burden etc and thus failed to turn up studies that have adopted the endogenous growth model while classifying taxes into distortionary and non-distortionary taxes in line with the recent approach of pairwise combination of variables in line with tax-growth studies. This is the gap this study fills.

METHODOLOGICAL FRAMEWORK

Research design, data issues and sampling concerns

This study is designed to structurally ascertain the effect of tax policy variables on economic growth in sub-Saharan Africa and thus adopted an ex-post facto research design. This implies that the event investigated had already taken place; therefore, the data used are already in existence. The adoption of this research design is based on the fact that the study relied on historic data obtained from relevant publications and as such the data already are in existence. In this study an attempt was made to account for the endogenous tax policy variables that affect economic growth in sub-Saharan Africa.

In line with the approach adopted by Mathew (2009), Bleany et al. (2000) and Fu et al. (2003) in their works on fiscal policy and economic growth using various inter-country data, this research made use of handpicked data from the International Monetary Fund (IMF) and World Bank Data websites. This is because the data are ideal in answering our research questions and to empirically test our research hypotheses in order to achieve the objectives of the study. The theoretical model requires the classification of taxation into distortionary and non-distortionary. We thus classified consumption taxes (VAT) as non-distortionary since consumption taxes do not distort the choice between consumption at different times and are less distortionary than income taxes, while classifying income taxes as distortionary taxes. Our annual dataset covered sub-Saharan African countries for various periods during 1990-2012 from two sources. Government budget data were gathered from the IMF Government Finance Statistics Yearbook (GFSY); remaining data were gathered from the World Bank databank. While it could not be technically possible at least within the context of this study to consider all African countries, it was considered ideal to use a sample. The use of a sample became imperative also to ensure availability of a reasonable dataset. This study in terms of sampling is geared towards a geographical location and limited to a selected countries in the sub-Saharan Africa. This is because of the peculiar characteristics of the sub-Saharan African countries including its location, with agriculture based on cash crops for exports. The sub-Saharan African countries studied include: Benin Republic, Botswana, Burkina Faso, Burundi, Cameroun, Cape Verde, Central African Republic, Equatorial Guinea, Liberia, Kenya, Lesotho, Madagascar, Malawi, Namibia, Nigeria, Seychelles, Sierra Leone, and South Africa. There we arrived at our sample using a combination of cluster and purposive sampling.

Definition of variables and model specification

Distortionary taxes

A distortion is a departure from the allocation of economic resources from the state in which each agent maximizes his/her own welfare. A proportional wage-income tax, for instance, is distortionary. Tax on income, profits, capital gains, taxes on payroll and workforce, taxes on property including taxes on inheritance, capital and financial transaction reduce incentive for investing in physical / human capital and thus deter growth. Bleany et al. (2001) support a negative effect on economic growth.

Non-distortionary Taxes

Non-distortionary is a lump-sum tax which is a fixed amount, no matter the change in circumstance of the taxed entity. In economic theory, a lump-sum tax is considered to be pareto-efficient because it does not interfere with optimal market mechanisms and will only reduce people's available income and therefore increase their budget constraint, but leave the relative price of goods unchanged. Lump sum taxes or non-distortionary taxes include indirect taxes including custom, sales tax, federal excise taxes and do not discourage investing in physical/ human capital and thus have neutral impact on economic growth. Bleany et al. (2000) also support zero effect on economic growth.

The models for this work were structured in a way to empirically show the effect of tax policy on economic growth in sub-Saharan Africa. Bearing in mind that aside taxation, other fiscal variables (expenditure) are considered in the growth studies, thus in line with Barro and Sala-i-Martin (1992), Bleaney et al (2001) show that the long-run growth rate in an endogenous growth model (f) can be expressed as

f = l (1-t )(1-a)A1/(1-a)(g/y)a/(1-a) - m (1)

Where l and m are constants that reflect parameters in the utility function. Equation (1) shows that the growth rate is decreasing in the rate of distortionary taxes (t) and increasing in trade openness (g), but is unaffected by non-distortionary taxes (L) or inflation (C). This is the model which we tested in this study. Practically and as in Bleany et al (2001) we accounted for the fact that government finances the budget solely from tax revenue and as such the budget is not balanced in every period, so the constraint becomes

ng + C + b = L + t ny (2)

g = trade openness (+tive)

t = distortionary taxes (a proportional tax on output at rate) (-tive)

L = non-distortionary taxes (lump sum) (0)

C = inflation (0)

b = budget surplus.

The predicted signs of these components in a growth regression would be: g – positive; t – negative; C and L – zero; b – zero provided that the composition of expenditure and taxation remains unchanged. Specifically, to achieve the objective of this study we modeled in a log linear equation as follows:

Yit = a + b1nlDISTit + b2nlNDISTit + b3nlINFit + b4nlTROPENit + b5nlFISit + Uit (3)

where: a = constant;

nl = natural log

nlDIST = natural log distortionary tax defined as direct tax;

nlNDIST = natural log non-distortionary tax defined as indirect tax;

lnTROPEN = natural log of total trade (import and export) (control variable);

nlINF = natural log inflation rate (control variable);

nlFIS= natural log budget deficit/surplus;

Yt = GDP Per Capita

We carried our analysis under the panel data estimation technique under the fixed effect assumption and as such decomposed the error term in equation 3 as follows: uit = hit + eit. In the above decomposition, eit is the standard disturbance term, which varies across time and cross-sections, while hit is a set of group specific effects, which refer to each cross section in the model. It follows that equation 3 is re-written as follows:

Yit = a + b1nlDISTit + b2nlNDISTit + b3nlINFit + b4nlTROPENit + b3nlFISit + hit + eit (4)

DISCUSSION

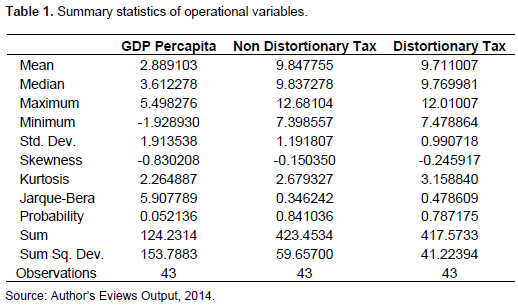

We start our analysis by presenting the summary statistics of the operational variables of GDP, distortionary and non-distortionary taxes as well as trade openness and inflation rate, budget balance in a common sample.

Table 1 presents the descriptive statistics for all the variables that operationalized our study in a common sample. The standard deviation of 1.91, 1.19 and 0.99% for GDP, distortionary tax, and non-distortionary tax implies that those individual observations did not deviate much from their respective means and this also reflected in the squared deviation figures of 153.78 and 5965 respectively.

The skewness estimate is used to capture how the variables for the Sub-Saharan African countries lean to one side. GDP Per Capita, non-distortionary tax, and distortionary tax variables are negatively skewed which implies a fatter tails to the left of their respective means. We also noted that the relative skewness of the variables lie closer to zero which implies that the probability distribution is evenly distributed around their respective mean i.e. been approximate to normal distribution.

Again the normality of the probability distribution is further justified by the Jarque-Bera statistics as we reject the null hypothesis that the variables are not normally distributed. The statistical properties of the operational variables are further enhanced by the kurtosis statistic which shows the relative peakness of the probability distributions. The low kurtosis of all the variables further justifies the normal probability without an excess peak. The null hypothesis of this test is that the data are normally distributed. Rejection of the null hypothesis implies that the data do not follow a normal distribution. The probability value below the Jarque-Bera test 0.049 < 0.10, we reject the null hypothesis which implies that the dataset does not follow a normal distribution.

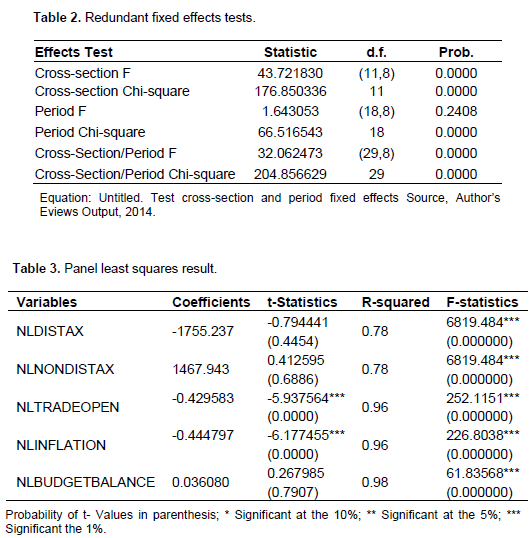

The Redundant Fixed Effects Test

Given that the panel least squares in this study were estimated under the fixed effects assumptions thereby imposing time and cross section independent on fiscal policy variables specific effects on the panel series controlled for distortionary and non-distortionary taxes, productive and unproductive expenditures as well as the element of the budget on the economic growth of Sub-Saharan African countries, the Redundant Fixed Effects test were conducted on the panel least squares to ensure that the fixed effects assumptions were adequately applied. To check whether the cross-sectional and time specific effects are appropriately included in our model we carried out the "Redundant Fixed Effect -Likelihood Ratio test". The (Cross-Section/Period F Cross-Section/Period Chi-square) tests the validity of a model where both cross-sectional and time effects are included in the model against a standard OLS model. The null hypothesis is that the set of dummies, hi and ht, are not statistically different from zero. The appropriate application of the fixed effects strengthens the result of our panel least squares. The results are presented and discussed in Table 2.

The null hypothesis is that the set of dummies, hi and ht, are not statistically different from zero. However, a look at table 2 presenting the cross-section and period fixed effects for equation 4 reveals that the probability of the Cross-section/Period F and Cross-Section/Period Chi-square statistics of 32.062473 and 204.856629 respectively are perfectly significant at 0.0000 < 0.05 respectively. We therefore, reject the null hypothesis and conclude that hi and ht is statistically significant from zero thus implying that the cross-sectional and time specific effects are appropriately applied in our estimation.

Having ascertained that the applications of cross-sectional and time specific effects are appropriate, we thus presented the panel least results (Table 3).

Table 3 indicates that that our R-squared are high and that our models fit given that the probability of the F-statistics are all significant at 1%. Table 3 also shows the sign of the coefficient for distortionary tax at -1755.237 to be negative, t-Statistic of -0.794441 not been significant at 0.4454 > 0.10; thus we accept the null hypothesis that distortionary tax has a negative and insignificant effect on the economic growth of sub-Saharan African countries. Subsequently, Table 2 shows the sign of the coefficient of 1467.943 to be positive, t-Statistic of 0.412595 been insignificant at 0.6886 > 0.10; thus we accept the alternate hypothesis that non-distortionary tax has a positive and insignificant effect on the economic growth of sub-Saharan African countries.

Comparing our negative relationship of non-distortionary tax to economic growth with past reviewed empirical studies, our finding confirms Koester and Kormendi (1989) who using reduced-form cross-section regressions estimated that the marginal tax rate-conditional on fixed average tax rates found an independent, negative effect on output growth rates. Also, our negative relationship of non-distortionary tax corroborates Wang and Yip (1992) in Chiumia and Simwaka (2012) who reported a negative impact of specific taxes on economic growth, as well Stokey and Robelo (1995) in Chiumia and Simwaka (2012) who employed endogenous growth models in their analyses and found an insignificant negative effects of taxation on economic growth in developed economies. Koch et al. (2005), adopting a two-stage modeling technique to control for unobservable business cycle variables, found that decreased tax burdens are strongly associated with increased economic growth thus confirming our negative report of distortionary tax. Finally our negative insignificant finding of distortionary tax supports Chiumia and Simwaka (2012) who examined the impact of tax policy and donor inflows on economic growth in Malawi from 1970 to 2010 using data envelope analysis (DEA) and transcendental logarithm (Translog) and reported that reduction in tax burden is more potent in influencing economic growth than fine tuning the proportion in which income and consumption taxes are collected in Malawi. The results of this study confirm certain previous evidence by a number of scholars for the inter-country as well as country studies while not in consonance with certain findings. Taxation which was decomposed into distortionary and non-distortionary taxes suggest that distortionary tax has a negative and insignificant effect while non-distortionary tax has a positive but insignificant effect on economic growth of sub-Saharan African countries.

Our findings of a positive relationship for non-distortionary tax somewhat corroborates Chigbu et al. (2012) who examined the causality between economic growth and taxation in Nigeria for the period 1970-2009 and found that taxation as an instrument of fiscal policy affects the economic growth and taxation granger cause economic growth of Nigeria. Chigbu et al. (2012) concluded that taxation is a very important instrument of fiscal policy that contributes to economic growth of any country.

CONCLUSION

As one of the recent studies that empirically analyzed the extent that tax policy engenders growth in Africa, this study has attempted to ascertain and project the drivers of economic growth in Africa given Government deliberate actions through taxation. Endogenous growth theory predicts that the drivers of economic growth depend on internal factors such as the level as well as the effect of taxation. Using a sub-Saharan Africa data set, we have found that in tax policy variables, distortionary and non-distortionary taxes raise the economic growth rate. Our results also suggest that consumption taxation can realistically be regarded as non-distortionary, rather than as merely less distortionary than income taxation.

Evidence arising from this study show taxes generate sufficient revenue to Government for further productive investment in the economy to crowd in the private sector whose activities enhances economic growth, thus the proportion in which taxes are collected is more important than the level of taxation in explaining economic growth. Thus efficient collections of all forms of taxes are imperative.

CONFLICT OF INTERESTS

The authors have not declared any conflict of interests.

REFERENCES

| Anyanwu JC (1997). Nigerian public finance. Onitsha: Joanne Educational Publishers. | ||||

|

Barro RJ (1990). Government spending in a simple model of endogenous growth. J. Polit.Econ. 98: 100-105. Crossref |

||||

|

Barro RJ, Sala-i-Martin X. (1992). Public finance in models of economic growth. Rev.Econ. Stud. 59: 645-661. Crossref |

||||

| Barro R, Xavier S (1995). Economic Growth. New York: McGraw-Hill | ||||

|

Bleaney M, Gemmell N, Kneller R (2001). Testing the endogenous growth model: public expenditure, taxation, and growth over the long-run. Canadian J.Econ., 34(1): 36-57. Crossref |

||||

| Chigbu EE, Akujuobi LE, Appah E (2012). An empirical study on the causality between economic growth and taxation in Nigeria. Curr. Res.J. Econ. Theory 4(2): 29-38. | ||||

|

Chiumia A, Simwaka K (2012). Tax policy developments, donor inflows and economic growth in Malawi", J.Econ. Inter.l Finance, Vol. 4 (7), 159–172. Crossref |

||||

| Dowrick S (1992). Estimating the impact of government consumption on growth: growth accounting and optimizing models. Mimeo: Australian National University. | ||||

| Easterly W, Rebelo S (1993). Fiscal policy and economic growth: An empirical investigation, J. Monetary Econ., Elsevier, 32(3): 417-458. | ||||

|

Engen E, Skinner J (1996). Taxation and economic growth. Nat.Tax J., 49(4): 617-642. Crossref |

||||

| Fadare SO (2010). Recent banking sector reforms and economic growth in Nigeria". Middle Eastern Finance and Economics, 8, 77-88. | ||||

| Keh Y (2010). Estimating the growth-maximizing tax rate for Coted'Ivoire: evidence and implications. J. Econ. Inter. Finance, 2(9): 164-174. | ||||

|

Kim SJ (1998). Growth effects of taxes in an endogenous growth model: to what extent do taxes affect economic growth. J. Econ. Dyn. Cont. 23(1): 125-158. Crossref |

||||

|

Koch SF, Schoeman NJ, Tonder JJ (2005). Economic growth and structure of taxes in South Africa. South Afr. J. Econ. 73 (2), 190-210. Crossref |

||||

|

Koester RB, Roger CK (1989). Taxation, aggregate activity and economic growth: cross country evidence on some supply-side hypotheses. Economic Inquiry, 27(3): 367–386. Crossref |

||||

| Pecorino P (1994). The growth rate effects of tax reform. Oxford Economics, 46: 492-501. | ||||

| Skinner J (1988). Taxation and output growth in Africa. (Policy, Planning and Research Working Paper 73). Washington: The World Bank. | ||||

|

Toshihiro I (2001). Wealth taxation and economic growth. J. Pub. Econ., 79: 129-148 Crossref |

||||

|

Tosun MS, Abizadeh S (2005). Economic growth and tax components: an analysis of tax changes in OECD", Appl.Econ.37: 2251-2263. Crossref |

||||

|

Romer PM (1994). The origins of endogenous growth. J. Econ. Perspect. 8(1): 3–22. Crossref |

||||

Copyright © 2024 Author(s) retain the copyright of this article.

This article is published under the terms of the Creative Commons Attribution License 4.0