Full Length Research Paper

ABSTRACT

This study produces weak and ineffective corporate governance practices in both state owned and privately owned commercial banks in Bangladesh. The paper presents key aspects requiring reforms: the role, constitution and accountability of board, risk management, and transparency. To analyze the corporate governance practices of the private commercial banks (PCBs) and State owned commercial (SCBs), this study focused on four aspects of corporate governance namely; board size, board meeting frequency, audit committee composition, audit committee meeting frequency. Banking performance has been measured through Return on Equity (ROE) and Return on Assets (ROA). To find out the variability in corporate governance, coefficient of variation of the governance indicators of SCBs and PCBs was calculated. The descriptive statistics show that in case of board size greater variability in PCBs but for board meeting frequency and audit committee meeting frequency greater variability exists in SCBs. The trend in write-off of bad debt of PCBs during the period from 2009-2013 is not rising like SCB. On an average, SCBs induce write-off of Tk. 53.16 billion per year whereas PCB decelerates write–off of Tk. 5.52 billion per year. Taken together, our findings suggest that the inferior performance of SCBs in our analysis during the period of 2008–2012 can best be explained corporate governance theory on state ownership of firms and contestable markets perspectives of banking policy mistakes. This paper also brought out some recommendations that need to be improved. Enforcement and monitoring became the main hurdles in establishing the good corporate governance. The accountability of auditors was recommended to ease the corporate governance and financial reporting matter.

Key words: Corporate governance, accountability, state owned commercial bank, private commercial bank, regulatory compliance, non performing loan, write-off.

INTRODUCTION

Corporate governance describes the interaction of government regulators, shareholders, boards of directors, independent observers, auditors, accountants and managers to provide quality information to shareholders, the market, and society at large. Each stakeholder plays an important part to creating an environment where transparency and accountability are encouraged, enforced, and rewarded. Corporate governance is the manner in which power is exercised in the management of a country's economic and social resources for development. Key elements of good corporate governance principles include honesty, trust and integrity, openness, performance orientation, responsibility and accountability, mutual respect, and commitment to the organization.

For Bangladesh, the first step in strengthening the role of stakeholders in corporate governance is raising their awareness regarding these issues. For companies to have sufficient motivation to disclose information and improve governance practices, the relevant stakeholders must place a value on that information and there must be consequences for corporate governance practices. Since the banking sector provides the primary source of capital to business organizations in Bangladesh, any examination of corporate governance practices must examine the role that banks can play in enforcing better corporate governance. In Bangladesh, financial sector is dominated by banks. In terms of share in Gross Domestic Product (GDP), total asset of the banking sector was 65.5 percent of GDP in 2010. The banking sector has flourished during the last three decades or so as a result of increased demand of the growing economy. During this period the banking sector has also undergone several reforms and fallen under the jurisdiction of a number of acts in a bid to improve the efficiency of this sector. However, the sector is yet to improve its performance in terms of trust and confidence of people as shocks hit the sector from time to time in a major way. It has been estimated that the cost of banking inefficiency to the size of the Bangladeshi economy is 1.18% of GDP (using independent estimates of recapitalization requirements).

The most recent development of Bangladesh banking sector include i) Automation and Technological development, ii) Institutional development and iii) Regulatory development. Banking sector experienced remarkable progress in respect of automation in functioning in last several years. For the pro-active and forward-visioning approach of Bangladesh Bank, numbers of automation initiatives have been implemented. Through the Central Bank Strengthening Project, there have been a good number of achievements regarding the institutional development in Bangladesh banks including implementation of Enterprise Resource Planning (ERP), establishment of Enterprise Data Warehouse, Internal networking system etc. Banking industries of Bangladesh have also experienced diversified regulatory developments over last few years, for instance, full implementation of Basel-II (International capital adequacy standard), Guidelines on Environmental and Climate Change Risk Management for banks, Guidelines on Stress Testing for banks etc. All these advancements have been implemented from 2006 to 2012.

Higher credit expansion, increased profitability, lower non-performing assets and increased financial inclusion have contributed to an improved banking system during the past decade. The regulatory framework has supported this growth to a large extent. It is from this ground that the central bank and other regulators frame-works and standards for the financial system of a political economy so that the constituents and participants of the system generate more transparency, accountability, and oversight. Commercial banking sector is very crucial type of participant of the financial system and their compliance to standards and guidelines under the policy frameworks constitute regulatory compliance. On the other hand, such compliance procedures tend to strengthen corporate governance of the banks. For instance, audit standards require banks to submit key information about their financial statement so as to improve the transparency and accountability in the private sector banking industry. Against this backdrop, nonperforming loan is an outbreak of corporate moral hazard that not only proves corporate governance failure but also regulatory governance failure. The empirical results in Dinç (2005) indicate that state-owned commercial banks (SCB) increase their lending in election years relative to private banks in major emerging markets in the 1990s, and these actions are influenced by political motivations other than differences between privately-owned commercial banks (PCB) and SCBs in efficiency and objective.

LITERATURE REVIEW

There is a growing body of research in the economics and management literatures that link general governance factors, such as the pattern and amount of stock owner-ship and board characteristics, with strategic decisions (Bruton et al., 2003; Filatotchev et al., 2002; Hambrick and Jackson, 2000; Tihanyi et al., 2003), and, eventually, corporate performance (Dalton et al., 2003; Daily et al. , 2003; Demsetz and Lehn, 1985; Hansmann, 1996). Little is known about which laws and regulations enhance the governance of banks although many argue that banks are extraordinarily complex and opaque (Morgan, 2002; Caprio et al., 2007). From this perspective, investor protection laws alone may not provide a sufficiently powerful corporate governance mechanism to small shareholders. Official bank regulations may arise in part to stop bank insiders from expropriating or misallocating bank resources as argued in Caprio and Levine (2002). Thus, effective regulation towards more institutional shareholding might augment investor confidence and boost market valuations. On the other hand crisis, volatility and corruption in the banking sector have been found to have negative implications for the growth of the banking industry (Park, 2012; Moshirian and Wu, 2012; Lin and Huang, 2012; Serwa 2010). The US financial crisis has been proved to have occurred due to regulatory governance failures (Anwar, 2009). As opposed to such havocs, the usual good times are generally characterized by opaqueness of either regulatory measures or the corporate management at all levels. Such opaqueness are also termed as failure from two related perspectives corporate governance failure when one or a few firms of an industry are devoid of transparency, accountability, monitoring and oversight of their own managerial practices, and regulatory governance failure when such opaqueness are industry-wide, given that ultimate accountability to the stakeholders remains with the regulators.

In the banking sector corporate governance is the way of business and affairs of the bank by the management and the board, affecting how they define the objectives and goals, lead current bank activities, fulfill the obligation of accountability to shareholders and take into account the interests of stakeholders and apply the requirement to operate safely and to ensure a good financial situation and compliance with applicable regulations; protect the interests of depositors and other clients and creditors. In 1986, the National Commission for Money, Banking and Credit submitted a list of recommendations to address problems in the banking sector that included supervisory handicap and non-performing loan (NPL) criteria set by Bangladesh Bank (BB). In 1990, the Financial Sector Reform Project (FSRP) was initiated to assist BB in implementing the reform measures such as liberalize interest rate, enhance the capacity of loan classification and provisioning, capital restructuring and risk analysis, strengthening central bank and improving the legal system and framework for loan recovery (Bangladesh Bank, 2002). Both the measures have been undertaken on the perspective that the ongoing industrial loan defaults and inherent loan losses have become regular phenomena in Bangladesh and such other developing economies (Hoque and Hossain, 2009). Government dictated the credit disbursement in the late 1990s that has been messed up mainly by political influence on loan approval procedures. Besides, state-owned enterprises (SOEs) also borrowed from the banking sector and these loans were never fully repaid. As Shleifer and Vishny (1997) point out, state-owned firms are technically controlled by the public; they are run by political bureaucrats who can be thought of as having extremely concentrated control rights, but no significant cash flow rights. That is, cash flow rights are dispersed among many taxpayers in a particular country. Political bureaucrats have goals that are often dictated by political interests but in conflict with social welfare improvements and firm value maximization. This theory suggests that the performance of SCBs is inferior to that of PCBs predominantly because of the perverse incentives of managers/bureaucrats of state-owned banks.

A bank’s failure to follow good practices in corporate governance and lack of effective governance are among the most important internal factors which may endanger the solvency of a bank. Banks are subject to special regulations and supervision by state agencies (monitoring activities of the bank are therefore mirrored); supervision of banks is also exercised by the purchasers of securities issued by banks and depositors; problem in principal-agent is more complex in banks, among others due to the asymmetry of information not only between owners and managers, but also between owners, borrowers, depositors, managers and supervisors.

Firm’s corporate governance emblems

BB regulates the operation of banks and financial institutions on the basis of powers vested by the Bangladesh Bank Order 1972 and the Bank Company Act 1991 (as amended to date). It is from this ground that BB, the nation’s central bank generates more transparency, accountability, and oversight. Regulatory governance thus becomes a crucial setting for sound functioning of the banking system to protect the interest of shareholders and depositors and ultimately to monetary policy stability. It is a general belief that good corporate governance enhances a firm performance. A study by Kyereboah-Coleman (2008) shows the effect of corporate governance o n performance of firms. An empirical analysis in Kenya examines the relationship between ownership structure and bank performance (Barako and Tower, 2007). Good corporate governance leads to increased valuation, higher profit, higher sales growth and lower capital expenditure. The good governance in bank may comprise the followings:

Board Size

Usually larger boards are better for firm value because they have a range of expertise to help make better decisions, and are harder for a powerful CEO to dominate. However, some authors have advocated for smaller boards. Fama and Jensen (1983) argue that large boards are less effective and are easier for the CEO to control. When a board gets too big, it becomes difficult to coordinate, encourages free riding and poses problems. Smaller boards, however, reduce the possibility of free riding, and increase the accountability of individual directors. Hence there will be a positive or negative relationship between board size and firm value.

Board diversity

People with a different gender, ethnicity, or cultural back ground might raise questions that would not come from directors with more traditional backgrounds, then diversity increases board independency. A more diverse board might be a more militant board because outside directors with nontraditional characteristics could be considered the ultimate outsider. However, a different perspective may not necessarily result in more effective monitoring because a militant board members may be marginalized.

Board meeting frequency

In the arguments of Fama and Jensen (1983), they pro-pose a very important role for the board as a mechanism to control and monitor managers. The role of the board in an agency framework is to resolve agency problems between managers and shareholders by setting compensation and replacing managers that do not create value for the shareholders. The linkage between board activity and the degree of monitoring is difficult to isolate. Fama and Jensen (1983) argue that boards of well-functioning firms should be relatively inactive and exhibit few conflicts. Frequently scheduled meetings generate costs including managerial time, travel expenses, administrative support and directors’ meeting fees.

Board meeting frequency potentially carries important governance implications as it is less costly to adjust the frequency of its board meetings to attain better governance of the firm, than to change the composition of its board or ownership structure. The association between board meeting frequency and firm value remains unclear. In addition, as a firm’s performance declines, boards are likely to become more actively scrutinized by shareholders and are likely to meet more often to cope with the declining value. The benefits to increased board activity will include more time for directors to confer, set strategy and monitor management.

Audit committee

The growing global acceptance of the Audit Committee (AC) as a relevant governance structure can be linked to claims made in professional and governmental reports about AC benefits on a number of aspects of corporate governance. ACs influence the balance of power in accountability and audit relationships. ACs are perceived as effective mechanisms for reducing agency costs. Some studies (Pincus et al., 1989; Adams, 1997) have found a significant positive relationship between company size and AC formation; others using similar definitions of size have not found any significant relationship (Bradbury, 1990; Collier, 1993; Menon and Williams, 1994). Size has been found to be significant in explaining firms’ decisions to include a separate AC report in the annual report to shareholders but interestingly other agency variables were not found to be associated with such voluntary reporting (Turpin and DeZoort, 1998). Recent studies have reported that independent and active ACs are associated with a decreased likelihood of both fraud and non-fraudulent earnings misstatements, but also that AC size and AC expertise are not significantly related to reduced earnings misstatements (Abbott et al., 2000). It is clear that there is no automatic relationship between the adoption of AC structures or characteristics and the achievement of particular governance effects. AC characteristics are valuable and worthy of promotion but caution may be needed over expectations that greater standardization will deliver guaranteed standard governance contributions (Turley and Zaman, 2004).

Firm performance

Performance may also refer to the development of the share price, profitability or the present valuation of a company. Bank performance is the bank profitability and productivity in banking. Velnampy and Nimalathasan (2008) examined firm size on profitability between Bank of Ceylon and Commercial Bank of Ceylon in Sri Lanka during ten years period from 1997 to 2006 and found that there is a positive relationship between firm size and profitability in Commercial Bank of Ceylon Ltd., but there is no relationship between firm size and profitability in Bank of Ceylon. The existing literature on corporate governance practices has used accounting-based performance measures, such as return on equity (ROE) and return on assets (ROA).

METHODOLOGY

This research is characterized as exploratory and descriptive in nature. This paper aims to present the specificity of the corporate governance of banks and indicates the main deficiencies in the bank governance system. The main research methods used in the study are the review and critical analysis of literature and study of the regulations; based on that, a method of logical deduction has been applied; the analysis of numerical data presented (based on case studies retrieved from literature and financial analysis of banks’ aggregate data) allow for an illustration of the issues discussed. The methodologies of the present study are outlined below.

Sample

The sample for this study is the state and private sector banking organizations of Bangladesh. For the research study three state banks (Agrani Bank Ltd., Janata Bank Ltd. and Rupali Bank Ltd.) and three private banks (Prime Bank Ltd. Dutch Bangla Bank Ltd. and Dhaka Bank Ltd.) have been selected as per the convenient sampling. Other private commercial banks were not included in this study due to insufficient information regarding the research topic of this study.

Data sources

In order to meet the objectives and hypotheses of the study, data are collected from secondary source mainly from financial report of the selected banks as the sources of samples data for the sample period of the year 2013. Furthermore, this research only focuses on the directors’ reports, balance sheet, and income statements in their annual reports which are regularly updated in the official websites of the respective institutions.

Mode of analysis

In the present study, we have analyzed our data by calculating covariance of different corporate governance indicators. For testing hypothesis we have calculated standard deviation and standard error of ROE of both SCB and PCB. Time series analysis of write-off bad debt loans of SCB and PCB (from 2009 to 2013) was also done.

RESULTS AND DISCUSSION

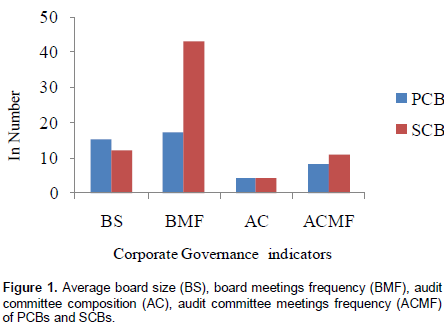

To analyze the corporate governance practices of PCBs and SCBs, we look at the pattern of governance changes of countable indicator i.e. in board size, board meetings frequency, audit committee composition, audit committee meetings frequency as shown in Figure 1.

There are two crucial deviations in governance of PCBs in Bangladesh, viz, appointment of independent directors, and setting the audit committee absent with directors. Of the sample of PCBs, no board has independent director(s) appointed from outside the organization. Moreover, the audit committee of every PCB is headed by one or two directors of the firm. It has long been recognized that board composition is very important with respect to the ability to monitor and is related to the reduction of agency costs (Fama and Jensen, 1983). Although there is a controversy surrounding the efficacy of outside directors in exercising effective corporate oversight (Byrd and Hickman, 1992), outsiders have the potential to exercise devil’s advocacy and to use dialectic enquiry approaches towards more crucial decisions aided and guided by fresh ideas, independence (lack of cohesiveness), objectivity, and expertise gained from their own fields (diversity).

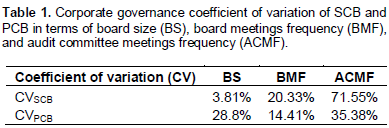

To find out the variability in corporate governance coefficient of variation of the governance indicators of SCBs and PCBs have been calculated. The results of the analysis are summarized in the Table 1.

The descriptive statistics produced in Table 1 show that in case of BS greater variability in PCBs but for BMF and ACMF greater variability exists in SCBs. Since these variables are explanatory governance variables, directors’ remuneration growth is very high followed by institutional shareholding. The reason(s) underlying so high remuneration volatility is ambiguous. From the annual reports of the respective banks it has been found that the members in all the audit committees are also members of their board for which good governance is in doubt.

Hypotheses development

Ho = Corporate governance failure does not affect the performance of the bank

Ha = Corporate governance failure affect the performance of the bank.

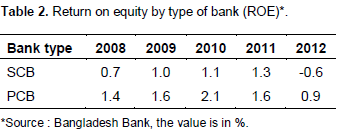

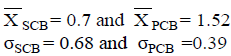

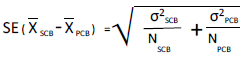

To test the hypothesis, we calculate standard deviation and standard error of ROE of Both SCB and PCB from the year 2008 to 2012. The data of ROE are shown in Table 2.

From the above data,

Standard error (SE) of the difference in the mean of two samples is,

i.e. the difference in the mean of two samples is = 2.34

Since, the difference is more than 1.96 SE (at 5% level of significance), it does not support the hypothesis i.e. corporate governance failure affects the performance of the bank.

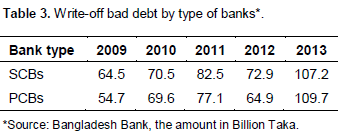

Write-Off condition of bad debts in SCBs and PCBs

Write-off bad debt conditions by SCBs as well as PCBs of our study are shown in Table 3.

From the time series analysis we get the equation as follows:

YSCB = 53.16 +8.78t and

YPCB = - 5.52 +23.93t

where, Y = write-off (in Billion Tk.), t =Time (Year)

The above equation means that on an average SCBs induced write-off of Tk. 53.16 billion per year. The inter year variation in write-off by SCBs is measured in terms of Billion Tk. 8.78. There has been rising trend in write-off of bad debt during the period from 2009-2013 by considering the base year 2008 and sustain positive trend during the period.

In case of PCBs, it averagely decelerates write-off of Tk. 5.52 billion per year. The inter year variation in write-off by the PCBs is measured in terms of Billion Tk. 23.93. The trend in write-off of bad debt during the period from 2009-2013 by considering the base year 2008 is not rising as it does in SCBs.

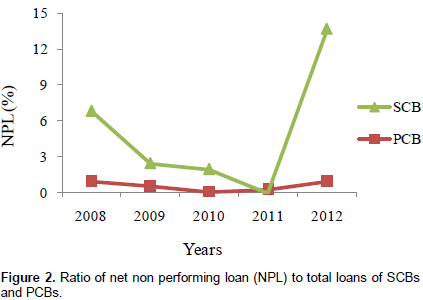

Usually it is anticipated that non-performing loans should decrease if corporate governance is effective. However, from the analysis of our study, it is ascertained that NPL of SCBs increase every year in a large volume. Although it was the lowest in 2011, it got the highest position in 2013; whereas in PCB the tendency is increasing but the rate is not as high as SCB (Figure 2). The way committees of the banks are been constituted, members of audit committee in Bangladesh are mixed, that is both finance and none finance members constitute the committee. This can affect the way the committee discharges its functions. The reason for sacking the Managing Director/Chief Executives and Executive Directors of the banks by the Central Bank of Bangladesh that the banks’ officials were removed due to high level of non-performing loans in the banks which was attributable to poor corporate governance practices, lax credit administration processes, and absence or non-adherence to the banks’ credit management practices.

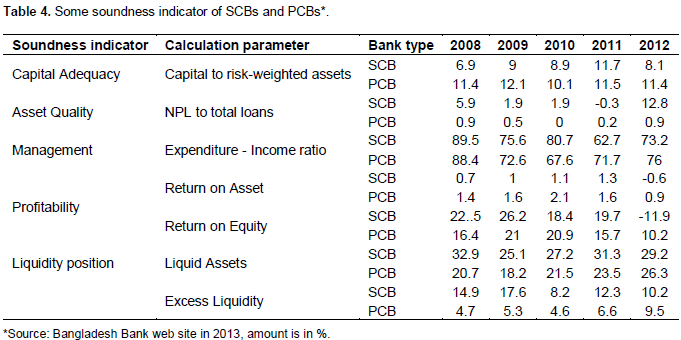

Soundness indicator of SCB and PCB

Soundness of the banking sector, which basically reflects on the quality of performance of the sector, is measured by indicators such as capital adequacy, asset quality, management quality, earnings and liquidity position.

From Table 4 the soundness indicators of these two types of banks show that the performance of the SCBs is weaker than PCBs. Even though there have been improved performances the SCBs continue to be grappled with problems of inefficiency and solvency. Thus the seemingly good performance does not capture the reality which raises elements of doubts as regards the real health of SCBs.

The major findings as revealed from the study are as under:

1. A number of unwanted and abnormal cases by the board of the bank have been identified including pressure exerted by powerful sections, corrupted alliance between senior managers of the bank and clients, lack of super-vision from the head office, and absence of oversight.

2. As the state is more powerful and does not adequately share information with minority shareholders, independent directors have significant influence on the decision making process of the board in case of SCBs.

3. PCBs relied more on loans than SCBs to generate interest income which is alike our study similar to the findings of Dinç (2005).

4. The performance of SCBs is relatively of lower rank of importance due to the perverse incentives of their managers.

5. The current system in Bangladesh does not provide sufficient legal, institutional or economic motivations for the stakeholders to encourage and enforce good corporate governance practices.

6. The combination of banking practices and legal inefficiencies with regard to financial issues has put the condition of the banking sector in serious doubt.

7. It is noteworthy that statutory and prudential regulations for good corporate governance have been circulated in the banks. However, widespread misappropriation by the directors of PCBs in taking loans and other illegal benefits from the bank is still prevalent.

8. Illegally opened local back to back L/Cs and provided acceptance to documents raised by different banks in favour of non-existent organization.

The banking sector is now more discreet and vivacious. It is shown that the central bank cannot identify or take action against cheats unless the audit departments convey their findings properly.

RECOMMENDATIONS

Corporate governance is concerned with the structures and processes associated with, for example, production, decision-making and control within an organisation. Accountability, which is a sub-set of governance, involves the monitoring, evaluation and control of organisational agents to ensure that they behave in the interests of shareholders and other stakeholders (Keasey and Wright, 1993).

Most government accountability methods have been limited to external control methods aimed at securing compliance in the legal, political and hierarchical dimensions (Dicke and Ott, 2002). To ensure accountability and to provide good governance in the banking sector in Bangladesh following proposal can be suggested:

1. It is the time to strengthen the regulatory capacity in order to bring stability in the banking sector by empowering the central bank.

2. It is important to strengthen the risk management policy, making the board of directors free from political influence, providing more autonomy to the central bank and demanded exemplary punishment to the persons responsible for the scam and to take measures to recover the embezzled fund immediately.

3. Fortifying the inspection and audit department and better coordination among audit, inspection and surveillance department of the central bank are required.

4. A separate department to deal with financial crimes is required.

5. The PCBs should not sign the improper internal control and compliance reports before sending it to the Bangladesh Bank.

6. Strengthening the surveillance activities on the boards of directors of the scheduled banks by the Bangladesh Bank is suggested.

7. Targeted reforms in institutions or sectors can begin to provide the internal and external motivation for transparency and accountability that will lead to better corporate governance.

8. To achieve the required level of compliance, the Bangladesh Bank should issue instructive circulars and develop a training module for bank personnel.

9. International Accounting Standard (IAS-30) has to be adopted quickly as completely as possible for better disclosure of information.

10.Monitoring and follow-up of loans should be strengthened and the borrowers should be given early signals before the problem goes out of controls.

These suggestions are made to ensure a sound and sustainable growth of the banking sector of the country. Three essential actions can be taken to improve corporate governance in Bangladesh. First, a high powered committee including members from government, regulatory agencies, companies, and ICAB should write a code for corporate governance in Bangladesh. Second, amendments to existing laws should be adopted to enforce corporate governance norms. Third, academic and professional institutions should include corporate governance principles in their syllabi. In addition, the author encourages institutional investors to exercise their influence and discourage nominee directors from the Government of Bangladesh and financial institutions.

CONCLUSION

To move from the agriculture based economy to an industry-based one, Bangladesh needs its banking sector, which is the single largest element of the financial sector, to operate at its best with utmost efficiency. Sound corporate governance remains to be a key requirement for efficient and stable banking system. Better governance helps lower poverty and improves living standards. Usually SCBs take a more active role in financing the government itself relative to PCBs. Over the last few years the banking sector of Bangladesh has made significant progress with regard to corporate governance indicators. However, a collective performance of the indicators for SCBs and PCBs shows that the performance of the SCBs has been weaker than PCBs. Even though there have been improved performances the SCBs continue to be grappled with problems of inefficiency and solvency. Thus the seemingly good performance does not capture the reality which raises elements of doubts as regards the real health of SCBs. The application of good corporate governance practices to the state owned enterprises could, therefore, have a significant effect on the economy, but at present the concept or practice of corporate governance is almost non-existent in state owned enterprises as well as in private companies. Each corporate governance stake-holder should play an important part to create an environment where transparency and accountability are encouraged, enforced, and rewarded. The report is a diagnostic tool from which a consensus can emerge regarding the way forward for corporate governance in Bangladesh. To make the corporate governance mechanisms work, we need to establish an enabling environment first, and this is only possible through top-level commitment to provide good governance in the corporate level. Equal treatment and rights of all share-holders would bring about much positive disciplinary change in the banks.

CONFLICT OF INTERESTS

The author has not declared any conflict of interest.

REFERENCES

| Abbott LJ, Park Y, Parker S (2000).The effects of audit committee activity and independence on corporate fraud. Manag. Fin. 26(11): 55–67. | ||||

|

Adams M (1997). Determinants of audit committee formation in the life insurance industry: New Zealand evidence. J. Bus. Res. 38(2): 123–129. Crossref |

||||

| Anwar GMJ (2009). The US financial crisis from 2007: Are there regulatory and governance failure? J. Bus. Pol. Res. 4(1), 25-49. | ||||

| Bangladesh Bank (2002). Policy on capital adequacy of banks, BRPD circular No. 10, November 25. [Online] Available: http://www.bangladesh-bank.org/mediaroom/guide_regul/prudential_regulations.html#bkt1 | ||||

| Barako DG, Tower G (2007). Corporate governance and bank performance: Does ownership matter? Evidence from Kenyan banking sector. Corp. Own. Contr. 4(2): 133-144. | ||||

|

Bradbury ME (1990). The incentives for voluntary audit committee formation. J. Acc. Pub. Pol. 9: 19-36. Crossref |

||||

|

Bruton G, Ahlstrom D, Wan J (2003). Turnaround in East Asian firms: evidence from ethnic overseas Chinese communities. Strat. Manag. J. 24, 519-540. Crossref |

||||

|

Byrd J, Hickman K (1992). Do outside directors monitor managers?: evidence from tender offer bids. J. Fin. Econ. 32: 195-221. Crossref |

||||

| Caprio G, Laeven L, Levine R (2007). Ownership and bank valuation. J. Fin. Int. 16, 584-617. | ||||

| Caprio G, Levine R (2002). Corporate governance in finance: concepts and international observations. In: Litan RE, Pomerleano M, Sundararajan V (Eds.), Financial Sector Governance: The Roles of the Public and Private Sectors. Brookings Institution Press, Washington, DC, pp. 17–50. | ||||

| Collier P (1993). Audit committees in major UK companies. Manag. Aud. J. 8(3): 25-31. | ||||

|

Daily C, Dalton D, Rajagopalan N (2003). Governance through ownership: centuries of practice, decades of research. Acad. Manag. J. 46: 151-158. Crossref |

||||

|

Dalton D, Daily C, Certo S, Roengpitya R (2003). Meta-analysis of financial performance and equity: fusion or confusion? Acad. Manag. J. 46: 13-26. Crossref |

||||

| Demsetz H, Lehn K (1985). The structure of corporate ownership: causes and consequences. J. Pol. Econ. (93): 1155-1177. | ||||

|

Dicke LA, Ott S (2002). A Test: can stewardship theory serve as a second conceptual foundation for accountability methods in contracted human services? Int. J. Pub. Adm. 25(4), 463-487. Crossref |

||||

|

Dinç S (2005). Politicians and banks: political influences on government-owned banks in emerging markets. J. Fin. Econ. 77: 453-479. Crossref |

||||

|

Fama E, Jensen M (1983). Separation of ownership and control. J. Law. Econ. (26): 301-325. Crossref |

||||

|

Filatotchev I, Buck T, Zhukov V (2002). Downsizing in privatized firms in Russia, Ukraine, and Belarus. Acad. Manag. J. 43: 286-304. Crossref |

||||

|

Hambrick D, Jackson E (2000). Outside directors with stake: The linchpin in improving governance. Cal. Manag. Rev. 42: 108-127. Crossref |

||||

| Hansmann H (1996). The ownership of enterprise. Harv. Univ. Press: Cambridge MA, pp 372. | ||||

| Hoque MZ, Hossain MZ (2009). Impact of interest rates on loan defaults: experience from a developing country. Glob. Econ. Fin. J. 2(1): 172-186. | ||||

|

Keasey K, Wright M (1993). Issues in corporate accountability and governance. Acc. Bus. Res. 23(91A): 291-303. Crossref |

||||

| Kyereboah-Coleman A (2008). Corporate governance and firm performance in Africa: a dynamic panel data analysis. J. Stud. Econ. Econometr. 32(2): 1-24. | ||||

|

Lin PC, Huang HC (2012). Banking industry volatility and growth. J. Macroecon. 34: 1007-1019. Crossref |

||||

|

Menon K, Williams JD (1994). The use of audit committees for monitoring. J. Acc. Pub. Pol. 13: 121-139. Crossref |

||||

|

Morgan D (2002). Rating banks: Risk and uncertainty in an opaque industry. Am. Econ. Rev. 92: 874-888. Crossref |

||||

|

Moshirian F, Wu Q (2012). Banking industry volatility and economic growth. Res. Int. Bus. Fin. 26: 428- 442. Crossref |

||||

|

Park J (2012). Corruption, soundness of the banking sector, and economic growth: a cross-country study. J. Int. Mon. Fin. 31(5): 907-929. Crossref |

||||

|

Pincus K, Rusbarsky M, Wong J (1989). Voluntary formation of corporate audit committees among NASDAQ firms. J. Acc. Pub. Pol. 8: 239-265. Crossref |

||||

|

Serwa D (2010). Larger crises cost more: impact of banking sector instability on output growth. J. Int. Mon. Fin. 29: 1463-1481. Crossref |

||||

|

Shleifer A, Vishny RW (1997). A survey of corporate governance. J. Fin. 52: 737-783. Crossref |

||||

|

Turley S, Zaman M (2004). The corporate governance effects of audit committees. J. Manag. Gov. 8: 305-332. Crossref |

||||

|

Tihanyi L, Johnson R, Hoskisson R, Hitt M (2003). Institutional ownership differences and international diversification: the effects of boards of directors and technological opportunity. Acad. Manag. J. 46: 195-211. Crossref |

||||

|

Turpin RA, D-eZoort FT (1998). Characteristics of firms that include an audit committee report in their annual report. Int. J. Aud. 2: 35-48. Crossref |

||||

| Velnampy T, Nimalathasan B (2008). An association between organizational growth and profitability: a study of commercial bank of Ceylon ltd, Sri Lanka. Annals of University of Bucharest, Econ. Adm. Series. 2: 46-57. | ||||

Copyright © 2024 Author(s) retain the copyright of this article.

This article is published under the terms of the Creative Commons Attribution License 4.0