This study examines the effect of audit quality on share prices of Nigerian oil and gas firms using the regression and covariance analyses. Findings from the regression anlysis suggests that the composition of the audit committee and auditor type has significant effect on the market prices of quoted firms. There is a positive and significant relationship between audit committee composition and share prices. The covariance analysis suggests that while auditor type (BIG4/NONBIG4), auditor independence, and composition of the audit committee have a positive and significant relationship with market price of shares, tenure of external auditors has a negative relationship with the market price of shares. The implication of the findings is that audit quality will enhance reported earnings and hence the share market prices. The study recommends that firms should strive to associate with the BIG4 external auditors in Nigeria as such an association could enhance the credibility of the audit process and by extension their share prices; regulatory authorities should discourage joint audit and non-audit services to firms because it could threaten the independence of external auditors. Regulatory agencies should also present distinct statements on the tenure of the external auditors to be clearly stated in annual reports. This is because a long attachment between the external auditors and a client may threaten the independence of the external auditors.

Auditing of financial statements serves as a control mechanism for shrinking information unevenness and safeguarding interests of the differing claimants by ensuring that the audited financial statements are free from contents misstatements (Macharia and Gatuhi, 2013). Auditors help to reduce the perils of significant misstatements by ensuring financial statements are prepared according to preset standards. Lower perils on misstatements intensify confidence in stock markets, which in turn lowers the cost of capital for firms (Hoti, 2012). Standard setters and implementers can increase the effectiveness of public firms by propagating standards that help guarantee that auditing improves the excellence of financial information. This is because both internal and external users of financial statement are interested in the excellency of audits (Miettinen, 2011).

A quality audit can allow income management so that earnings per share figures reach desired levels. Earnings can be manipulated to ensure that earning per share meets analysts’ forecasts. Since current income is a signal of expected cash flows, failure to meet analysts’ expectations of earnings per share could result in a dejected share price, while meeting these expectations brings about a maintenance or growth in stock price (Jordan et al., 2010). Signaling theory opines that firms with good performance send a signal to the market through financial information disclosures. Firms are provided an incentive to signal through their choice of an external auditor. Even voluntary disclosures that may be used as signals improve credibility in the presence of a quality audit. A financial statement audited by dependable auditors signals to the market that the financial statements are more reliable than those audited by unreliable auditors. The market perceives size and specialist auditors to be of a higher quality than others and rewards (punishes) companies with larger improvements or falls in share prices accordingly. Bearing the aforementioned in mind, a superior and independent audit plays an important role in maintaining an efficient market environment, underpins confidence in the reliability and veracity of financial statements essential for well functioning markets.

The acknowledged failure of audit process to capture financial misstatements has provoked the ostensible outburst of interest and attention in general financial reporting. The perceived failure of audit to fully alert equity and other claimants concerning misrepresentations has made investors helpless and inept to undertake rational financial decisions affecting entities generally. This is so because the quality of reported earnings and the capability of auditing to efficiently contain management earnings machinations have become highly doubtful. Thus, there is a worry about the truthfulness of reported income and its relationship with the audit process given the pockets of corporate failures. Thus, questions whether these corporate failures and by extension stock price fluctuations are not the result of poor audit process and the incapabality of the audit function to cushion earnings misstatements.

Stock price fluctuation is a sudden and negative reverse in investors’ prospects about a firm’s shares. Studies of stock prices fluctuations discovered two main reasons, namely management activities and accounting systems, which boost them (Khajavi and Zare, 2016). Management tries to mis-represent earnings, which leads to investors’ prospects about the earnings of firms and ultimately increases their share price than the actual amount. Also, management illogically raises or hides bad news until they are unable to prevent it from broadcasting. At this point, stock price reacts to such bad news by crashing dramatically (Kim and Zhang, 2015). Stock price fluctuations in recent years due to occurrence

of certain events have become an increasingly important issue among financial and accounting researchers, whereas the main purpose of the auditing function is for reliable financial reporting for decision making. Lotfi (2011) pointed out that accounting was always an accomplice to management in studies regarding stock price fluctuations.

Due to the divorce of firm ownership from management, audit function arises. The agency problem arises from the existence of asymmetric information in the principal agent contracts (Jenson and Messier, 2000). The existence of information asymmetry between firm management and ownership influences the changes in market prices of shares. The audit function in a corporation is an inbuilt system that reduces information asymmetry for the interests of the owners. Auditors’ theory of inspired confidence links the users’ need for credible financial reports and the capapability of the processes to meet such needs. It reduces the possibility of hidden misstatement to an appreciated assurance level (Knechel, 2009). The quality of an audit process should influence the reported earnings and strongly influence investors’ confidence. Conventionally, external audit function is necessary for enhancing confidence in financial reports. However, with the pockets of business collapses, there is a concern about the quality of auditing. This concern could also be extended to the underlying changes in market prices of shares over time, and hence, this study determines the impact of the quality of an audit on the market prices of shares for Nigerian firms.

Concept of audit quality

De Angelo (1981) defined the quality of audit services as “the market-assessed joint probability that a given auditor will both (a) discover a breach in the client’s accounting system and (b) report the breach.” The probability that a given auditor will discover a breach depends on the auditor’s capabilities and the audit procedures employed on a given audit (Khajavi and Zare, 2016). After De Angelo, other researchers like (Palmrose, 1988; Teoh and Wong, 1993) jointly agreed that audit quality is perceived as discovering and reporting misstatements in financial statements by the auditor depending on his competence and independence. De Angelo (1981) developed a two dimensional definition of audit quality that set the standard for addressing the issue. First, a material misstatement must be detected, and second, the material misstatement must be reported. De Angelo (1981) further theorizes that larger firms perform better audits because they have a greater reputation at stake. In addition, because larger firms have more resources at their disposal, they can attract more highly skilled employees.

Measures of audit quality

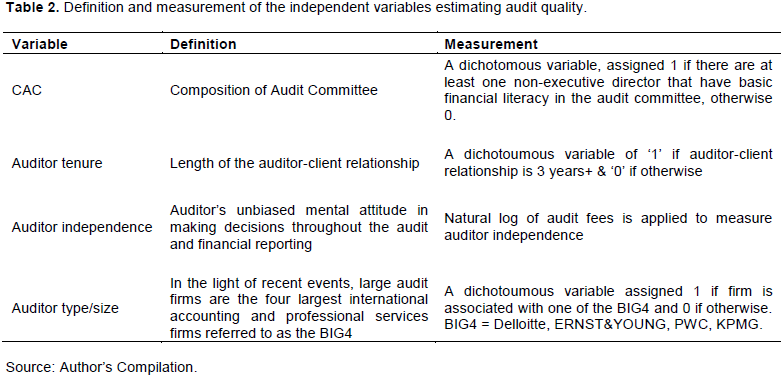

Audit size/fees: Okolie and Izedonmi (2014) pointed out that scholars have theorized that large auditors attract a fee premium because their greater wealth reduces clients’ exposures in litigation (the deep pockets theory); while others have theorized that there is no real audit quality difference, but rather that large firms are perceived to have gained experience and reputation for quality. Based on the report of De Angelo (1981), previous studies proxied the size of the auditor categorizing auditing firms belonging to the Big8, Big6 or Big5 as against non-Big8, non-Big6 or non-Big5 to classify levels of audit quality (Copley, 1991; Clarkson and Simunic, 1994; Becker et al., 1998; Krishnan and Yang, 1999). Some studies (Palmrose et al., 2004; Copley, 1991; Colbert and Murray, 1998) have also related audit fees with the quality of audit bearing in mind that firms who charge high fees for audit deliver high quality audit. However, the outcomes are mixed, but show a relationship between the size of the auditing firm and audit quality.

Audit independence: Okolie and Izedonmi (2014) defined audit independence as an auditor’s unbiasedness in taking decisions during an audit. Independence implies being free from inspiration, stimulus or guidace of which in the absence of independence, the value of the audit function will be greatly compromised (Sweeney, 1994). Prior studies suggest that high audit fees paid by a company to its external auditor enhances the economic ties between them and as such may compromise the indepence of the auditor (Frankel et al., 2002; Li and Lin, 2005). This weakened unconventionality results in failed audit quality and gives room for earnings manipulations (Okolie and Izedonmi, 2014). In past studies, audit fees have been used to measure auditors’ independence (Palmrose, 1986, 1988; Moizer, 1997; Wooten, 2003).

Auditor industry specialization: Auditor industry specialization is another proxy for audit quality (Khajavi and Zare, 2016) bearing in mind that the auditor expertise or incapability in an industry will affect the quality of the audit. Specialized audit firms that audit clients in specific industry is in an advantaged position to view business and operational risks in such industry and conversely. Conclusively, if auditors remain restricted in specialised industries, there are high tendencies of providing higher quality of audit (Yaghoobnezhad and Amiri, 2009). Craswell et al. (1995) opined that auditors with specialty in given industries always demand higher fees due to higher-quality capabilities. Auditors of industries specialty have been shown to have positive and significant relationships with audit quality (Chen et al., 2012; Jubb et al., 2004).

Auditor tenure: Auditor tenure is viewed as the length of time between auditor-client relationship (Okolie, 2014). A

lengthy link between the auditor and his client may threaten unconventionality given developed familiarity. This may lead to less caution and compromise on the part of the auditor. Besides, a lengthy engagement may bring about less effort to signal the failings of internal control and risk sources (Okolie, 2014). Knapp (1991) established a linkage between audit tenure and competence. The objectiveness of an auditor in detecting anomalies increases in the first years of engagement but wanes with time, reaching its weakest level after 20 years of service (Okolie, 2014). There has been considerable decrease in number of years for auditor tenure. In the US, auditor tenure was reduced from seven to five years; the European Commission recommended a rotation of engagement partners every seven years; in France, auditors are chosen for six financial years, while in Nigeria audit engagement should not exceed three years (Okolie, 2014). Auditor tenure studies (Knapp, 1991; Lys and Watts, 1994; Geiger and Raghunandan, 2002; Frankel et al., 2002; Myers et al., 2003) abound in literature. For this study, auditor tenure was proxied as length of auditor-client relationship using a dichotoumous variable of ‘1’ if 3 years+ and ‘0’, if otherwise.

Composition of an audit committee: Composition of an audit committee is the percentage of non-executive and executive directors; and audit committees composed of higher non-executive directors viewed to be highly independent (Glover-Akpey and Azembila, 2016). Shivdasani (1993) and Yermack (1996) note that executive directors divulge limited information to non-executive directors and hence the domination of executive directors affects an effective control and management structure. The existence of majority of non-executive directors in an audit committee enhances the independence of the committee (Glover-Akpey and Azembila, 2016). Studies show that non-executive directors are capable of providing unconventional opinions and positive roles in corporate governance given their potents to be more independent than executive directors (Vinten and Lee, 1993; Beasley, 1996). Vicknair et al. (1993) note increasing ratio of non-executive director membership of audit committees and signify the importance of independence of the audit committee. Porter and Gendall (1993) observe that a high ratio of non-executive directors in an audit committee enhances the worth of an audit committee as an internal control mechanism. A high ratio of non-executive directors drastically reduces the probability of financial misstatements (McMullen and Raghunandan, 1996).

Perspective of share price measurement

Blessing (2015) notes that there are two perspectives of share prices measurement in the capital market: information and measurement perspectives. Information perspective measures the usefulness of accounting to individual users without much emphasis on the precise structure of the relation accounting data and firm value (Bernard, 1995) while the measurement perspective assumes that share price movement can be determined by the degree of volume or price change following release of the information. The study by Ball and Brown (1968) was the first to document statistically a share price response to reported net income and their methodology is still employed today. The measurement perspective is rooted on the theoretical framework of equity valuation models (Ohlson, 1995), which expressed the value of a firm as a function of book value and earnings (Blessing, 2015). However, attention has turned in recent years to valuation models that include dividend per share, net assets per share earnings yield, and others (Francis and Schipper, 1999; Blessing, 2015; Kaplan, 2001).

Theoretical framework

The theoretical framework of this study is the agency theory used to determine the impact of audit quality on the market prices of firms quoted on Nigerian Stock Exchange. According to the agency theory, a company consists of a set of linked contracts between the owners of economic resources (the principals) and managers (the agents) who are charged with using and controlling these resources (Sarens and Abdolmohammadi, 2007). Jensen and Meckling (1976) state that in agency theory, agents have more information than principals and this information asymmetry adversely affects the principals’ ability to monitor whether or not their interests are being properly served by the agents.

Sarens and Abdolmohhamadi (2007) opine that an assumption of agency theory is that principals and agents act rationally and use contracting to maximize their wealth. A consequence of this is the moral hazard issue (Farouk and Hassan, 2014) since all available information are not known to the principals at the time a decision is being made by an agent. Thus, the principal fails to determine whether the agent’s actions are in the best interest of the firm. To reduce the likelihood of the moral hazard corporate governance ensures the inclusion of auditing as an internal control and mornitoring function. While Defond (1992) stresses the divergence of diffusion, separation of ownership and controlling such divergence demand monitoring. Therefore, numerous auditing processes will be needed to monitor the agent’s actions in more diffused ownership structures (Farouk and Hassan, 2014).

The principal-agent association as shown in agency theory is important to understand how the role of an auditor has developed (Farouk and Hassan, 2014). Watts (1998) observes that auditing is considered as a bonding cost paid by agents to a third party to satisfy the principals’ demand for accountability. Like any other cost of running the business, the cost of auditing is borne by principals to protect their economic interests. Louise (2005) states that audits serve as a fundamental purpose in promoting confidence and reinforcing trust in financial information. Agency theory therefore, stresses a useful economic theory of accountability, which helps to explain the development of audit function and by extension the quality of an audit process.

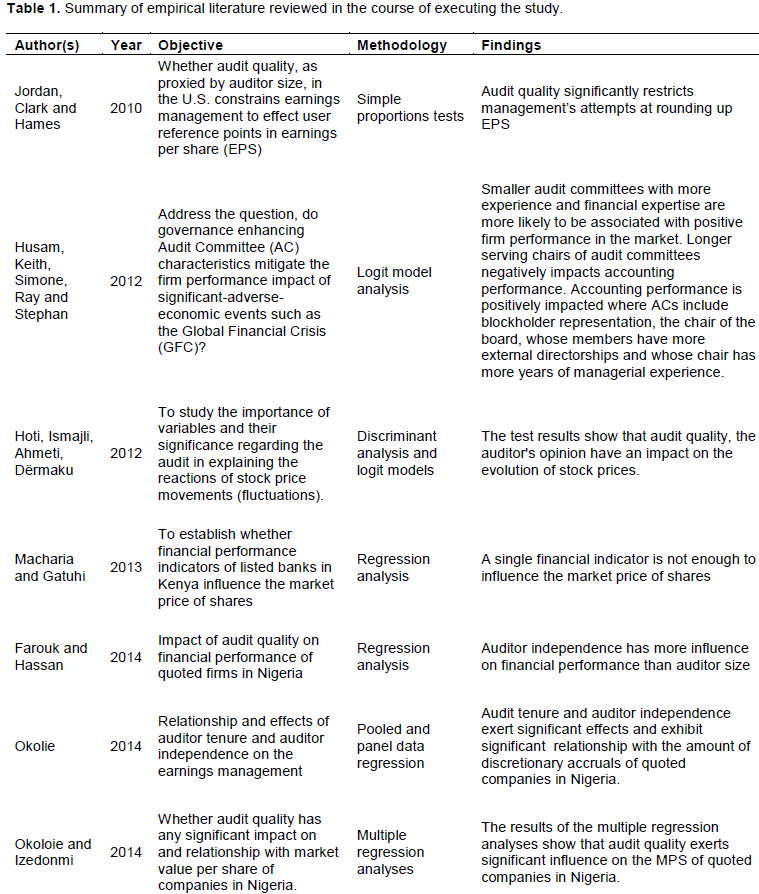

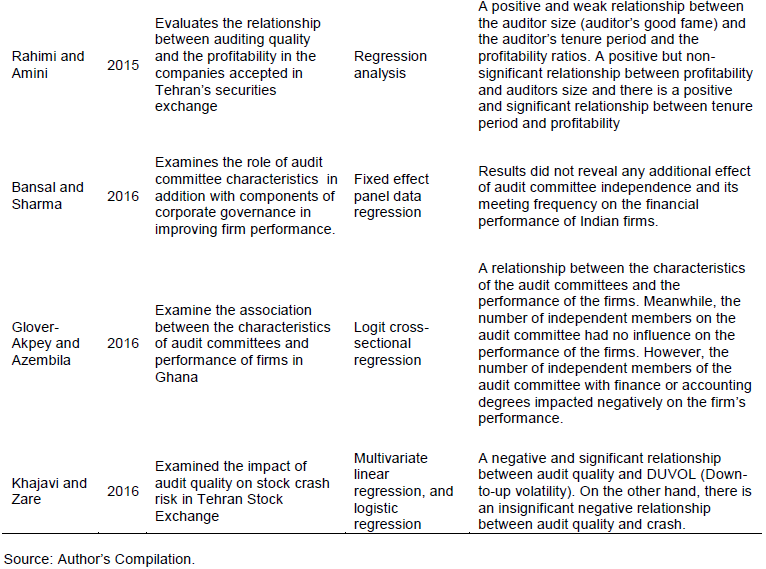

Table 1 shows a summary of empirical literature reviewed in the course of executing the study.

Research gaps

Studies on audit quality in Nigeria center on firms’ performance and utilizing various performance measures as well as on earnings management utilizing the discretionary accrual method. Other studies on audit quality reviewed earlier were carried out outside the shores of Nigeria. The gap filled by this study could be viewed as follows: bearing the signaling theory in mind, it is expected that the release of a firm’s financial reports and its earnings has a ripple effect on the market price of such firms. Thus, this study moves away from financial performance measures to ascertain the effect of audit quality on the value placed by investors in the stock market, the market price. Secondly, the essence of concentrating on market value is that the value of a firm especially the market value is reflective of the fundamentals of a firm including auditing practices (type, size, independence, tenure and audit committee composition). Thirdly, in the wake of improved financial reporting and by extension, the mandatory International Financial Reporting Standards (IFRS) adoption and its implication for firms, investors and the overall economic performance, this study examines the effect of audit quality on the value placed on firms by the stakeholders.

The research design adopted for this study is the ex-post facto as the study relied on historic data. The nature of data for this study is secondary and sourced from the annual reports and accounts of sampled oil and gas firms for audit quality variables. For stock prices, the study used firm-level data bothering on stock prices gathered from the Nigerian Stock Exchange. Stock prices data exist in daily, weekly and monthly forms. This study adopts the monthly stock prices and using the December month as the closing price of the stocks in each of the periods. The population of the study consists of all the firms classified under the oil and gas sector of the Nigerian Stock Exchange.

Model

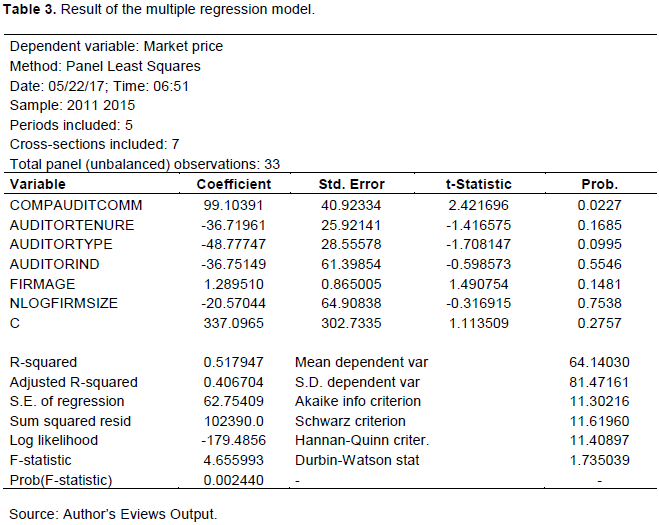

The Panel Least Squares (PLS) was applied to the series of data; the signs of the coefficients were relied upon in describing the direction and strength of linear relationship between the dependent variable (stock prices) and audit quality (independent) variables (composition of audit, auditor type, auditor independence, and auditor tenure). The general model is represented thus:

MPSit = a + b1CACit + b2AUDTit + b3AUDTINDit + b4AUDTYPit + b5FSit + b6AGEit + Uit (1)

where a = constant; CAC = composition of audit committee for firm i at time t; AUDT = tenure of the external auditor for firm i at time t; AUDTIND = independence of the auditor for firm i at time t; AUDTYP = auditor type for firm i at time t; FS = firm size for firm i at time t; AGE = firm age for firm i at time t.

Dependent variable

Market price per share of quoted firms of each of the firms were obtained directly from www.cashcraft.com at the end of the year.

Control variables

Control variables used in this study are related to firms’ size and age. Kinney and McDaniel (1989) find that larger firms tend to have better internal controls, better information systems, more resources for hiring fully qualified personnel, and therefore increased reporting quality. Firm size is measured as the logarithm of the book value of total assets and age was measured as the number of years given for firms’ incorporation.

The result of the multiple regression model in Table 3 shows that why composition of the audit committee is statistically significant at 5% (0.0227 < 0.05), auditor type is significant at 10% (0.0995 < 0.10). The relationship between the variables was estimated with a covariance analysis and the result of the covariance analysis is shown in Table 4.

The covariance analysis result in Table 4 shows that while auditor type (BIG4/ NONBIG4), auditor independence, and composition of the audit committee have positive and significant relationships with market price of shares, the tenure of the external auditor has a negative and insignificant relationship with the market price of shares.

Findings from the test of hypotheses show that the composition of the audit committee has a positive and significant effect on market price of quoted firms. This implies that enhancement in the composition of audit committee improves audit quality. This finding corroborates the findings of Hoti et al. (2012) who determined the effects of stock prices following the announcement of audited financial reports of Slovenian and Croatian public interest entities in the role of audit in explaining the reactions of stock price movements (fluctuations); they found that audit quality has an impact on the evolution of stock prices.

Khajavi and Zare (2016) examined the impact of audit quality on stock crash risk in Tehran Stock Exchange and reported that there is an insignificant negative relationship between audit quality and crash. This finding supports the findings of this study where auditor size, auditor tenure and auditor independence have negative and insignificant effect on stock prices for oil and gas firms in Nigeria.

The quality of stated earnings and capability of the audit function to effectively constrain information missrepresentation of firms across the world have become highly questionable. Concerns abound about the audited reported accounting information and its relationship with the quality of the auditing function. This questions if corporate failures and stock price fluctuations are not outcome of poor audit function particularly in arresting earnings mis-representations. To this extent, this study examines the effect and relationship between audit quality and the market price of shares of Nigerian quoted firms. Findings from the multiple regression anlysis of the study suggest that the composition of the audit committee and auditor type exerts significant effect on market prices of quoted firms. The covariance analysis suggests that while auditor type (BIG4/ NONBIG4), auditor independence, and composition of the audit committee have a positive and significant relationship with market price of shares, the tenure of the external auditor has a negative relationship with the market price of shares.

Conclusively, the adequate pricing of shares of corporations to a large extent depends on the perception of investors as regards the audit fundamentals of such firm.

Given a positive and significant effect of audit committee composition, firms should strive to increase

the number of non-executive directors in the audit committee. This will enhance audit quality and by extension share prices. Although the size of the external auditor constitutes an insignificant effect on share prices, firms should strive to associate with the BIG4 external auditors in Nigeria as such an association could enhance the credibility of the audit process and by extension their share prices. Regulatory authorities should discourage audit firms from rendering non-audit services to firms because the joint provision of audit and non-audit services may eventually become a threat to the independence of the external auditor. This is because the joint provision of audit and non-audit services may lead to personal ties and familiarity may develop between the parties. This may lead to less vigilance on the part of the external auditor and even to an obliging attitude of the latter towards the top managers of the company and by extension to poor audit quality. In order to improve the quality of audit in Nigeria, the regulatory agencies should present distinct statements on the tenure of the external auditor and this should be clearly stated in annual reports. This is because a rather too long association between the external auditor and his client may constitute a threat to the independence of the external auditor.