Full Length Research Paper

ABSTRACT

This study examined the performance of the Agricultural Credit Guarantee Scheme (ACGS) which is the major credit policy of the Federal Government of Nigeria. It was established in 1977 but started operation in 1978. Time series data from 1978-2014, extracted from the 2014 bulletin of the National Bureau Statistics were used for the study. Total volume and number of loans given were used to proxy the strength of the scheme, while the contribution of agriculture to GDP was used to proxy agricultural productivity. ARDL (Bounds) test approach to cointegration was employed to investigate both long and short run dynamics of ACGS and agricultural growth. The estimated results revealed that there is a long relationship among the total volume of loans, total number of loans and agricultural productivity. The long run elasticity showed that total volume of loan will not significantly influence productivity in the long run while the total numbers of loans have a significant long run relationship with the productivity. In the short run elasticity, total volume of loans was not significant with productivity in the current year while it was significant in the past four years. The total number of loan beneficiaries had a negative but significant relationship with productivity in the past 2 and 3 years while the relationship in the past year was also negative but insignificant. However, there was a positive and significant relationship between total number of loans issued and productivity in the current year. The speed of adjustment, ECT(-1) value of -0.1991 shows that the model will return to long run equilibrium at the speed of 19.91% from short run disequilibrium.

Key words: Agricultural credit, Agricultural Credit Guarantee Scheme (ACGS), ARDL, loan volume.

Abbreviation: ADP, Agricultural Development Programme; OFN, Operation Feed the Nation; RBP, Rural Banking Programme; GR, Green Revolution; NAIC, Nigerian Agricultural Insurance Corporation; CACS, Commercial Agricultural Credit Scheme; NIRSAL, Nigerian Incentive-Based Risk Sharing for Agricultural Lending; NAPEP, National Poverty Eradication programme; ACGS, Agricultural Credit Guarantee Scheme; BoA, Bank of Agriculture; TVL, total volume of loans; TNL, total number of loans.

INTRODUCTION

Credit has been a main focus of many research works in agricultural finance. To some, credit is “all in all” for a farmer to produce (productive input) while others hold different opinions. Whichever way it is looked at, credit is an important instrument in the development of agriculture. In fact, as emphasized by many researchers, the smallholder farmers caught in the quagmire of the vicious cycle of poverty require not only labour or land but an injection of adequate capital to extricate it from that cobweb. Funds for agricultural finance are met through macro and micro finance sources. The macro finance source pertains to financing agriculture through government capital allocation to agriculture and mobilizing resources for agricultural development using institutional credit agencies (Olowa and Olowa, 2011). Loans are usually acquired for productive reasons: particularly to enhance business operating capacity and generate more revenue for the business survival. The role of financial capital as a factor of production to facilitate economic growth and development, as well as the need to appropriately channel credit to rural households for economic development of the poor rural farmers cannot be over emphasized. Credit (capital) is viewed as more than just another resource such as labour, land, equipment and raw materials (Rhaji, 2008). Shepherd (2002) opined that credit determines access to all of the resources on which farmers depend. Consequently, provision of appropriate macroeconomic policies and enabling institutional finance framework for agricultural development are critical to facilitating agricultural development with a view to enhance the contribution of the sector in the generation of employment, income and foreign exchange (Olomola, 1997).

According to Alfred (2005), acquisition and utilization of credit for agricultural purposes promote productivity and consequently improve food security status of a community. Good access to credit would enable farmers venture into new areas as well as acquire improved technology for enhanced productivity. Credit is an important support service for increased agricultural productivity. Nwaru et al. (2006) observed that credit facilitates adoption of innovations, leading to increased farm productivity and income, encourages capital formation and improves marketing efficiency. In addition, it enables farmers to purchase required inputs, hire adequate labour and procure equipment and improved seed varieties for increased agricultural production. According to Nwankwo (2013), there has been serious argument in favour of on agricultural financing to reverse the persistent decline in the sector’s contribution to growth and development in many developing countries. Despite the steady decline of the financing of agriculture, it is still a leading economic sector, providing major employment, income and means of livelihood, especially for the poor and vulnerable rural households.

Over the years, the inability of the agricultural sector to expand vis-à-vis its inherent potentials and as well contribute significantly to economic growth of Nigerian was due to inadequate financing to facilitate farmers’ access to modern technologies/inputs and engaged adequate labour. Also, the problem of rapid agricultural development in Nigeria indicates that efforts directed at achieving expanded economic base of the rural farmers were frustrated by the scarcity of and restrictive access to loanable fund (CBN, 2010). In light of the above, the government of Nigeria has over the years developed policies and programs aimed at making financing available to the agricultural sector of the nation’s economy. These policies and programs among others include:

1. Agricultural Development Programme (ADP), 1975

2. Operation Feed the Nation (OFN) 1976

3. Rural Banking Programme (1977)

4. Green Revolution, 1980

5. Nigerian Agricultural Insurance Corporation (NAIC), 1987

6. National Poverty Eradication Programme (NAPEP), 1999

7. Agricultural Credit Guarantee Scheme (ACGS), 1977

8. Bank of Agriculture, (BoA) 2010.

There are two major sources of agricultural credit, that is, formal and informal sources. In the formal credit window, institutions provide intermediation between depositors and lenders, and charge farmers for relatively lower rates of loans interest that usually are government subsidized. In informal credit medium, loanable funds are lent by private individuals (John and Osondu, 2015). Among all of these programs and policies, aside NAIC which makes money available to farmers in form of indemnification in the event of an insured loss, only ACGS and BoA are still existing in extending credit facilities to farmers for production. While BoA is a product of a re-engineering of a former agricultural policy named Nigerian Agricultural Bank (NAB) which was incorporated in 1972 and was re-christened in 1978 to Nigerian Agricultural and Co-operative Bank Limited, (NACB) to reflect the inclusion of co-operative financing into its broader mandate and was later merged with People’s Bank of Nigeria (PBN) and the risk assets of the Family Economic Advancement Programme (FEAP) in 2001 for overlapping functions, in 2010, following the rebranding of the Bank to reflect its institutional transformation programme, the Bank adopted the new name “Bank of Agriculture”.

According to World Bank (2009), the Agricultural Credit Guarantee Scheme is one major credit policy of the Federal Government of Nigeria and for this reason, it is crucially important to study how this agricultural policy has influenced productivity in the agricultural sector of Nigeria. The Agricultural Credit Guarantee Scheme was set up in 1977 but started operation in 1978. The Federal Government holds 60% and Central Bank of Nigeria 40% of the shares of the shares. It was designed primarily to induce banks to increase and sustain lending to agriculture. To show how serious the government is, this policy is protected within the legislative framework (Decree No 20 of 977), that is, it is protected by law against being scrapped by any government due to any reason without going through the process of amendment which will put such government on the spot to explain why such development policy is to be scrapped. It is resident at the apex bank of Nigeria, Central Bank of Nigeria, CBN. Bank loans to farmers under this scheme are guaranteed 75% against default by the CBN.

Critical among the factors contributing to poor attainment of the development objectives of the agricultural sector are inadequate and/or non-availability of loanable fund with which agro-entrepreneurs can explore opportunities along the agricultural value chain (Awe, 2013; Zakaree, 2014).

In an attempt to break barrier of paucity of fund for agricultural production and processing, the Federal Government through the Central Bank of Nigeria established Commercial Agricultural Credit Scheme (CACS) in 2009 in collaboration with the Federal Ministry of Agriculture and Water Resources to facilitate adequate and timely funding of agricultural projects by commercial banks. A whooping sum of N200 billion seven-year bond was raised through the Debt Management Office and channeled through designated commercial banks for onward lending to actors in the agricultural sector (Olomola and Yaro, 2015)

Furthermore, Nigerian Incentive-Based Risk Sharing for Agricultural Lending (NIRSAL) came on board in 2011 to mitigate the challenges of underfunding in agro-business development, especially value chain enhancement in six major crops popularly grown across six agro-ecological belt of Nigeria. These crops are cassava, tomato, soya beans, cotton, maize and rice. NIRSAL’s mandate supports provision of adequate credit line to participants along value chain of the aforementioned crops in different scales/sizes of production.

These composite programmes, schemes, projects, policies and incentives, cum enormity of financial resources deployed towards scaling up agricultural production notwithstanding, the sector continues to record abysmal performance, as it cannot meet national food requirement, supply basic inputs (raw materials) for industrial production and produce cash across agro-climatic regions with comparative and competitive advantages to generate robust foreign exchange reserve (Awe, 2013; Olomola and Yaro, 2015; Anector et al., 2016). The bane of development in the sector as highlighted by these researchers has been underfunding, as target beneficiaries of various programmes/schemes/projects could not mobilize adequate and timely financial resources to operate at optimal production level.

The dearth of literature on the performance of this government credit policy is a source of concern. There have been studies on the effects or influence of agricultural credit on farmers’ productivity using primary data collected from the farmers based on their cost of production and revenue from their production process. However, primary data studies are location-specific and cannot explain the influence of credit on agricultural performance at a national level. This gap is the reason this study was executed so as to position the ACGS policy for better performance. After almost 40 years of operation of this credit scheme, about N84bn has been disbursed to about 931,863 farmers in the 36 states of the federation (ACGS, 2016). Sequel to the foregoing, it is imperative to assess the performance of the ACGS scheme in line with its programme development objectives.

Review of literature

Literature is replete with studies on the relationship between agricultural production and credit supply. However, point(s) of congruency on degree of association between credit supply and agricultural output have not been firmly established. In the study of Ammani (2012) where the relationship between agricultural production and formal credit supply in Nigeria was investigated, simple regression model was used. He established that formal credit positively and significantly influenced agricultural productivity. The study revealed the effects of formal credit on key agricultural sub-sectors- crops, livestock and fishery. But key set back of the study was the use of cross-sectional data which made the result location specific.

Ayegba and Ikani (2013) assessed how agricultural credit has improved rural farmers’ production/productivity in Nigeria, using cross-sectional data and found that agricultural credit supply had not significantly boosted production and productivity of farming households in the rural area. Similarly, Awe (2013) investigated the mobilization of domestic financial resources for agricultural productivity in Nigeria, using credit supply through Nigerian Bank for Commerce and Industries (NBCI) and commercial banks. His finding showed that there was a positive relationship between credit supply and agricultural productivity in Nigeria. Tasie and Offor (2013) analyzed the impacts of International Fund for Agricultural Development (IFAD) credit supply on rural farmers’ production and income in River State, Nigeria through the administration of questionnaires. They found that the IFAD credit programme contributed significantly to farm output and income.

Furthermore, Zakaree (2014) examined the impact of ACGSF on domestic food supply in Nigeria, using the ordinarily least square approach and asserted that the credit scheme had a positive and significant impact on domestic food supply. Recent study of Chisasa and Makina (2015) on bank credit and agricultural output in South Africa using cointegration and error correction model (ECM) revealed that credit supply has a positive and significant impact on agricultural output in the long run, while the ECM result showed that bank credit had negative impact on agricultural out in the short run. In the study of Anector et al. (2016) on Credit Supply and Agricultural Production in Nigeria: A Vector Autoregressive (VAR) Approach, they found that ACGSF had performed poorly in explaining agricultural sector performance while commercial loans to agricultural sector had a significant impact on agricultural production. The key area of departure of the present work from the previous studies is in the matching of volume of credit facilities of ACGF with number of beneficiaries and isolating its impacts on agricultural productivity at national level.

MATERIALS AND METHODS

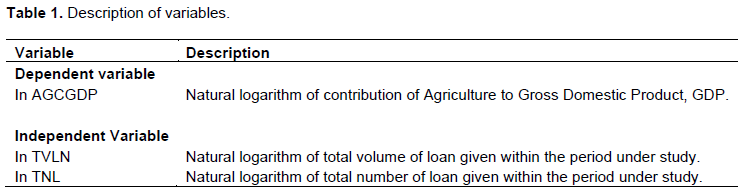

This study was carried out in Nigeria. Nigeria is a West African country blessed with green land in vast quantity and available labour to maximize the opportunities nature has afforded her. Time series data of 1978-2014 from the 2014 bulletin of the National Bureau of Statistics, NBS, were used for the purpose of this research. Agricultural productivity was proxy with the contribution of agriculture to Gross Domestic Product, while the total volume of loans given in naira (N) and total number of loans issued were proxy as performance of the credit policy within the period under review. The definition of variables is stated in Table 1.

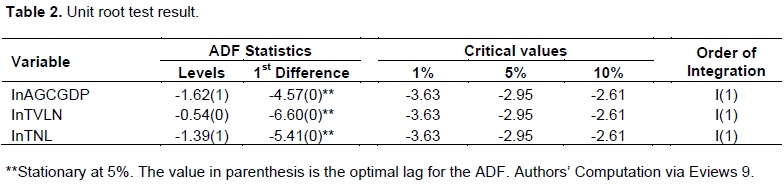

To ascertain the order of integration of the variables, the Augmented Dickey Fuller (Dickey and Fuller, 1979) unit root test was carried out using:

where, Yt refers to the variables (InAGCGDP, InTVLN and InTNL) to be tested. The sufficient lag lengths, i, are chosen using Schwarz Information Criterion (SIC). The sufficient lag lengths j of ∆Yt whitens the errors. The Ut is the error term. These tests were employed under the null hypothesis that there is unit root in the variable. If the t-statistics is higher than the critical value, the null hypothesis cannot be rejected; otherwise, the null hypothesis cannot be accepted. The estimate of the ADF unit root test is stated in Table 2.

From the above, the three variables are integrated of order I(1), that is, they are all stationary after first difference. The ARDL model which was developed by Pesaran and Shin (1999) and Pesaran et al. (2001) was employed to estimate the long and short run dynamics of ACGS credit policy and agricultural productivity. The ability of this model to estimate both long and short run relationship of variables in a single model informed its adoption for this study. The ARDL functional relationship is stated as:

To test for the long and short run dynamics in Equation 2 according to Pesaran et al (2001), Equation 2 was developed into the unrestricted error correction model. The general ARDL model is given as:

Where,  is the intercept,

is the intercept,  are the short-run coefficient,

are the short-run coefficient,  are the long-run coefficients and

are the long-run coefficients and  is the white noise.

is the white noise.

In order to ascertain the presence of cointegration among the variables, Bounds test was carried out. The Bounds testing which is based on F-statistics was used to test the hypothesis of no presence of cointegration against the alternative of presence of cointegration which is stated as:

that is, there is no conitegration among the variables;

that is, there is no conitegration among the variables;

that is, there is cointegration among the variables.

that is, there is cointegration among the variables.

Since a long run relationship was established among the variables under study, then, the parameters (elasticities) of the long-run relationship were estimated in the following equation:

To estimate the short run influence of total volume and number of loans given over the period under study, the following short run function was estimated:

RESULTS AND DISCUSSION

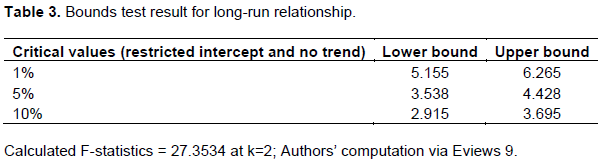

Due to the small sample size of this study, the Narayan (2005) critical values table was used to compare the F-statistics for the validation or otherwise of the hypothesis. Where, the F-statistic is below the lower bound I(0), the null hypothesis of no cointegration is accepted and if it is above the upper bound I(1), the null hypothesis of no cointegration cannot be accepted; therefore, the alternative is accepted. However, if the F-statistic falls in-between the lower and upper bound values, the result is deemed inconclusive. The number of lags used for his study based on the Akaike Information Criterion is 5. The calculated F-statistics from the bound test is presented in Table 3.

From the estimates above, the F-statistics is higher than the upper bound critical value. Thus, there is presence of a long run relationship among the variables, indicating a long run economic relationship among agricultural productivity, numbers and volumes of loans given to the farmers under the ACGS credit policy.

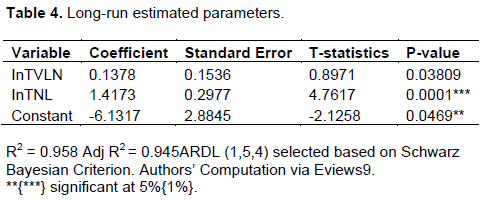

Estimate of long-run parameters

The result of the estimate of the influence of total volume of loan in the long run on agricultural productivity is presented in Table 4. As indicated in the table, the total volume of loan in the long run does not significantly influence agricultural productivity. This may be due to the fact that the volume of loan given yearly has been static with imperceptible marginal increase. For instance, the two notable periods where there were increases in the volume of loans given out were between 2010/2011 and 2013/2014. The volume of loan given in 2011 increased to about N10.19bn from about N7.7bn in 2010 and the highest increase was from about N9.42bn in 2013 to about N13bn in 2014. Whereas, the total number of beneficiaries increased from 50,849 in 2010 to 56,328 in 2011 and from 56,277 in 2013 to 72,322 in 2014. Though total number of loans given was highly significant and positive, the volume of loans made available for this increase in beneficiaries could not justifiably influence agricultural productivity. The positive and significant relationship between total number of loans and agricultural productivity may be associated with the fact that the farmers look elsewhere for alternative sources of credit to fund their farming activities. Be that as it may, ceteris paribus, the result further revealed that everyone involved in agriculture added to productivity irrespective of the magnitude. This may also account for the positive relationship of total number of loans with productivity because the higher the number of loans, the higher the number of beneficiaries. If the amount available to each beneficiary will now be adequate for production is another question which as well had being answered by the negative relationship of volume of loan with productivity. The negative coefficient of constant affirms the general saying that credit is the lubricant to the wheel of production without which other factors of production may not be employed. Thus, should there be no loan given to anyone, this negative relationship portends that productivity would be negative. Though agriculture could sometimes thrive even with no deliberate efforts from man, as some crops and fruits may just produce in their own time on their own, the kind of productivity being considered in this study is commercial agriculture. This thus confirmed the general understanding of credit as a lubricant without which rational and national agricultural productivity may not be achieved.

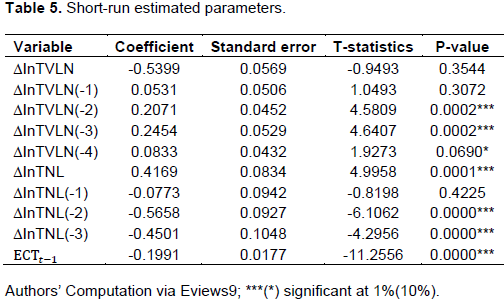

Short-run parameter estimate of dynamics of ACGS and agricultural productivity

Results of the elasticities of the short run dynamics of ACGS credit policy and agricultural productivity are shown in Table 5. From the table, total volume of loan disbursed to farmers was significant in the past 2 and 3 years at 1% and 4 years at 10%. While it positively and significantly influenced productivity within these periods, ACGS credit policy has a positive but insignificant relationship with productivity in the penultimate year and a negative, insignificant relationship in the current year. Apart from the current year where total number of loan is positive and significant with productivity, there is a negative relationship between total number of loan and productivity in the past 3 years. However, there is no significant relationship in ∆InTNL (-1). This negative relationship can be attributed to inadequacy of the volume of loan given to farmers under this scheme. The ECT (-1) is both negative and significant at 1%, suggesting backward movement of the model from a short run disequilibrium to a long run steady state at the speed of adjustment of 19.91%. This also confirms the presence of long run relationship among the variables.

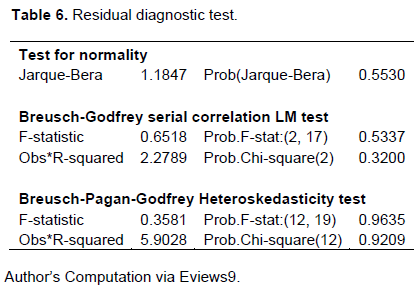

Residual diagnostic tests

The results of the diagnostic tests are presented in Table 6. Information contained in Table 6 indicates that the model is free from serial correlation, normally distributed and free from heteroskedasticity with p-values greater than 5% in all residual tests.

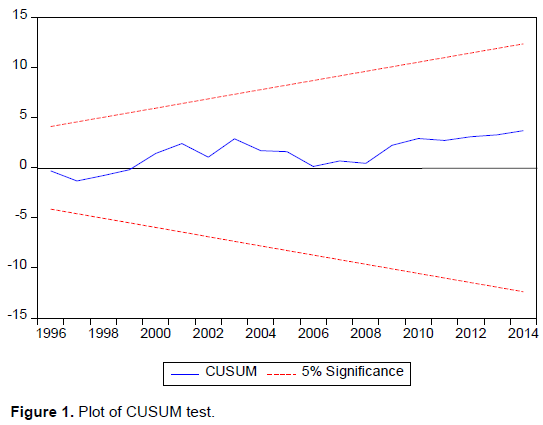

Stability tests

As proposed by Brown et al. (1975), the CUSUM and CUSUMSQ tests were used to examine the stability of the model. If the plot of the cumulative sum goes outside the area of 5% critical lines, the parameter estimates are found not to be stable. The test results are graphically presented in Figures 1 and 2. As shown in the figures, both CUSUM and CUSUMSQ are stable with the mean and variance lying in-between the two critical boundaries at 5% significance level. This implies that the residuals of model used in this study is stable, hence policy implications and recommendations emanating from this study are adoptable and adaptable to improve agricultural productivity in Nigeria through the ACGS credit scheme.

Summary of findings

This study examined the performance of the major credit policy of the Federal Government of Nigeria, that is, the Agricultural Credit Guarantee Scheme which was created in 1977, but started operation in 1978. The data used for this study spanned from 1978 to 2014. The focus is on how well this major credit policy of the government has been able to influence agricultural productivity. Credit is so crucial to agricultural production such that without it, it might be impossible for optimum production to take place. If production takes place without credit, it will be subsistent production. Hence, such a credit policy which began over 30 years should be examined so as to position it rightly to maximize its potentials.

Autoregressive Distributed Lag model was used to estimate the long and short run dynamics of the performance of the credit policy and agricultural productivity after the variables have been confirmed not to contain an I(2) variable, that is, variable stationary after second difference. From the ADF unit root test, the variables are all I(1). That is, all the variables became stationary after first difference. The ARDL (Bound) testing approach to conitegration was used to establish the presence of a long run relationship among the variables. From the F-statistic, there is a presence of long run relationship among the variables. The long run estimates show that the total volume of loans was not significantly related to productivity. This may be, because the total amount of loans made available for the beneficiaries was not adequate for commercial agriculture which is the kind of production system that can take Nigeria away from its present economic comatose, as well as make agriculture work again like it was before the oil boom. However, the total number of loan given is significant. This is because even though the amount given to each beneficiary may not have been enough for production, each beneficiary adds to the total productivity in agricultural sector, no matter how little the output could be. The short run estimates however differ on the total number of loans given within the period. Although, there is a significant relationship between the number of loans given under the credit policy and productivity in the current year, and past 2 and 3 years, it was not significant in the past 1 year. Except for the current level where total number of loan had a positive relationship with productivity, in the past three years, it shows a negative relationship. There is a negative and insignificant relationship between productivity and volume of loan in the current year while the relationship in the past year is though positive but insignificant. However, there is a significant and positive relationship in the past 2-3 years. This may be due to adequate monitoring of the loans which were given to beneficiaries in the past 2-3 years and favourable weather conditions, which enhanced higher production.

CONCLUSION

In sum, it cannot be emphatically said that ACGS credit policy has really achieved much in terms of using the instrument of credit to stimulate commercial agriculture and greater productivity, as well as ensure that farmers earn commensurate returns on their investment and adequate food availability for the citizens in good quantity, quality and prices. This reason for this is not far- fetched. With insignificant volume of loan, the numbers of farmers benefiting from the credit scheme have been increasing disproportionately to credit amount, such that the available facility cannot adequately go round among the beneficiaries for commercial production.

Policy implication

It is therefore important that government should focus on how to make use of the scheme to engineer commercial agriculture. Loan volume disbursed to farmers in year 2014 with a total volume of about N13bn for instance, would have achieved better result, if it was disbursed to 30,000 intended beneficiaries (farmers). Agriculture is a business and should be treated so. Disbursement of credit to farmers should be done without political inclination, such that only the target beneficiaries access the designed facility. Hence, every political tendency which lead to propaganda of creating thousands of jobs in agricultural sector devoid of quality production should be put aside and commercial focus and market driven agricultural production be built into the credit policy.

CONFLICT OF INTERESTS

The authors declare that there is no conflict of interest.

ACKNOWLEDGMENTS

The authors sincerely acknowledge the efforts of post graduate students who proofread and made useful corrections/contributions to enhance to quality of the paper.

REFERENCES

|

Alfred SDY (2005). Effect of Extension Information on Credit Utilization in a Democratic and Deregulated Economy by Farmers in Ondo State of Nigeria. J. Agric. Ext. 8:135-140. |

|

|

Ammani AA (2012). An investigation into the relationship between agricultural production and formal credit supply in Nigeria. International Journal of Applied Agricultural Sciences 2(1):46-52. |

|

|

Anector FO, Ogbechie C, Kelikume I, Ikpesu F (2016). On Credit Supply and Agricultural Production in Nigeria: A Vector Autoregressive (VAR). Journal of Economics and Sustainable Development 7(2):131-143. |

|

|

Awe AA (2013). Mobilization of Domestic Financial Resources for Agricultural Productivity in Nigeria. Australian Journal of Business and Management Research 2(12):01-07. |

|

|

Ayegba O, Ikani DI (2013). An impact assessment of agricultural credit on rural farmers in Nigeria. Research Journal of Finance and Accounting 4(18):80-89. |

|

|

Central Bank of Nigeria (CBN) (2010). Agricultural Credit Guarantee Scheme Fund of Nigeria (ACGSF): An impact assessment. Report of study conducted by Centre for resource Analysis and Management for the Governing Board of the ACGSF, Abuja. |

|

|

Chisasa J, Makina D (2015). Bank Credit and Agricultural Output in South Africa: Cointegration, Short Run Dynamics and Causality. Journal of Applied Business Research 31(2):489-500. |

|

|

Dickey DA, Fuller WA (1979). Distribution of the estimators for autoregressive time series with a unit root. Journal of the American Statistical Association 74:427-431. |

|

|

John CI, Osondu CK (2015). Agricultural Credit Sources and Determinants of Credit Acquisition by Farmers in Idemili Local Government Area of Anambra State. Journal of Agricultural Science and Technology 3(5):34-43. |

|

|

Narayan PK (2005). The Saving and Investment Nexus for China: Evidence from Cointegration tests. Applied Economics 37:17. |

|

|

Nwankwo O (2013). Agricultural financing in Nigeria: An empirical study of Nigerian agricultural co-operative and rural development bank (NACRDB). Journal of Management Research 5(2):28-44. |

|

|

Nwaru JC, Onyenweaku CE, Nwosu AC (2006). Relative Technical Efficiency of Credit and Non-credit User Crop Farmers. African Crop Science Journal 14 (3):241-51. |

|

|

Olomola AS, Yaro M (2015). Commercial Banks' Response to Government's Financial Stimulus for Improved Agricultural Financing in Nigeria. Abuja: International Food Policy Research Institute (IFPRI). National Strategy Support Programme II Working Paper 28. |

|

|

Olomola AS (1997). Agricultural finance. In A.O. Philips and S.Tunji Titilola (eds.) NISER, Ibadan pp. 51-62. |

|

|

Olowa OW, Olowa OA (2011). Issues, Problems and Policies in Agricultural Credit: A Review of Agricultural Credit in Nigeria. Bangladesh e-Journal of Sociology 8:2. |

|

|

Pesaran MH, Shin Y (1999). "An autoregressive distributed lag modelling approach to cointegration analysis", In: Strom, S., Holly, A., Diamond, P. (Eds.). Centennial Volume of Rangar Frisch, Cambridge University Press, Cambridge. |

|

|

Pesaran MH, Shin Y, Smith JR (2001). Bounds testing approaches to the analysis of level relationships. Journal of Applied Econometrics 16(3):289-326. |

|

|

Rhaji MA (2008). An Analysis of the Determinants of Agricultural Credit Approval/Loan size by commercial banks in south-western Nigeria. Nigeria Agricultural Development Studies 1(1):17-26. |

|

|

Shepherd WG (2002). Market Power and Economic Welfare. New York: Random House. |

|

|

Tasie CM, Offor US (2013). Effects of International Fund for Agricultural Development (IFAD) Credit Supply on Rural Farmers in Rivers State, Nigeria. Journal of Poverty, Investment and Development 1:65-70. |

|

|

World Bank (2009). Human Development Report. The World Bank, Washington, D.C. |

|

|

Zakaree SS (2014). Impact of Agricultural Credit Guarantee Scheme Fund (ACGSF) on Domestic Food Supply in Nigeria. British Journal of Economics, Management and Trade 4(8):1273-1284. |

|

Copyright © 2024 Author(s) retain the copyright of this article.

This article is published under the terms of the Creative Commons Attribution License 4.0