Full Length Research Paper

ABSTRACT

Banking plays a significant role in the economy of any country. Bangladesh is a Muslim dominated country and more than 80% of their populations are Muslim. These people have strong faith on Islamic rules and regulations and they want to lead their lives as per the canon given in the holy “AL- QURAN” (The religious book of Islam). But no Islamic banking system had been developed in Bangladesh up to 1983. The study focuses on Perception of Non Muslim Client/Customer on Islamic Banking in Bangladesh. Changes in the Bangladesh financial landscape and the introduction of Islamic banking have generated new dimensions and phenomena in the banking sector. Such scenario had also led to the changes in the customer’s (both Muslim and Non- Muslim) taste and demand for better and high quality banking services. This paper also aims at understanding the perception of Non Muslim client/customer on Islamic Banking and also their growth in Bangladesh. The study uses primary (180 sets of questionnaire on non-Muslim Islamic Banking client) published secondary data from various relevant sources, financial reports, websites, journals, and publications. The researcher used his own personal experience regarding the country’s socio economic background. The Islamic Banking Sector of Bangladesh is developing new financial products and services to meet the increasing clients’ (Non-Muslim) demand. Islamic banking sector increases its profit day by day and successfully meets its financial target.

Key words: Islamic banks, Islamic law, non-Muslim client, investment opportunity utilization, financial stability.

Abbreviation: JEL Code: G20; G21; N20INTRODUCTION

Banking sector plays an important role in the business sectors and in the industrialization of a country. Basically, the main jobs of schedule banks are taking deposits from the customers against interest and lending it to borrowers against interest for a cessation period. Banks also offer different interest rates on the basis of deposits. In the banking sector of Bangladesh, there are 4 types of banking system: Schedule commercial banks (national and private), Islamic banks (private and foreign), foreign commercial banks and specialized banks.

The main concept behind the Islamic banking system is to follow Islamic rules and regulations: interest free banking and equity based financing. Islamic banks offer savers risky open-ended mutual fund certificates instead of fixed-interest deposits. Difficulties however arise on the lending side. Arrangements to share profits and losses in Islamic banking lead to considerable problems of monitoring and control, especially in lending to small business”. Ahmed (1995) argues that the elimination of interest does not mean zero-return on capital. Rather, Islam forbids a fixed predetermined return for a certain factor of production i.e. one party having assured return and the whole risk of an entrepreneurship to be shared by others. The Islamic banking system also proposes that resources can be contracted on the basis of venture capital and risk sharing deals.

The idea of equity-based investment banking is not new to the financial market. If we look into history it may be observed that capital, as loan capital as well as venture capital, played a great role in promoting industrial and economic development of various countries of the world. Islamic banking is now spread over almost all the world, in both Muslim and non-Muslim countries, as a viable entity and financial intermediary. The second half of the twentieth century witnessed a major shifting of thinking in devising banking policy and framework on the basis of the Islamic system. This new thought was institutionalized at the end of the third quarter of the century, and emerged as a new Islamic banking system (Ahmad, 1984; 1981). Ahmed El Naggar is considered to be the first man to implement this concept. After the establishment of Mit Ghamr Local Savings Bank in a provincial rural center in the Nile Delta, Egypt in 1963, through the initiative of Naggar, the initial shape of Islamic banking modality was injected into the Egyptian economy. The establishment of the Islamic Development Bank (IDB) in 1975 gave formal momentum to the Islamic banking movement. Since the establishment of IDB, a number of Islamic banking and financial institutions have been established all over the world.

At present, more than two hundred Islamic banking and financial institutions are working in different parts of the world, and Iran and Pakistan have taken steps to reorganize their entire banking systems based on the Islamic model. Bangladesh was not inactive in this movement toward Islamic banking. One and a half decades have passed since the establishment of the first Islamic bank in Bangladesh in 1983, and the number of banks has risen to five, in addition to two Islamic branches of conventional banks. It is now time to analyze their function and performance. Keeping this in view, an attempt has been made here to focus on the growth, structure, and performance of Islamic banking in Bangladesh.

Problem statement

Bangladesh is a Muslim dominated country and more than 80% of its populations are Muslim. These people have strong faith on Islamic rules and regulations and they want to lead their lives as per the canon given in the holy “AL- QURAN” (The religious book of Islam). The study uses published secondary data from various relevant sources financial reports, websites, journals, publications and the researcher has used his own personal experience regarding the country’s socio economic background and its impact on the Islamic Bank Bangladesh Limited.

Changes in the Bangladesh financial landscape and the introduction of Islamic banking have generated new dimension and phenomena in banking sector. Such scenario had also led to the changes in the customer’s taste and demand for better and high quality banking services. Since the emergence of more financial institutions in recent years, both conventional and Islamic, customers, Muslims and non Muslims alike have been presented with enormous choices to choose from in terms of banking system (Abbas et al., 2003). Rather, customers are now spoilt for choices to choose the ones that meet their needs and wants before making any decisions. Similarly, this situation also applies to the system offered by the Islamic banking system.

These products not only have to compete with products offered by the conventional banking but also among the products offered by the Islamic banking itself. Due to this stiff competition, the Islamic banking therefore needs to consider several criteria such as bank’s image and performance, speed of transaction, channel of delivery system, banking convenience and product diversity to attract Muslims and non Muslims customers to continuously do banking business with them.

Islamic banking is gaining grounds with non Muslims in Bangladesh, where it was reported that half of some of Islamic banks customers in Bangladesh are non Muslims. Why is it so? Is it because of its resilience in the global economic downturn or strong liquidity management or any other reasons?

Purpose of the study

Based on the statement of problem, the purpose of this study is to investigate the following items:

1. Respondents’ background will influence customer’s perception towards Islamic banking products and service.

2. Views and general perception of non Muslims customers will influence Islamic banking system.

3. Establishment of Islamic banking in Bangladesh will create more banking opportunity for non-Muslims.

4. Islamic banking system is able to dominate conventional banking in Bangladesh.

LITERATURE REVIEW

Islamic Banking Act 1983 (IBA) was introduced to allow the establishment of IBS with the Conventional Banking System (CBS). The IBS offers system in accordance to the Shariah law as well as principles and subject to Bank Negara Bangladesh regulation (Central Bank of Bangladesh, 2006).

Bank Islam Bangladesh Berhad (BIMB), which was established in July 1983, was the first Islamic bank in Bangladesh established under the IBA 1983 with paid-up capital of RM80 million (Bank Islam, 2011). It operates under tight regulatory regime where it has to fulfill the conventional banking guidelines and regulation as well as IBA. BIMB was allowed to operate without a healthy competition for over 10 years.

The period is considered reasonable for BIMB to introduce and innovate Islamic banking system. In its first decade of operation, BIMB experienced a healthy growth with over 80 branches and 1,200 staff (Bank Islam, 2011).

After 10 years, the government thought it would be reasonable for the Islamic banking operations to be expanded so that more Muslims and non Muslims would be able to enjoy Islamic banking facilities. This led to the introduction of a dual banking system called Skim Perbankan Tanpa Faedah (Banking Scheme without Interest) (SPTF) in 1993 by the government of Bangladesh. The system allows conventional banking to offer Islamic Banking system besides their existing conventional system. As such, they need to set up a separate unit called Islamic Banking Unit (IBU) that will be entrusted and be responsible for all aspects of Islamic banking system. In 2007, the financial landscape saw further liberalizations by the government on the establishment Islamic banking institution with the establishment of several foreign-owned Islamic banking institutions in Bangladesh (Source: International Journal of Business and Social Science Vol. 3 No. 11; June 2012).

METHODOLOGY

Population and sampling

180 (one hundred and eighty) questionnaires were distributed to non- Muslim respondents in the area of Bangla Bazaar, Naya Bazaar, Tati Bazaar, Jatrabari (the area of non-Muslim zone are of Dhaka Bangladesh)

For the purpose of this study, the sampling technique used is probability sampling based on simple random sampling. A simple random sample is a subset of individuals (a sample) chosen from a larger set (a population).

Data analysis

Demographic profile

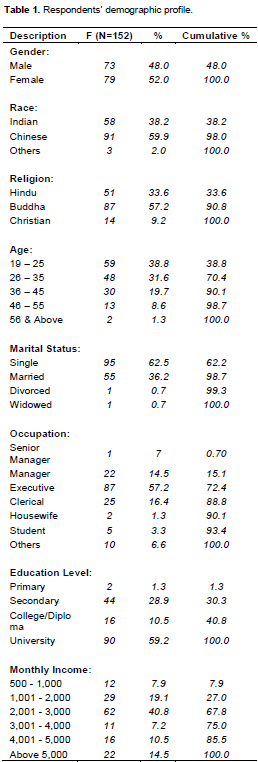

The backgrounds of respondents based on religion, race, gender, age, occupations, level of education, monthly income and type of banking institution used are in Table 1.

Out of the 180 survey questionnaires distributed, only 152 were returned to the researchers. From the total 152 respondents, 48 percent were males and 52 percent were females. This shows that the ratio between male and female is almost balance. Majority of the respondents (59.9%) were Chinese, while Indian (38.2%) and others (2.0%) made up the rest. On religion, from 152 respondents, Buddhist made up 57.2%; Hindus, 33.6% and Christians, 9.2%. Thus, the respondents represented a good mixture of Bangladesh’s non-Muslims, multi-religion society. The sample was collected from the group ranging between 19 to 56 years old. Nonetheless, the majority of the respondents were young, between the ages of 19 - 25 years old. They represent 38.8 percent of the sample. The result also showed that 62.5 percent of the respondents are single, 36.2 percent married and the balance 14 percent are equally divided between the groups consisting of divorcees and widows.

Analysis

The banking system of Bangladesh is composed of a variety of banks working as Nationalized Commercial Banks (NCBs), private sector banks, foreign sector banks, specialized banks, and development banks. Seventeen of the thirty-nine banks are private, out of which only five are Islamic Bank Bangladesh Limited, Al-Baraka Bank Bangladesh Limited, Al-Arafah Islamic Bank Limited and Social Investment Bank Limited, First security Islamic bank and Faysal Islamic Bank of Bahrain. Besides these full-fledged Islamic banks, two conventional banks in the private sector, namely Prime Bank Limited and Dhaka Bank Limited, have opened two full-fledged Islamic banking branches, and an Islamic banking counter, respectively. The five Islamic banks in Bangladesh cover only 5% of total deposits and 4% of total investments (loans and advances in the conventional sense), and operate only 2.84% of the bank branches. Historically, conventional banks are guided by the broad-based capitalistic monetary framework and business environment, which is predominantly based on interest. Only Iran, Pakistan, and Sudan, and Bangladesh to an extent, are on the way toward establishing an interest-free monetary and banking system on an economy-wide basis. It is gratifying that the transition from an interest-based banking system to an interest-free one has proceeded smoothly both in Pakistan and Iran.

In many countries, on the other hand, Islamic banks operate without any proper legal backing or provision, and face difficulties from the hostility of the entire environment. In Bangladesh Islamic banks have been operating since 1983 without any legal backing, relying instead on the guidelines framed in the Memoranda and Articles of Association submitted to Bangladesh Bank at the time of incorporation. Islamic Bank Bangladesh Limited started operation in the private sector in 1983 on a joint ownership basis, and had only 105 branches by June 1998.

The central bank has the sole authority to issue currency, manages the liquidity of the economy and monitors the monetary policy for maintaining the stability of money value and regulating banking system in Bangladesh. As a central bank, Bangladesh Bank was not aloof from the ongoing changes in the world financial system, especially in the country’s own banking system. It issued a license for the establishment of the first Islamic bank in Bangladesh in 1983. The Bangladesh Government participated in establishing Islamic Bank Bangladesh Limited, by taking a 5% share in the paid up capital. Taking the lack of Islamic financial markets and instruments or products in the country into consideration, Bangladesh Bank granted some preferential provisions for the smooth development of Islamic banking in Bangladesh, including the following:

1. Islamic banks in Bangladesh have been allowed to maintain their Statutory Liquidity Requirement (SLR) at 10% of their total deposit liabilities, instead of the 20% set for conventional banks. This provision facilitated Islamic banks to hold liquid funds for more investment, and thereby generate more profit.

2. Under the indirect monetary policy regime, Islamic banks have been allowed to fix their profit-sharing ratios and markups independently, in accordance with their own policy and banking environment. This freedom in fixing PLS ratios and markup rates provided scope for the Islamic banks to follow the principles of the shariah independently.

3. Islamic banks have been permitted to reimburse 10% of their proportionate administrative cost on a part of their balances held with the Bangladesh Bank. This facility has given some scope for the enhancement of the profit base.

An analysis of the performance of Islamic banking

Performance evaluation is an important prerequisite for the sustained growth and development of any institution. It is customary to evaluate the predetermined goals and objectives of commercial banks. With changing goals and objectives, the criteria for evaluation have changed over time. For the performance evaluation of the Islamic banking in Bangladesh, the “Banking Efficiency Model” must be taken into consideration.

Banking Efficiency Model criteria have been developed to measure the efficiency of the Islamic banking system. These five criteria are measured and expressed in terms of ratios. The following discussion deals with the empirical testing of the findings from dynamic analysis to measure the overall efficiency and performance level of Islamic banks operating within a conventional banking set-up in Bangladesh. Primary data were collected directly from the banks’ concerned departments.

Productive efficiency of Islamic banks

Investment opportunity utilization test

Under productive efficiency, it can be seen that Fund Utilization Rate (FUR) of IBBL went up progressively from 1989 to 1992, but fell to 0.75 in 1993. While it was more than 100% in 1996, it fell to 0.88 in 1997. Al-Baraka showed a higher FUR after 1989, due to its large non-performing assets, though normally considerably lower than the present rate. AIBL recorded 65% for 1996, and 75% for 1997, which also showed an increasing trend in fund utilization. SIBL also recorded 56 to 63%; PBL’s Islamic branches showed figures of 48.70% in 1996, which fell to 30.23% in 1997, due to the opening of a new branch. FIBB also showed a low rate of 21%, due to investments in limited areas. Deposit Mobilization per Employee doubled for IBBL from 1988 to 1997, despite mixed trends during the period. ABBL and other Islamic banks also showed a rising trend. Fund utilization per employee also showed the same trend for all banks. Though fund utilization showed improvement, it was still below the optimal level, due to the state of the economy, competition among Islamic banks, and borrowers’ preference for conventional banks.

Profit maximization test

All the four indicators of Profitability (i.e. Income-Expenditure Ratio, Profit-Expenditure Ratio, Profit- Loan-able Fund Ratio, and Profit-Employed Fund Ratio) show that IBBL and Al-Arafah experienced a declining trend, while ABBL and SIBL incurred huge losses for several years. The decline shown by the former two was due to the growing percentages of their investments which were converted into bad debts, which reduced their incomes, as well as the requirement to maintain bad debt provisions for classified loans. Of the latter two, ABBL incurred losses due to a huge amount of non-performing loans, while SIBL’s losses were due to conflicts between the owners and management of the bank.

Project Efficacy Test

How far a bank can contribute effectively in running a project it finances can be determined by the level of linkage it can establish through its financing mechanism, which are:

1. Project selection criteria.

2. Pre-financing appraisal of projects.

3. Post-financing supervision.

4. Built-in mechanical linkage of the bank to its financed projects.

Loan recovery test

It is evident from an analysis conducted by the central bank that the number of bad debts of Islamic banks is raising. The ratio of bad debts to total debts rose from 18% in 1996 to 20% in 1997.

Test of elasticity in loan financing

The loan financing mechanism of Islamic banks is still not very elastic. Islamic banks in Bangladesh lack modes to meet call loan demands and the working capital needs of entrepreneurs. They also face problems in inter-bank borrowing due to a lack of suitable financing modes.

Operational efficiency of Islamic banks

The two criteria used to measure operational efficiency of Islamic banks are Per Employee Administrative Cost (PEAC), and Administrative Cost/Loan-able Fund Ratio (ACLFR). The PEAC of all Islamic banks is increasing. PEAC for IBBL in 1996 was Taka 91,362.00, which reached Taka 188,807.00 in 1997. The ACLFR also shows an increasing trend. Since both ratios are increasing steadily, it can be seen that the banks are stable.

Allocative efficiency of Islamic banks

Allocative efficiency can be analyzed by examining the application of modes of financing, which shows that short-term trade financing on the basis of markup is extensively used. The shares of musharaka and mudaraba modes where profitability acts exclusively as an allocative device, in portfolio distributions are declining, however. Investment under musharaka has declined; while there have been no mudaraba investments at all. Islamic banks in Bangladesh cannot use mudaraba financing as a tool for investment.

Distributive efficiency of Islamic banks

Distributive efficiency is measured by three criteria; percentage shares of a bank’s gross income going to its depositors (indicated by its profit-income ratio), the distribution of deposits and advances classified by account size, and the rural-urban classification of deposits and advances. Profit-income ratio denotes the percentage share of income distributed to the depositors as profit. It is assumed that a high ratio indicates better distribution of income generated by financing. IBBL’s ratio declined from 23.01% in 1996 to 12.47% in 1997, and Al-Arafah’s rose from 9.16 to 31.10%. Al Baraka’s showed a negative trend as the bank has been maintaining provision for huge bad debts since 1990, and SIBL’s ratio fell due to a conflict between the Chairman and the management till mid-1998. The overall situations of both banks have been improving recently, due to better loan discipline, and increased cooperation between the owners and managers. Al- Baraka’s half-yearly balance sheet for the period ending June 1998 shows that the bank has been able to make a profit, and SIBL is working to reduce its losses. Al Baraka’s loss has been reduced from Taka 273.20 million in 1996 to Taka 162.12 million in 1997, while SIBL’s loss has fallen from Taka 18.94 million to Taka 5.46 million. The annual rate of growth of deposits in the Islamic banks stood at 20% for IBBL, 10% for ABBL, 300% for Al-Arafah, and 140% for SIBL. The two Islamic banking branches of Prime Bank Limited also made remarkable progress in mobilizing deposits. In 1996 they mobilized deposits from Taka 400.83 million to Taka416.97 million. In 1997, this growth fell by Taka 12.74 million. For IBBL, deposit accounts of Taka 10,000 and below represented 5.84% of the whole, while investment in them amounted to only 0.67%. For ABBL the figures were 9.04 and 0.001%; for AIBL, 0.03 and 0.0001%; and for SIBL, 0.01 and 0.01%. For deposits up to Taka 50,000, the ratios were 0.06 and 0.01% for IBBL; 0.05 and 0.001% for ABBL; 0.03 and 0.005% for AIBL; and 0.01 and 0.15% for SIBL. Fifty percent of the total deposits made to Islamic banks came from accounts amounting to Taka 300,000 or less, while investment in them was only 0.03%. Islamic banks in Bangladesh are thus following the current trend of transferring investable resources from low-income depositors to high-income borrowers, and thus creating greater income inequality. It is evident from an analysis of the rural-urban classification of deposits and advances of a bank whether its allocation of financial resources has distributional implications. Since there was no data available, it proved impossible to conduct this analysis. According to the Quarterly Scheduled Banks Statistics, however, during April- June 1997, the total distribution of deposits by urban/rural areas revealed a ratio of 77:23, while the ratio of an advance was 82:18. Since the report treats the banking system as a whole, ignoring the operation of government owned banks will result in a much lower ratio. The urban bias in investment will be prominent in private sector banks, including Islamic banks, since their investment operation was designed to be urban-oriented.

Analysis: Non Muslim clients’ perception

Among the common factors used to measure customers’ selection criteria are cost and benefits of products offered, service delivery (fast and efficient), confidentiality, size and reputation of the bank, convenience (location and ample parking space), friends and families’ influences and friendliness of personnel of Islamic banks. Additionally, the religious issue is also perceived as one of the important criteria to be considered for the selection of Islamic banking services.

The bank selection criteria are expected to affect a customer’s overall satisfaction towards his or her bank. These studies have identified a number of such factors: convenience (i.e. the location), friends’ recommendations, reputation of a bank, availability of credit, competitive interest rates, friendliness of bank staffs, service charges, adequate banking hours, availability of ATM, specially services and the quality of services of checking accounts.

Researchers have looked into attitudes towards Islamic banking and the criteria used by customers to select a particular bank have specifically looked into the bank selection criteria used by customers to bank either with Islamic bank or conventional bank. These studies reported that customers who only banked with the Islamic banks chose to do so because of provision of fast and efficient service, bank’s reputation and image and bank’s confidentiality. However, since these studies were conducted almost a decade ago, it was appropriate to investigate once again the bank selection criteria adopted by Muslims customers Of Old Dhaka. As far as the Islamic banking system is concerned, no attempt is made to study customers’ satisfaction. They concluded that the Islamic banks should put more coherent efforts to improve their long term competitive position.

Studies show that Non Muslim customers prefer Islamic banking for savings, safety, and reliable for their needs. So they are satisfied with Islamic banking in Bangladesh.

Based on the findings, it could be concluded that Islamic services and products are well-received by non-Muslims population especially in Old Dhaka (Naya bazaar, Tati bazaar, Shakari bazaar, Jatrabari) Bangladesh. They are fast gaining popularity and more widely accepted by the society at large, in particular the non-Muslims. The results also indicated that majority of the respondents have both Islamic and conventional banking accounts. This

phenomenon is also in line with the worldwide support on Islamic banking.

Meanwhile, the respondents were unsure if the establishment of Islamic banking will improve the overall banking facility and products. They were also unsure about the customer’s perception and the potential of Islamic banking products in the future. This may be due to lack of information provided by the banking fraternity to the public. Also, not much has been written on the potential of Islamic banking products that could alleviate any misunderstanding of the Bangladeshi public.

Non Muslim respondents will consider establishing a banking relationship with Islamic bank but they need to have sufficient information of Islamic banking operations. However, the finding indicated that male respondents are more particular on the bank’s image and reputation when selecting an Islamic bank. Therefore this study developed certain perception of non Muslim on Islamic banking although conventional banking is more dominant than Islamic banking in Bangladesh. Non Muslim respondents, especially those with higher education level strongly believed that Islamic banking would dominate conventional banking in Bangladeshi. This is due to their easy access to information on Islamic banking.

CONCLUSION

Based on the findings in this study, it could be concluded that Islamic services and products are well-received by non Muslims population especially the old Dhaka, Bangladesh. They are fast gaining popularity and are more widely accepted by the society at large, in particular the non-Muslims. The results also indicated that the majority of the respondents have both Islamic and conventional banking accounts. This phenomenon is also in line with the wide support worldwide on Islamic banking.

The study also revealed that non-Muslims of the age group between 19 – 35 years old and with higher education possessed better knowledge and understanding on Islamic banking system. This is due to a wider exposure to news and information from various sources. They state that the higher the age level, the more possibility people will engage in Islamic system; while educated people have better understanding of the concept of Islamic banking operations.

The survey result is also consistent with old Dhaka study which indicated that non-Muslim respondents will consider establishing a banking relationship with Islamic bank if they have sufficient information of banking operations. On the criteria of selecting Islamic banking system, the study revealed that there is no specific demographic profile of non-Muslim customers and also the criteria used for selection of Islamic banking system. However, there may exist some constraints in the study which had resulted in the inconsistency of the results as the respondents surveyed are within the old Dhaka where most banks, including Islamic and conventional are within vicinity and most banks, be it Islamic and conventional provides the same level of services.

Therefore, this study developed certain perception of non Muslim on Islamic banking although conventional banking is more dominant than Islamic banking in Bangladesh. Non Muslim respondents, especially those with higher education level strongly believed that Islamic banking would dominate conventional banking in Bangladesh. This is due to their easy access to information on Islamic banking.

On the degree of the non Muslim’s customer perception of an Islamic banking, most respondents are unsure whether the establishment of Islamic banking will improve the general banking facility and products. This may be due to lack of public information on knowledge and news of Islamic banking since not much had been widely and publicly written on the potential of Islamic banking systems in the future. Nevertheless, most respondents strongly agree that Islamic banking will dominate the banking industry in Bangladesh.

CONFLICT OF INTERESTS

The authors have not declared any conflict of interests.

REFERENCES

|

Abbas SZM, Hamid MAA, Joher H, Ismail S (2003). Factors That Determine Consumers' Choice in Selecting Islamic Financing Products, Perceptions of customers towards Islamic banking system, Int. J Islamic Financial Services 3(4):13-29. |

|

|

|

|

|

Ahmed A (1995). "The Evolution of Islamic Banking" in Encyclopedia of Islamic Banking and Insurance. London: Institute of Islamic Banking and Insurance, |

|

|

|

|

|

Ahmad Z (1984). "Islamic Banking at the Crossroads: Development and Finance." In Islam pp.155-171. |

|

|

|

|

|

Ahmad Z (1981). Concept and Models of Islamic Banking: An Assessment. Islamabad: International Institute of Islamic Economics. |

|

Copyright © 2024 Author(s) retain the copyright of this article.

This article is published under the terms of the Creative Commons Attribution License 4.0