Full Length Research Paper

ABSTRACT

This paper explores the use of BSC as technique for assessing performance in the Nigerian banking industry. The population of the study comprised 21 banks operating in Gombe State, Nigeria. A purposive sampling technique was adopted to arrive at the sample of eleven banks. A survey technique was used to obtain data for the study. Fifty five copies of questionnaire were distributed to the executive staff of the sampled banks (5 each to every selected bank), out of which forty three copies were duly completed and returned. Descriptive statistics and Kruskal-Wallis ANOVA was used as techniques for data analysis. The study concludes that Nigerian banks relied heavily on financial performance measures followed by customer performance measures as technique for assessing their performance. The study recommended that Nigerian banks should enhance their performance measurement systems by balancing their performance measures within the four perspectives of BSC. This will check the skewness of the CAMEL’s rating approach (C = capital adequacy, A = asset quality, M = management quality, E = earning quality and L = liquidity), which uses financial measures to assess banks performance in Nigeria.

Key words: Balanced scorecard (BSC), bank, performance, performance measurement, Nigeria.

INTRODUCTION

Banks serve vital intermediary role in a market-oriented economy and have been seen as the key to investment and growth. Most studies have argued that the financial sector is vital for the socio-economic development of any country. For example, studies by Beck et al. (2000) and Levine (2003) suggest that a well developed and sound financial system can contribute significantly to economic growth by recognizing the important role financial intermediaries play in bridging the disequilibrium between savings and investment needs within an economy. They argue that economic growth can be sustained only if scarce resources are mobilized efficiently and trans-formed effectively into productive investments, and this function is efficiently conducted by the financial intermediaries. Furthermore, Hamid (2008) observes that a developing economy, like Nigeria, requires the services of a well-functioning banking system in order to realize its socio-economic objectives. Hussey (1999) posits that a bank is a commercial institution licensed as a taker of deposit and is concerned mainly with making and receiving payments on behalf of its customers, accepting deposits and making short-term loans to private indivi-duals, companies and other organizations. However, pperformance measurement is an integral part of management accounting (Emmanuel and Otley, 1995). At present, management accountants do more management activity and less accounting dealing with costs (Burns et al., 2004). The position of manager or management accountant is now similar to that of an internal business consultant (Siegel and Sorenson, 1994).

Companies around the globe have stuck to the traditional measures of financial performance until in the late 1980s when increased globalised competition has forced them to consider non-traditional measures (Ghalayini and Noble, 1996). Furthermore, the operating environment and the nature of business operations have become increasingly future-orientated. This has recently set new requirements for management accounting to become more future and business-oriented, which in turn has led to the use of forward-looking accounting information including non-financial measures. The requirements of the customers keep changing and a satisfied customer today may be lost in the future if his changing requirements are not met. In order to retain the customer, therefore, his changing requirements must be satisfied by way of innovation in products, services and processes (Ahmed et al., 2011).

However, in order to adapt to internal and external changes, the method of monitoring performance should be dynamic. Kaplan and Norton (1992) developed an innovative multi-dimensional corporate performance scorecard known as the BSC. It provides a framework for selecting multiple key performance indicators that supplement traditional financial measures with operating measures of customer satisfaction, internal business processes, and learning and growth activities.

In both research and practice, the BSC has received much attention, particularly as a strategic performance measurement system in many industries, including hospitality, health, manufacturing and banking (Beechey and Garlick, 1999). In the same vein, BSC is a framework which has been widely used during the last decade for performance measurement in different disciplines (Lee et al., 2008; Luu et al., 2008). It has been observed that most of the successful organizations are adopting BSC (Rigby, 2001; Fernandes et al., 2006).

However, according to Etim and Agara (2011), despite widespread adoption of BSC, there appears to be no significant documentation on the translation of BSC in any Nigerian firm that could serve as a reference point for replication in spite of the success already recorded by companies that have implemented it. The study relating to BSC in Nigeria is the one conducted by Iwarere and Lawal (2011) which empirically evaluated the performance of facility maintenance of public organizations in Nigeria and recommended that public organizations in Nigeria should adopt four key aspects of the BSC that focus on four related perspectives of organizational and management performance such as financial performance measures; internal process; customer satisfaction and workforce support. In addition, Etim and Agara (2011) empirically explore how the strategic management performance model called BSC, has faired among firms that have introduced/adopted the model in Nigeria. They concluded that for Nigerian organizations to participate in the global economic arena, the adoption of BSC is imperative. The foregoing discussion suggests that there are relatively few empirical studies on the use of BSC as technique for assessing performance in Nigeria. It is against this bedrock that this study intends to examine the use of BSC as a technique for assessing performance in the Nigerian banking industry. Thus, this study hypothesized that Nigerian banks do not use all the four perspectives of BSC as technique for assessing performance. The paper is thus organized into five sections. Section one which is the introduction. Section two, which is the next section, reviews related literature on the subject matter of the study. Section three discusses the methodological issues of the paper, while section four presents and discusses the results obtained from the data generated for the study and finally, section five gives the conclusion of the paper.

The concept of performance

The term performance has been defined by different authors in different ways. According to Drucker (1954), when discussing the issue of performance, the issues of effectiveness and efficiency are interrelated and that efficiency refers to the ability of an organization to do things right, while effectiveness is about doing the right things. Kohli and Jaworski (1996) observe that organizational performance consists of cost-based performance measures, which reflect performance after accounting for the costs of implementing a strategy (profit measures), and revenue-based performance measures, which do not account for the cost of implementing a strategy (sales and market share). Aluko (2003) defines performance as the execution or accomplishment of work, tasks or goals to a certain level of desired satisfaction and that organizational performance is defined in terms of the ability of an organization to satisfy the desired expectations of three main stakeholders comprising owners, employees and customers. An institution that persistently makes a loss will ultimately deplete its capital base, which in turn puts equity and debt holders at risk. Moreover, since the ultimate purpose of any profit-seeking organisation is to preserve and create wealth for its owners, the bank’s return on equity (ROE) needs to be greater than its cost of equity in order to create shareholders’ value. Dauda (2010) highlighted that organization performance is determined by the demand for its product or services. Many organizations put in place methods and strategies that could enable them attract customers and improve the quality and quantity of their product.

From the foregoing definitions, it can be deduced that performance is the efficient and effective use of resources by an organization for the accomplishment of its objective or goal leading to increase in the following: share price, sales, market share, sustainable profitability, net present value, earnings, generating cash flows, risk-taking, leverage and demand of its product or service and satisfying the desired expectations of its three main stakeholders comprising owners, employees and customers.

The concept of performance measurement

Though the term performance measurement has been used since the late 1970s, there has not been a universally accepted definition for it. An aged saying indicates that what gets measured gets managed (Schmenner and Vollmann, 1994). Performance measurement is the process of ensuring that an organization pursues strategies that lead to the achievement of overall goals and objectives (Nanni et al., 1992). According to Cheng (2008), performance measure can be defined as the system by which an organization monitors its operations and evaluates whether the organization is attaining its goals. Besides, to fully utilize the function of the performance evaluation, it is necessary to set up a series of indicators that properly reflect the performance of the organization.

Given the aforementioned definitions, it can be inferred that performance measurement is multidimensional, comprising the ways and manners through which the operations of an organization overtime are monitored and assess with a view to determining whether the organization is attaining its goals in terms of value delivery to customers and other stakeholders.

The financial measures of performance

Financial measures have long been used to effectively evaluate the performance of business organizations. Financial measures are required by legislation and have been in existence for many years. All businesses, therefore, use some form of financial measurement systems. The term traditional performance measurement system, however, has been coined to describe performance measurement systems where the overall focus is financial and, as a consequence, the scorecard is dominated by financial-outcome-related measures. However, prior to 1992, various absolute and relative accounting measures were being utilized for performance evaluations. Prominent accounting measures were total income, operating profit, net profit, cash flows, return on investment, residual income, and value added income (Garrison et al., 2003; Kaplan and Atkinson, 2005; Horngren et al., 2006). Although the use of financial performance measures is important in performance measurement, there has been growing criticism of financial measures as they are historic in nature and lack futuristic outlook (Schoenfeld, 1986; Dearden, 1987; Emmanuel and Otley, 1995; Kaplan and Norton, 1996).

From the foregoing, despite the heavy criticisms of the use of financial measures of performance by companies, some organizations still consider it as the most effective tool for measuring performance. However, it is as a result of the heavy criticisms on the use of financial performance measures that some have argued for the inclusion of non-financial performance measures.

The non-financial measures of performance

Prior to the 1980s, management accounting control systems tended to focus mainly on financial measures of performance, where only those items that could be expressed in monetary terms were considered, while product quality, delivery, reliability, after sales service and customer satisfaction were not given prominence in the measurement (Drury, 2004). Also, Fisher (1995) states that there are three main reasons for the emergence of non-financial performance measures: the limitations of traditional financial performance measures, competitive pressures, and the growth of other initiatives. Chartered Institute of Management Accountant (2005) as cited in Agyei-Mensah (2009) defines non-financial performance measures as measures of performance based on non-financial information which may originate in and be used by operating departments to monitor and control their activities without any accounting input. Non-financial performance measures provide managers with timely information centred on the causes and drivers of success and can be used to design integrated evaluation systems (Kaplan and Norton, 1996; Banker et al., 2000).

From the above discussion, one can see that the proponents of non-financial measure of performance consider it to be the best measure of performance which focuses on the future performance rather than on historical information due to increasing competition, changing organisational roles, changing external demands and the power of information and communication technology.

The concept of balanced scorecard

French people began using a measure called “the tableau de board”, or the dashboard of measure, which included both financial and non-financial measures (Stewart and Hubin, 2001). The emphasis on quality in the American continent during the 1980s made Canadian companies to include non-financial measures also in evolving their business strategy. This was the initial conception of the balanced scorecard (Stewart and Hubin, 2001). The BSC arose out of the need to improve the planning, control and performance measurement functions of management accounting. Because of the rise in popularity of the BSC, and benefits attributed to its use, Atkinson et al. (1997) state that the BSC is a significant development in management accounting that deserves intense research attention. French and the Canadians were the first to use the BSC in a different form. The BSC balances the financial indicators with non-financial drivers of performance. It allowed measuring the business performance in a more balanced way by considering both financial and non-financial measures (Ishtiaque et al., 2007).

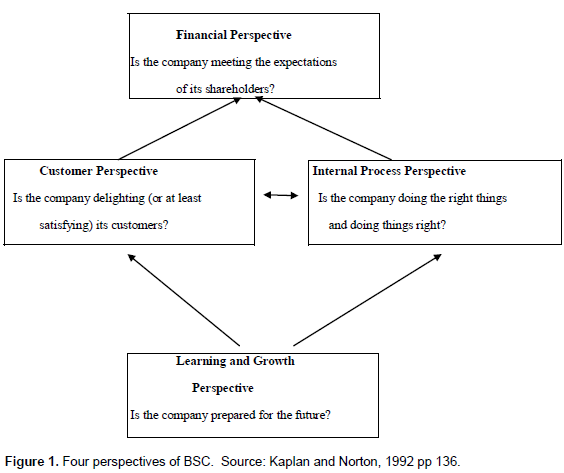

Within the BSC framework, four categories of measures are identified in order to achieve balance amid the financial and the non-financial, between internal and external and between current performance and future performance (Kaplan and Norton, 1992). These perspectives are not mutually exclusive to one another; rather, they affect each other in quite a high degree as shown in Figure 1.

The financial measures typically focus on profitability related measures (the basis on which shareholders, in turn, typically gauge the success of their investments), such as return on capital, return on equity and return on sales among others (Kaplan and Norton, 1992; Lipe and Salterio, 2000). Measures that are closely related to customers include results from customer surveys, sales from frequent customers, and customer profitability. The customer perspective is a core of any business strategy that describes the unique mix of product, price, service, relationship, and image that a company offers (Kaplan and Norton, 2001). Out of the four BSC perspectives, the customer is at the core of any business and is crucial to long-term improvement of a company’s performance (Kaplan and Norton, 1992; Pineno, 2002).

In addition, the internal process measures are typically based on the objective of most efficiently and effectively produced products or services that meet customer needs. For example, such measures may include order conversion rate, on-time delivery from suppliers, cost of non-conformance, and lead time reduction (Kaplan and Norton, 1996). Furthermore, Kaplan and Norton (1996) suggested that measures of employee capabilities, information systems capabilities and employee motivation and empowerment are examples of performance measures relating to learning and growth perspective. In the same vein, the innovation and learning perspective includes three broad constructs: human capital, measured by employee skills (Ellingson and Wambsganss, 2001; Libby et at., 2004; Ullrich and Tuttle, 2004) and know-how, organization capital measured by sharing of worker knowledge, shared vision, objectives and values, information capital measured by knowledge management capabilities and accessibility of information (Kaplan and Norton, 2004).

Empirical study on the use of BSC as performance indicators

Balanced Scorecard (BSC) is a framework which has been widely used during the last decade for performance measurement in different disciplines (Epstein and Wisner, 2001; Lawson et al., 2006; Idalina et al., 2007; Lee et al., 2008; Luu et al., 2008). It has been observed that most of the successful organizations are adopting BSC (Silk, 1998; Malmi, 2001; Rigby, 2001; Fernandes et al., 2006). In addition, increase use of BSC can be seen in recent researches like: in supply chain integration (Bhagwat and Sharma, 2007 Chang, 2009), research and development projects (Eilat et al., 2008; Asosheh et al., 2010), university performance evaluation (Wu et al., 2011). According to Kuang – Hua (2005), BSC is the most influential managerial concept in the last 75 years.

The use of BSC can be seen through several other similar studies. Malmi (2001) investigated how BSC is applied in Finish companies and why companies adopt it. The study document that BSC is used in two different ways. The first approach is management by objectives and the second is to use BSC as an information system. Also, the idea of linking measures together based on assumed cause-and-effect relationship was not well understood by the early adopters of BSC. In addition, Anand et al. (2005) analyzed the practice of the organizational performance management system of India with a focus on BSC from 2002 – 2003 using a survey method. The study finds that about 45.28 per cent of the companies are using BSC. Also, initiating the change process in the organization 50 per cent, broadening of the performance measures 45.8 per cent, and facilitating the integration of business plans with the financial plans 45.8 per cent are the major motivations for the implementation of BSC in corporate India. Similarly, Ishtiaque et al. (2007) conducted a survey in Bangladesh to identify the use of BSC and found that the number of hours spent for training per employee, on time deliveries, delivery cycle, throughput time and set up time are the performance measures used by the firms. They recommend that frequent in house and outdoor development sessions should have to be arranged and product and service innovations and modifications need to be encouraged and customer complaints need to be resolved quickly. Furtheremore, Ahmed et al. (2010) conducted a survey on commercial banks in Pakistan to know the extent to which the BSC was being applied. The study concluded that the commercial banks were using all the perspectives of the BSC without knowing that they were using them. Al-Matarneh (2011) conducted a survey to determine the ability of Jordanian industrial companies to apply the BSC for evaluating their overall performance and the availability of the necessary data for that. The results show that there is recognition by the Jordanian industrial companies of the importance of implementing the BSC in assessing their overall performance. They also found that the Jordanian industrial companies realized the importance of using the operational measurements (non-financial) for assessing their overall performance and they can afford the cost of applying the BSC and they have the necessary human resources to implement it. The study recommends that the Jordanian industrial companies should use the BSC as a means to rationalize the decisions of managers and guide their behaviour and performance evaluation and that the Jordanian industrial companies should attract experts from developed countries to apply the BSC. Moreover, Ahmed et al. (2011) conducted a survey to know what measures are used by the commercial banks in Pakistan to evaluate their performance within the four perspectives of the BSC. The study results show that: first, the common most financial measures used by the commercial banks in Pakistan are return on investment, percentage growth in revenue and profit per account; second, the measures for customer satisfaction are number of complaints, number of new customers and number of appreciation letters; third, the measures for internal process are improvement in response time to customers queries, introduction of new products and services, reduction in waiting time and number of new facilities, and lastly measures for learning and growth are feedback from employees, employees’ suggestions, labour turnover and number of trained employees.

From the foregoing, the BSC has been applied by companies in both developed and developing economies cutting across various industries. But its application in the Nigerian context received little attention. This study, therefore, tries to fill this gap by studying the use of BSC in assessing performance in the Nigerian banking industry.

THEORETICAL FRAMEWORK

The theory that explains this work is the contingency theory of performance measurement. The contingency theory and contemporary performance measurement unlike the traditional approach to performance measurement where performance measurement is comparable across industries and measures are alike; contemporary performance measurement pays attention to particular characteristics of a company. Though BSC follows the same approach, they may only be comparable with one another. The actual choice of performance measures differs not only among companies active in different industries but also among companies competing within the same industry. These differences may stem not only from the fact that some managers conduct the affairs of their company so as to achieve only a satisfactory and not the maximum level of the objectives (Cyer and March, 1963). Or, as theory of limited rationality says, they may emerge because human beings differ in their abilities to process and understand large quantities of information. Contingency theory of management accounting can be used as theoretical foundations to explain these differences. The contingency approach to management accounting is based on the premise that there is no universally appropriate accounting system, which applies equally to all organizations in all circumstances (Otley, 1980). Since a performance measurement system is considered part of the management accounting system or at least depends on its part, the contingency approach to performance measurement can be formulated in the same way. It is based on the premise that there is no universally appropriate performance measurement sys-tem applicable to all organizations in all circumstances. Instead, a contingency theory attempts to identify specific aspects of a performance measurement system that are associated with certain defined circumstance and to demonstarte appropriate matching (Rejc, 2003).

METHODOLOGY

The study evaluates the use of BSC as a technique for assessing performance. The research focuses on all the twenty one (21) banks operating in Gombe State, Nigeria. A judgemental/purposive sampling technique was adopted to arrive at the sample of eleven (11) banks. A survey technique was therefore used to obtain relevant data for the study. This was done by means of questionnaire administered on the banks’ executives. The questionnaire was adopted by the researcher from Kaplan and Norton (1996) approach, with some modifications. A five (5) item scale (Strongly Agree (SA) = 5 Points, Agree (A) = 4 Points, Undecided (UD) = 3 points, Disagree (DA) = 2 Points, and Strongly Disagree (SD) = 1 Point) was used to measure the respondents’ views on the use of BSC as a technique for assessing performance. Furthermore, the questionnaire was administered directly by the researcher and his research assistants on the banking executives (Branch Managers, Operations Managers, Heads Customer Service, Marketing Managers and Branch Accountants) because it is believed that they are in a better position to provide the right information about how banks measure their performances.

The data generated for this research were first analyzed using Descriptive Statistics to ascertain the level of agreement or disagreement with the statement in the questions. Under the Descriptive Statistics, percentages, means, medians, modes, standard deviations, minimum points and maximum points were used in data analysis.

i. Mean value of 3.50 is benchmarked as minimum

ii. Minimum acceptable values for median and mode stand at 3.50

In addition, Kruskal Wallis Test was carried out to compare the perception of the banks on the four perspectives of the BSC, with a view to finding which of the four perspectives is given much attention by them. The Kruskal Wallis Tests were utilized because the study variables were not amenable to quantifiable measurements. Thus, this justifies the use of this tool for analysis. The Statistical Package for Social Sciences (SPSS) version 19.0 was used to carry out the analyses.

RESULTS AND DISCUSSION

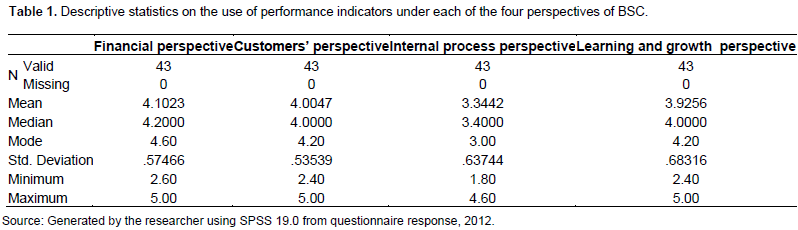

The data collected in the study using questionnaire are presented and interpreted from which inferences were drawn. Of the fifty five (55) copies of questionnaire administered to the respondents of the sampled banks, forty three (43), representing 78%, were filled and returned, while twelve (12), representing 22%, were not returned. Table 1 presents the results of analysis of the use of the four perspectives of BSC as technique for assessing banks’performance.

Table 1 presents the elements of descriptive statistics on the use of performance measures under each of the four perspectives of BSC in assessing performance of banks in Nigeria. From the table, it can be seen that the modal and the median responses are high for all the four perspectives of BSC with the exception of the internal process perspective which has 3.00 and 3.4000 as its mode and median respectively. This implies that majority of the respondents opted for agreement and strong agreement with the statements on financial, customer and learning and growth perspectives of BSC.

However, there is low inclination toward internal business process perspective. Furthermore, it could be deduced from the table that the respondents place a major weight on the use of performance measures under financial perspective (mean = 4.1023), followed by customer perspective (mean = 4.0047), learning and growth perspective (mean = 3.9256) and internal process perspective (mean = 3.4884). The mean scores of financial, customer and learning and growth perspectives of BSC stand above cut-off value mean of 3.5000, and this indicates a high score on the use of performance indicators under the three perspectives of BSC and low performance on the use of performance indicators under internal process perspective.

Moreover, the standard deviation around the mean value in all the four perspectives of BSC is insignificant. Even the internal process perspective which has the mean below the cut-off mean value, its standard deviation is still insignificant (.63744). Additionally, all the four perspectives have 5 as their maximum value and the minimum values of 2.60, 2.40, 1.80 and 2.40 for financial, customer, internal process and learning and growth perspectives, respectively.

The four perspectives of the BSC

This sub section compares the perception of the banks on the four perspectives of the BSC, with a view to finding which of the four perspectives is given much attention by them. The results are presented in Table 2.

Table 2 shows Kruskal Wallis Test of 13.474 and P-value of 0.004. This suggests that, there is significant variation by the respondents on the four perspectives of BSC. The table also indicates that financial perspective has the highest mean rank of 15.60 followed by customer perspective with a mean rank of 13.80 and learning and growth perspective with mean rank of 9.60. The internal process perspective has the least mean rank of 3.00.

The above discussion suggests that, the banks focus more on financial perspective followed by customer perspective and learning and growth perspective, but they put less emphasis on internal process perspective of BSC. This means that, on the average, Nigerian banks are utilizing financial, as well as, non-financial measures for their performance evaluation systems, without any formal recourse to the BSC. This finding correlates with the finding of Ahmed, Bowra et al. (2010) who conducted a survey on commercial banks in Pakistan and concluded that the commercial banks were following all the four perspectives of BSC without knowing that they were following them. Similarly, it is consistent with the findings of Anand et al. (2005) who found that the financial perspective of BSC has been found to be the most important perspective followed by the customer perspective and learning and growth perspective.

CONCLUSION AND RECOMMENDATIONS

In this paper an attempt was made to explore the use of BSC as technique for assessing performance by Nigerian banks. The concept of performance, performance measurement, financial and non-financial measures of performance and the concept of balanced scorecard have been discussed. Other issues such as the four perspectives of the BSC and empirical studies on the use of BSC as technique for assessing performance were also highlighted.

From the analysis of related literature, analysis and interpretation of data and results of hypothesis test, the researcher concludes that, for the fact that Nigerian banks relied heavily on financial performance measures followed by customer performance measures as a technique for assessing their performance, a compre-hensive view of their performance cannot be guaranteed without incoporating all the four perspectives of BSC.

Lastly, Nigerian banks should enhance their performance measurement systems by balancing their performance measures within the four perspectives of BSC. This will check the skewness of the CAMEL’s rating approach (C = capital adequacy; A = asset quality; M = management quality; E = earning quality and L = liquidity), which uses financial measures to assess banks’ performance in Nigeria.

CONFLICT OF INTERESTS

The author has not declared any conflict of interest.

REFERENCES

|

Agyei-Mensah BK (2009). The Impact of Contingent Factors on Performance Measures in the Rural Banks of Ashanti Region of Ghana, |

|

|

Ahmed Z, Bowra ZA, Ahmad I, Nawaz M, Khan MS (2010). Balanced Scorecard: Is it a Spontaneous Performance Measurement Tool, Interdiscipl. J Contemporary Res. in Bus., 2(2): 99-10. |

|

|

Ahmed Z, Bowra ZA, Ahmad I, Nawaz M, Khan MS (2011). Performance Measures used by the Commercial Banks in Pakistan within the four Perspectives of Balanced Scorecard, J Money, Investment and Banking, 21: 12-20. |

|

|

Al-Matarneh GF (2011). Performance Evaluation and Adoption of Balanced Scorecard in Jordanian Industrial Companies, Eur. J Econ., Financ. Admin. Sci. 35:1-10. |

|

|

Aluko MAO (2003). The Impact of Culture on Organizational Performance in Selected Textile Firms in Nigeria, Nordic J Afr. Stud., 12(2):164-179. |

|

|

Anand M, Sahay BS, Saha S (2005). Balanced Score Card in Indian Companies, Vikalpa, 30(2):1-15. |

|

|

Asosheh A, Nalchigar S, Jamporazmey M (2010). Information Technology Project Evaluation: An Integrated Data Envelopment Analysis and Balanced Scorecard Approach, Expert Systems with Applications, 37:5931-5938. |

|

|

Atkinson AA, Balakrishan R, Booth P, Cote JM, Groot T, Malmi T, Roberts H, Uliana E, Wu T (1997). New Directions in Management Accounting Research, J Manag. Account. Res., 9: 79-101. |

|

|

Banker RD, Potter G, Srinivasan D (2000). An Empirical Investigation of an Incentive Plan that includes Non-Financial Performance Measures, The Accounting Review, 75(1): 65-92. |

|

|

Beck T, Levine R, Loayza N (2000). Finance and the Sources of Growth, J Financ. Econ., 58(1&2):261-300. |

|

|

Beechey J, Garlick D (1999). Using the Balanced Scorecard in Banking, The Australian Banker, 133: 28-30. |

|

|

Bhagwat R, Sharma MK (2007). Performance Measurement of Supply Chain Management: A Balanced Scorecard Approach, Computers & Industrial Engineering, 53: 43-62. |

|

|

Burns J, Hopper T, Yazdifar H (2004). Management Accounting Education and Training: Putting Management in and taking Accounting out, Qualitative Research in Accounting and Management, 1(1):66-84. |

|

|

Chang HH (2009). An Empirical Study of Evaluating Supply Chain Management Integration using the Balanced Scorecard in Taiwan, Service Industries J, 29: 185-202. |

|

|

Cheng CB (2008). Performance Evaluation for a Balanced Scorecard System by Group Decision Making with Fuzzy Assessment, Int. J Appl. Sci. Eng., 6(1): 53-69. |

|

|

Cyer RM, March JG (1963). A Behavioural Theory of Firm. Engliwood, Prentice-Hall, pp 332. |

|

|

Dauda YA (2010). Employee's Market Orientation and Business Performance in Nigeria: Analysis of Small Business Enterprises in Lagos State, Int. J. Market. Stud., 2(2): 1918-7203. |

|

|

Dearden J (1987). Measuring Profit Centre Managers, Harvard Business Review, 65(5): 84-88. |

|

|

Drucker PF (1954). The practice of Management, Newyork, Harper & Row Inc. |

|

|

Drury C (2004). Management and Cost Accounting (6th Ed.), London, Book Power. |

|

|

Eilat H, Golany B, Shtub A (2008). Research & Development Project Evaluation: An Integrated Data Envelopment Analysis and Balanced Scorecard Approach, Omega, 36: 895-912. |

|

|

Ellingson DA, Wambsganss JR (2001). Modifying the Approach to Planning and Evaluation in Governmental Entities: A Balanced Scorecard Approach, J. Public Budgeting, Account. Financ. Manage. 13(1): 103-120. |

|

|

Emmanuel C, Otley D (1995). Readings in Accounting for Management Control, London, Chapman and Hall. |

|

|

Epstein MJ, Wisner PS (2001). Using a Balanced Scorecard to Implement Sustainability, Environmental Quality Management, 11(2):1-10. |

|

|

Etim RS, Agara IG (2011). The Balanced Scorecard: The new Performance Management Paradigm for Nigerian Firms, Int. J Econ. Dev. Res. and Investment, 2(3): 64-73. |

|

|

Fernandes KJ, Raja V, Whalley A (2006). Lessons from Implementing the BalancedScorecard in a Small and Medium Size Manufacturing Organization, Technovation, 26: 623-634. |

|

|

Fisher J (1995). Use of Non-financial Performance Measures, in Young, S. M. (ed),Readings in Management Accounting, Englewood Cliffs, Prentice Hall, pp. 329-335. |

|

|

Garrison RH, Noreen EW, Seal W (2003). Management Accounting, New York, McGraw Hill. |

|

|

Ghalayini AM, Noble JS (1996). The Changing Basis of Performance Measurement, Int. J Operations and Production Management, 16(8):63-80. |

|

|

Hamid KT (2008). An Assessment of the Relationship between Corporate Governance and Internal Control System in the Nigerian Banking Industry, An Unpublished Ph. D. Thesis Submitted to the Department of Accounting, Bayero University, Kano, for the award of Ph. D. Degree in Accounting. |

|

|

Horngren CT, Datar SM, Foster G (2006). Cost Accounting: A Managerial Emphasis. (12th Ed), New Jersey, Prentice-Hall Inc. |

|

|

Hussey R (1999). Oxford Dictionary of Accounting, (2nd ed.), London, Oxford University Press. pp 43. |

|

|

Idalina DS, Lucas R, Paula A (2007). Developing Sustainability Balanced Scorecards for Environmental Services: A Study of three Large Portuguese Companies, Environmental Quality Management, 16(4): 13-34. |

|

|

Ishtiaque AA, Khan H, Akter S, Fatima ZK (2007). Perception Analysis of Balanced Scorecard: An Application over a Multinational Corporation of Bangladesh, J Bus. Stud., 28 (2): 238-268. |

|

|

Iwarere HT, Lawal KO (2011). Performance Measures of Maintenance of Public Facilities in Nigeria, Res. J Bus. Manag., 5(1): 16-25. |

|

|

Kaplan RS, Norton DP (1992): Balanced Scorecard: Measures That Drive Performance, Harvard Business Review, 70(1):71-79. |

|

|

Kaplan RS, Norton DP (1996). Using the Balanced Scorecard as a Strategic Management System, Harvard Business Review, 74(1): 75-85. |

|

|

Kaplan RS, Atkinson AA (2005). Advanced Management Accounting. (3rd Ed), New Jersey: Prentice-Hall Inc. |

|

|

Kaplan RS, Norton DP (2001). The Strategy Focused Organization: How Balanced Scorecard Companies Thrive in the New Business Environment, Boston: Harvard Business School Press. |

|

|

Kaplan RS, Norton DP (2004). Measuring the Strategic Readiness of Intangible Assets, Harvard Business Review, 82(2): 52-63. |

|

|

Kohli AK, Jaworski BJ (1996). Market Orientation: Review, Refinement and Roadmap, J Market. focused Management, 1 (2):119-135. |

|

|

Kuang-Hua H (2005). Using Balanced Scorecard and Fuzzy Data Envelopment Analysis for Multinational Research & Development Project Performance Assessment, J. Am. Acad. Bus., Cambridge, 7: 189-196. |

|

|

Lawson R, Stratton W, Hatch T (2006). Scorecarding Goes Global, Strategic Finance, 87(9): 34-41. |

|

|

Lee AHI, Chen WC, Chang CJ (2008). A fuzzy Analytic Hierarchy Process and Balance Scorecard Approach for Evaluating Performance of Information Technology Department in the Manufacturing Industry in Taiwan, Expert Systems with Applications, 34: 96-107. |

|

|

Levine R (2003). More on Finance and Growth: More Finance, More Growth? Federal Reserve Bank of St. Louis Review, 85(4): 31-46. |

|

|

Libby T, Salterio SE, Webb A (2004). The Balanced Scorecard: The Effects of Assurance and Process Accountability on Managerial Judgment, Accounting Review, 79(4): 1075-1094. |

|

|

Lipe MG, Salterio S (2000). The Balanced Scorecard: Judgmental Effects of Common and Unique Performance Measures, The Accounting Review, 75(3): 283-298. |

|

|

Luu TV, Kim SY, Cao HL, Park YM (2008). Performance Measurement of Construction Firms in Developing Countries, Construction Management and Economics, 26(4): 373-386. |

|

|

Malmi T (2001). Balanced Scorecards in Finnish Companies: A Research Note. Management Accounting Research, 12: 207-220. |

|

|

Nanni AJ, Dixon JR, Vollmann TE (1992). Integrated Performance Measurement: Management Accounting to Support the New Manufacturing Realities, J Manag. Account. Res., 4: 1-19. |

|

|

Otley DT (1980). The Contingency Theory of Management Accounting: Achievement and Prognosis. Accounting, Organization and Society, 5(4):413-428. |

|

|

Pineno CJ (2002). The Balanced Scorecard: An Incremental Approach Model to Health Care Management, J Health Care Finance, 28(4): 1-69. |

|

|

Rejc A (2003). Traditional Versus Contemporary Performance Measurement: Evidence from Large Suvenian Companies. Economic and Business Review, 5: 117-135. |

|

|

Rigby D (2001). Management Tools and Techniques: A Survey, California Management Review, 43(2): 139-160. |

|

|

Schmenner WR, Vollmann ET (1994). Performance Measures: Gaps, False Alarms and Usual Suspects, Int. J. Oper. Prod. Manag., 14(12):58-69. |

|

|

Schoenfeld HM (1986). The Present State of Performance Evaluation in Multinational, in Holzer HP, Schoenfeld HM (ed), Managerial Accounting and Analysis in Multinational Enterprises, Berlin, Walter De Gruyter Publishers, pp. 217-252. |

|

|

Siegel G, Sorenson JE (1994). What Corporate America Wants in Entry-level Accountants, Management Accounting, 76(3):26-31. |

|

|

Silk S (1998). Automating the Balanced Scorecard, Management Accounting, 79 (11): 38-44. |

|

|

Stewart AC, Hubin JC (2001). The Balanced Scorecard: Beyond Reports and Rankings, Planning for Higher Education, 29(2):37-42. |

|

|

Ullrich MJ, Tuttle BM (2004). The Effects of Comprehensive Information Reporting Systems and Economic Incentives on Managers Time planning Decisions, Behavioural Research in Accounting, 16:89-105. |

|

|

Wu HY, Lin YK, Chang CH (2011). Performance Evaluation of Extension Education Centres in Universities based on the Balanced Scorecard, Evaluation and Program Planning, 34: 37-50. |

|

Copyright © 2024 Author(s) retain the copyright of this article.

This article is published under the terms of the Creative Commons Attribution License 4.0