ABSTRACT

This paper reviews the existing and emerging perspectives on fair value accounting (FVA) in the context of the stewardship function of financial reporting. This study draws on diverse research threads and theoretical notions to advance a comprehensive assessment of existing FVA research in the context of the trade-off between decision-usefulness and the stewardship objective. By conducting a narrative literature review, the authors identify two distinct domains of literature: FVA- a result of a conceptual shift in financial reporting; and FVA- an enhancement of decision-usefulness in general-purpose financial reporting. This study posits that FVA can be considered as an evolutionary, rather than revolutionary, development in financial reporting measurement which emerged from financialisation and globalisation of economies. It is further suggested that the ability of FVA to provide stewardship-relevant information may be reduced due to the emphasis it places on the provision of decision-useful information for investment purposes. Therefore, the authors call for a greater engagement between policy-setters and researchers when choosing conceptual underpinnings for financial measurement objectives.

Key words: Fair value accounting, stewardship function, decision usefulness, IFRS 13.

Regarded as a ‘quiet revolution’ in financial reporting, growing controversy surrounds the subject of financial measurement due to a perceived movement from the traditional basis of financial measurement (historical cost) towards a ‘new’ basis of fair value accounting (FVA). Driven by the alleged decision relevance of market-based values, FVA has manifested itself as an increasingly dominant measurement system, with its theoretical dominance now embedded in the IASB and FASB Conceptual Framework. With the increasing implementation of FVA across many jurisdictions, critics have pointed to a shifting emphasis from the stewardship function of financial reporting towards the facilitation of investment decision-making (Whittington, 2008; Ronen, 2008; Hitz, 2007). The existing FVA literature reflects this information content objective by typically addressing the trade-off between relevance and reliability of fair values (Müller et al., 2015; Chung et al., 2017; Israeli, 2015; Song et al., 2010; Siekkinen, 2016; Wang and Zhang, 2017; Demerjian et al., 2016; Shalev et al., 2013; Manchiraju et al., 2016; Mäki et al., 2016; Hlaing and Pourjalali, 2012; Guthrie et al., 2011; Cairns et al., 2011). In this paper, the authors challenge this tendency and document the position of stewardship-relevant information when extending adoption of FVA. The importance of the stewardship function has been long established in accounting and is based on the central idea of accountability. The accountability notion encompasses managers’ responsibility over financial resources to ensure profitability for equity providers, an obligation to protect creditors’ interests, and the ability to ensure long-term business operations (Barton, 1982). Some authors have argued that displacement of accountability as a backbone of accounting with the information usefulness objective is a result of transformation of accounting academy into a sub-division of financial economics (Ravenscroft and Williams, 2009). Dominance of neoclassical discourse of finance created the information-driven objective focused on a forward-looking but less reliable approach to predict future events or outcomes.

By drawing on diverse research threads and theoretical notions, this paper advances a comprehensive assessment of existing FVA research, particularly in the context of the trade-off between informativeness and the stewardship objective.

The application of FVA, particularly through the mark-to-market accounting, entails a considerable range of assumptions and judgments. Some commentators describe FVA as being ‘fictional’ and ‘imaginary’ in essence (Casson and Napier, 1997) with a potential to promote manipulation and bias. Yet it also implies more timely and decision-relevant information, supporting the prevalence of FVA in the viewpoint of current accounting standard setters (Danbolt and Rees, 2008, Whittington, 2008). However, the authors question the ability of decision-useful information to replicate the stewardship effect. This conundrum has stimulated our interest in FVA within the context of the stewardship function, echoed in the following question: ‘How does the information embedded in fair values support the demand for information to control agents?’

Much of the existing research focuses on the effect of FVA on market proxies such as valuation differences across fair value hierarchy levels (So and Smith, 2009; Goh et al., 2015; Magnan et al., 2015), valuation differences between recognised and disclosed fair values (Müller et al., 2015; Chung et al., 2017; Israeli, 2015), and valuation differences across different corporate governance structures (Song et al., 2010; Siekkinen, 2016). Other studies have explored the effect of FVA on corporate decisions such as debt structure (Wang and Zhang, 2017; Demerjian et al., 2016), CEO compensation and dividend policy (Sikalidis and Leventis, 2017; Shalev et al., 2013; Manchiraju et al., 2016) and capital structure (Valencia et al., 2013; Greiner, 2015). Others have focused on the factors driving the choice between fair value and historical cost accounting (Quagli and Avallone, 2010; Mäki et al., 2016; Hlaing and Pourjalali, 2012; Guthrie et al., 2011; Cairns et al., 2011; Chang et al., 2021). Moreover, some authors have discussed the usefulness of fair value measurement in relation to countries with different socio-economic environments (Balfoort et al., 2017; Zhang et al., 2012; Marra, 2016) and the impact of FVA on the quality and reliability of accounting information (Dahmash et al., 2009; Dietrich et al., 2001; Landsman, 2007). All the research threads mentioned above are based upon the informational approach, representing the majority of FVA research. This significant portion of FVA research reflects the shift towards the notion of the information usefulness of financial statements that occurred in the late 1960s (Beaver, 1981).

The authors argue that the impact of FVA cannot be fully understood without considering the long-standing objective of financial reporting, the stewardship function, and without factoring in the developments in the major accounting standards. Therefore, our interest is in the conceptual basis of FVA emerging from the IASB and FASB Conceptual Frameworks. Both frameworks emphasise ‘decision-usefulness’ as a general purpose of financial reporting, in particular, towards existing and potential investors and creditors in capital markets. The key argument highlights the view that shareholders make decisions other than to buy, sell or hold securities; their other concerns also include the evaluation of management and potential intervention to correct agency problem. Thus, financial reporting should effectively enable shareholders to evaluate management contribution towards the shareholder value enhancement. In other words, information provided within financial statements should minimise information asymmetry between shareholders and managers to effectively evaluate management performance. However, fair value accounting presents an additional layer of concern to this assessment. The key issue emerges from the emphasis that fair value places on current values which may be significantly affected by elements other than management conduct, most predominantly associated with market volatility.

Despite the acknowledgement from the accounting policy setters, it was asserted that shareholders’ reporting requirements could be subsumed within the general purpose of decision-usefulness, served by providing information relevant to prediction of future cash flows. In this paper, the link between the stewardship function and FVA is revisited by reviewing and classifying relevant FVA literature. For this paper, stewardship is not solely defined on the basis of information provision to assist an evaluation of the competence and integrity of appointed agents. Instead, the authors question the arguments justifying the ability of decision-relevant information to fully replicate stewardship effects. The first argument relates to the primacy of the demand for information to protect property rights to hold agents accountable; and the second notion argues for such information to be capable of verification in order for it to be fully effective (Miller and Oldroyd, 2018). The stewardship function requires not only the information that could explain the values of assets and liabilities at the start and the end of an accounting period but also information to justify the changes in these values. While the authors do not argue that the stewardship function entails close adherence to historical cost accounting, this study reflects upon the argument that FVA hinders the generation of information that could fully replicate stewardship effects (Ronen, 2008; Lennard, 2007; Whittington, 2008).

The existing FVA research has moved forward in three different strands. First, the majority of research interest examines the impact of FVA on equity valuation (Hann et al., 2007; Carroll et al., 2003; Petroni and Wahlen, 1995; Barth, 1994) and FVA impact on economic decisions made by financial intermediaries (Lim et al., 2013; Magnan et al., 2015; Ayres et al., 2017). Secondly, following the joint project between IASB and FASB to develop a conceptual framework, the second strand evaluates the fundamental shift in the development of accounting standards towards emphasis on the primacy of assets and liabilities rather than their value changes (Sutton et al., 2015; Bromwich et al., 2010). Thirdly, an important strand of the literature has surfaced in response to the accusations of FVA being a cause of the subprime mortgage crisis which resulted in the global financial meltdown in 2007-08 (Laux and Leuz, 2009; Véron, 2008). The key concern of this strand of research asserts that FVA exacerbates swings during the business cycle with potential to provoke a contagion effect across the financial markets.

There is a limited understanding of the overall FVA research terrain that would identify and document new perspectives in relation to existing approaches in FVA research. The contribution of this paper addresses the knowledge deficiency in the context of the stewardship function. The importance of the link between fair value accounting and the stewardship function becomes evident when evaluating the management contribution towards shareholders’ value. The adoption of fair value accounting, primarily served by market input, has been justified by its ability to provide decision-relevant information to investors to predict future cash flows. However, the assessment of managers’ contribution to shareholders value may not be satisfied by the market information since these are exogenous to management performance.

By categorising the existing literature into discrete domains, the authors intend to provide more robust insight into approaches to FVA research and suggest future research ideas to address FVA research complexity. To fulfil these two objectives, a narrative literature review of FVA research is conducted. Compared with systematic reviews which use a set of rigid rules, narrative reviews are particularly valuable when there is a need to identify new research opportunities (John and Lawton, 2018). Furthermore, narrative literature reviews establish patterns and trends in the literature and thus help to identify gaps and inconsistencies in the body of knowledge (Machi and McEvoy, 2016). Subjectivity, typically acknowledged as an issue in narrative reviews, can be mitigated by borrowing more rigorous strategies from systematic literature review methodology (Hammersley, 2001; Jones and Gatrell, 2014).

While this paper has adopted a narrative literature review methodology, in order to improve the objectivity and verifiability of the analysis, the authors have decided to follow more transparent and less biased procedures when selecting relevant studies. To further enhance the research transparency, the conceptual boundaries are first outlined, followed by determination of thematic and disciplinary parameters and research process. The authors then present the literature review results by establishing key domains emerging from the sample selected. In conclusion, possible future research directions in FVA literature are developed and highlighted.

Conceptual boundaries – what is fair value?

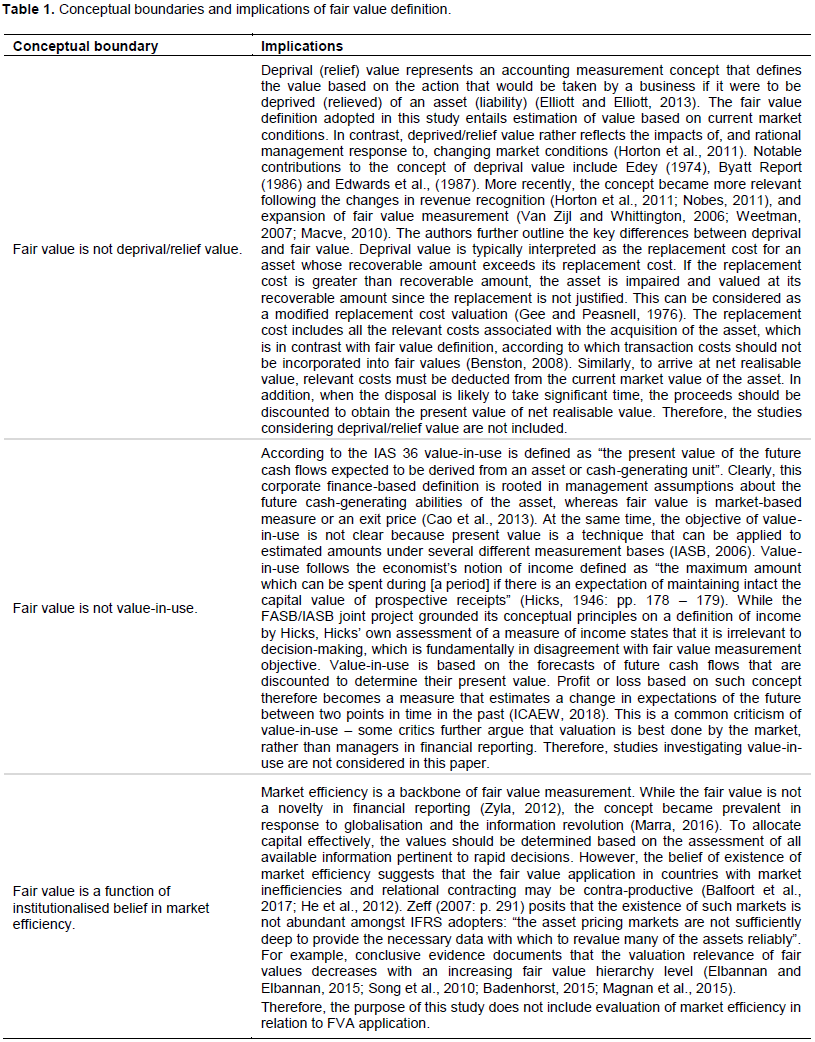

The conceptual boundaries established in this study are based upon a fair value definition in accordance with the International Accounting Standards Board (IASB, 2007) and Financial Accounting Standards Board (FASB) the two major accounting standards setters. In their respective accounting standards (IFRS 13 and SFAS 157), fair value is defined as “the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date” (IFRS, 13.9). It is worth mentioning that this definition entails further assumptions such as those about its measurement and classification. There are some practical misconceptions with the definition of fair value that are explained in the accounting standards. For example, while the definition of fair value requires the use of exit values, in some cases, value-in-use and entrance values are used instead. This inconsistency arises from the individual perception of the value of an asset. For instance, when there is no potential purchaser, fair value (the exit value) would be equal to zero or even negative, however, a different entity might regard the price of the asset as the value to that firm and use value-in-use instead (Benston, 2008). Therefore, the authors envisage several conceptual implications of the fair value definition adopted in this study and decide to delineate its conceptual boundaries explicitly in Table 1.

Thematic boundaries – what FVA themes are relevant to this study?

The authors distinguish between research into the conceptual principles of FVA, and research into decision-usefulness in the context of FVA. These two literature streams emphasise different origins and implications adopted within existing FVA literature. In the first stream, FVA originates within the accounting standard setters’ pronouncements, hence the focus on its theoretical basis established in the Conceptual Framework. The second stream originates within the application of FVA standards in financial reporting. This stream of research evaluates decision-usefulness of FVA through the information perspective. According to the information perspective useful information is defined as “signals capable of transforming a priori expectations into a posteriori expectation” (Hitz, 2007: p. 333). Therefore, signals embedded in fair values may also provide relevant information to support the stewardship role.

Stream 1 primarily considers research into reliability and quality of fair values, the role of the Conceptual Framework in development and expansion of FVA, and the so-called “de-legalisation of the balance sheet” (Power, 2010: p. 205) of an economic institution. The focus on reliability and quality of fair values can be explained, at least in part, by the use of estimates of hypothetical market prices at Level 2 and 3 of the fair value hierarchy. The project by IASB and FASB to develop a joint conceptual framework and its amendments, such as the shift from reliability to faithful representation, and the removal of free from bias from the fundamental qualitative characteristics, further support the trend in favour of FVA in the development of accounting standards for many years to come. The case is often made that the FASB and IASB highlight the primacy of assets and liabilities, based on a definition of income grounded on a theory prevalent in economics (Sutton et al., 2015). However, the attributes contained within this definition solely apply to assets and liabilities in complete and perfect markets (Bromwich et al., 2010), a fact which further questions the reliability of Level 2 and 3 fair values. These theoretical underpinnings are vital to the development of future accounting standards and the way they approach different stakeholders’ informational needs.

Stream 2 focuses on the examination of FVA information content. The accounting information has an information value if “the benefits of the improved decisions [resulting from incorporating such accounting information into decision making] exceed the cost of information procurement and processing” (Hitz, 2007: p. 333). In other words, information embedded in fair values is decision relevant if the provision of such data can be viewed as cost-efficient information aggregation (Barth, 2000; Beaver, 2002). The analysis of the information aggregation criterion has primarily been directed towards evaluation of value relevance in the context of standard setting. Besides the valuation approach which prevails in information perspective, others evaluate the impact of FVA on corporate decisions such as debt structure (Wang and Zhang, 2017; Demerjian et al., 2016), CEO compensation and dividend policy (Sikalidis and Leventis, 2017; Shalev et al., 2013; Manchiraju et al., 2016) and capital structure (Valencia et al., 2013; Greiner, 2015). In addition, other research focuses on the factors driving the choice between fair value and historical cost accounting (Quagli and Avallone, 2010; Mäki et al., 2016; Hlaing and Pourjalali, 2012; Guthrie et al., 2011; Cairns et al., 2011; Chang et al., 2021). To sum up, this paper considers FVA as a consequence of theoretical principles outlined in the Conceptual Framework and as a dimension in decision-making for relevant stakeholders.

Disciplinary boundaries

Most FVA studies and their implications are in the field of accounting, finance and economics. In particular, there are numerous studies in the area of the economic consequences of FVA on the regulatory capital (Chircop and Novotny-Farkas, 2016; Laux, 2016; Valencia et al., 2013; Greiner, 2015; Fiechter et al., 2017). These studies are beyond the scope of our review. This is because, for the most part, these studies seek to establish the impact of FVA on the financial stability objectives through the lens of banks’ regulatory capital. They specifically address the link between FVA and banks’ financial reporting, and thus concentrate on the implications of FVA on a specific set of stakeholders - banks’ supervisors and regulators. As outlined earlier, this study is concerned with the evaluation of FVA in the context of the stewardship function. Therefore, within the stewardship function, it is argued that the implications of the theoretical principles delineated in the Conceptual Framework (Stream 1) and the application of FVA standards on decision-making (Stream 2) are the most relevant streams of FVA research to consider. Given that this paper is primarily concerned with the conceptual basis of FVA and its implications on the information content of accounting in the context of stewardship role, our focus is on studies published in the accounting journals only. Through focusing on an accounting discipline, the authors could capture more relevant studies with an essence of accounting based on legal protection of property rights of shareholders encompassed within the stewardship function of financial reporting.

Research process

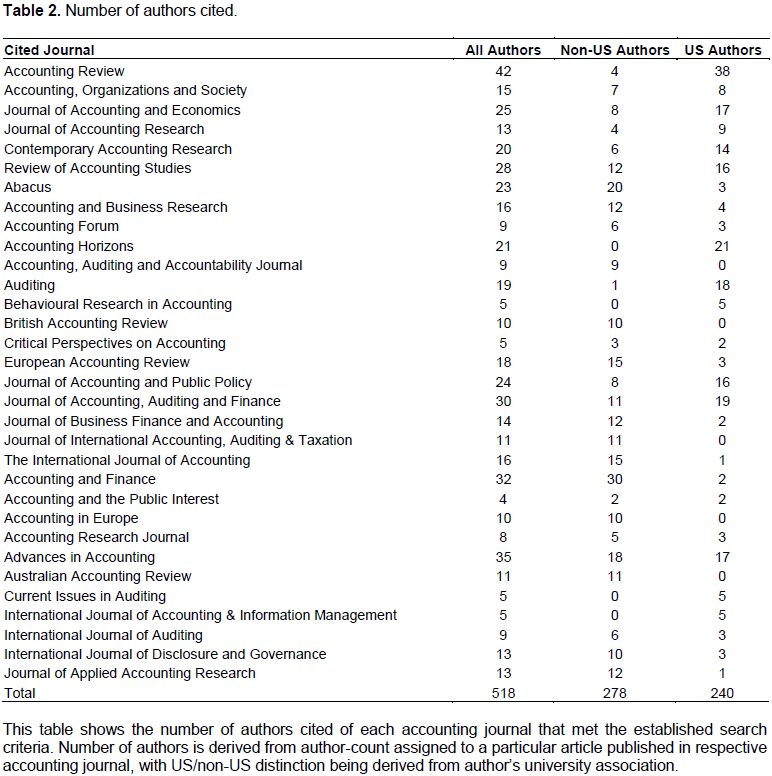

The search criteria for the literature review have been based on relevant keywords, time period and database. SCOPUS database was used for the literature search with the following keyword fair value included in the article title, keywords or abstract. All peer-reviewed articles published in the accounting journals as per the Association of Business Schools in Academic Journal Guide (2018) have been included. The database was designed primarily to provide data for an examination of the accounting literature by academics from different traditions, notably between US-based and non-US-based academic researchers. Given that this paper is primarily concerned with the theoretical underpinnings as per the joint IASB/FASB Conceptual Framework, the authors analyse the breakdown between the studies published by US versus non-US authors. Table 2 illustrates the number of authors cited of each accounting journal that met the established search criteria. The sample is relatively balanced in terms of a breakdown between accounting academics with US versus non-US tradition, with 240 and 278 authors cited respectively. This study spans a time horizon from January 2007 to June 2017 and reviews 158 journal articles (Figure 1). The purpose of these search criteria was to provide a comprehensive overview of research literature concerning FVA with a focus on recent evidence from both theoretical and empirical research. The database search was conducted in June 2018. While all the accounting journals listed in ABS Academic Journal Guide (2018) have been targeted, the analysis has focused on studies with methodological and theoretical rigor published in higher-ranked journals (the journals rated 3 and above in the ABS system).

Sample quality

Considering the sample generated by the adopted research process, two issues are raised about its quality. First, there is a clear divide between theoretical and empirical studies where exclusively theoretical studies provide direct insights into stewardship evaluation in the context of FVA. On the other hand, empirical research is substantially based on evaluation of policy change and policy implementation in the context of decision-usefulness for investment decision-making. This clear-cut division suggests that the adoption of FVA is strongly associated with enhancement of information content to facilitate investment decisions, rather than the stewardship role of financial reporting. Since our major field of interest is at the intersection of stewardship and FVA, the sample is focused on studies concerning theoretical insights into this relationship. Nonetheless, the authors still view empirical evidence on decision-usefulness as a relevant stream of research, in particular, when evaluating the stance subsuming the stewardship objective within decision-usefulness (Miller and Oldroyd, 2018). Therefore, this literature stream has been incorporated in the review of the literature.

Second, there is a significant number of studies concerning FVA and its contribution to the Global Financial Crisis 2007/08 (GFC) (Laux and Leuz, 2009; Véron, 2008; Ryan, 2008; Goh et al. 2015; Elbannan and Elbannan, 2015; Blankespoor et al., 2013; Bleck and Liu, 2007; Amel-Zadeh and Meeks, 2013). This paper also accounts for these studies in the sample, since they represent substantial and significant evidence concerning FVA usefulness through both theoretical and empirical points of view. In principle, these studies are not part of Stream 1 nor Stream 2 as defined in Thematic Boundaries section. This is because most of these studies seek to establish the relationship between the financial crisis and FVA in the context of wider financial stability objectives. As argued earlier, this stream of research is primarily valuable to banking regulators and thus this group of studies has been integrated on a selective basis to fit the purpose of the two research streams already identified.

Research framework

The analysis starts with the development of the research framework by seeking criteria or assumptions that would allow evaluation of studies from different perspectives. The studies evaluate FVA from two distinct viewpoints: (1) FVA as a result of a conceptual shift in financial reporting; and (2) FVA as an enhancement to the decision-usefulness of general-purpose financial reporting. The subsequent sections discuss the two domains in further detail.

Domain 1: FVA - a result of a conceptual shift in financial reporting

The conceptual perspective on FVA in the context of the stewardship function is well established in the FVA literature. The scope of the studies facilitates understanding of the role of the IASB/FASB joint Conceptual Framework in the development of accounting standards applying fair value measurement (Whittington, 2008; Hitz, 2007; Ronen, 2008; Yong et al., 2016; Sutton et al., 2015). The joint project has sparked interest amongst academics discussing the possible implications of the common framework, and its changes, for measurement basis in current and future accounting standards. The development of the common framework has come under the spotlight following GFC when its conceptual underpinnings were actively reconfigured to serve financial markets (Zhang and Andrew, 2014).

The first phase of the Conceptual Framework Project, completed in 2010, dealt with the objective and qualitative characteristics of financial reporting. It emphasises decision-usefulness as a general purpose of financial reporting, in particular towards investors and creditors in capital markets. In contrast, the stewardship function is viewed as valuable only in so far as it contributes to the overall aim of decision-usefulness in investment decision-making. Whittington (2008: pp. 141 – 142) states that this move was “a bold step at the time, sweeping away the traditionalist view that accounting is primarily for legal and stewardship purposes, with decision usefulness as a useful possible additional benefit”. The lack of a proprietary perspective within the general-purpose view was acknowledged in a substantial volume of comments from IASB members, stating that decision-usefulness entails more than just the prediction of future cash flows. Despite the recognition, it was asserted that the stewardship role of financial reporting could be subsumed within the general purpose of decision-usefulness, served by providing information relevant to prediction of future cash flows.

The literature has further evaluated the changes introduced in the joint project, which are likely to impact the interpretation of the underlying principles (Zhang and Andrew, 2014; Whittington, 2008; Ronen, 2008; Yong et al., 2016). The main change in language was the replacement of ‘reliability’ by ‘faithful representation’. Whittington (2008: p. 146) asserts that this amendment “eliminate[s] the possibility of a trade-off between relevance and reliability” which was seen as an important factor in the precedent framework and which is often cited as a major concern in FVA. The other important aspect that can be seen as tilting the criteria of the Framework in favour of FVA is the removal of the phrase ‘free from bias’. Many opponents argue that fair value estimation involves significantly more subjectivity (bias) than the alternative measures, and thus this change reduces the force, within the Framework criteria, of this objection. Whittington (2008) further argues that the Conceptual Framework implicitly assumes perfect and complete markets, which is in conflict with, what he refers to as ‘alternative view’, that regards markets as imperfect and incomplete where financial statements fulfil a stewardship function. Ronen (2008) calls for a more comprehensive set of theoretical accounting principles and governance reforms that would align the interests of managers and shareholders. This reflects a long-standing debate over the competing objectives of financial statements (informativeness vs. stewardship) and the recent developments in conceptual underpinnings, which broadly support FVA (Ronen, 2008; Whittington, 2008).

Other studies evaluate changes in the Conceptual Framework in relation to the definition of income and resulting conceptual primacy of assets (Penman, 2009; Yong et al., 2016; Hitz, 2007). Given the superiority of the Conceptual Framework principles in the formation of accounting standards, Sutton et al. (2015) point to FVA as ‘a default presumption’ to serve general purpose financial reporting with asset-liability approach following its theoretical foundations. The move towards FVA reflects the belief that the key objective of financial statements is to measure the financial position of a business entity. The asset-liability approach deems income statement merely as a medium to reflect changes in the value of assets and liabilities during the accounting period. In contrast, under the revenues-expenses perspective, the income statement is the primary tool that summarises the transactions between the entity and the markets with value added being reported as accounting income. Controversy surrounding the asset-liability approach can also be observed when looking into reporting of other comprehensive income and comprehensive income. The comprehensive income represents “the change in equity (net assets) of an entity during a period from transaction and other events and circumstances form non-owner sources (paragraph 56, FASB Concepts Framework 2, 1980). This definition emphasises the value changes of the assets and liabilities, rather than the residuals stemming from matching revenues with expenses, as in traditional income statement (Zhang and Andrew, 2014; Zeff, 1999). Reporting of comprehensive income is based upon the notion of clean surplus accounting that recognises unrealised gains and losses from value changes in assets and liabilities (Andrejcik, 2016). These value changes would typically bypass the traditional income statement and be reported as a direct adjustment to equity. However, their inclusion under other comprehensive income and comprehensive income puts emphasis on real economy performance and its fluctuation. Given that elements of other comprehensive income typically include transitory and non-operating flows, their relevance in evaluation of long-term earnings generation is limited. Instead, these would rather emphasise investment decisions driven by financial speculation (Zhang and Andrew, 2014).

Following the Great Depression and Savings and Loans Crisis, enthusiasm for the superiority of assets and liabilities was revived by adopting a theory prevalent in economics. The pursuit of the FASB/IASB joint project grounded its conceptual principles in a definition of income by Hicks (1946). Although this step has broadly been welcomed by the academic community, some commentators have expressed concern that such theories must be considered in their entirety. Bromwich et al. (2010) present reasons why the Hicksian concept of income cannot be invoked to support the asset-liability approach as promoted by IASB/FASB. First, the application of Hick’s definition of income requires the presence of complete and perfect markets to reliably capture the value of business in the observable market prices of their net assets. Since markets are rarely perfect or complete and the value of a firm is more than just a sum of its assets (less liabilities), the significant cash flow components are being excluded and not compounded into the value of business. Secondly, Hicks’ own assessment of a measure of income states that it is irrelevant to decision-making – fundamentally in disagreement with Boards’ decision-making usefulness objective of general-purpose financial reporting. Thirdly, if the focus were to move towards income ex ante, it can be argued that it is equally important to consider the standard stream concept of income (Hicks No 2 income) in order to triangulate the amount to be reported as a firm’s expected earnings. Others have suggested that the accounting arena becomes a sub-discipline of financial economics.

IASB defines income as a by-product of the measurement of assets and liabilities in the balance sheet. Baker and Penman (2016) note that by conceptually assigning primacy to assets and liabilities, an income statement approach involving matching expenses to revenues is rejected. Although there is generally broad consensus over the importance of income statement (Penman, 2009), it is less clear what information it should carry in order to improve its relevance to decision makers. Adding to its significance, Yong et al. (2016) indicate that chartered accountants perceive the income statement as being the primary financial statement. Penman (2009: p. 358) also points out the substance of income statement when reporting a firm’s value of intangible assets values by stating that “income statement perfectly corrects for a deficient balance sheet and the case where it does [report it] so imperfectly”.

Other studies have shown how FVA is not always deemed reliable and bias-free given the range of estimation sources allowed when determining fair value (Landsman, 2007; Penman, 2007; Power, 2010; Marra, 2016; Danbolt and Rees, 2008; Balfoort et al., 2017; Benston, 2008). Power (2010: p. 201) suggests that reliability in accounting is a social construct that allows for subjective estimates to acquire authority “when they come to be embedded in taken-for-granted routines”. On a similar note, some authors have suggested that compliance with accounting rules automatically generates reliable and credible information, even if the rules may be incoherent or difficult to comply with (Barth, 2007; Ravenscroft and Williams, 2009). Barth’s conception of reliability shifts the attention from transaction-based reliability to notions of markets and the values they provide. However, this idea of reliability greatly depends on the level of market efficiency, which is an inherent assumption of value relevance studies. With market efficiency challenged in recent years, even Level 1 fair values become of questionable reliability (Marra, 2016).

In the extreme case of economic equilibrium, in which all information is incorporated into asset prices, it is generally agreed that the purpose of traditional financial reporting would be limited, if any (Barth and Landsman, 1995; Beaver and Demski, 1979). However, in the real world of imperfect information and uncertainty, financial reporting plays an important part in economic decision-making and so does the measurement system. A debate about the pros and cons of FVA takes us back to the underlying issue of trade-off between relevance and reliability. Advocates of FVA often appeal to notions of verifiability and objectivity of fair values since these are quoted and taken from the active markets. On the other hand, opponents argue that fair values are subject to greater estimation error by management, and prone to greater managerial discretion. In particular, the reliability concept suffers fundamental problems if fair values are not readily observed on the active markets and management must estimate these using considerable discretion or manipulation (Landsman, 2007; Pandya et al., 2021). The research suggest that fair values are informative to investors, but the value relevance diminishes with higher level of fair value hierarchy, which is often a subject of management bias and measurement error (Song et al., 2010). These limitations create information asymmetry between investors and management undermining the reliability of financial statements and essentially render effective monitoring of management accountability (Landsman, 2007; Penman, 2007).

Despite the concerns over fair value fictionality and intellectual incoherence, the proponents frequently argue that it offers a higher and updated level of information to financial statement users supporting its primacy in current standard setters’ viewpoint (Danbolt and Rees, 2008, Whittington, 2008). Since FVA is based on the philosophical underpinnings of ‘Western’ market economies, its application in cultures where market inefficiencies and relational contracting are present may not be suitable (Pandya et al., 2021; Balfoort et al., 2017; He at al., 2012; Peng and Bewley, 2010). Balfoort et al. (2017) argue that the qualitative characteristics of neutrality and faithful representation in fair value measurement may seriously be undermined in Asian economics and transactions. A similar line of evidence is provided by Pandya et al. (2021: p. 216) which documents reluctance of South African practitioners to apply fair value measurement due to its “de-emphasis of the traditional stewardship role of financial reporting” and costs associated with fair value estimation and subjectivity. This research theme has further emphasised the implications of FVA and its strong reliance on market efficiency. The perceived benefits associated with FVA adoption may be strongly dependent on the existence of efficient markets, which strengthens the reliability concerns. However, the concept of reliability is primarily relevant for the information usefulness perspective within which current value is the backbone of ability to make future projections. However, accounting data should primarily provide objective feedback about the actions managers have taken, rather than subjective expectations about future prospects (Sterling, 1970; Edwards et al., 1987).

Domain 2: FVA - an enhancement of decision-usefulness in general-purpose financial reporting

Most scholars have examined FVA via the lens of valuation relevance supporting the notion of decision-usefulness. The studies confirm that the value relevance of fair values is negatively related with fair value hierarchy (So and Smith, 2009; Siekkinen, 2016; Goh et al., 2015; Magnan et al., 2015; Müller et al., 2015; Chung et al., 2017; Israeli, 2015; Song et al., 2010; Badenhorst et al., 2015), which supports the argument that investors are more likely to decrease the weight they place on less reliable Level 2 and Level 3 fair value estimates. Given greater information asymmetry associated with higher fair value levels, researchers became interested in the potential of firm-internal and external characteristics to alleviate this impediment. Song et al. (2010) provide evidence that firms with weaker corporate governance mechanisms exhibit greater information asymmetry leading to more severe moral hazard problems and thus lower value relevance. Siekkinen (2016) uses similar reasoning and documents that value relevance of fair values is positively associated with the level of a given country’s investor protection. The lack of value relevant fair value information is evident is countries with weak investor protection environments, where only Level 1 estimates are significantly relevant for valuation purposes.

Other studies associate value relevance with risk modelling. For example, Bhat and Ryan (2015) find that banks’ market risk and credit risk modelling improve the value relevance of their fair value gains and losses, in particular for less liquid instruments. In response, McDonough and Shakespeare (2015) suggest that risk modelling may improve the faithful representation of fair values by reducing estimation error. They continue by noting that risk modelling activities may result in “fair value estimates that are more verifiable and understandable to investors” (McDonough and Shakespeare, 2015: p. 98). Badia et al. (2017) echo these arguments by providing evidence that the conditional conservatism of Level 2 and 3 financial assets fair values increases when the measurements are evaluated by more knowledgeable investors, verified by more independent third parties, and disclosed more fully in financial statements. These findings suggest that investors are sensitive to reliability deficiencies in Level 2 and 3 fair values, which cause investors to discount these measurements. If one agrees with the statement in Zeff (2013: p. 313) that stewardship can be defined as “an indicator of management effectiveness in generating a return to shareholders”, reporting higher levels of fair values cannot only act as a detriment to potential investors due to reliability concerns, but it may also introduce a noise preventing existing shareholder from effectively evaluating management conduct.

A further underlying feature of studies in this domain is that they place an emphasis on the existence of efficient markets – assuming that market figures represented by share values are not only unbiased but error-free (Holthausen and Watts, 2001). However, there is a general consensus that accounting figures (such as those represented by fair values) may be measured with error and thus be unreliable (Barth, 1994). This view has serious implications, since FVA has been under significant scrutiny for its potential to promote manipulation and bias, as discussed in Domain 1. Since prior studies point to a considerable information asymmetry among fair value hierarchy levels (in particular in Level 2 and 3 fair values), researchers also became interested in answering whether (and why) managers use the inherent opportunity to exercise discretion while determining fair values. The studies mostly focus on accounting for goodwill and intangible assets where considerable management latitude to exercise discretion and judgment is necessary to convey private information about future cash flows (Jarva, 2009; Filip et al., 2015; Bens et al., 2011). Based upon agency theory, it is predicted that managers exploit the unverifiable goodwill estimates to manage earnings opportunistically in line with their own private incentives. The research evidence documents the fact that although both goodwill and identifiable intangible assets are valuation-relevant, they are not reliable, which is in line with the fact that unverifiable information can be used opportunistically since estimates are rather difficult to challenge ex-post (Dahmash et al., 2009; Ramana, 2008; Ramanna and Watts, 2012).

The second theme of this domain cuts across a presentation format of fair values (Müller et al., 2015; Israeli, 2015; Riedl and Serafeim, 2011; Chung et al., 2017; Blacconiere et al., 2011). In particular, these studies evaluate the pricing differences across recognised and disclosed fair values. This stream of research is motivated by a psychology-based framework predicting that presentation format does not affect users’ acquisition and evaluation of information but does significantly impact their information weighting (Maines and McDaniel, 2000). A change in reporting location can result in strengthening the perception of importance, in particular, if the change increases the visibility of that information. Research evidence documents the fact that investors place a different value on fair value information disclosed versus that recognised in financial statements, with disclosed information being significantly discounted (Israeli, 2015; Müller et al. 2015). Schipper (2007) indicates that recognised and disclosed fair values possess differential attributes in terms of reliability and information-processing costs. Müller et al. (2015) support this reasoning by providing evidence of reduced discounting in firms employing an external appraiser (a proxy of high reliability) and in firms followed by a high analyst (a proxy of low information-processing costs). This further strengthens a suggested positive relationship between information asymmetry and fair value discounting.

Within this research theme, the role of supplemental fair value disclosure in mitigating reliability concerns is also considered central to FVA discussion. On average, these studies support the view of decision-usefulness enhancement as a result of additional disclosures related to fair value inputs (Riedl and Serafeim, 2011; Chung et al., 2017). Research evidence documents that greater exposure to more opaque financial information, such as that reflected in Level 3 fair values, leads to higher information risk. The evidence within this research theme further supports the findings of decreasing value relevance associated with increasing fair value hierarchy level. Chung et al. (2017) find that firms with more subjective estimates are more likely to supplement additional disclosures in view of improving investors’ perceptions of fair values reliability. The emergence of supplementary disclosures is consistent with a perception by managers that there are benefits to such disclosures. Evidence provided by Blacconiere et al. (2011) supports this hypothesis, however, there is also evidence pointing to managers using disclosures opportunistically.

Although economic theory predicts that disclosure improves management transparency (Verrecchia, 2001), studies such as Clor-Proell et al. (2014) question additional disclosure as it may lead to information overload and inefficient information processing. In contrast, they point to ‘visibility’ of fair values and conclude that the separation of financial information into multiple columns can improve users’ judgments about the reliability of fair value estimates. This finding suggests that simple changes to the income statement can facilitate the use of supplemental accounting disclosures. Lachmann et al. (2015) provide similar evidence regarding IFRS 9, which requires the changes in fair value of liabilities to be presented in other comprehensive income and thus excluded from net income (IFRS 9.5.7.7(a)). Their evidence indicates that the evaluation of firm performance is less biased if fair value gains are reported separately from net income. These results echo the fact that characteristics of the presentation format influence individual information processing and suggest that acquisition of information is enhanced by a degree of isolation. Since the degree of visibility is greater in other comprehensive income presentation format, this leads to lower cognitive costs and thus lower information asymmetry (Maines and McDaniels, 2000). Additionally, it suggests that separation of transitory and non-recurring items improves predictive ability of reported earnings (O’Hanlon and Pope, 1999). This is important not only for equity valuation purposes but can be equally relevant for stewardship purposes since temporary changes in fair values resulting from non-operating flows do not reflect management’s ability to enhance shareholder wealth.

Domain 2 also considers the significance of fair values for decision processes made by financial analysts. The majority of the evidence suggests that financial analysts are well aware of fair value related issues, in particular those concerning reliability, since they tend to devote considerable attention to FVA implications (Bischof et al., 2014; Gaynor et al., 2011; Koonce et al., 2011). This may be explained by the negative implications on financial analyst forecast accuracy and forecast dispersion following the reclassification choice of financial assets (Lim et al., 2013; Fiechter et al., 2017; Paananen et al., 2012).

Drawing on the notion of the trade-off between reliability and relevance, an important research area of this domain seeks to establish the link between the recent financial crisis and FVA. This research has been integrated into this review since its underlying motivation is to evaluate whether FVA contributed to the crisis via its reliability concerns. For stewardship purposes, any financial turmoil represents a risk of losing property entitlements held by shareholders. In particular, concerns exist over market reactions when assets are marked to market once it is recognised that there are ties to contracts and regulation (Laux and Leuz, 2009).

The recent global financial crisis has turned attention towards procyclicality and its effect on the reliability of fair value estimates. A key concern is that fair value measurement exacerbates swings during the business cycle with potential to provoke contagion effect across the financial markets (Laux and Leuz, 2009). Véron (2008) further notes that procyclicality could artificially enhance the apparent robustness of the balance sheet during economic booms, and by the same measure, weaken the financial position in times of economic busts. This is manifested by the fact that FVA provides early signals of depression in asset values, which forces businesses to take action and sell assets early at a price below their fundamental value (Ryan, 2008). Regulators have also expressed concerns that FVA can encourage procyclical lending by exaggerating banks’ profits during expansionary times and thus improving banks’ ability to access credit (International Monetary Fund, 2008; SEC, 2008). Goh et al. (2015) and Elbannan and Elbannan (2015: p. 143) observe that whilst Level 1 and Level 2 fair values are priced superior to Level 3 fair values during GFC, there is an indication of pricing differences reduction after GFC. This could suggest that investors are concerned with the likelihood that banks might have to liquidate their assets at fire-sale prices during GFC, however, these concerns are alleviated as the economic cycle recovers. In other words, provision of fair values might serve investors’ needs when estimating of exit values during economic downturn rather than management contribution to shareholders’ value when considering going concern perspective.

By contrast, academics emphasise that FVA improves the transparency of financial information by providing timely and relevant financial data, and as such the trade-off between transparency and financial stability needs to be addressed by prudential regulations that “accept FVA as a starting point but sets explicit counter-cyclical capital requirements” (Laux and Leuz, 2009: p. 832). In support, Blankespoor et al. (2013) provide evidence that credit risk in the banking industry is better explained when financial assets are measured at fair value. This indicates that fair value information provides the earliest signal of financial trouble, consistent with the theoretical model developed by Bleck and Liu (2007), which suggests that historical cost accounting may conceal a company’s true financial performance, while FVA is better equipped to reveal poor economic performance.

DIRECTIONS FOR FUTURE RESEARCH

This FVA literature review identifies two distinctive research domains in the context of the stewardship function of financial reporting: FVA as a result of a conceptual shift in financial reporting; and FVA as an enhancement of decision-usefulness in general-purpose financial reporting. While the two domains are discussed in separation, both domains have some common features. In particular, the two domains are confined in the specific pronouncements made by the accounting bodies. In other words, the FVA literature has been stimulated by the facts embodied in the accounting standards and therefore research has mostly suggested the ex-post evidence. Our findings also identify shortcomings in existing FVA literature and propose resulting directions for future research. These limitations stem from two observations: first, great emphasis has been placed on events in the world economy, and second, there is a great disconnect between accounting standard setting and academic research. These two concerns and future research opportunities to approach these concerns are discussed in the following section.

FVA – revolution or evolution?

It is well-known that the rise of FVA, in general, is attributed to the specific challenges of accounting for derivatives and other financial instruments, and indicates a new distinctive episode described as financialisation in accounting (Power, 2010). Proclaimed as “the beginning of the end of conventional accounting” (Nobes, 1999: p. 48), these changes have been referred to by many commentators as profoundly systemic and qualitative (Müller, 2014) and liable to re-format the principles of financial reporting. Some even refer to Thomas Kuhn’s theory of scientific revolutions (1996), according to which natural science does not develop through incremental advances, but through a period of revolution when the ideals are redefined, followed by periods of modest scientific progress within an established paradigm (Barlev and Haddad, 2003; Dodd et al., 2008). In this context, the movement from historical cost to fair value is not revolutionary, but rather evolutionary (ICAEW, 2018). The shift in theoretical principles embedded in the joint Conceptual Framework should be understood in terms of ongoing social, political and economic changes and not the alleged technical superiority of FVA over historical cost (Müller, 2014). This could explain not only the emergence of a particular accounting theory, but also its unprecedented success and wider endorsement by regulators and policy setters. These socio-politico-economic changes have manifested themselves in unparalleled growth of financial markets, financial investment and dominance of the circuit of money capital (Barlev and Haddad, 2003).

Furthermore, some commentators argue that widespread FVA implementation has been driven by events in the world economy rather than the work of academics or standard setting bodies (Whittington, 2015). Marra (2016) outlines the way in which the information revolution, innovations and globalisation have played a significant role in establishing FVA as a financial reporting measurement system. The emergence of new industries driven by activities embedded in intangible assets has led to an increasing need for information to reflect the requirements of a globalised economy. Globalisation has placed further emphasis on efficient capital allocation informed by proper assessment of all available information pertinent to rapid decisions.

The authors argue that current FVA research has not fully reflected upon the evolutionary progression of the global economy and does not critique the relevance of fair value in relation to the neo-liberalisation and financialisation of political and economic systems currently taking place (Zhang et al., 2012). Instead, much of the research is concentrated around evaluation of decision-usefulness with respect to investment decisions. The widespread emphasis on valuation-centric concepts further serves to strengthen the already prevailing role of capital in the Anglo-Saxon variety of capitalism in terms of praising a financial analyst as a principal of the market mechanism. It can be argued that this path is inherently uncertain, most notably the way in which FVA “compresses an expected vision of the future into present values, which can subsequently become mistaken for economic reality” (Perry and Nölke, 2006: p. 581).

“A brave new world in financial reporting” (Ball, 2016: p. 545) and its focus on decision relevance can be regarded as primarily concerned with short-term financial performance, given its emphasis on continuous price movement in capital markets. This view overlooks the enduring solvency and stability of a business which places emphasis on a conservative and cautious view of the future, acknowledging inherent uncertainty (Perry and Nölke, 2006). Instead, decision-relevant information is primarily forward-looking in order to be pertinent to future cash flow predictions. This feature is also inconsistent with the second argument about stewardship-relevant information that should be capable of verification to be fully effective for stewardship purposes. While fair values may be decision-useful, their verifiability, for example via the contracting process, is not met. The essence of fair value definition is to derive a price estimate obtainable in a hypothetical market transaction between willing parties.

Bridging the gap between standard setters and academics

The accounting profession does not develop in vacuum. Accounting standards and other professional pronouncements are developed by practitioners with different epistemic commitment – that is, different level of professional knowledge template (Reybold, 2008). The professional knowledge templates become pertinent when discussing the notion of financial measurement since it defines one’s assumptions about the nature of knowledge and its purpose. For example, in the context of historical cost accounting, emphasis is placed on reliable and verifiable information to fulfil managers’ stewardship responsibilities. In contrast, FVA implies that current value reporting enhances information value-relevance for investment decision-making purposes. This contention between the two underlying views of purpose of financial reporting is ever present and may impact not only accounting standard setting, but equally academic research and its focus. This has been primarily observed with respect to a shift from a normative to a positive stance where decision-usefulness evaluation becomes a dominant research instrument. This increasing narrowness of accounting research in terms of philosophical principles, methodological approaches and theoretical underpinnings in mainstream accounting research undermines the fundamental nature of the discipline as one of the social sciences (Lukka, 2010). The positive approach towards accounting research has been primarily supported by the adoption of the notion of decision usefulness that puts emphasis on capital market data. Such research typically starts with specific policies such as accounting standards and examines whether transactions in accordance with such policies can enhance information usefulness. However, the deductive approach does not question the principles of accounting standards development, and thus, cannot offer any significant insights beyond the already established epistemic commitment emerging from the notion of decision usefulness. It is argued for keeping paradigm debates open and dynamic, since praising market capital data presents an issue of data reliability, as discussed earlier. In addition, it is unlikely that one accounting research paradigm could fully embrace the central issue of purpose of financial reporting and financial measurement. Allocation of financial, human, natural and knowledge resources play relevant roles in the definition of financial reporting efficiency (Van Mourik, 2013). Furthermore, accounting practitioners should not be seen as solely technicians whose reflective capacities are to be constrained within explicit statements of accounting standards. Durocher and Gendron (2014) provide evidence of a low degree of cognitive unity among practitioners with respect to financial measurement. This demonstrates the variety of epistemic commitment exercised by accounting practitioners, demonstrating the relevance of normative questioning of accounting principles such as decision-usefulness underpinned by FVA. This argument closely relates to Kuhn’s theory of scientific revolutions (1996) which could advocate a need to change the set of practices to formulate and examine research questions.

On the other hand, the focus of standard setters has allegedly shifted from a positive to a normative attitude, in which prescription of conceptual underpinnings has been criticised as “cherry-picking […] to serve the immediate aims of standard setters” (Bromwich et al., 2010: p. 348). Bromwich et al. (2010: p. 348) warn against picking and quoting parts of a theory in pursuit of principles-based concepts and standards due to dangers of “misunderstanding and misinterpretation of the element of a theory” leading to even more distortion.

The division between academic research and policy-standard setting has not merely resulted from the conflicting theoretical viewpoints, but rather from the limited efforts by practitioners to turn to academia in development of new practices (Kaplan, 2011). McKelvey (2006) claims that practitioners do not value academic research findings and are not motivated to seek engagement with academic research output. This divide certainly points to FVA research which primarily appears as a response to the proposed changes in the conceptual framework or issuance of a particular accounting standard or its amendment both initiated by the policy setters. Diffusion of innovation theory has been proposed to remedy a research-practice gap in accounting (Tucker and Lowe, 2014), according to which new ideas, beliefs, knowledge or practices should be communicated in a two-way fashion. Change, the last stage of diffusion of innovation theory, represents the ultimate objective of applied academic research, when evidence from research is adopted and put into practice. While fair value reporting is gradually improving from the practical viewpoint, it is questionable how much these innovations are informed by the research findings at the epistemic level. For instance, Fülbier et al. (2009: p. 483) argue that “academics should take standards setters’ politically set objectives as given and, through their research, help identify means to achieve them”. They continue noting that academic research should be understandable to practitioners and, in particular, have the characteristics of ex ante research.

The question of whether the academic research should be ‘repackaged’ to be considered by the standard setters, or whether standard setters should become more eager to acknowledge the academic research is up to the future researchers. However, even though FVA research has gone down the path of evidence from positive research, the research shows that the adoption of FVA has some major epistemic shortcomings. Therefore, standard setters need to pay attention to these limitations and concede them in their reporting practices.

The FVA project is currently at a stage when there needs to be further debate about the current complex, diverse and apparently inconsistent financial measurement practices. In this paper a narrative literature review of FVA research in the context of the stewardship function has been conducted. In doing so, existing literature has been categorised into two distinctive domains: FVA as a result of conceptual shift in financial reporting; and FVA as an enhancement of the decision-usefulness of general-purpose financial reporting.

The existing FVA research demonstrates that the style of argument adopted tends to be top-down and deductive. This approach is suitable in situation where issues can be examined by defining terms and where evidence is non-existent. However, the challenge presented by financial measurement does not follow this principle (ICAEW, 2018) and entails more collaborative efforts among academic researchers and policy setters. In particular, the existing FVA literature reflects the focus on the information content objective that strengthens the emphasis on information provision for the prediction of future cash flow. Such focus is criticised for its inadequacy to fulfil the stewardship function of financial reporting. This observation highlights the fact that the majority of FVA literature adopts the external view of fair value examination emphasising the decision usefulness view and reliance on capital market data. The support for the evidence-based approach could be explained by the number of pronouncements made by policy standard setters that fed more into hypotheses statements and further empirical testing.

In response, two dimensions are outlined that could facilitate the examination and exploration of the FVA question in further detail in relation to the stewardship role. First, the evolutionary process to financial measurement could explain the shift from historical cost to fair value. “[B]odies of practices are rarely systematic; they have evolved over time as collections of diverse responses to practical problem” (ICAEW, 2018: p. 6). In other words, FVA should be seen as a response to financial reporting problems previously unencountered, and not as technically superior to historical cost accounting (Müller, 2014). New ways of doing business, such as financial instruments and share-based payments, have presented challenges which needed innovative ways to understand a business’s financial performance and position. Practices like frequent revaluations designed to deal with disparities between current value and historical cost fit a logic of evolution.

Secondly, the theoretical research suggests that FVA is connected with a shift in socio-politico-economic changes which follow a financialisation of money capital. This has provided the strong systematic theoretical backdrop against which FVA firmly stands in accounting pronouncements. Therefore, the authors call for a greater engagement between policy-setters and academics, in particular, when choosing the conceptual underpinnings for financial measurement. Overall, it is suggested that much of the FVA research has been backward looking, focusing on the effect of existing accounting standards rather than the possible effects of alternative measurement options.

The authors are also aware that our research review is limited to the last ten-year period. However, the fundamental nature of measurement in financial reporting makes it essential to evaluate how FVA research is evolving. Doing so at the time of rapid progression of FVA into practice is valuable for both academics and practitioners as it exposes new avenues of research and the weaknesses of its practical application.

Finally, as with all interpretative research, the findings are constrained by the breadth and depth of the data analysed and our own interpretation of the results. Thus, the authors take all responsibility for our interpretation of the results including any errors and omissions.

The authors have not declared any conflict of interests.

The authors thank the participants at the 2019 annualcongress of the European Accounting Association (EAA) in Paphos (Cyprus) and the participants at the 2018 British Accounting and Finance Association (BAFA) annual conference in London (UK), for many useful comments.

REFERENCES

|

Accounting Standards Board (ASB) (2007). Stewardship/accountability as an objective of financial reporting: A comment on the IASB/FASB Conceptual Framework project. Available at:

View

|

|

|

|

Amel-Zadeh A, Meeks G (2013). Bank failure, mark-to-market and the financial crisis. Abacus 49(3):308-339.

Crossref

|

|

|

|

|

Andrejcik D (2016). Value relevance of profit and loss and comprehensive income in the Slovak Republic (Unpublished master's dissertation), The Open University, Milton Keynes, UK.

|

|

|

|

|

Ayres D, Huang X, Myring M (2017). Fair value accounting and analyst forecast accuracy. Advances in Accounting 37:58-70.

Crossref

|

|

|

|

|

Badenhorst WM, Brümmer LM, de Wet JH vH (2015). The value-relevance of disclose summarised financial information of listed associates. Journal of International Accounting, Auditing and Taxation 24:1-12.

Crossref

|

|

|

|

|

Badia M, Duro M, Penalva F, Ryan S (2017). Conditionally conservative fair value measurements. Journal of Accounting and Economics 63(1):75-98.

Crossref

|

|

|

|

|

Balfoort F, Baskerville RF, Fülbier RU (2017). Content and context: "Fair" value in China. Accounting, Auditing and Accountability Journal 30(2):352-377.

Crossref

|

|

|

|

|

Ball R (2016). IFRS - 10 years later. Accounting and Business Research 46(5):545-571.

Crossref

|

|

|

|

|

Baker R, Penman S (2016). Moving the conceptual framework forward: Accounting for uncertainty. Unpublished paper, Oxford University and Columbia University.

|

|

|

|

|

Barlev B, Haddad JR (2003). Fair value accounting and the management of the firm. Critical Perspectives on Accounting 14(4):383-415.

Crossref

|

|

|

|

|

Barton AD (1982). Objectives and basic concepts of accounting. Australian Accounting Research Foundation.

|

|

|

|

|

Barth EM (1994). Fair value accounting: Evidence form investment securities and the market valuation of banks. The Accounting Review 69(1):1-25.

|

|

|

|

|

Barth M (2007). Standard-setting measurement issues and the relevance of research. Accounting and Business Research 37(3):7-15.

Crossref

|

|

|

|

|

Barth M, Landsman W (1995). Fundamental issues related to using fair value accounting for financial reporting. Accounting Horizons 9(4):97.

|

|

|

|

|

Barth ME (2000). Valuation-based research implications for financial reporting and opportunities for future research. Accounting and Finance 40(1):7-31.

Crossref

|

|

|

|

|

Beaver WH (1981). Financial reporting: An accounting revolution. Englewood Cliffs, NJ: Prentice-Hall Inc.

|

|

|

|

|

Beaver WH (2002). Perspectives on recent capital market research. Accounting Review 77(2):453-474.

Crossref

|

|

|

|

|

Beaver WH, Demski JS (1979). The Nature of Income Measurement. The Accounting Review, 54(1):38-46.

|

|

|

|

|

Bens DA, Heltzer W, Segal B (2011). The information content of goodwill impairments and SFAS 142. Journal of Accounting, Auditing and Finance 26(3):527-555.

Crossref

|

|

|

|

|

Benston GJ (2008). The shortcomings of fair-value accounting described in SFAS 157. Journal of Accounting and Public Policy 27(2):101-114.

Crossref

|

|

|

|

|

Bhat G, Ryan SG (2015). The impact of risk modelling on the market perception of banks' estimated fair value gains and losses for financial instruments. Accounting, Organizations and Society 46:81-95.

Crossref

|

|

|

|

|

Bischof J, Daske H, Sextroh C (2014). Fair value?related information in analysts' decision processes: Evidence from the financial crisis. Journal of Business Finance and Accounting 41(3-4):363-400.

Crossref

|

|

|

|

|

Blacconiere WG, Frederickson JR, Johnson MF, Lewis MF (2011). Are voluntary disclosures that disavow the reliability of mandated fair value information informative or opportunistic? Journal of Accounting and Economics 52(2):235-251.

Crossref

|

|

|

|

|

Blankespoor E, Linsmeier TJ, Petroni KR, Shakespeare C (2013). Fair value accounting for financial instruments: Does it improve the association between bank leverage and credit risk? The Accounting Review 88(4):1143-1177.

Crossref

|

|

|

|

|

Bleck A, Liu X (2007). Market transparency and the accounting regime. Journal of Accounting Research 45(2):229-256.

Crossref

|

|

|

|

|

Bromwich M, Macve R, Sunder S (2010). Hicksian income in the conceptual framework. Abacus 46(3):348-376.

Crossref

|

|

|

|

|

Byatt Report (1986). Accounting for economic costs and changing prices. London, UK: HMSO.

|

|

|

|

|

Cairns D, Massoudi D, Taplin R, Tarca A (2011). IFRS fair value measurement and accounting policy choice in the United Kingdom and Australia. The British Accounting Review 43(1):1-21.

Crossref

|

|

|

|

|

Cao T, Donnelly R, Hasnah S (2013). Fair value and value in use: An improvement over historical cost? Accountancy Ireland 45(3):59-61.

|

|

|

|

|

Carroll TJ, Linsmeier TJ, Petroni KR (2003). The reliability of fair value versus historical cost information: Evidence from closed-end mutual funds. Journal of Accounting, Auditing and Finance 18(1):1-24.

Crossref

|

|

|

|

|

Casson P, Napier C (1997). Representing the future: Financial benefits and obligations, risk and accounting, Copenhagen, Denmark: AOS Conference on Accounting, Time and Space.

|

|

|

|

|

Chang YL, Liu CC, Ryan SG (2021). Accounting policy choice during the financial crisis: Evidence from adoption of the fair value option. Journal of Accounting, Auditing and Finance 63(1):108-141.

Crossref

|

|

|

|

|

Chircop J, Novotny-Farkas Z (2016). The economic consequences of extending the use of fair value accounting in regulatory capital calculations. Journal of Accounting and Economics 62(2-3):183-203.

Crossref

|

|

|

|

|

Chung SG, Goh BW, Ng J, Yong KO (2017). Voluntary fair value disclosures beyond SFAS 157's three-level estimates. Review of Accounting Studies 22:430-468.

Crossref

|

|

|

|

|

Clor-Proell SM, Proell CA, Warfield TD (2014). The effects of presentation salience and measurement subjectivity on nonprofessional investors' fair value judgments. Contemporary Accounting Research 31(1):45-66.

Crossref

|

|

|

|

|

Dahmash FN, Durand RB, Watson J (2009). The value relevance and reliability of reported goodwill and identifiable intangible assets. The British Accounting Review 41(2):120-137.

Crossref

|

|

|

|

|

Danbolt J, Rees W (2008). An experiment in fair value accounting: UK investment vehicles. European Accounting Review 17(2):271-303.

Crossref

|

|

|

|

|

Demerjian PR, Donovan J, Larson CR (2016). Fair value accounting and debt contracting: Evidence from adoption of SFAS 159. Journal of Accounting Research 54(4):1041-1076.

Crossref

|

|

|

|

|

Dietrich RJ, Harris MS, Muller KA (2001). The reliability of investment property fair value estimates. Journal of Accounting and Economics 30:125-158.

Crossref

|

|

|

|

|

Dodd JL, Rozycki JJ, Wolk HI (2008). Accounting Theory: Conceptual Issues in a Political and Economic Environment. Los Angeles, CA/London, UK: Sage Publications.

|

|

|

|

|

Durocher S, Gendron Y (2017). Epistemic commitment cognitive disunity toward fair-value accounting. Accounting and Business Research 44(6):630-655.

Crossref

|

|

|

|

|

Edey HC (1974). Deprival value and financial accounting. In: Edey HC, Yamey BS (eds,). Debits, Credits, Finance and Profits London, UK: Sweet & Maxwell.

|

|

|

|

|

Edwards J, Kay J, Mayer C (1987). The Economic Analysis of Accounting Profitability. Oxford, UK: Oxford University Press.

|

|

|

|

|

Elbannan MA, Elbannan MA (2015). Information content of SFAS 157 fair value reporting. Journal of International Accounting, Auditing and Taxation 25:31-45.

Crossref

|

|

|

|

|

Elliot B, Elliot J (2013). Financial Accounting and Reporting. Harlow, UK: Pearson.

|

|

|

|

|

Fiechter P, Landsman W, Peasnell R, Renders K (2017). The IFRS option to reclassify financial assets out of fair value in 2008: The roles played by regulatory capital and too-important-to-fail status. Review of Accounting Studies 22(4):1698-1731.

Crossref

|

|

|

|

|

Filip A, Jeanjean T, Paugam L (2015). Using real activities to avoid goodwill impairment losses: Evidence and effect on future performance. Journal of Business Finance and Accounting 42(3-4):515-554.

Crossref

|

|

|

|

|

Fülbier RU, Hitz JM, Sellhorn T (2009). Relevance of academic research and researchers role in the IASBs financial reporting standard setting. Abacus 45(4):455-492.

Crossref

|

|

|

|

|

Gaynor L, McDaniel L, Yohn T (2011). Fair value accounting for liabilities: The role of disclosures in unravelling the counterintuitive income statement effect from credit risk changes. Accounting, Organizations and Society 36(3):125-134.

Crossref

|

|

|

|

|

Gee K, Peasnell KV (1976). A pragmatic defence of replacement cost. Accounting and Business Research 6(24):242-249.

Crossref

|

|

|

|

|

Glover J (2014). Have academic accountants and financial accounting standard setters traded places? Accounting, Economics, and Law 4(1):17-26.

Crossref

|

|

|

|

|

Goh BW, Li D, Ng J, Yong KO (2015). Market pricing of banks' fair value assets reported under SFAS 157 since the 2008 financial crisis. Journal of Accounting and Public Policy 34(2):129-145.

Crossref

|

|

|

|

|

Greiner AJ (2015). The effect of the fair value option on bank earnings and regulatory capital management: Evidence form realized securities gains and losses. Advances in Accounting 31(1):33-41.

Crossref

|

|

|

|

|

Guthrie K, Irving JH, Sokolowsky J (2011). Accounting choice and the fair value option. Accounting Horizons 25(3):487-510.

Crossref

|

|

|

|

|

Hammersley M (2001). On systematic reviews of research literatures: A narrative response to Evans & Benefield. British Educational Research Journal 27:543-554.

Crossref

|

|

|

|

|

Hann RN, Heflin F, Subramanayam KR (2007). Fair-value pension accounting. Journal of Accounting and Economics 44(3):328-358.

Crossref

|

|

|

|

|

He X, Wong TJ, Young D (2012). Challenges for implementation of fair value accounting in emerging markets: Evidence from China. Contemporary Accounting Research 29(2):538-562.

Crossref

|

|

|

|

|

Hicks JR (1946). Value and Capital. Oxford, UK: Oxford University Press.

|

|

|

|

|

Hitz JM (2007). The decision usefulness of fair value accounting - A theoretical perspective. European Accounting Review 16(2):323-362.

Crossref

|

|

|

|

|

Hlaing KP, Pourjalali H (2012). Economic reasons for reporting property, plant, and equipment at fair market value by foreign cross-listed firms in the United States. Journal of Accounting, Auditing and Finance 27(4):557-576.

Crossref

|

|

|

|

|

Holthausen RW, Watts RL (2001). The relevance of value-relevance literature for financial accounting standard setting. Journal of Accounting and Economics 31:3-75.

Crossref

|

|

|

|

|

Horton J, Macve R, Serafeim G (2011). Deprival value vs. fair value measurement for contract liabilities: How to resolve the revenue recognition conundrum? Accounting and Business Research 41(5):491-514.

Crossref

|

|

|

|

|

IASB (2006). Preliminary Views on an Improved Conceptual Framework for Financial Reporting: The Objective of Financial Reporting and Qualitative Characteristics of Decision-Useful Financial Reporting Information. London: IASC Foundation.

|

|

|

|

|

IFRS Foundation (2011). IFRS 13 Fair Value Measurement. London, UK: IFRS.

|

|

|

|

|

IFRS Foundation (2011). IFRS 9 Financial Instruments. London, UK: IFRS.

|

|

|

|

|

Institute of Chartered Accountants of England and Wales (2018). Measurement in financial reporting. London, UK: ICAEW.

|

|

|

|