Full Length Research Paper

ABSTRACT

Economic policies in every nation strive to attain basic macroeconomic goals, one of which is poverty reduction. The paper examines empirically whether or not financial deepening has played a significant role in poverty alleviation effort in Nigeria for the period 1990 to 2013. Utilizing both quantitative and descriptive analyses, the paper estimated three models in which poverty rates for the rural areas, urban areas as well as national poverty rates were regressed on financial development indicators. Based on the estimated parameters, the paper found that the coefficient of ratio of broad money supply to GDP reduces poverty rate in Nigeria. The ratio of market capitalization to GDP and ratio of foreign direct investment in equities to GDP have positive impact on rural and urban poverty reduction respectively. However, the ratio of credit to the private sector and the ratio of total stock traded to GDP revealed opposite impact on poverty alleviation at all levels. The descriptive analysis indicated that poverty rate in Nigeria has been unacceptably high in spite of abundant natural and human resources. The paper therefore, recommends the need for urgent reforms in the financial sector that would facilitate development in both the money and capital markets to improve liquidity; reduce interest rate spread to attract deposits and broaden financial access to the poor.

Key words: Poverty rate, financial deepening, ordinary least squares(OLS).

INTRODUCTION

The basic macroeconomic policies of any nation are aimed at achieving all or some of the following: sustained and irreversible economic growth, reduction of inequality, full employment equilibrium, price stability, balance of payment equilibrium and exchange rate stability. These goals play complementary rather than conflicting roles. The overall target of the policies is to improve the wellbeing of the citizenry on a continuous basis.

These goals are usually pursued through well coordinated monetary and fiscal policies of government. The potency and effectiveness of monetary policy in the attainment of these goals depends to a large extend on the level of financial development (deepening) of a nation. Central to these macroeconomic goals to the state is the protection of life and property of its citizens. The responsibility of protection of life and property can be direct which involves investment in institutions like the police force, judiciary and defense. The indirect protection comes in the form of provision of enabling environment and opportunities for the citizens to achieve their full potentials, thereby improving their living standard and guaranteeing the dignity of men. Macroeconomic goals fall under the indirect responsibility of government.

It is the differences in governments’ commitment to its responsibilities that differentiate the developed nations from the developing nations. The countries which are referred to as backward or developing are so designated because they are economically, politically and socially behind the developed countries. Specifically, they are, in the opinion of Todaro (1997) and Jhingan (2002), characterized by persistent high incidence of absolute poverty, low levels of income per capita, consumption, as well as high mortality rates, administrative incompetence and high dependence on foreign advanced economies. It is widely believed that poverty is largely responsible for the persistence of these characteristics in developing countries. According to Abimiku (2009), this explains why eradicating poverty has not only been seen as the most important goal of human wellbeing but also, removal of hunger, disease and provision of productive employment for all are also an important aspect of poverty reduction.

It is possible to measure poverty statistically by establishing a line expressed in terms of per capita income below which the individual or group concerned encounters unacceptable difficulties in satisfying the basic needs of life. Naturally, the poverty line varies in relation to the general level of development. What is poverty for one may be wealth for another. In developing economies, an adult daily expenditure below two dollars ($2) is considered as living under the poverty line (International Monetary Fund, 2012).

On the material level, in terms of the distribution of monetary income as the basis of purchasing power in a monetized economy like Nigeria, it has been uneven. At the global level, inequality between nations and within nations has created a social pyramid where the poor are at the base and the minute rich individuals are at the top. Eradication of absolute poverty seems a fruitless effort; as stressed by Bartoli (1991) who observed that, failure to find a cure for poverty, ignorance and death, men have decided, for their own peace of mind, not to think about them. However, the social upheavals and tensions occasioned by perverse poverty suggest that the more men refuse to look for solutions, the more their peace of minds and happiness are jeopardized.

Absolute poverty level in Nigeria has remained persistently above 50% in spite of the nation’s enormous wealth (a situation described as a paradox). Between 1994 and 2012, the number of people living below the poverty line continues to rise (Nnadozie, 2012). While poverty level in Nigeria stood at 67% in 2013, data for China, Brazil, Singapore, South Korea, Taiwan, Indonesia, Malaysia, South Africa and Ghana for the period 2007 and 2013 revealed that poverty level in these countries range from 1.5% in Taiwan to 31.3% in South Africa; with Kenya having 43.4% of its population in poverty as at 2013 (Abimiku, 2014)

Financial development is considered an integral factor in the economic growth of a country. A well functioning financial system that mobilizes saving, allocates resources and facilitates risk management contributes to economic growth by supporting capital accumulation, improving investment efficiency, generates employment opportunities, increases output/income and reduces poverty, all things being equal.

However, the relationship between finance and poverty reduction is neither direct nor automatic as it has to affect other targets through monetary policy transmission mechanism. These targets according to Mbutor (2009) include interest rates, exchange rates and credit channels, which have implications and impact for/on the availability, direction and cost of credit and ultimately poverty level of the people. Governments in developing countries use monetary policy to achieve economic growth that includes equitable income distribution and poverty reduction. In other words, economic growth can be grouped into either growth with rising income inequality and poverty, or growth with falling income inequality and poverty (Beck et al., 2007). The differences between these two can alter the impacts of growth on the poor.

According to Inoue and Hamori (2010) if financial development increases average growth, only by increasing the incomes of the rich and hence worsening income inequality, then financial development has not helped the poor. This is the case with Nigerian economy whose rebasing in 2014 indicated that it is the largest economy in Africa with hundreds of billions of Naira declared as profits by financial institutions while more than 50% of Nigerians are living in poverty.

Poverty reduction is at the centre of development agenda of every nation, Nigeria inclusive. Regrettably, in spite of several reforms in the financial sector couple with the relative improvement in financial deepening indicators, these have not translated to poverty reduction in Nigeria. It is on the basis of the foregoing that this paper seeks to investigate whether financial deepening matters in poverty reduction efforts in Nigeria. In order to achieve this, the paper is structured into five sections: section one is the introduction; section two deals with literature review; section three contains the methodology; while sections four and five discuss the findings and recommendations respectively.

LITERATURE REVIEW

Financial deepening is defined as an increase in the size of financial system and its role and pervasiveness in the economy. From the monetary policy perspective, the growing diversification of firms’ and households’ portfolios is especially relevant, as they are more affected by the developments in the financial markets (Visco, 2007). Also, Shaw (1975) refers to the financial deepening as increased provision of financial services with a wider choice of services geared to all levels of society. In other words, it implies an increased ratio of money supply to gross domestic product (GDP). Financial deepening results to financial liquidity. The more liquid money is available in an economy, the more opportunities exist for continued growth as well as improvement in material wellbeing of the citizenry (poverty reduction)

Poverty, on the other hand, describes a condition in which individuals, families or groups are considered to be in want and lack the resources, particularly real income to obtain the types of diets needed to enjoy some fixed minimum standard of living determined by a given society. This minimum standard of living considers some amount of goods and services essential and those who are unable to obtain them are said to be poor (Miller, 1968; Wedderburn, 1974; Plotnick and Skidmore, 1978; Schiller, 1976; Abimiku, 2006).

Financial deepening and financial inclusion work hand in hand. A shallow financial sector lacks the depth to include or accommodate a large spectrum of financial investors and economic agents, thereby resulting in financial alienation for the poor. Financial inclusion and financial deepening play an important role in promoting economic growth and reducing poverty while mitigating systematic risk and maintaining financial stability. However, the focus of this paper is financial deepening.

A growing body of empirical research reveals remarkable consistent results that the services provided by the financial system create a first order impact on long run economic growth. Based on the pioneering work of Bagehot (1873) and Schumpeter (1912), recent researches have produced a key result that countries with better developed financial systems tend to grow faster in terms of income and poverty reduction than those with underdeveloped financial system. Financial services and financial development (as measured by the size of the intermediary sector) stimulate economic growth by increasing the rate of capital accumulation and by improving the efficiency with which economies use that capital in current period as well as in the future (King and Levine, 1993).

Local financial development enhances the probability that an individual starts business, increases industrial competition, widens consumers’ choice for goods and services at competitive price, thereby improving economic and social welfare of the people. For a household, financial deepening offers better and cheaper services for saving money and making payments by allowing firms and households to avoid the cost and waste associated with barter or cash transactions, cutting remittance costs and providing the opportunity for asset accumulation and consumption smoothing (Balackrishman et al., 2013). Thus, it is expected to further improve access to credit for the poor. This is the connection between financial deepening and financial inclusion.

Financial deepening, according to Clarke et al., (2006), not only promotes economic growth but can also help distribute financial resources more evenly. Certain forms of financial development, particularly those that broaden access to finance, can benefit the poor disproportionately by increasing capital flow and increasing efficiency of capital allocation, thereby reducing inequality and poverty in the society (Beck et al., 2007).

Again, better access to credit by the poor, which is both a component of financial deepening and inclusion, enables the poor to pull themselves out of poverty by investing in their human capital and micro-enterprises, thus reducing aggregate poverty (Benerjee and Newman, 1993; Galor and Zeira, 1997; Aghion and Bolton, 1997). This argument is consistent with the AK version of endogenous growth theory advanced by DeGrejorio (1997) which argues that financial liberalization and development increase the quality of human capital by financing education to financially constrained households (the poor) and, by extension, increase their productivity and income.

Ayyagari et al. (2013) submitted that financial development has a significant impact on poverty reduction through channels such as: entrepreneurship and inter-state migration (labour mobility of workers) toward financially more developed states and blue chip enterprises. Although the paper is not on poverty and entrepreneurship, finance affects poverty through entrepreneurship channel as observed above. It is on the basis of this that Abimiku (2014) observed that emerging economies like Brazil, China, Indonesia, Taiwan, South African etc. have been able to drastically reduce poverty, unemployment and inequality and their resultant effects due largely to the growth of the entrepreneurial class supported by a relative sound and developed financial sector.

There has been increasing number of empirical studies on the effects of financial deepening on poverty reduction. For example, Jalilian and Kirkpatrick (2008) examined whether financial deepening can contribute to the goal of poverty reduction in many developed and developing countries including India. Their study incorporates three distinct research approaches. These are the link between financial development and economic growth, the link between economic growth and poverty as well as the link between financial development and inequality. By estimating each link separately, they concluded that financial development helps to reduce poverty; the results indicate that a unit of change in financial development improves the income growth prospects of the poor by almost 0.3%.

In the same vein, Beck et al. (2007) analyzed the impact of financial deepening on the poor by estimating the relationship between finance and changes in both income distribution and poverty levels, because financial development may affect the poor through both aggregate growth and changes in income distribution. The result reveals that an increase in financial development lowers income inequality, increases the income of the relatively poor disproportionately and is strongly associated with poverty alleviation. These studies were conducted with large sample from different countries.

However, there have been studies on the relationship between finance and poverty within individual countries. For instance, Quartey (2008) investigated the inter-relationship between financial development, savings mobilization and poverty reduction in Ghana from 1970 to 2001. The pair wise granger causality test shows that financial development (ratio of private credit to GDP) Granger-causes poverty reduction. Odhiambo (2009) examined the relationship among financial development, economic growth and poverty reduction in South Africa from 1960 to 2006 using a trivariate causality test based on an error correction model. The causality result indicates that financial development (M2/GDP) and economic growth cause an increase in per capita consumption (a proxy for poverty reduction) and that economic growth causes financial development.

Furthermore, Inoue and Hamori (2010) investigated the effects of financial deepening on poverty reduction in India using unbalanced panel data for 28 states and union territories between 1973 and 2004. From the dynamic Generalized Method of Moments (GMM) estimation, they found that financial deepening and economic growth alleviated poverty in India and separately, in urban areas and rural areas. In Nigeria, there has been little or less attention paid to researches on the relationship between financial development and poverty reduction.

The study that comes close to this is a study by Onwumere (2007) on the impact of capital market on poverty alleviation in Nigeria. The paper was more of a proposal on how capital market could be used as a tool for poverty alleviation; it has no methodology and, therefore, lacks empirical findings. Also, Ugiagbe and Edegbe (2015) identified globalization as being responsible for the financial exclusion of the poor in Nigeria, especially farmers who receive $2, 000 for a ton of dried cocoa pods/seeds exported abroad and pay $10, 000 for the processed imported chocolate and bounvita; a bi-product of cocoa they exported.

This paper differs from the reviewed literature in the following ways. First, there is no empirical work on Nigeria’s data. Secondly, the variables used in this paper include the money market, capital market and international financial integration indicator. These made this paper broader in terms of variables, unique and novel.

METHODOLOGY

The paper employs both descriptive and quantitative analyses using secondary data to investigate the impact of financial deepening on poverty reduction in Nigeria. The descriptive analysis use graphical presentation on poverty trend in Nigeria for the period between 1990 and 2013. On the other hand, the quantitative analysis is based on the classical ordinary least squares regression (OLS) technique. This method of analysis is suitable when investigation requires estimating the coefficient of parameters of a linear model because of its properties of; Best, Linear Unbiased Estimator (BLUE) (Gujarati, 2006).

The regression model used to determine the magnitude of the estimated coefficients of financial deepening on poverty reduction in the rural, urban and national levels in Nigeria involved three equations. The equation for rural poverty and financial deepening is presented as follows:

RPR = ao + a1RM2/GDPt-1 + a2RCP/CGPt-1 + a3RMC/GDPt-1 +a4RST/GDPt-1 +a5 RFE/GDPt-1 …………………. (1)

Where

RPR = Rural poverty rates

RM2/GDP = ratio of broad money supply to GDP

RCP/GDP = ratio of credit to the private sector to GDP

RMC/GDP = ratio by stock market capitalization to GDP

RST/GDP = ratio of total stock traded to GDP

RFE/GDP = ratio of foreign direct investment in equities

Ut = error term

The estimated parameters a1, a2 ……. a5 are expected to be less than 0 (a1, a2 ……. a5 < 0) on a priori grounds. Theoretically, we expect financial development to have negative impact on the growth rate of rural poverty.

Poverty rate is one of the economic development indicators. A declining rate of poverty, inequality and unemployment on a sustained basis is an indication that the economy is on the path of sustained development (Eneji, 2014).

Ratio of broad money supply to Gross Domestic Product (GDP) and ratio of credit to the private sector to Gross Domestic Product (GDP) are measures of banking sector development (Money market). Two of stock market development and activities are also used in this paper. First, ratio of market capitalization to gross domestic product is the total value of all shares in the stock market as percentage of GDP; it measures the size of the stock market in relation to the economy. Second, the ratio of value of stock traded to gross domestic product is the value of all shares traded in the stock market as percentage of GDP. It measures how active and liquid the stock market is as a share of the economy (Rioja, 2014).

The third category of variables is the ratio of foreign direct investment in equities to gross domestic product (FD/GDP). This ratio measured the degree of capital market integration to international financial institutions. It equally measures the ease with which foreign investors access the Nigerian capital market and also the ease with which local firms access financial capital from foreign investors, thereby availing local investors/firms with additional source of capital for investment. Equation 1 is expressed in a log linear function. The reasons for this include;

1. To allow the researcher to interpret the coefficient of the dependent variable directly as elasticity in relation to the explanatory variables (Upender, 2003)

2. To minimize the problem of heteroscedasticity and multicolinearity (Gafar, 1988; Doroodia, 1994; Adenikinju and Busari, 2009), and

3. To bring the numerical values of the different variables to a common base. On the strength of the foregoing, Equation 1 is expressed thus:

4. logRPR = ao + a1logRM2/GDPt-1 + a2logRCP/CGPt-1 + a3logRMC/GDPt-1 +a4logRST/GDPt-1 +a5 logRFE/GDPt-1 …………………. (2)

The general use of differencing has been found to minimize the possibility of spurious regression results, especially when dealing with time series data like this (Granger and Newbold, 1974; Philip, 1986). Studies by Layson and Seak (1984); Adams (1992); Anyanwu and Udegbunam (1996) concluded that first differencing achieves stationary of variables and thus reduces the possibility of spurious results. Based on the conclusion of the studies above, and to roughly gauge the robustness and consistency of our estimation results, equation (2) becomes:

∆logRPR = ao + a1∆logRM2/GDPt-1 + a2∆logRCP/CGPt-1 + a3∆logRMC/GDPt-1 +a4 ∆logRST/GDPt-1 +a5logRFE/GDPt-1 …………………. (3)

Where: ∆ = first difference operator.

The model for poverty rates in urban areas is given as

∆logUPR = bo + b1∆logRM2/GDPt-1 + b2log∆¬ RCP/GDPt-1 + b3∆logRMC/GDPt-1 + b4 ∆logRST/GDPt-1 + b5logRFE/GDPt-1……………………….. (4)

The a priori expectations are as in Equation 1.

Where: UPR = Urban poverty rates and

b0, b1……b5 are the parameters to be estimated

The model for estimating the impact of financial deepening on national poverty is presented in Equation 5.

∆logNPR = αo + α1∆logRM2/GDPt-1 + α2¬âˆ†logRCP/GDPt-1 + α3∆logRMC/GDPt-1 + α4 ∆logRST/GDPt-1 + α5logRFE/GDPt-1……………………….. (5)

The a priori expectations are the same as those in equations above.

Where: NPR = National poverty rates and

α1, α2…..α5 are the parameters to be estimated

RESULTS AND DISCUSSION

Descriptive analysis

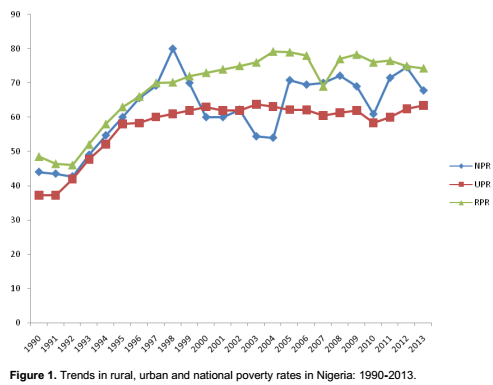

This section looks at the trend in the three poverty rates in Nigeria over the period of study. Figure 1 is based on the poverty data provided in columns 7, 8 and 9 in the appendix.

Figure 1 reveals that poverty in Nigeria has persistently remained above 50% on the average for the period under study, especially as from 1994. Rural poverty is relatively the highest owing to the fact that the rural dwellers have limited access to social amenities, lack the minimum requirement of collateral to obtain loans from commercial banks and the low price of agricultural produce. Urban poverty, as shown on the graph is relatively lower as most investors in the money and capital markets are urban dwellers who have better financial education, could afford collateral and enjoy better social amenities than their rural counterparts. The national poverty rate indicated that poverty was highest prior to the entrenchment of democratic governance in 1999. The capital market reform of 1999, banking sector reform/ consolidation of 2005, the implementation of National Economic Empowerment and Development Strategies (NEEDS) and the relative improvement in the distribution of fertilizers to farmers collectively contributed to the relative decline in national poverty from 1999 to 2010 as shown above. This finding agrees with the submission of Soludo (2006) that poverty in Nigeria has significantly dropped from 70% in 1999 to 54% in 2006 as a result of several reform measures put in place by government and improvement in economic governance.

The banking sector consolidation of 2004 did not benefit the poor as rural poverty started rising from 2008, while national poverty started declining within the same period. The effect of global financial crisis of 2007/2008 adversely affected Nigeria, as Professor Ndi Okereke- Onyiuke explained the drastic fall in capitalization of the Nigerian Stock Exchange to the Senate Joint Committee on Banking Capital Market and Finance in February, 2009. She revealed that between 2007 and 2008, foreign investors withdrew N812 billion from the market (Tella, 2009). This suggests that there were contagion effects on the financial assets of Nigerians. However, national, urban and rural poverty declined during the period. This may not be unconnected to the fact that the poor do not own significant assets in the formal financial sector which was the main victim of the global financial crisis. All the poverty rates increased from 2011 perhaps, as a result of political activities (electioneering campaigns) crowding out economic investments (Dabwor, 2015). Again, the post election violence of that year also compounded the poverty situation.

Quantitative analysis

The quantitative analysis is based on the application of ordinary least square regression technique. This tool is used to empirically estimate parameters of financial deepening indicators and their impacts on the three poverty rates in Nigeria. The impact of financial deepening on the three poverty rates are presented in Tables 2, 3 and 4 respectively. The data for these analyses are obtained from the appendix.

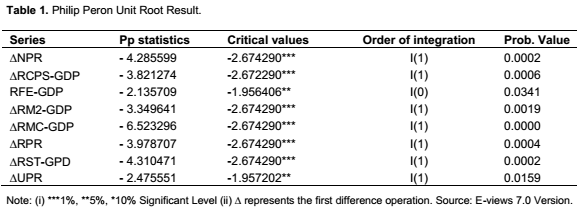

Unit root test (Philip Peron)

The estimation was preceded by a pretest of unit root. This paper employed the Philip Peron (PP) statistics to test stationarity of the series. The PP statistics is chosen because it is more efficient in analyzing unit root. The Dickey Fuller (DF) and Augmented Dickey Fuller (ADF) statistics have low power, that is, they tend to accept the null hypothesis of unit root more frequently than warranted (Gujiarati, 2006). According to Granger and Newbold (1974), if a non-stationary time series is regressed on another time series, the outcome may be a spurious regression. Time series data has a high probability to exhibit “random walk”. In other words, the variables in a time series data have the tendency to wander away from their true mean values. The result in Table 1 revealed that the variables had unit root; implying that they were non-mean reverting except ratio of foreign direct investment in equities to GDP which was integrated at level I(0). On the other hand, NPR, RCPS/GDP, RM2/GDP, RMC/GDP, RPR, RST/GDP and UPR were integrated at first difference I(1). By this result, the series have achieved stationarity and can be used to estimate the impact of financial deepening on poverty rates in Nigeria with minimum fear of spurious outcome (Adams,1992).

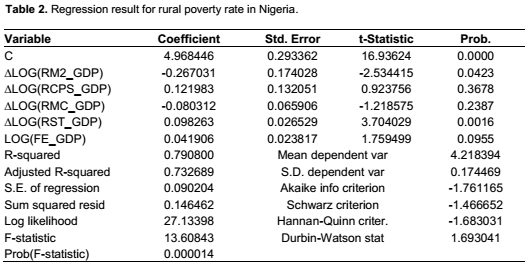

The regression result for rural poverty reveals that an increase in the ratio of broad money supply to GDP by 1% reduces rural poverty by 26.7%. On the other hand, a 1% increase in the ratio of market capitalization to GDP reduces rural poverty by 8.0%. The result further indicates that other financial deepening indicators did not contribute to reduction in rural poverty. The result notwithstanding, financial deepening explained rural poverty reduction in rural areas by 73%.

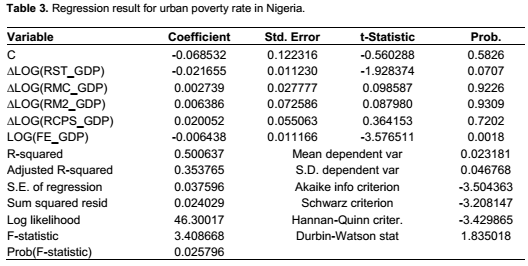

The urban poverty result indicates that 1% increase in the ratio of stock trade to GDP reduces poverty by 2.2% and it is statistically significant at the 5% level. Also, a 1% increase in the ratio of foreign direct investment in equities to GDP reduces urban poverty by 0.64% and it is statistically significant at 1% level. Ratios of market capitalization, broad money supply and credit to the private sector to GDP revealed that an increase of 1% in each of the ratios increased poverty in the urban Nigeria by 0.027, 0.064 and 2.00% respectively. This result is in line with the findings of Amoo (2014) who observed that a 10% increase in income resulted in an increase in poverty in Nigeria by 17.2%. The coefficient of multiple determination reveals that variation in urban poverty is 35% caused by financial deepening. This result implies that the marginal productivity of financial resources is higher in the rural areas compared to urban areas in spite of the fact that the rural areas are characterized by informal sector activities and are partly non-monetized. On the other hand, the urban areas are highly monetized and operate in the formal sector of the economy (Tables 2 and 3).

At the national level, the result shows that a 1% increase in the ratio of broad money supply to GDP reduces poverty by 73% and the coefficient of RM2/GDP is statistically significant at 5% level. 59% change in national poverty is caused by variations in financial deepening. The three results indicate that the ratio of credit to the private sector to GDP did not impact positively on poverty reduction in Nigeria for the period under study. This suggests that the poor do not benefit from credit facilities of banks and other financial institutions in spite of the relative increase in the capital base of commercial banks following the banking sector consolidation of 2005. Banks in Nigeria demand for collaterals that are beyond the reach of the poor as prerequisite for advancing loans (Table 4).

Again, the ratio of stock traded to GDP in the three equations fails to influence poverty reduction positively in Nigeria. This result confirms the findings of Rioja (2014) that on the average, stock market liquidity in developing countries and in the Nigerian capital market have not developed to the required threshold capable of promoting and attracting investment in their capital markets. While the ratio of foreign direct investment in equities to GDP could not contribute to rural and national poverty reduction, the ratio of market capitalization to GDP, on the other hand, was not able to positively impact on urban and national poverty in Nigeria for the period 1990 to 2013.

CONCLUSION AND RECOMMENDATIONS

The descriptive analysis has revealed that poverty is still endemic in Nigeria for the period under investigation. Findings from quantitative analysis revealed that financial deepening guarantees financial inclusion to Nigerians and, by extension, reduces poverty. This therefore, implies that financial deepening matters in poverty reduction strategies based on Nigeria’s data. On the basis the findings, this paper proffers the following recommendations.

There is the need for government and financial regulators to design a policy framework that would improve the financial literacy of Nigerians, especially the rural dwellers. Financial literacy will help the rural poor to appreciate the benefits of savings and borrowing for investment which is expected to impact positively on their income and, consequently, poverty reduction all things being equal.

The rural poor should be encouraged to form co- operative societies to be headed by people of impeccable character in the communities. The cooperative societies are expected to provide avenue for members to pool financial resources together that can be accessed as loans by members at lower interest rate. Where their financial resources are not adequate, members can easily raise funds (loans) in the formal financial market using the cooperative societies as collateral.

Government and financial authorities should design policies that would promote the growth of the financial sector. Since the size of the capital market in relation to the economy is low also, credit to the private sector is equally low and these are indications of a weak financial sector.

To improve on the financial depth, liquidity and financial assets to the poor, there is the need to establish financial institutions (money and capital markets) in the rural areas to encourage savings culture among Nigerians. This should be done simultaneously with improvement in financial markets and instruments such as: derivatives, bond and commodity markets which are largely non-existent or moribund in Nigeria.

There is the need to diversify the Nigerian economy to allow wider participation of Nigerians in productive activities that would improve employment of men and resources, increase the flow of financial income, hence poverty reduction. This is achievable if cottage industries are established in geo-political zones with comparative/ absolute advantage in the production and supply of agricultural goods and raw materials for the industries.

This is expected to reduce post harvest wastages, add value to primary products before exports and guarantees stable income to farmers.

Government through the ministry of labour and productivity should sponsor a bill in the national assembly mandating foreign firms to reserve not less than 50% of employment for local content in highly technical formal sectors of the economy (petroleum, mining, manu- facturing, and telecommunication). This is expected to widen employment opportunity to more Nigerians to participate in productive venture, thereby improving their income and, consequently, reduce poverty.

CONFLICT OF INTERESTS

The authors have not declared any conflict of interests.

REFERENCES

|

Abimiku AC (2006). Causes and effects of poverty in developing countries, Social Science Study Group Monograph Series 26 March. |

|

|

Abimiku AC (2009). The myths in poverty reduction efforts in Nigeria, Social Science Study Group Monograph Series 28 Vol. 1. |

|

|

Abimiku AC (2014). A speech delivered on the occasion of book launch titled: Entrepreneurship and poverty reduction in Nigeria, at ASUU secretariat, University of Jos, December, 6. |

|

|

Adams CS (1992). Recent development in econometric methods: An application to the demand for money in Kenya, Centre for the study Africa economics, Oxford. AERC, Special Paper, 15. |

|

|

Adenikinju A Busari D (2009). Overview of macroeconometrics modeling in Nigeria.Ibadan: University press, 11-15. |

|

|

Aghion P, Bolton P (1997). A trickle-down theory of growth and development with debt overhang, Rev. Econ. Stud. (64):151-172. |

|

|

Amoo BAG (2014). Growth-poverty and inequality perspective: Empirical discourse for Nigeria, The Niger. J. Econ. Soc. Stud. 56(3):445-463. |

|

|

Anyanwu JC, Udegbunam RI (1996). Financial deregulation, interest rate sensitivity and stability of money demand in Nigeria, Niger. J. Econ. Manage. Stud. (1):122-134. |

|

|

Ayyagari M, Beck T, Hosaini M (2013). Finance and poverty. Evidence from India, Centre Econ. Policy Res. pp. 1- 66. |

|

|

Bagehot W (1873). Lombard Street, 1962 (ed). Irwin Homwood. IL. |

|

|

Balackrishman R, Stanberg C, Syed MMH (2013). The illusive quest for inclusive growth. Growth, poverty and inequality in Asia, International Monetary Fund, No. 13-152. |

|

|

Bartoli H (1991). Poverty, progress, pauperization and marginalization: Concepts and propositions. In: H, Paul-Mak (ed) Poverty, progress and development, Kegan Paul International, pp. 1-57. |

|

|

Beck T, Demirguc-kunt A, Levine R (2007). Finance, inequality and the poor.J. Eco. Growth. 12(1):27- 49. |

|

|

Benerjee A, Newman A (1993). Occupational choice and the process of development, J. Political Econ. 101:27- 49. |

|

|

Clarke GRG, Xu LC, Zou, HF (2006). Finance and income inequality: what do the data tell us? Southern Euro. J. 72(3):578-596. |

|

|

Dabwor TD (2015). Analysis of the impact of capital market on Nigeria's manufacturing output: 1990-2012, Unpublished Ph.D Thesis Submitted to Postgraduate School, University of Jos. |

|

|

DeGrejorio J (1997). Borrowing constraints, human capital accumulation and growth. J. Monetary Econ. 37:49-71. |

|

|

Doroodia K (1994). An examination of traditional aggregate import demand function for Saudi-Arabia. Appl. Econ. Rev. 26:909-915. |

|

|

Eneji MA (2014). Entrepreneurship and poverty reduction in Nigeria, Impresive Print. Jos, 25-29. |

|

|

Gafar JS (1988). The determinants of import demand in Trinidad and Tobago 1960-1984. Appl. Econ. Rev. 55:271-273. |

|

|

Galor O, Zeira J (1997). Income distribution and macroeconomics, Rev. Econ. Stud. 60:35-52. |

|

|

Granger CWM, Newbold R (1974). Spurious regression in econometrics, J. Econ. 2(2):111-120. |

|

|

Gujarati DN (2006). Basic econometrics, New Delhi: Tata McGraw Hill Company Ltd. |

|

|

Inoue T, Hamori S (2010). How has financial deepening affected poverty reduction in India? Empirical analysis using state level panel data, Institute of Developing Economies, 249:1-30. |

|

|

IMF (2012). Financial deepening for macroeconomic stability and sustainable development. An IMF- DFID Collaboration. |

|

|

Jalilian H, Kirkpatrick C (2008). Does financial development contribute to poverty reduction? J. Dev. Stud. 41(4):636-656. |

|

|

Jhingan ML (2002). The economics of development and planning, New Delhi, Vrinda Publishers Ltd, pp. 734- 744. |

|

|

King R, Levine R (1993). Finance and growth Schumpeter might be right, The Quaterly J. Econ. 108(3):717-737. |

|

|

Layson SK, Seak GT (1984). Estimation and testing for functional form in first difference models, Rev. Econ. Stat. 66(2):98-116. |

|

|

Mbutor OM (2009). The dominant channels of monetary policy transmission in Nigeria: An empirical investigation, CBN Economic and Financial Review, 47(1). |

|

|

Miller HP (1968). Poverty: American style, California, Wadsworth, pp. 1-107. |

|

|

Nnadozie E (2012). Managing the Nigerian economy in an era of global financial and economic crises, Proceeding of the Eight Annual Public Lecture of the Nigerian Economic Society, Delivered at Transcorp Hiltop Abuja, 15 March. |

|

|

Odhiambo NM (2009). Finance-growth-poverty nexus in South Africa: a dynamic causality linkage. J. Socio-Econ. 38(2):320-325. |

|

|

Onwumere JUJ (2007). The capital market and financing of SMEs in Nigeria. Niger. J. Bank. Fin. 7(1). |

|

|

Plotnick RD, Skidmore F (1978). Progress against poverty, New York Academic Press pp. 35-42. |

|

|

Quartey P (2008). Financial sector development, savings mobilization and poverty reduction in Ghana, In: B. Guha-Khasnobis & G. Mavrotas (eds.), Financial development institutions, growth and poverty reduction, Basingstock: Palgrave Macmillan, pp. 87-119. |

|

|

Rioja FNV (2014). Stock markets, banks and the sources of economic growth in low and high income countries. J. Econ. Fin. 38:302-320. |

|

|

Schumpeter JA (1912). The theory of economic development, Havard University Press, Cambridge, M. A. 1934. |

|

|

Schiller BR (1976). The economics of poverty and discrimination, New Jessey, Prentice Hill, Inc, pp. 7-8. |

|

|

Shaw E (1975). Financial deepening in economic development, Oxford University Press. |

|

|

Soludo CC (2006). Law, institutions and Nigeria's quest to join the first world economy,Being a Lecture Delivered in Honour of the Retired Justice of the Supreme Court of Nigeria, Justice Kayode Eso, at the Obafemi Awolowo University Ile-Ife on July 25. |

|

|

Tella SA (2009). The global economic crises and Nigerian stock market: issues on contagion, Niger. J. Secur. Fin. 14(1):101-116. |

|

|

Todaro MP (1997). Economic development, New York, Longman, pp. 136-177. |

|

|

Ugiagbe EO, Edegbe MA (2015). Globalization and endemic poverty in Nigeria, J. Soc. Issues, 7(1):149-170. |

|

|

Upender M (2003). Applied econometrics, Delhi: Vrinder Publication. |

|

|

Visco I (2007). Financial deepening and monetary policy transmission mechanism, Being a speech Delivered at the IV Joint High-Level Eurostem-Bank of Russia Seminar, Moscow, 10-12 October. |

|

|

Wedderburn D (1974). Poverty, inequality and class structure, London, Cambridge University Press, pp. 1-20. |

|

Copyright © 2024 Author(s) retain the copyright of this article.

This article is published under the terms of the Creative Commons Attribution License 4.0