Full Length Research Paper

ABSTRACT

Zimbabwe’s economic progress is hinged on the performance of the agricultural sector, which supports the majority of the population. Bank credit empowers farmers to adopt inputs and technologies that are key for enhancing productivity and income. This study sought to establish the bank credit access trends among farmers in the Hurungwe District of Mashonaland West Province in Zimbabwe, comparing the current (2019-2015) and past (2014-2000) periods. A questionnaire was administered on a sample of 354 farmers. SPSS was used for data analysis. Credit access was significantly (p<0.05) influenced by the type of farmers, farmers’ education, age, farm size and alternative employment. Credit access was higher (p < 0.05) among Model A2 than Model A1 farmers, farmers with higher educational qualifications, aged between 46-55 years, with more than 35 hectares of farmland, and with alternative occupation. Failure to access bank loans by Model A1 farmers was ascribed to their lack of collateral assets, human capital and weather resilience infrastructure. Government should invest in irrigation infrastructure and create a conducive investment climate to stimulate financial capital inflows. Farmers should invest in physical and human capital to enhance their access to bank credit. Banks should devise collateral substitution models to avoid segregating poor farmers with productivity potential.

Key words: Bank credit, capital formation, credit access, Model A1 farmer, Model A2 farmer.

INTRODUCTION

Several nations like Japan, China and Korea have advanced and entered the ranks of developed nations because of their heavy investment in agriculture (Huang and Ma, 2010). African countries like Burkina Faso, Rwanda, Kenya, Cote d’Ivore, Ghana and Ethiopia that made vast investments in agriculture had great productivity from existing farms; they had 6% productivity increases annually, and had an average annual increase of 4% GDP in (AGRA, 2018). Therefore, no region in the world has developed a diverse, modern economy without initially establishing a successful foundation in agriculture (AGRA, 2017). Agriculture is also important in Zimbabwe, where the majority of the economically active population is self-employed in the sector (Swinkels and Chipunza, 2018). Approximately 36% of the adults in Zimbabwe also entirely rely on money from farming (Finmark Trust, 2014). Despite being central to livelihoods, the Zimbabwean agricultural sector faces various challenges, especially the farmers’ lack of access to financial capital for their operational and long-term investment needs in human and physical capital.

According to Echanove (2017), Zimbabwe’s national budgets have been largely inclined towards consumptive expenditure because of the prevailing economic turmoil, which saw most of the budgeted finance being taken up by administrative costs not operations. The Reserve Bank of Zimbabwe (RBZ, 2006) confirms that government funding from the fiscus has always fallen short of the national agricultural financing requirements, and consequently urges the banking sector to support the government to meet those needs. However, lending by private banks to agriculture is still very low in Zimbabwe. This is evidenced by low agricultural loan books in most commercial banks, which have mostly failed to reach the 20% threshold recommended by the RBZ (2016). The reduction in lending to agriculture is ascribed to the change in land tenure from freehold before independence in 1980, to user rights after the year 2000’s Fast Track Land Reform Program (FTLRP) (Richardson, 2005). The RBZ (2019)’s June Quarterly Economic Review showed bank agricultural loan portfolios improving to 20.59%, which improved further to 31.69% in the December Quarterly Economic Review (RBZ, 2019). Despite these improvements, local banks are yet to reach the pre-land reform maximum of 91.3% attained in the year 1999 (RBZ, 2006).

The government of Zimbabwe formulated various policies over the years seeking to improve the local farmers’ access to the indispensable bank credit, for example the 99 Year Lease Agreements (Inter-Ministerial Task-Force (IMT) Technical Committee, 2016) and the Collateral Registry (Government of Zimbabwe (GoZ), 2017; RBZ, 2013). However, concerns over the bankability of the 99 Year Lease Agreements have presented challenges over their acceptability by local banks, whilst the Collateral Registry is yet to be operationalized. Despite these interventions, several studies propagate that credit access constraints still persist in the agricultural sector in Zimbabwe. According to the Ministry of Agriculture (2013), commercial banks withdrew their outreach in rural areas where most farmers reside because of lack of collateral among farmers in the absence of legal title to land. Besides most farmers depend on rain fed agriculture, which exposes them to weather risks, especially droughts (Chakoma and Chummun, 2019; United Nations, 2014). Output price volatility also affects the farmers’ performance in terms of revenues and profitability, thereby reducing their loan repayment capacity (Leaver, 2004; Muchapondwa, 2009). Political interferences by the government also repel local banks from financing farmers in the country (Dale, 2009; Masiyandima et al., 2011; United Nations, 2014; Vitoria et al., 2012).

According to Mayowa (2015), agricultural credit includes all loans and advances granted to borrowers for financing and servicing agricultural production activities. Access to credit is key for improving agricultural productivity among poor resource farmers because it enables them to invest in their human and physical capital, thereby creating a pathway for economic development and poverty reduction (Anyiro and Oriaku, 2011). Madafu (2015) avers that credit access occurs when the price and non-price barriers are absent in the use of bank loans or credit by farmers. Therefore, he expounds that improved access to bank credit would mean improving the degree to which bank credit is available to everyone at a fair price. Several studies in Zimbabwe have explored alternative financing options for farmers in light of their failure to fulfil the local banks’ stringent collateral requirements (FACASI, 2015; Masiyandima et al., 2011; Vitoria et al., 2012). Besides, policy direction at government level has largely been enthused by the desire to circumvent the collateral hurdle to credit access, and to ensure that agricultural production amongst land reform beneficiaries perseveres despite the absence of collateral assets in resettlement farms. However, a few studies, if any, have attempted to measure the extent to which local farmers have accessed bank credit since the FTLRP, and how credit access varied across different farmer social groups. This is the gap that the study aims to fill, focusing on Model A1 and Model A2 farmers in the Hurungwe District of Mashonaland West Province in Zimbabwe. The study therefore seeks to establish bank credit access trends among farmers in Hurungwe District; and to explore the socio-demographic determinants of credit access among the farmers.

MATERIALS AND METHODS

The study was carried out in Hurungwe District of Mashonaland West province in Zimbabwe (Figure 1), which is a home to 4 273 Model A1 farmers and 1 107 Model A2 farmers (Agritex, 2019). The Model A1 comprises smallholder farmers with landholdings averaging 6 hectares. On the other hand, Model A2 farmers are settled individually on farm sizes ranging from 71-600 hectares, which are operated as commercial entities (Vitoria et al., 2012).

Data collection

A cross-sectional survey was carried out on a sample of 354 farmers. The sample size was determined by the Raosoft sample size calculator. Stratified random sampling was used to come up with 281 Model A1 farmers and 72 Model A2 farmers for the study. The study was underpinned by the positivism research philosophy and adopted quantitative techniques to answer its objectives. A pretested structured questionnaire was used to collect data from farmers.

Data analysis

The Statistical Package for Social Sciences (SPSS) Version 26 was used to analyze the data through frequencies, cross tabulations and Chi Square. Frequencies enabled the researcher to identify the number of farmers who accessed/ received term loans from banks in the two periods (2000-2014 and 2015 -2019) and to compare differences in credit access levels. Cross-tabulations also helped to establish the trends of bank credit access by farmers with different demographic characteristics like age, gender and education level. Chi Square enabled the determination of the significance of differences in credit access among farmers in the two periods under study, and to establish relationships between different farmers’ characteristics and access to bank credit. Chi Square was suitable for the study because the variable under study (credit access) was measured at the nominal/ordinal level, and was also measured by frequency counts (Mchugh, 2013). Findings from the study were presented using tables and figures.

RESULTS AND DISCUSSION

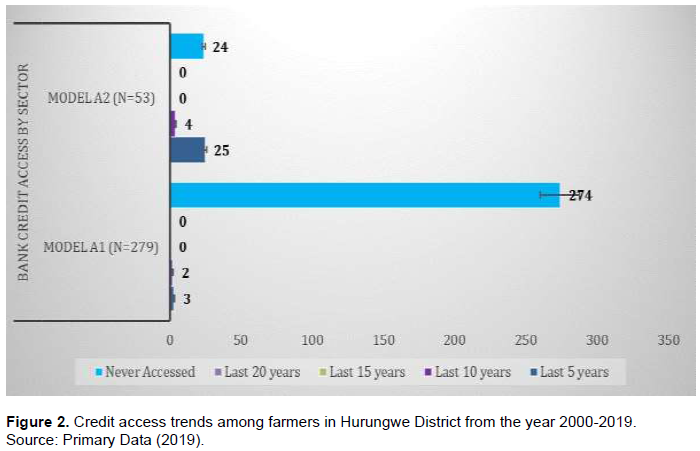

Figure 2 shows the credit access trends among farmers in Hurungwe District from 2000 to 2019. Since the implementation of the Fast Track Land Reform (FTLRP) in the year 2000 twenty years ago, approximately 98% of Model A1 farmers never accessed any bank credit compared to 45% in the Model A2 sector up to the current period (Figure 2). Within the last 15-20 years, there was also zero credit access among both Model A1 and Model A2 farmers. This supports Richardson (2005)’s assertion that lending to agriculture instantaneously diminished after the FTLRP as farmers could no longer use their land as collateral to secure borrowing. Credit access in both sectors began to grow within the past ten years, but was very marginal as only 0.7 and 1.4% Model A1 and Model A2 farmers accessed bank loans respectively. Whereas credit access grew by 50% in the Model A1 sector in the current period within the last five years, the Model A2 sector experienced a massive 525% growth in credit access. Credit access growth in both farming sectors may be attributed to government driven financing programs like Command Agriculture, which was aggressively implemented through local banks in the country within the past five years. Chisasa and Makina (2012)’s study in South Africa similarly established higher credit access by commercial farmers compared to smallholder farmers who lacked the eligible collateral required by banks, farming skills and technical knowhow.

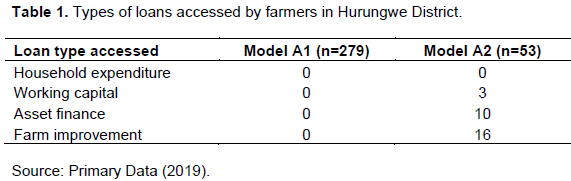

There was no borrowing for consumptive purposes among Hurungwe District farmers as both Model A1 and Model A2 farmers did not access household expenditure loans (Table 1). Whilst, Model A1 farmers never accessed working capital loans, approximately 6% of Model A2 farmers had access to them. Model A1 farmers also had zero access to asset financing and farm improvement loans, signalling the absence of physical capital formation activities in the sector. The failure by Model A1 farmers to access any bank loans may be ascribed to their lack of collateral assets in the absence of secure property rights as they mostly hold offer letters and permits as proof of land ownership, and also their lack of human capital skills to run vibrant agricultural enterprises compared to their predecessors, the former white commercial farmers (Masiyandima et al., 2011; Richardson, 2005).

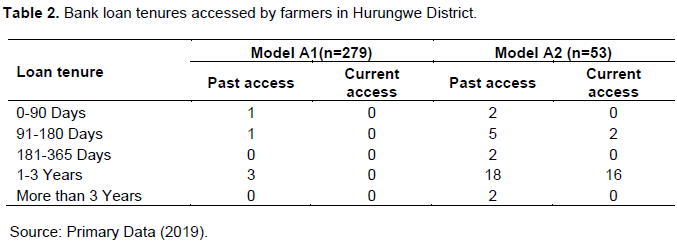

In the past period, Model A1 farmers had minimal access to short-term (0-90-days), short-to-medium (91-180-days) and medium-to-long-term (1-3 years) loans, whilst they had zero access to medium-term (181-365 days) and long-term (more than 3 years) loans. Access to short-term, short-to-medium term, medium-term and longer-term loans (>3 years) was marginally higher among Model A2 farmers in the same period. However, the Model A2 sector had the highest access to medium-to-long-term tenure loans of 1 to 3 years (Table 2). In the current period, Model A1 farmers had no access to any of the loans, whereas Model A2 farmers only had access to short-to-medium (91-180 days) and medium-to-long-term (1-3 years) loans. As highlighted above, higher access to longer tenure loans in the Model A2 sector may signal the presence of physical capital formation activities, which may have contributed to the farmers’ enhanced productivity, resilience to weather vagaries like recurring drought spells and capacity to repay loans. All of this may have also contributed to their better access to bank credit than their Model A1 counterparts (Awotide et al., 2015; Bisaliah, 2015; Lemma, 2015; Njoku and Odii, 1991).

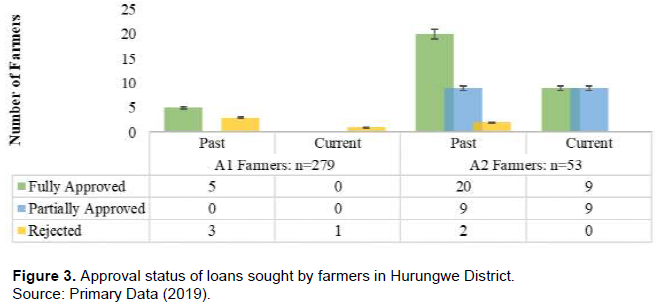

In the past period, Model A1 and Model A2 farmers’ loan applications were mostly fully approved (Figure 3). The number of Model A2 farmers whose loans were fully approved in the past quadruples that of Model A1 farmers whose loans were also fully approved. Whilst there were no partially approved loan applications in the Model A1 farming sector in the past, 17% of Model A2 farmers had their loan applications partially approved in the same period. However, there was a marginal difference between farmers whose loans were completely rejected in the past in the Model A1 and Model A2 farming sectors, which had 3 and 2 rejections respectively.

The current period had no fully or partially approved loans in the Model A1 farming sector as the only loan application made was rejected (Figure 3). However, rejected loan applications from the Model A1 farming sector decreased by a small margin from 3 rejections in the past to 1 rejection in the current period. Fully approved loans plummeted by 55% in the Model A2 farming sector, whilst partially approved loan applications remained constant in both time frames. The Model A2 farmers’ rejected loan applications also marginally decreased from 2 to none in the current period. Based on prior findings of this study, Model A1 farmers may have accounted for most of the rejected loan applications because they have not made any meaningful physical and human capital investments in their farms compared to their Model A2 counterparts, who have higher educational qualifications and are persistently seeking asset financing and farm improvement loans. Therefore, Model A1 farmers have not been able to enhance the agricultural production capacities of their farms through both farm and personal development, hence the higher rejection rate of their loan applications by lenders.

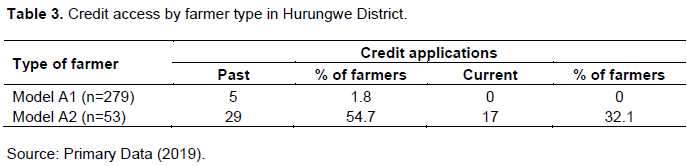

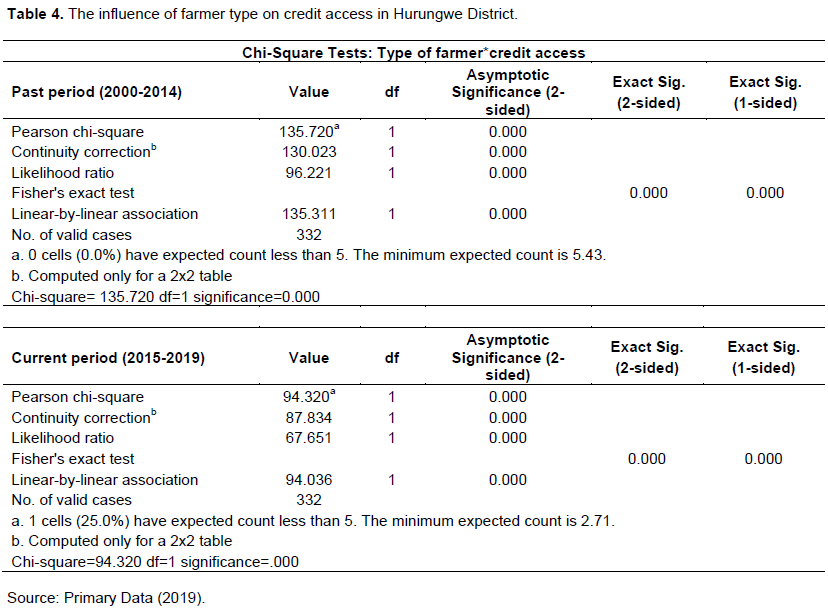

Only 1.8% of Model A1 farmers accessed bank credit in the past period compared to 54.7% in the Model A2 sector (Table 3). In the current period, none of the Model A1 farmers accessed bank credit, whereas 54.7% of Model A2 farmers accessed it. However, access to bank credit in the Model A2 farming sector plummeted by 41.4% in the current period from the past as only 17 Model A2 farmers accessed bank loans compared to 29 farmers who used to access loans in the past. The type of farmer had a significant (p<0.05) effect on bank credit access in Hurungwe District in both the past and current periods (Table 4). Credit access was significantly (p<0.05) higher among Model A2 farmers compared to Model A1 farmers. Poorer farmers like smallholder Model A1 farmers, who lack collateral assets and largely rely on rain-fed agriculture, are perceived as risky to lend to (Nyamutowa and Masunda, 2013; United Nations, 2014). Therefore, they are generally excluded from accessing bank credit. Bigger and highly collateralized farmers, who are mostly found in the Model A2 farming sector, are the most preferred borrowers by local banks (FACASI, 2015; Masiyandima et al., 2011; Vitoria et al., 2012).

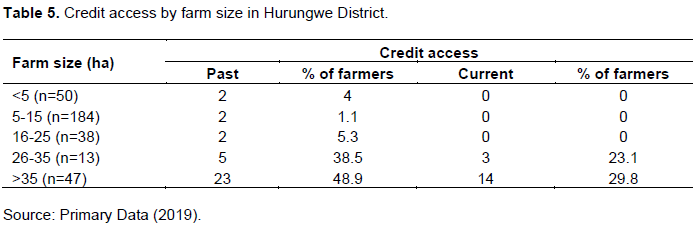

Credit access in Hurungwe District was higher among farmers with more than 35 ha of farmland in both the past (48.9%) and current (29.8%) time frames (Table 5). In the current period, there was zero credit access among farmers with 25 ha or less of farming land. However, access to bank credit began to improve among farmers with 26 ha or more in the current period. Credit access also declined by 100% among farmers with less than 5 to 25 hectares, and by 40 and 39% among farmers with 26-35 and more than 35 ha respectively.

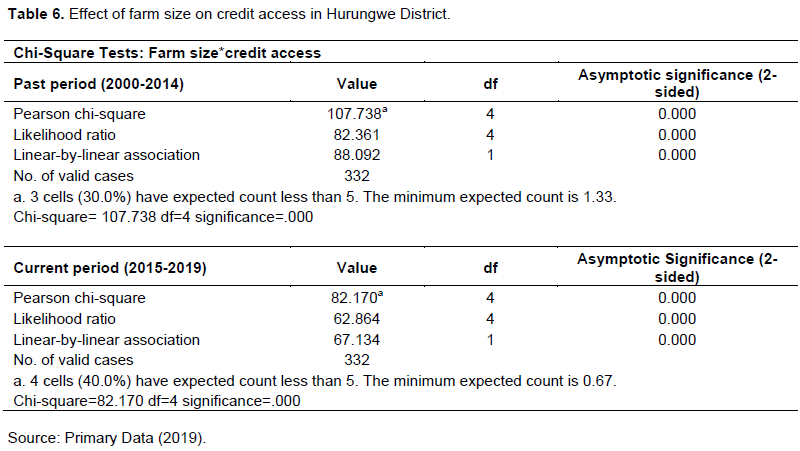

Farm size had a significant (p<0.05) influence on both current and past credit access in Hurungwe District (Table 6). Credit access was significantly (p<0.05) higher among farmers with more than 35 ha of farmland. Total landholdings of farmers in Pakistan also positively influenced their access to agricultural credit because land fulfilled the collateral role (Saqib et al., 2018). Mukasa et al. (2017) also confirmed that farm size significantly reduced the likelihood of farmers being credit quantity constrained in Ethiopia. This is because farmers with large landholdings were perceived as more capable of repaying their loans without defaulting because of their higher income generating potential. Mayowa (2015) equally established that farmers with larger land sizes had better access to bank credit in South Africa because they had higher productivity prospects, which therefore enhanced their ability to repay bank loans.

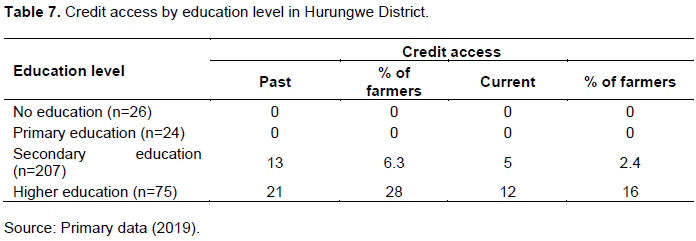

Uneducated farmers and those who attained primary level education had no access to bank credit in both the past and current periods in Hurungwe District (Table 7). A few (6.3%) farmers with secondary education had access to bank credit, whereas farmers with higher educational qualifications had the highest (28%) access to bank credit in the past period. However, credit access among farmers with secondary education tumbled to 2.4% in the current period. Under the same period, credit access among farmers with higher education also declined by approximately 43% from 21 farmers to only 12 farmers.

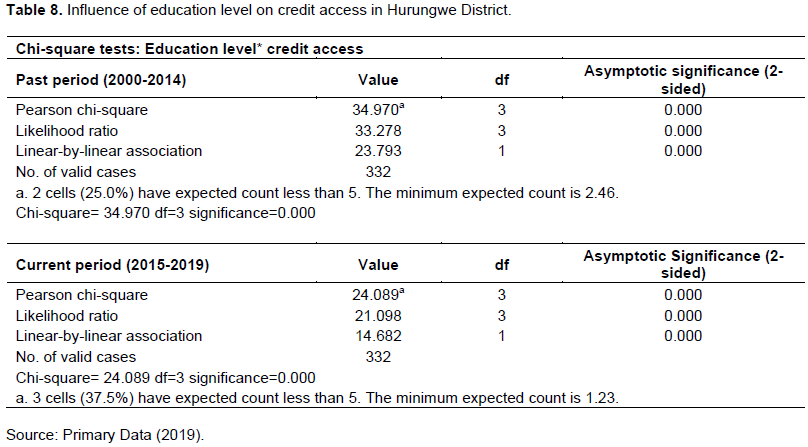

Education had a significant (p<0.05) effect on the farmers’ access to bank credit in Hurungwe District (Table 8). Credit access increased with education level as farmers with higher educational qualifications had significantly (p<0.05) higher access to bank credit. Sebatta et al. (2014) in Zambia and Muhongayire et al. (2013) in Rwanda argued that educated farmers’ better access to credit was ascribed to their ability to determine the loan amounts required for their agricultural projects through the drafting of business plans or budgets that are usually needed by loan granting institutions. Higher levels of education were also equated to better knowhow, farming skills and familiarity with lenders’ bureaucratic procedures, which all enhanced access to bank credit Sebatta et al. (2014). According to Ijioma and Osondu (2015), educated farmers are also considered to have better tendencies of loan management and adoption of new productivity enhancing technologies that improve their repayment potential, which is attractive to lenders.

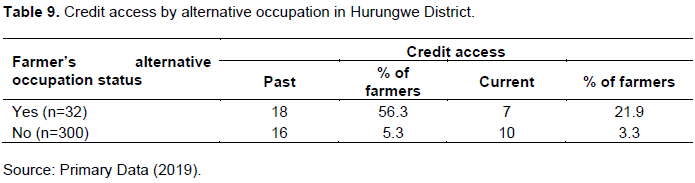

Farmers with alterative occupations off the farm in Hurungwe District had higher (56.3%) access to bank credit compared to full-time farmers (5.3%) who had no alternative employment in the past period (Table 9). Despite there being a decline in credit access among farmers in Hurungwe District in the current period, access was still higher among farmers with alternative occupations (21.9%) compared to full-time farmers (3.3%).

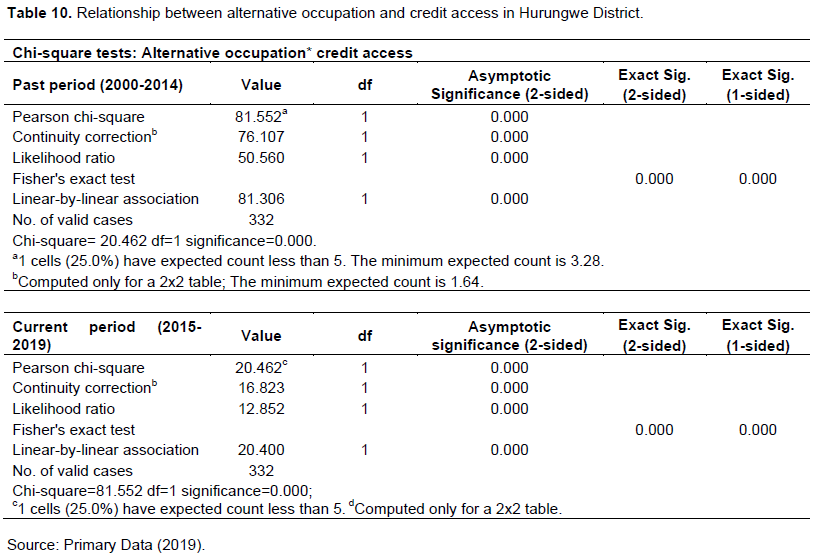

The farmers’ alternative occupation status had a significant (p<0.05) effect on their access to bank credit in Hurungwe District (Table 10). Farmers with alternative occupations had significantly (p<0.05) higher access to bank credit compared to full-time farmers who were not employed off the farm. Several studies in Zimbabwe confirm that local banks prefer advancing loans to salaried individuals who have less default risk as their salaries are received through the loan granting bank (FACASI, 2015; Makina, 2010). Duflo et al. (2008); Muhongayire et al. (2013) and Vuong Quoc (2012) also established that income from the farmers’ alternative employment helped to cushion banks from default risk if they failed to earn meaningful income from their agricultural projects to cover outstanding loan obligations.

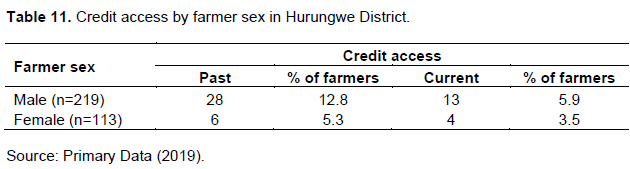

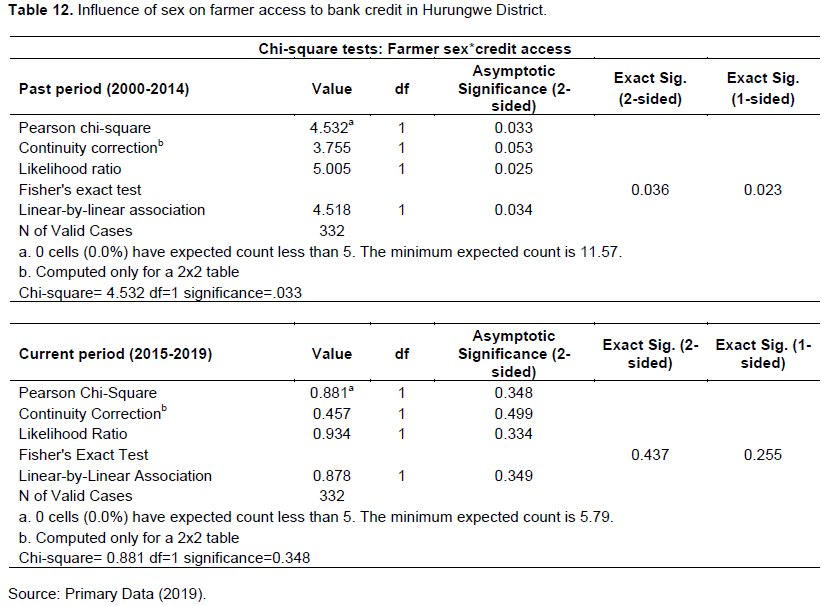

In the past period, male farmers had higher (12.8%) access to bank credit compared to female farmers (5.3%) (Table 11). This position persisted in the current period as more males (5.9%) accessed bank credit compared to women (3.5%). However, the decline in credit access was higher (54%) among males than among women (33%) from the past to the current period. Sex had a significant (p<0.05) influence on the Hurungwe District farmers’ access to bank credit in the past period (Table 12). Male farmers had significantly (p<0.05) higher access to bank credit compared to women. This raises questions over the efficacy of gender equity and women empowerment policies like the Gender Commission Act (Government of Zimbabwe (GoZ), 2015) that advocate for women’s enhanced access to production resources just like men in the country. Vuong Quoc (2012) similarly established that loan access by farmers was positively related to being a male borrower in Vietnam. Men’s better access to credit was ascribed to their high dominance in the agricultural field than women in most developing countries (Samuel et al., 2015). However, Abdul-Jalil (2015) on the contrary revealed that male farmers failed to access credit due to their higher default rates compared to women in Ghana. Thuku (2017)’s study in the Nyeri County of Kenya also established that banks preferred women to men when issuing credit because women honoured their credit obligations better than men. However, in the current period, sex does not have a significant (p>.05) effect on the Hurungwe farmers’ access to bank credit.

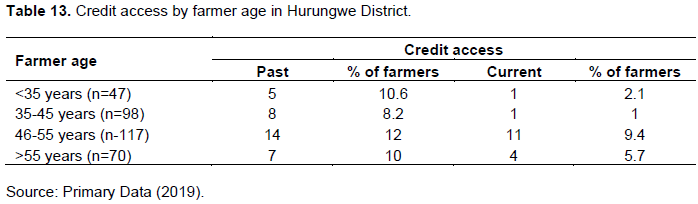

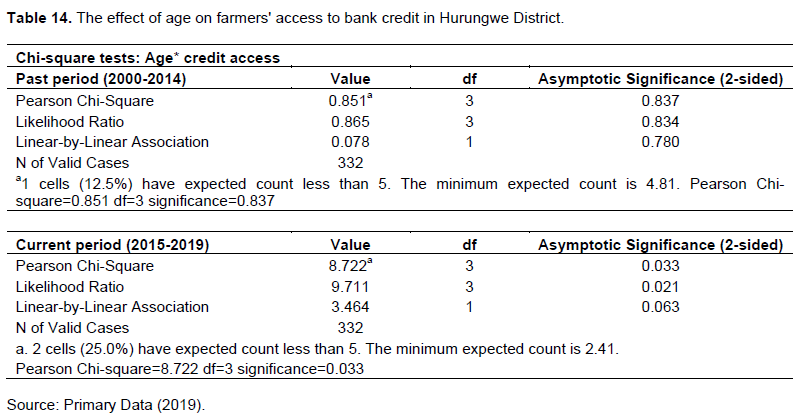

Frequency statistics show that credit access in Hurungwe District was higher among farmers within the 46-55 years age group in both the past (12%) and current (9.4%) periods (Table 13). Credit access also declined in general across all farmer age groups from the past to the current period. The 35-45 years age group recorded the largest reduction (88%) in credit access from the past to the current period. The Chi Square test showed no association (p>0.05) between farmers’ age and access to bank credit in Hurungwe District only in the past period. However, in the current period, age had a significant (p<0.05) effect on bank credit access. Hence, credit access was significantly (p<0.05) higher among farmers in the 46-55 years age group in the current period. Credit access increased with age, but decreased as the farmers became older at 55 years or more. Mukasa et al. (2017)’s study in Ethiopia equally established that as potential borrowers’ age increased, their risk of becoming credit constrained diminished, but however started to increase with older age. According to the study, older loan applicants’ probability of defaulting was perceived as higher than younger ones because of their higher risk of premature death and other recurring age-related health complications that could considerably undermine their ability to generate revenues and repay credit. Hence, their lower access to bank credit (Table 14).

CONCLUSIONS

The majority of farmers in Hurungwe District from both the Model A1 and Model A2 farming sectors never accessed bank credit since they were allocated farmland under the Fast Track Land Reform Program (FTLRP). Credit access among farmers was zero some 15-20 years ago, marginally improved some 10 years ago, and grew immensely within the last five years. However, access was higher among Model A2 farmers, who mostly accessed asset financing and farm improvement loans with medium-to-long-term tenures of 1-3 years. Smallholder Model A1 farmers accounted for all of the rejected agricultural loan applications in Hurungwe District, whilst Model A2 farmers’ loan applications were either fully or partially approved. Farmers with 35 ha or more of farmland, alternative employment and those with higher educational qualifications had better access to bank credit in both the past and current periods. Male farmers and those in the 46-55 years age range also had better access to bank credit. In the current period, credit access was significantly influenced by the type of farmer, farmers’ education, farm size, alternative occupation and age.

RECOMMENDATIONS

The government of Zimbabwe is encouraged to address the infrastructural and human capital development needs of the agricultural sector, especially in the Model A1 farming sector to enhance bank credit access. Special attention must be given to the development of irrigation infrastructure in the Model A1 farms to reduce the farmers’ dependency on rain-fed agriculture, which repels financial investors. Banks are also challenged to relax their demands for collateral in smallholder farming, but instead devise a locally adaptive model that prioritizes the farmers’ ability to produce and repay and collateral substitution financing models like group financing. Farmers must also invest in personal and farm development initiatives in their own capacity in order to enhance their access to the indispensable bank credit, instead of always waiting for government intervention. Investments in human capital development, especially succession planning must also be prioritized by local farmers to ensure sustainable access to bank credit across all generations. Future studies must attempt to quantify the supply of bank credit to local farmers in actual monetary terms in order to have a clearer picture of the prevailing financing gap in Zimbabwe.

CONFLICT OF INTERESTS

The authors have not declared any conflict of interests.

REFERENCES

|

Abdul-Jalil MA (2015). Determinants of access to credit and its impact on household food security in Karaga District of the norther region of Ghana. |

|

|

Alliance for Green Revolution in Africa (AGRA) (2017). Africa Agriculture Status Report: The business of smallholder agriculture in Sub-Saharan Africa. Alliance for a Green Revolution in Africa (AGRA), 5:180. |

|

|

Alliance for Green Revolution in Africa (AGRA) (2018). Impact: Towards Africa's Agricultural Transformation P. 48. |

|

|

Anyiro C, Oriaku B (2011). Access to and investment of formal micro credit by small holder farmers in Abia State, Nigeria: A case study of Absu Micro Finance Bank, Uturu. Journal of Agricultural Sciences 6(2):69. |

|

|

Awotide B, Abdoulaye T, Alene A, Manyong V (2015). Impact of access to credit on agricultural productivity: Evidence from Cassava Farmers in Nigeria. International Association of Agricultural Economists (IAAE) > 2015 Conference, August 9-14, 2015, Milan, Italy. |

|

|

Bisaliah S (2015). Capital Formation, agriculture growth, and poverty: Conceptual and empirical constructs. |

|

|

Chakoma I, Chummun BZ (2019). Forage seed value chain analysis in a sub-humid region of Zimbabwe: Perspectives of smallholder producers. African Journal of Range and Forage Science 36(2):95-104. |

|

|

Dale D (2009). The recovery and transformation of Zimbabwe's communal areas. Comprehensive Economic Recovery in Zimbabwe. |

|

|

Duflo E, Crepon B, Pariente W, Devoto F (2008). Poverty, access to credit and the determinants of participation in a new micro-credit program in rural areas of Morocco: Impact Analyses (October). |

|

|

Echanove J (2017). Food security, nutrition, climate change resilience, gender and the small-scale farmers. |

|

|

FACASI (2015). Financial products for farmers and service report. |

|

|

Finmark Trust (2014). Finscope Consumer Survey Zimbabwe. |

|

|

Government of Zimbabwe (GoZ) (2015). Zimbabwe Gender Commission Act (Chapter 10:31). Zimbabwe. |

|

|

Government of Zimbabwe (GoZ) (2017). Movable Property Security Interests Act (Chapter 14:15), Pub. L. No. 9/2017, 149 (2017). Zimbabwe. |

|

|

Ijiom JC, Osondu CK (2015). Agricultural credit sources and determinants of credit acquisition by farmers in Idemili Local Government Area of Anambra State. Journal of Agricultural Science and Technology 5:34-43. |

|

|

Inter-Ministerial Task-Force (IMT) Technical Committee (2016). Ministry of Lands and Rural Resettlement: Bankers Conference on the 99 Year Lease. |

|

|

Leaver R (2004). Measuring the supply response function. Agrekon 43(1):113-131. |

|

|

Lemma M (2015). Role of banks' deposit mobilization and credit financing on capital formation in Ethiopia. Addis Ababa. |

|

|

Madafu E (2015). Access to bank credit by smallholder farmers in Tanzania : Challenges, opportunities and prospects: A Case of Mvomero District. |

|

|

Makina D (2010). Historical perspective on Zimbabwe's economic performance: A tale of five lost decades. Journal of Developing Societies 26(1):99-123. |

|

|

Masiyandima N, Chigumira G, Bara A (2011). Sustainable financing options for agriculture in Zimbabwe (ZWPS 02/10). |

|

|

Mayowa BT (2015). Determinants of agricultural credit acquisition from the Land Bank of South Africa: A case study of smallholder farmers in peri-urban areas of Mopani District, Limpopo Province, South Africa. |

|

|

Mchugh, M. L. (2013). The Chi-square test of independence lessons in biostatistics. Biochemia Medica 23(2):143-149. |

|

|

Ministry of Agriculture (2013). Zimbabwe Agriculture Investment Plan (ZAIP): A comprehensive framework for the development of Zimbabwe's agriculture sector. |

|

|

Muchapondwa E (2009). Supply response of Zimbabwean agriculture: 1970-1999. Afjare 3(1):28-42. |

|

|

Muhongayire W, HitayezuP, Mbatia OL, Mukoya-Wangia SM (2013). Determinants of farmers' participation in formal credit markets in rural Rwanda. Journal of Agricultural Sciences 4(2):87-94. |

|

|

Mukasa AN, Simpasa AM, Salami AO (2017). Credit constraints and farm productivity: Micro-level evidence from smallholder farmers in Ethiopia. African Development Bank. |

|

|

Njoku J, Odii MAC (1991). Determinants of loan repayment under the Special Emergency Loan Scheme (SEALS) in Nigeria: A case study of Imo State. African Review of Money, Finance and Banking 1:39-52. |

|

|

Nyamutowa C, Masunda S (2013). An analysis of credit risk management practices in commercial banking institutions in Zimbabwe. International Journal of Economic Research 41(2229-6156):31-46. |

|

|

Reserve Bank of Zimbabwe (RBZ) (2016). Monetary Policy Statement. |

|

|

Reserve Bank of Zimbabwe (RBZ) (2006). Sustainable financing of agriculture. |

|

|

Reserve Bank of Zimbabwe (RBZ) (2013). Operationalising a collateral registry in Zimbabwe (2013). |

|

|

Reserve Bank of Zimbabwe (RBZ) (2019). Quarterly Economic Review. |

|

|

Richardson CJ (2005). The loss of property rights and the collapse of Zimbabwe. Cato Journal 25(3). |

|

|

Samuel E, Isah MA, Patil BL (2015). The Determinants of access to agricultural credit for small and marginal farmers in Dharwad district, Karnataka, India. Research Journal of Agriculture and Forestry Sciences 3(5):1-5. www.isca.me |

|

|

Saqib SE, Kuwornu JKM, Panezia S, Ali U (2018). Factors determining subsistence farmers' access to agricultural credit in flood-prone areas of Pakistan. Kasetsart Journal of Social Sciences 39(2):262-268. |

|

|

Sebatta C, Wamulume M, Mwansakilwa C (2014). Determinants of smallholder farmers' access to agricultural finance in Zambia. Journal of Agricultural Science 6:11. |

|

|

Swinkels R, Chipunza P (2018). Trends in poverty, urbanization and agricultural productivity in Zimbabwe: Preliminary findings. |

|

|

Thuku AG (2017). Factors affecting access to credit by small and medium enterprises in Kenya: A case study of agriculture sector in Nyeri county. |

|

|

United Nations (2014). Zimbabwe country analysis working document final draft. |

|

|

Vitoria B, Mudimu G, Moyo T (2012). Status of agricultural and rural finance in Zimbabwe. FinMark Trust (July). |

|

|

Vuong Quoc D (2012). Determinants of household access to formal credit in the rural areas of the Mekong Delta, Vietnam. Munich Personal RePEc Archive. |

|

Copyright © 2024 Author(s) retain the copyright of this article.

This article is published under the terms of the Creative Commons Attribution License 4.0