Full Length Research Paper

ABSTRACT

The purpose of this study is to investigate the contribution of borrowers’ characteristics and credit terms on loan repayment performance of MFIs in rural areas of Uganda. This study is cross sectional and correlational. Data were collected through a questionnaire survey of 51 MFIs in Uganda. Results indicate that there is a significant relationship between credit terms and loan repayment performance among clients of MFIs unlike borrowers’ characteristics. This study’s regression model predicts 16% of the variance in loan repayment performance of MFIs in rural Uganda. The study is relevant to persons who borrow money and managers of MFIs and Savings and Credit Cooperatives (SACCOs). Managers may need to flex their credit terms and borrowers may have to identify those MFIs and SACCOs that are ready to discuss credit terms if the microfinance industry in Uganda is to help in reducing poverty. Whereas hitherto both borrowers’ characteristics and credit terms had been viewed as possible explanations of loan repayment performance, this study only confirms credit terms as a significant predictor of loan repayment performance.

Key words: Microfinance institutions (MFIs), borrower characteristics, credit terms, loan repayment.

INTRODUCTION

In this paper, the contribution of borrowers’ characteristics and credit terms on loan repayment performance among clients of Microfinance Institutions (MFIs) is reported using evidence from rural areas of developing countries like Uganda. Loan repayment is critical in terms of development of both the client and the microfinance institution. When MFIs disburse funds to the clients, they are expected to repay the loans in a specified period of time as agreed upon in the loan agreement. Repayment usually takes the form of periodic payments that includes part of the principal plus interest in each installment payment (Ifeanyi et al., 2014). MFIs through their loan officers screen their clients in terms of their demographics, ability to pay and assets owned (borrowers’ characteristics) before disbursing the loans. In addition, they explain to these clients about the terms and conditions governing the loan in terms of interest rate, collateral and loan period (credit terms). This is done to ensure that only clients who qualify for the loan receive it after understanding their obligations to ensure timely repayment. Whereas MFIs put in place measures to ensure that loans are repaid on time, loan default has continued to increase tremendously (Makorere, 2014; Morduch, 2006).

For quite a long time, the poor people were neglected by the commercial banks until 1976 when Professor Muhammad Yunus introduced the concept of micro financing to the world through the establishment of Grameen Bank in Bangladesh to offer unsecured small loans to the poor (Nanayakkara and Stewart, 2015; Ray and Mahapatra, 2016). In their study, Nanayakkara and Stewart (2015), the time to approve and disburse the loan, loan cycle, gender and age of the borrower, whether a group or individual borrower, the purpose for which the loan is used and visiting frequency by the loan officers were found to be significant when predicting the loan repayment in Sri Lanka, and time to approve and disburse the loan, interest repayment frequency and gender were the three factors that were found to be significantly associated with loan repayment in Indonesia. In India, MFIs have concentrated in areas where there is a richer population, good rural infrastructure, but lack in adequate banking facility, and have low human capital (Ray and Mahapatra, 2016). Qinlan and Izumida (2013) identify factors such as a higher degree of acquaintanceship in a group, migrant income, and employment in government agencies to be behind improved loan repayment in China.

In Uganda, MFIs include Savings, Credit and Cooperative Societies (SACCOS) which were initiated under the Uganda Cooperative Alliance (UCA) with the aim of providing quality financial services on the basis of self-reliance through mobilization and management of their own financial activities (Mpiira et al., 2014). One of the major roles of SACCOS is to provide loans to the poor either individually or in a group that is neglected by the commercial banks especially those in rural areas (Ray and Mahapatra, 2016). In Luwero district, studies carried out by Uganda Radio Network (URN) revealed a high default rate among clients in most of the SACCOS located in the district (URN report, 2014) for example in Community Development Microcredit Finance, loan officers disbursed shillings 36 million to the borrowers in October 2013, but only recovered 9 million shillings. The report indicated that borrowers are playing hide and seek with the SACCO officials, adding that some of them have never returned a single shilling, which has affected their revolving funds. Loan officers in such SACCOS have now resorted to arresting the borrowers due to increasing loan arrears. This has constrained MFIs’ capacity to lend to other clients and if unchecked will deter the MFIs from achieving their intended objectives and lead to their eventual collapse. The challenge is for MFIs to find ways of screening their clients before lending to them and set credit terms that will enhance loan repayment by their clients. MFIs in Uganda play a vital role in supporting the business sector as well as in national development through issuing loans to their clients. Atikus Insurance (2014) defined microfinance as the provision of financial services to low-income earners and those who are self-employed and lack access to banking and related services.

Given that Africa is one of the continents with majority of the population leaving in the rural areas in absolute poverty, researches like ours are very important. One-fifth of the world’s population lives in extreme poverty and approximately 2.5 billion adults lack access to formal financial services (Atikus Insurance, 2014). Extreme poverty in Africa fell from 57% in 1990 to 43% in 2012 (World Bank, 2016). Based on the 2012/2013 survey, it was estimated that 19.7% of Ugandans are poor, the incidence of poverty in Uganda remains higher in rural areas than in urban areas. The poor in the rural areas of Uganda represent 22.8% of the population compared to only 9.3% in the urban areas. The Uganda rural areas with about 77.4% of the population constitute 89.3% of national poverty. On the other hand, the urban areas represent 22.6% of the population and constitute 10.7% of national poverty (Uganda Bureau of Statistics, 2015). The world has a long way to go before achieving full financial inclusion. Today, microfinance is a mainstay development strategy for extreme poverty alleviation and is supported by many as a way of achieving the United Nations Millennium Development Goals and developing countries must allocate all the necessary resources to the microfinance industry. However, Uganda is one of those countries whose population is moving away from poverty given that the country has developed vision 2040 aimed at becoming a middle income status economy.

The results reported in this paper are particularly significant as they are expected to add on the body of existing knowledge on loan repayment performance among clients of MFIs in rural Uganda and possibly other developing nations facing MFI loan repayment performance challenges, can improve loan repayment performance whilst still enabling MFIs to achieve financial and operational sustainability. The strategies to improve financial and operational sustainability of MFIs may include: government incentives for MFIs to increase their outreach beyond urban limits, capacity building of MFIs to foster suitable products, policies and procedures, and the publication of interest rates and product fees charged by MFIs so as to motivate competition and efficiency in the sector. However, this can best be achieved through MFIs management negotiating credit terms with clients or MFIs management putting in place more friendly credit terms.

LITERATURE REVIEW

The predictor variables in this study were defined based on the existing literature. The predictor variables are credit terms and borrowers’ characteristics. The dependent variable for this study was also defined. The existing literature was also reviewed to develop the hypotheses.

Borrowers’ characteristics and loan repayment performance

Loan repayment performance among the clients of MFIs is a measure of whether the loans are repaid in full by the clients according to the loan contract or not. The higher the loan repayment performance, the higher the probability of the MFI collecting interest revenues and the lower the loan losses which enhance sustainability. High repayment rates are indeed largely associated with benefits both for the financial institution and the borrower. They enable the financial institution to cut the interest rate it charges to the borrowers, thus reducing the financial cost of credit and allowing more borrowers to have access to loans (Kon and Storey, 2003). Improving repayment rates also help reduce the dependence on subsidies of the financial institution which would improve sustainability. It is also argued that high repayment rates reflect the adequacy of financial institutions services to client’s needs. They limit the incidence of cross subvention across the borrowers. Similarly, repayment performance is a key variable for donors and international funding agencies on which many financial institutions still depend for their access to funds. The first-best level of repayment performance is a perfect (100%) on-time repayment rate (Ongena and Smith, 2001). If the maximum repayment rate the financial institution can reach given its lending methodology is lower than the targeted 100%, the financial institution will use second-level strategies to increase its repayment performance. Such strategies include the allocation of larger loans to borrowers with lower default probability and attempt to reduce the delay in repayment.

Borrowers’ characteristics are attributes borrowers should have if they are to benefit from or access micro credit institution services easily (Nyangiru et al., 2014). Accessibility to credit by the borrowers will depend on the seriousness MFIs attach to the borrowers’ characteristics before extending credit to clients (Nanayakkara and Stewart, 2015). For instance, borrowers who own assets will easily access credit since it reduces the risk of the institution losing its funds. These characteristics include demographic characteristics (age, gender, education, marital status, experience, training and number of times an applicant has ever borrowed a loan from the MFI), ability to pay and assets owned by the borrower. According to Nawai and Shariff (2010) for any credit scheme to operate effectively, it is important to know the character of borrowers in relation to payment. This calls for investing in information gathering by MFIs on their potential borrowers and always be mindful when setting performance targets against giving of credit to borrowers. The pay period and method of paying back should be determined early and understood by both parties (lender and borrower) since the payback period can be used as a decision criterion to accept or reject the investment proposals (Nanayakkara and Stewart, 2015).

Bhatt and Tang (2011) looked at the borrower’s socio economic variables for their influence on loan repayment. The borrower’s socioeconomic variables included gender, educational level, household income and characteristics of the business (type of business, years in business, among others). In their study, Bhatt and Tang (2011) found out that a higher education level was significant and positively related to better repayment performance. Conversely, female borrowers, level of household income, type of business and borrower’s experience had no significant effect on repayment performance (Bhatt and Tang, 2011). While Pasha and Negese (2014) carried out research in Ethiopia to determine the factors affecting loan repayment among MFIs and found out that the education level was positively and significantly influencing loan repayment at 1% significance level, an increase in one year schooling increases the probability of the loan repayment rate by 4.939%. This implies that the borrowers whose educational level is higher say university degree have the probability of loan repayment four times more than the borrowers who have lesser education level say primary education or illiterates.

Awunyo-Vitor (2012) indicated that the probability of a loan repayment was higher for males than the females. Awunyo-Vitor (2012) further argued that, male borrowers had experience in accessing microcredit than their female counterparts. Contrary, Roslan and Abdul Karim (2009) investigated microcredit loan repayment in Malaysia and in their research, they found that male borrowers who had a longer duration for repayments had a higher probability of defaulting. Borrowers involved in non-production oriented business activities such as in the service or the support sectors, who had training in their particular business and who borrowed higher loans had lower probabilities of defaulting (Roslan and Abdul Karim, 2009). Ifeanyi et al. (2014), studied loan repayment of smallholder cooperative farmers in Nigeria and a negative association was found between age and repayment ability of respondents, implying that younger farmers were more likely to repay credit than older ones. Thus, in this study, we try to reaffirm the relationship between borrowers’ characteristics and loan repayment performance by hypothesizing that:

HI: There is a positive relationship between borrowers’ characteristics and loan repayment performance in the Ugandan MFIs

Credit terms and loan repayment performance

Credit terms have been understood to mean collateral, repayment periods and interest rate (Atieno, 2001).

Collateral is the security given by a borrower to a lender as an assurance that the loan will be paid (Atieno, 2001) and operates as a broad insurance against uninsurable risk or intentional default leading to non-payment of the loan (Ayyagari et al., 2003). Loan repayment period is the time in which the borrower should repay the loan (Atieno, 2001; Yehuala, 2008; Nkundabanyanga, 2014). Interest rate is the rate which is charged or paid for the use of money (Cowling and Westhead, 1996) and is used as a means of compensating banks for taking risk. According to Stiglitz and Weiss (1981), credit terms are part of a general exercise to help determine the extent of risk for each borrower.

According to Malimba and Ganesan (2009), grace period, collateral, interest rate charges and number of official visits to the credit societies, have a strong effect on loan repayment. Nkundabanyanga et al. (2014), found out that the higher interest rates induce firms to undertake projects with lower probability of success but higher pay offs when they succeed. Nanayakkara and Stewart (2015) further indicated that since the financial institution is not able to control all actions of borrowers due to imperfect and costly information, the MFI will formulate terms of the loan contract to induce borrowers to take actions in the interest of the financial institution and to attract low risk borrowers. According to Ifeanyi et al. (2014), the interest rate has an effect on the use, repayment of the loan and the overall performance of the business. When the interest rate charged is high, there is a tendency for the borrowers to keep part of the borrowed money to pay the interest or to use the business capital to pay the interest. Malimba and Ganesan (2009) further argue that interest on borrowing is one of the costs of production. The higher the interest rate the higher the likelihood of loan repayment default as the costs of servicing the loan increase.

Anderson (2002) and Besley (1995) indicated that an increase in interest rates negatively affects the borrowers by reducing their incentive to take actions that are conducive to loan repayment. According to Makorere (2014), Grace period is the period given by the financial institution to the borrower before the first installment is due. In other words, it is considered to be the time between when the loan was disbursed to the loan applicant and when the first installment is paid. While conducting a study in Tanzania, Makorere (2014) found out that most of the financial institutions tend to provide a grace period of one month only, which was seen not to be sufficient for the small business enterprise owners to start realizing enough revenue for them to start paying their loans. Makorere (2014) further found out that businesses that get enough grace period have never defaulted. Woolcock (1999) observed that if the loan term is too short, the borrower fails to generate revenue to enable him/her make repayments while a longer loan term may make the client extravagant and the client may in the end fail to pay back.

Kakuru (2008) found that when Small and Medium Enterprises perceive repayment period as not being flexible, they will not apply for the loans. For successful results, the loan terms should match the cash patterns to help the client budget cash flows (Stiglitz and Weiss, 1981).

The findings made by Atieno (2001), indicates that stringent lending terms discourage borrowers to apply for bank debt even when they are searching for finance to execute valuable investment projects. For example, pledging business collateral limits the firms’ ability to obtain future loans from other lenders which creates a position of power for the lending bank (Mann, 1997). According to Zeller (1994), collateral value requirements deter SME borrowers from seeking credit. Stiglitz and Weiss (1981) found out that SMEs hesitate to seek credit when they do not understand why requirements like collateral are imposed on them. Banks, however, prefer borrowers with collateral. For example, Safavian et al. (2006) observed that commercial banks usually provide larger loans, longer repayment periods and lower interest rates when borrowers offer collateral. This means that a borrower who cannot provide the type of assets lenders require as collateral often gets worse loan terms than otherwise. Indeed Lehmann and Neuberger (2001) notes that borrowers who provide more collateral receive a better rating. Access to finance is particularly difficult for SMEs with insufficient collateral that do not have any established track record or credit history. But other findings (Chan and Kanatas, 1985; Bester, 1987; Besanko and Thakor, 1987) show that low-risk borrowers pledge more collateral than high-risk borrowers. Nevertheless, some studies (Shen, 2002; Atanasova and Wilson, 2004) indicate that higher availability of collateral is expected to increase the supply of bank debt as collateral can mitigate the information asymmetries between the borrower and lender. This foregoing paragraph concludes that commercial banks’ requirement for collateral positively affects access to formal credit where collateral is readily available. Contrarily, where collateral is not readily available, the demand for it will negatively affect access to formal credit. In the majority of studies, this distinction has not always been made explicit. The foregoing discussion suggests that:

HI: Credit terms is positively associated with loan repayment performance in the Ugandan MFIs

METHODOLOGY

Design, population and sample

This study’s research design is cross sectional and correlational. Cross sectional designs are suited for studies aimed at finding out the prevalence of a phenomenon, situation, problem or attitude by taking a cross section of the population at a given time. The study population is 90 microfinance institutions that are members of the Association of Microfinance Institutions of Uganda (AMFIU) (AMFIU directory, 2013) from which sample size of 73 MFIs was determined using Krejcie and Morgan table (1970). A simple random sampling method without replacement was used to select the 73 MFIs. Of the 73 MFIs, completed questionnaires were received from 51 MFIs indicating a response rate of 70%. This high response rate was as a result of the sufficient time given to respondents to complete the questionnaires. Such high response rates for a survey of this type have existed in previous studies involving such surveys but in other cases, such surveys have had lesser percentage response rates. The higher percentage response rate was possible because respondents were given 5 months to complete the questionnaire and a number of call backs were made. This study’s unit of analysis was an MFI and the unit of inquiry was the any two clients of the MFI. The clients were purposively selected on the basis that the MFI member had ever taken a loan. Loan officers were used to locate the actual respondents. Therefore, MFI members were sampled basing on their accessibility and willingness to participate in the study.

The questionnaire, measurement of variables, validity and reliability

Structured questionnaires designed on a 5 point Likert scale ranging from strongly disagree (1) to strongly agree (5) were used to collect primary data directly from the field which were self-administered by the researcher since most of the SACCO and other MFIs members were of low education level and not comfortable filling the questionnaires by themselves. Borrowers’ characteristics were operationalized using demographic characteristics, ability to pay and assets owned of the borrowers basing on the item scale adapted from Malimba and Ganesan (2009) who conducted a study on the factors influencing loan repayment behaviour of members of savings and cooperative societies in rural Rwanda. Credit terms were operationalized using interest rates, loan period and collateral requirements as adopted from Lehmann and Neuberger (2001) who conducted a study on lending terms to small and medium sized firms in East and West German and modified them to suit the local context. Loan repayment was operationalized in terms of willingness to pay, timeliness and ease of payment basing on the item scale adapted from Moti et al. (2012). To ensure validity, an expert opinion was sought from experts in the field of study to ensure relevance of the items or to establish if the item reflects the real meaning of the concept under consideration (Babbie, 2007). Reliability of instruments was ensured by estimating Cronbach alpha statistics for the scales. The overall Cronbach’s reliability index for borrowers’ characteristics, credit terms and loan repayment performance was 0.733, 0.704 and 0.742, respectively. The results affirm that all the components of the instrument had an acceptable Cronbach alpha greater than 0.7 which indicates that the instrument was reliable (Field, 2009; Kline, 1999).

Model

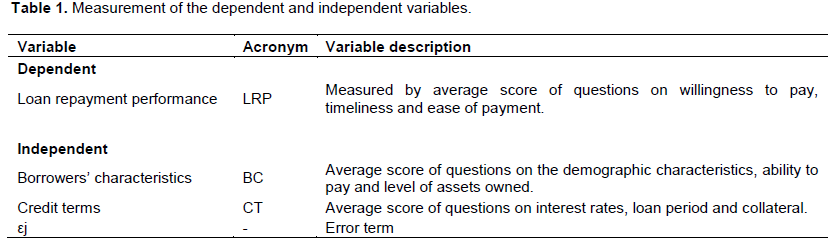

The study utilizes ordinary least squares (OLS) multiple regression model in investigating the effects of borrowers’ characteristics and credit terms on loan repayment performance in MFIs. Given that the dependent variable is not a binary indicator, applying an ordinary least squares estimator would not produce biased results. To examine the association between the borrowers’ characteristics, credit terms and loan repayment performance, we specified the following multiple regression model as explained in Table 1:

LRP = β0 + β1BC + β2CT + εj

RESULTS

Demographic characteristics

The findings indicate that majority of the respondents (77.3%) were female. This implies that most female do not have the size of collateral required to access credit from commercial banks. Considering the level of education, the majority of the respondents, (36.4%) had no education followed by certificate holders (30.7%), diploma 28.4%, degree holders were 3.4%, while master’s degree holders were 1.1%. This education profile is not surprising because generally economic endowment is directly related with education level and this determines whether one will have collateral to access money from commercial banks, absence of which leaves him/her no other option but to seek for credit from MFIs. The results revealed that majority of the respondents (44.3%) were aged between 25 and 29 years, followed by the 30 to 34 year age group (18.2%) and the 35 to 39 year age group (15.9%). This age distribution reveals that the most economically productive persons are in their youth age. When the potential borrowers access credits, they always try and put it to better use for example by engaging in different businesses. This will lead to increased productivity, ownership of assets and the end result will be improved household incomes of the poor people. The marital status of the respondents are that 53.4% were married 23.9% were single, 13.6% were divorced and 9.1 were widowed. This profile is probably because it is the married that have a heavier financial burden since they have families to support and therefore in need to have credit to engage in economic activities from which they can earn a living. Married people also borrow in order to get startup capital. This enables them to engage in businesses which will increase their productivity and eventually their household incomes. The time respondents had spent in business was such that majority (37.5%) was between 5 and 8 years which is long enough for them to have learnt enough lessons regarding access to credit in MFIs and loan repayment experiences.

Exploratory factor analysis

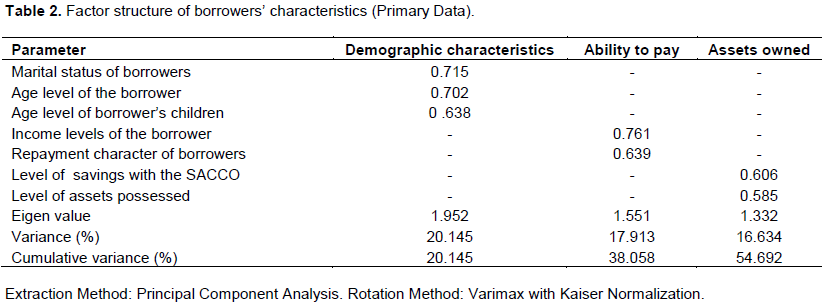

Exploratory factor analysis was used to have those factors that explain better the study constructs through data reduction. According to Field (2009), exploratory factor analysis is used first, to understand the structure of a set of variables, secondly, to construct a questionnaire to measure an underlying variable and thirdly, to reduce a data set to a more manageable size while retaining as much of the original information as possible. Exploratory factor analysis was done by running a rotated component matrix thereby reducing the questions to those that are more relevant to the study variables. Factor analysis was used to examine the most valid borrowers’ characteristics, credit terms and loan repayment performance among MFIs in rural Uganda.

The factor analysis for borrowers’ characteristics from Table 2 revealed three factors, the first factor being demographic characteristics, ability to pay and borrowers’ assets which explained a variance of 20.2, 17.9 and 16.9%, respectively. Demographic characteristics was underscored by marital status of the borrowers (0.715), age level of the borrower (0.702) and age level of the borrower’s children (0.638). Ability to pay was best represented by income levels of the borrower (0.761) and repayment character of the borrowers (0.639). Lastly, borrowers’ characteristics were represented by level of savings with the SACCO and level of assets possessed. So, demographic characteristics, ability to pay and assets owned in total explains 55% of borrowers’ characteristics.

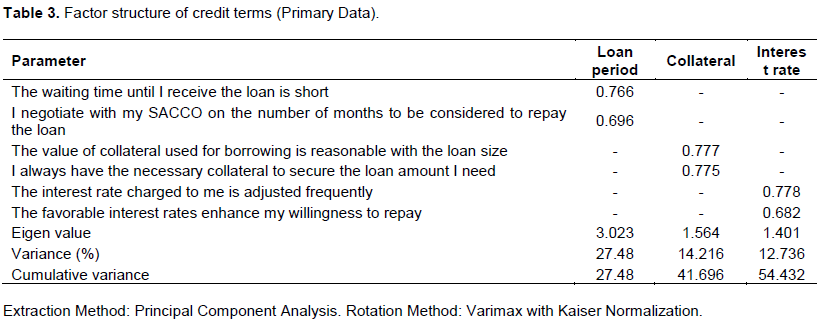

Factor analysis for credit terms

Results in Table 3 revealed the factor structure for credit terms to consist of three factors. In their order of significance, they include loan period (Eigen value = 3.023, Variance = 27.48%), collateral (Eigen value = 1564, Variance = 14.216%) and interest rate (Eigen value = 1.401, Variance = 12.74%), each explaining 27.48, 14.22 and 12.72% variance, respectively. Loan period was underscored by the waiting time before a borrower receives the loan being short (0.766) and the liberty to negotiate the length of the loan period (0.696). The salient items regarding collateral requirement include the value of collateral used for borrowing being reasonable with the loan size (0.777) and the necessary collateral to secure the loan amount one needs (0.775). The pertinent issues with respect to the interest rate were the frequent adjustment of the interest rate charged to the borrowers (0.778) and the favorable interest rates having the ability to enhance the borrowers’ willingness to repay (0.696). Together, loan period, collateral and interest rate explain 54% of the variance in credit terms.

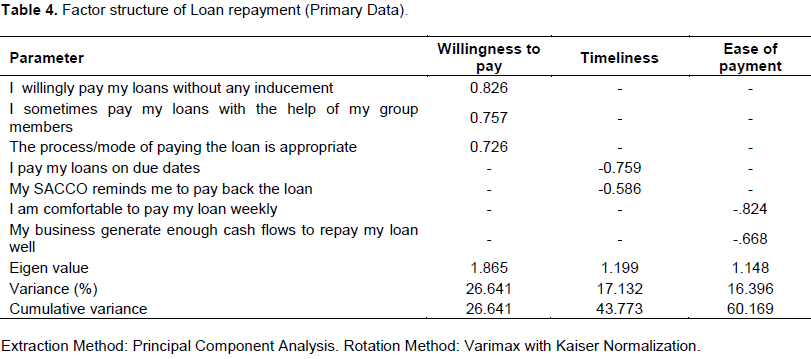

Factor analysis for loan repayment performance

The factor analysis for loan repayment from Table 4 showed that of the three factors; willingness to pay was the most significant, followed by timeliness and lastly ease of payment each explaining a variance of 26.6, 17.1 and 16.2%, respectively. The aspect of willingness to pay was underlined by paying ones loans with the help of his/her group members or with or without inducement and the appropriateness of the mode of payment. Timeliness of payment was underscored by the ability to pay the loans on due dates and the reminders from SACCOs and other MFIs about paying back. Ease of payment consisted of the ability of the borrowers’ businesses to generate enough cash flows to repay their loan well and their ability to pay the loans regularly.

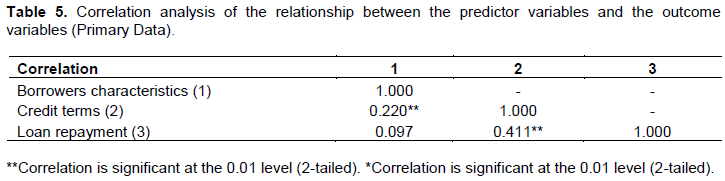

Correlation analysis

Correlation analysis was conducted to establish the relationships between the study variables. Thus, Pearson product moment correlation was used to establish the level of association between the predictor variables and the outcome variable. Pearson correlation coefficient was adopted for this study as it is a parametric statistic and requires interval data for both variables (Field, 2009).

Findings in Table 5 reveal that there was no significant relationship between Borrower's characteristics and Loan repayment (r = 0.097, P>0.05) and thus HI which states that there is a positive relationship between borrowers’ characteristics and loan repayment performance in the Ugandan MFIs is not supported. This is an indication that the borrower's characteristics were not necessarily associated with loan repayment performance. In Uganda, MFIs do not need to waste time evaluating borrowers and assessing them on aspects of marital status, age, income level, education level, work experience and occupation in a bid to improve loan repayment. However, there was significant positive relationship between credit terms and loan repayment (r = 0.411**, P<0.01). This implies that the level of flexibility of the credit terms was directly associated with the level of loan repayment. In other words, when the credit terms in terms of collateral requirement, loan period and interest rate are flexible and not too much straining, the clients also find it easy to repay their loans. This implies that loans officers of various MFIs in Uganda should concentrate on playing around with credit terms to be able to improve loan repayment performance.

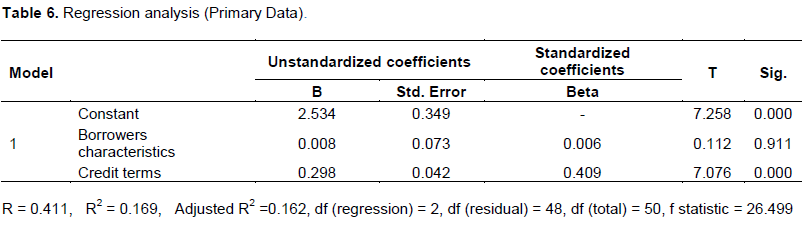

Regression analysis

The regression analysis was carried out to establish the degree of influence of the predictor variables onto the criterion variable as displayed in Table 6. Overall, borrowers’ characteristics and credit terms explain 16% of the variance in loan repayment performance (Adjusted R2= 0.162). However, only credit terms are significant predictors of loan repayment performance. This implies that the more flexible the credit terms are, the more easier clients of MFIs pay their loans. For instance, if clients are at liberty to negotiate the length of loan period or if collateral requirements are within the means of the clients then they would comfortably pay back the loans extended to them on time.

R2 is a measure of how much of the variability in the outcome is accounted for by the predictors (Field, 2009). The adjusted R2 provides an idea of how well the model generalizes the study variables and every researcher would like the Adjusted R2 values to be the same as or close to R2. For this study, the difference for the model is (0.169 – 0.162 = 0.007). The shrinkage of 0.007 (0.7%) means that if the model were derived from the population rather than a sample, it would account for approximately 0.7% less variance in the outcome.

DISCUSSION

According to this study’s results, it is now clear that credit terms are more critical for Ugandan MFIs if they are to recover the monies disbursed to their clients. It is important that the MFIs or even banks to some extent operating in rural areas with loan recovery difficulties may have to adjust their credit terms for example, Atieno (2001), indicates that stringent lending terms discourage borrowers to apply for bank debt even when they are searching for finance to execute valuable investment projects and when they access the loans, they are reluctant at paying back. Similarly, Kakuru (2008) also found that SMEs cannot apply for loans if the credit terms are not flexible. There is need for MFIs for example to shorten the time it takes to process loans for the clients. The logic here is that once an applicant applies for a loan and it is not processed on time, it is likely that it may not serve the intended purpose and in turn the loan amount could be used for other opportunities other than those that were earlier planned and this has a serious impact on loan repayment. There is also need by MFIs to agree on the loan payment period and where possible the loan installment to be paid per month. MFIs have to be careful in aligning collateral security and loan size as well as the interest rates for example according to Zeller (1994), collateral value requirements deter SME borrowers from seeking credit. MFIs do not need to require high valued assets like land for small loan amounts say below US$ 270.

The results suggest that, credit terms are more associated with loan repayment performance. Borrowers’ characteristics have no significant association with loan repayment performance. If loan repayment performance in Uganda is seen through willingness to pay, timeliness in loan repayment and ease of payment of loan installment and interest rates (Moti et al., 2012), it is then difficult to see how individual borrowers’ characteristics like age can affect loan repayment performance. In the African context especially the rural Uganda, it is clear that credit terms is a predictor of loan repayment performance and where credit terms have been carefully formulated and failed, the loans officers in such situations and other company policies relating to mechanisms of loan recovery may be questionable.

The results highlight the need to have better credit terms in place and ensure such credit terms are given full attention. Issues such as marital status of borrowers, age of the borrower, income levels, and repayment character of the borrower, level of savings with the SACCO or MFI and the assets possessed by the borrower may not so much be relied upon as a basis of giving a loan to rural loan applicants. In some MFIs say BRAC Uganda, it was observed that loans are given to groups and in other MFIs where loans are given in groups, loan default was minimal. The non-predictive potential or non-significant association of borrowers’ characteristics and loan repayment performance contradict the findings of Bhatt and Tanga (2011) whose results indicate a positive association between level of education and loan repayment. However, Ifeanyi et al. (2014), studied loan repayment of smallholder cooperative farmers in Nigeria and a negative association was found between age and repayment ability of respondents, implying that younger farmers were more likely to repay credit than older ones. In Uganda, borrowers’ characteristics have no association with loan repayment performance and this is an issue that requires more thinking especially in respect to the different demographic characteristics in different national settings.

CONCLUSION

The objective of this study was to investigate the contribution of borrowers’ characteristics and credit terms on loan repayment performance of MFIs in rural Uganda. Through cross sectional and correlational study design and use of a questionnaire survey of 51 MFIs in Uganda, the study found that credit terms significantly contributes to loan repayment performance of MFIs in Uganda and borrowers’ characteristics is not.

Overall, the findings of this study have important implications for academics as well as policy makers regarding MFIs. For academics, our results suggest that credit terms is more important for loan repayment performance than borrowers’ characteristics, and may be highly effective in reducing problems of loan default and non-sustainability of MFIs. For policy makers like the Government of Uganda, findings are important for regulating MFIs and SACCOs. In Uganda financial institutions are grouped into Tier 1, 2 and 3 which are regulated by Bank of Uganda while Tier 4 is not regulated. The membership of AMFIU includes all microfinance institutions regardless of the tier groupings. SACCOs are strictly in tier 4 and thus they are not regulated by Bank of Uganda. These SACCOs should ideally be regulated by Bank of Uganda.

Like any study, ours also has limitations the reader should be aware of. First, this study was limited to MFIs of Uganda and it is possible that the results are only applicable to Uganda’s MFIs. Secondly, this study was cross sectional thus changes in behavior over time were not monitored. Lastly, the use of the questionnaire may have limited respondents from freely expressing their views since the questionnaire used in this study contained closed ended questions. Future research may thus use longitudinal research designs and employ both the questionnaire and interview guides. Similar researches may also be done in other regions or national settings.

CONFLICT OF INTERESTS

The authors have not declared any conflict of interest.

REFERENCES

|

AMFIU directory (2013). The Uganda Microfinance Directory 2013/2014, 6th Edition, Kampala. |

|

|

Anderson F (2002). Taking a Fresh Look at Informal Finance". Fitchett eds:, Informal Finance in low income countries, Boulder: Westview Press. |

|

|

Atanasova CV, Wilson N (2004). Disequilibrium in the UK corporate loan market, J. Bank. Financ. 28(3):595-614. |

|

|

Atieno R (2001). Formal and informal institutions' lending policies and access to credit by small-scale enterprises in Kenya. AERC Research Paper No. 111, African Economic Research Consortium, Nairobi. |

|

|

Atikus Insurance (2014). Microfinance status report. pp.1-10 |

|

|

Awunyo-Vitor D (2012). Determinants of loan repayment default among farmers in Ghana. J. Dev. Agric. Econ. 4(13):339-345. |

|

|

Ayyagari M, Beck T, Demirgu¨c, KA (2003). Small and medium enterprises across the globe: a new database. Policy Research Working Paper No. 3127. The World Bank, Washington, DC. |

|

|

Babbie ER (2007). The basics of social research. 4th Edition, Belmont, CA: Thomson/Wadsworth |

|

|

Bhatt N, Tang SY (2011). Determinants of repayment in microcredit: Evidence from programs in the United States. Int. J. Urban Regional Res. 26(2): 360-376. |

|

|

Bester H (1987). The role of collateral in credit markets with imperfect information. Eur. Econ. Rev. 31(4):887-899. |

|

|

Besanko D, Thakor A (1987). Collateral and rationing: sorting equilibria in monopolistic and competitive credit markets. Financ. Anal. J. 28(3):671-689. |

|

|

Besley T (1995). Non-market institutions for credit and risk sharing in low income countries. J. Econ. Perspect. 9(3):115-127. |

|

|

Chan Y, Kanatas G (1985). Asymmetric valuation and the role of collateral in loan agreements. J. Money Credit Bank. 17(1):84-95. |

|

|

Cowling M, Westhead P (1996). Bank lending decisions and small firms: does size matter? Int. J. Entrepr. Behav. Res. 2(2):52-68. |

|

|

Field A (2009). Discovering Statistics Using SPSS, 3rd ed., Sage, London. |

|

|

Ifeanyi AO, Idowu AO, Ogbukwa BC (2014). Determinants of Loan Repayment Behaviour of Smallholder Cooperative Farmers in Yewa North Local Government Area of Ogun State, Nigeria: an Application of Tobit Model, J. Econ. Sust. Dev. 5(16):144-153. |

|

|

Kakuru J (2008). The Supply-Demand Factors Interface and Credit Flow to Small and Micro Enterprises (SMEs) in Uganda, University of Stirling, Stirling. |

|

|

Kline P (1999). The handbook of psychological testing, 2nd Ed., London. |

|

|

Kon Y, Storey DJ (2003). A theory of discouraged borrowers. Small Bus. Econ. 21(1):37-49. |

|

|

Krejcie RV, Morgan DW (1970). Determining Sample Size for Research Activities, Educational and Psychological Measurement, 30:607-610. |

|

|

Lehmann EE, Neuberger D (2001). Do lending relationships matter? Evidence from bank survey data in Germany. J. Econ. Behav. Organ. 45(4):339-359. |

|

|

Malimba PM, Ganesan P (2009). Repayment behavior in credit and savings cooperative societies: Empirical and theoretical evidence from rural Rwanda. Int. J. Soc. Econ. 36(5):608-625. |

|

|

Makorere RF (2014). Factors affecting loan repayment behavior in Tanzania: Empirical evidence from Dar es Salaam and Marogoro regions. Int. J. Dev. Sustain. 3(3):481-492. |

|

|

Mann RJ (1997). Explaining the pattern of secured debt, Harv. Law Rev. 110(3):625-683. |

|

|

Morduch J (2006). Smart Subsidies. J. Microfinance/ESR Rev. 8(1):72-85. |

|

|

Moti HO, Masinde SJ, Mugenda NG (2012). Effectiveness of Credit Management System on Loan Performance: Empirical Evidence from Micro Finance Sector in Kenya. Int. J. Bus. Humanities Technol. 2(6):99-108. |

|

|

Mpiira S, Kiiza B, Katungi E, Tabuti JRS, Staver C, Tushemereirwe WK (2014). Determinants of Net Savings Deposits held in Savings and Credit Cooperatives (SACCO's) in Uganda. J. Econ. Int. Financ. 6(4):69-79. |

|

|

Nanayakkara G, Stewart J (2015). Gender and other repayment determinants of micro financing in Indonesia and Sri Lanka. Int. J. Soc. Econ. 42(4):322-339. |

|

|

Nawai N, Shariff MNM (2010). Determinants of Repayment performance in microcredit Programs: A review of literature. Int. J. Bus. Soc. Sci. 1(2):152-161. |

|

|

Nkundabanyanga SK, Kasozi D, Nalukenge I, Tauringana V (2014). Lending terms, financial literacy and formal credit accessibility. Int. J. Soc. Econ. 41(5):342-361 |

|

|

Nyangiru MJ, Maingi J, Muathe SMA (2014). Effect of borrower characteristics to Government funded Micro credit initiatives in Murang'a county Kenya. Int. J. Innov. Res. Dev. 3(11):194-207. |

|

|

Ongena S, Smith DC (2001). The duration of bank relationships. J. Financ. Econ. 61(3):449-475. |

|

|

Pasha SAM, Negese T (2014). Performance of loan repayment determinants in Ethiopian microfinance – An analysis. Eurasian J. Bus. Econ. 7(13):29-49. |

|

|

Qinlan Z, Izumida Y (2013). Determinants of repayment performance of group lending in China: Evidence from rural credit cooperatives' program in Guizhou province, China. Agric. Econ. Rev. 5(3):328-341. |

|

|

Ray S, Mahapatra S (2016). Penetration of MFIs among Indian states: an understanding through macro variables. Int. J. Dev. Issues 15(3):294-305. |

|

|

Roslan AH, Abd Karim MZ (2009). Determinants of microcredit repayment in Malaysia: The case of Agro bank. Humanity Soc. Sci. J. 4(1):45-52. |

|

|

Safavian M, Fleisig H, Steinbuks J (2006). Unlocking Dead Capital: How Reforming Collateral Laws Improves Access to Finance, World Bank, Washington, DC. |

|

|

Shen C (2002). Credit rationing for bad companies in bad years: evidence from bank loan transaction data. Int. J. Financ. Econ. 7(3):261-278. |

|

|

Stiglitz J, Weiss A (1981). Credit rationing in markets with imperfect information. Am. Econ. Rev. 71(3):393-410. |

|

|

Uganda Bureau of Statistics (2015). Statistical abstract. |

|

|

World Bank (2016). Poverty in arising Africa, Africa poverty report. |

|

|

Woolcock MJV (1999). Learning from failures in microfinance: what unsuccessful cases tell us about how group-based programs work. Am. J. Econ. Sociol. 58:17-42. |

|

|

Yehuala S (2008). Determinants of Smallholder Farmers Access to Formal Credit, The Case of Metema Woreda, Haramaya University, North Gondar. |

|

|

Zeller M (1994), "Determinants of credit rationing: a study of informal lenders and formal credit groups in Madagascar. World Dev. 22(12):1895-1907. |

|

Copyright © 2024 Author(s) retain the copyright of this article.

This article is published under the terms of the Creative Commons Attribution License 4.0