Full Length Research Paper

ABSTRACT

Agricultural finance is needed for sustainable agricultural production and improved farm income. The study analysed the accessibility of institutional credit among poultry farmers in Rivers State. Specifically, it described the socio-economic features of the farmers, identified the institutionally-based agricultural credit sources and credit amount requested by farmers. Data was analysed using descriptive statistics and logit regression. Results showed that majority of the farmers (71.85%) were male, averagely 40 years old. The average household size of the farmers was 4 persons. Majority (66.67%) indicated they had tertiary education. Most (60%) of the farmers had access to credit through institutional sources of which 40.74% of them got the credit through cooperatives. On the other hand, less number of farmers (40%) accessed credit from non-institutional sources. The variables: Sex, credit awareness, education, and credit demand were significant influencers of credit accessibility. Major constraints limiting farmers’ access to credit included lack of understanding of existing agricultural credit programs, loan transaction costs, granted credit amounts that were too little, and excessive interest rates. The study suggests that relevant agencies should engage in creating greater awareness and enlightenment on available agricultural credits and how to obtain the agricultural loans and more so, the farmers should be encouraged to participate in cooperative groups.

Key words: Agriculture, credit access, financial institutions, poultry, smallholder farmers.

INTRODUCTION

Poultry farming is the rearing of birds such as chickens, ducks, quails, turkeys, and geese with the goal of raising them for meat, eggs, and incidental goods such as faecal droppings and feathers in businesses as natural unprocessed materials (Stiles, 2017). Domestication of birds began many years back with the gathering of their eggs and their chicks or offspring from their natural habitat, which eventually led to their domestication as farm animals. Poultry production is carried out in small, medium, and large scale (Heise et al., 2015). According to Anang and Kabore (2021), poultry production contributes significantly to the socioeconomic development of people all over the world. In Nigeria, the livestock sector is a vibrant and profitable part of the overall economy, with yearly growth of 12.7% (FAO, 2020). The sector is estimated to have a global worth of almost $1.4 trillion, and with Nigeria's livestock sector been valued at $78 billion (FAO, 2020). The enterprise is a vital contributor to the expansion of the country's agricultural sector, contributing about 2.29% to the nation’s Gross Domestic Product in 2020 (NBS, 2020; FAO, 2020). Improved social standing, financial earnings, compost, insurance coverage and investment are some of the benefits of poultry farming and other livestock business to people's livelihoods (FAO, 2020). The poultry sector is important to Nigeria's economy because it provides a reliable source of animal protein in the form of meat and eggs (Nmadu et al., 2014). The poultry industry accounts for roughly 10 percent of total national meat output and is an important means to reduce protein shortfall in Nigeria, among other livestock (Elsadig and Badamasi, 2015). In Nigeria, the majority of the birds are housed in semi-intensive or intensive farms particularly in the southern region of the country (FAO, 2018).

However due to impact of changing weather pattern on agricultural production, the agricultural industry is said to rely on credit more than any other sector of the economy. Credit availability gives farmers the option to earn more income, embark on a large scale production and raise their quality of life (Mahmood et al., 2009). As a result, there is need to address the lack of credit in the agricultural industry, particularly among poultry farmers. There is perceivably a lack of accessible loans for the agricultural industry, particularly for poultry production. Poultry producers' access to credit facilities provides a substitute for personal savings and has a favourable impact on poultry output in a variety of ways. Farmers contribute and lend funds to each other as loans through formal organisations like cooperative societies and small poultry farmer's associations, but the amount they obtain is often too low for investment due to the large number of members seeking for loans.

Poultry farming in Nigeria is a complex and expensive venture. It is one of the agriculture - based sub-sectors in Nigeria that needs extra funding aside from the farmer's own savings. Sustainable poultry production demands the use of advanced technologies in the poultry industry's operations. A key factor influencing productivity, according to Atagher and Atagher (2014), is agricultural loans. Farmers are hampered by conditions such as lack of access to innovation, poor infrastructure, and insufficient funding, low market access, land and environmental deterioration, poor extension, and research services (Lawal, 2011). Also, studies have noted that poultry farmers in Rivers state encounter series of problems, such as low management capabilities, climate change impact on poultry, and increased demand for products such as eggs and meat (Adesope et al., 2014). The poultry sector is faced with several issues as financial intermediaries encounter continuing difficulties in delivering financial services to the agricultural industry. Small-scale farmers frequently experience credit constraints from both institutional and non-institutional sources.

Many studies (Adesope et al., 2014; Ekine et al., 2015) on poultry production in Rivers state are centered on the status of poultry production among rural households and assessment of broiler production. This study examines the accessibility of institutional credit among small-holder poultry farmers in Rivers State and describes the socio-economic characteristics of poultry farmers in Rivers State, Nigeria. Specifically, the study ascertains the institutional sources of agricultural credit and size of credit demanded by poultry farmers, identify the characteristics of farmers that are credit constrained, determine the factors influencing institutional credit accessibility by poultry farmers and identify the constraints faced by poultry farmers in accessing credit in the study area. Hopefully, the research will add to the country's body of knowledge on the subject matter, inform policy on addressing credit availability and sources, as well as improve the growth and survival of the poultry business in Nigeria. This research will add to the existing information of the subject matter so as to know the quantity of credit made available to the farmers with the goal of improving the current condition of credit accessibility and the ease with which poultry farmers may obtain financing.

Conceptual framework

Agricultural credit is simply another name for credit used in the agricultural sector. Agricultural credit enhances agriculture businesses significantly. Hence, Ijioma and Osondu (2015) noted that lack of agricultural credit can be a barrier to the growth of smallholder farmers in Nigeria and elsewhere. Agricultural credit or farm credit can be defined as credit extended to farms and livestock farmers to help with crop production, harvesting and improve livestock management process. It is a monetary concept that describes the credit given out for agricultural purposes, such as advances/overdrafts. Agricultural credit, otherwise known as farm credit, may be used for production to satisfy the farmers' current or capital expenses. Credits set out for production are typically for a limited time and can be used in the procurement of seedlings, fertilizers, compost, fodder, chemicals such as pesticides, insecticides, and fungicides (Abhiman et al., 2009). Farmers need credit to fund the servicing, refurbishments and cost of renting heavy duty machines and equipment as well as payment of salaries, taxes, rent, land levies and other ongoing consumable expenditures. Agricultural credit is a critical part of a long-term agricultural development. In rural areas, credit has been shown to be a significant tool for alleviating poverty and rural development. Farmers, in particular, require credit to enable them sustain production in the midst of risks associated with the business (Ololade and Olagunju, 2013). Agricultural credit is important to small-scale agriculture that enables smallholder farmers to expand production and improve productivity (Ololade and Olagunju, 2013).

In most developing countries, such as Nigeria, individuals (farmers) have access to three types of credit namely; formal or institutional sources (commercial banks, micro-finance banks), semi-formal (NGOs, cooperative societies), and informal or non-institutional sources (money lenders, contributions, family and friends) as observed by Badiru (2010). Formal financial institutions are authorized institutions and are licensed to provide financial services and operate under the standards and procedures of the Central Bank of Nigeria. Farmers perceivably preferred sourcing credit from informal sources, such as relatives, neighbours, and moneylenders, according to Mgbakor et al. (2014). Their preference is based on the ease with which they can access the sources, the limited formalities involved in obtaining credit, and the prompt and effective remittance of loans. Non-institutional and institutional sources are the two broad categories of sources of credit. Relatives, friends, merchants, and money lenders are examples of non-institutional sources. Such loans are typically given directly to the borrower by the lender and are common in areas where people are familiar with and trust one another. In the other words, the lender is familiar with the borrower farmer and can attest for his (lender's) honesty. The great ease that come with obtaining loans without institutional delays, the lender's lack of assertion on security or collateral from the borrower, and the flexibility built into repayment programs have made non-institutional sources extremely popular among smallholders, who make up roughly 70% of Nigeria's farming population.

Non-institutional sources are also differentiated from institutional sources by the absence of rigid terms and conditions that must be followed before credit is accessed. Institutional credit refers to credit provided to farmers by institutions with set laws to collect financial resources and distribute them to investors. Deposit Money Banks (DMBs), Insurance Companies, Nigerian Agricultural and Cooperative Bank (now known as BOA), Microfinance Banks, Government Agencies, International Development Agencies, and Co-operative Societies are some of the institutions in Nigeria that fall into the category of institutional credit source.

However, financial lending institutions in Nigeria are often not open to giving loans to farmers because of the high transaction cost associated with administering loans to the farmers who are mostly smallholders, scattered across space and with perceivably high rates of default. Hence, the Nigerian government over the years has come up with various initiatives to enhance credit availability to farmers. Some of these initiatives had included the Agricultural Credit Guarantee Scheme Fund (ACGSF) which was established by Decree No. 20 of 1977, the Agricultural Credit Support Scheme (ACSS), an initiative of the Federal Government and the Central Bank of Nigeria with the active support and participation of the bankers’ committee. The scheme was introduced in 1977; the Nigerian Agricultural Bank established in 1973 by the federal government to deal exclusively with Agricultural loans and the Commercial Agriculture Credit Scheme (CACS) formed in 2009 by the Central Bank of Nigeria (CBN) in partnership with the Federal Ministry of Agriculture and Water Resources (FMA and WR) to provide credit for the country's agricultural value chain (production, processing, storage and marketing. Despite the Federal government's investment in the agricultural sector through the above-mentioned schemes, the agricultural sector continues to perform below expectations. The poultry products available in the country are insufficient for domestic processing and do not generate enough foreign exchange through exports (Awe, 2013; Olomola and Yaro, 2015). Several studies have examined the credit schemes' flaws and identified some problems of which include delays in the disbursement of loans to farmers by the financial institutions associated with the schemes due to the distance from the bank and that of the farmer (Saheed, 2014).

Although credit is a tool to help with agricultural transformation and economic growth (Yusuf et al., 2015), several factors have been found to influence credit demand and supply. Henri-Ukoha et al. (2011) found that age, level of education, farming experience, and farm size were major influencers of credit accessibility. Similarly, Anang and Kabore (2021) observed in their study, the significant association between small-scale poultry farmer’s access to credit and socioeconomic characteristics such as education, household size, farm size and belongingness of farm-based organization. Dzadze et al. (2012) also observed that farmers' access to agricultural financing is influenced by their level of education, savings habits, and contact with extension agents. More so, Etonihu et al. (2013) observed that education, distance to credit sources, and forms of credit accessible were the most important factors determining farmers' access to agricultural credit in Nigeria. Furthermore, Ibrahim and Aliero (2012) examined factors influencing rural farmers' access to formal credit in Nigeria and observed that income, collateral, educational attainment, and marital status are significant positive influencers of farmers' access to formal credit. Awotide et al. (2015) in their study of impact of credit access noted that farmers who have access to credit have higher output than those who did not. However, the Nigerian poultry sector has numerous challenges, varying from the high cost of raw ingredients used in formulating chicken feed to the wiring of all equipment used in the poultry house (Ahmed and Mohammed, 2015; Heise et al., 2015). Inadequate local corn, soya, and chick production; a scarcity of active youths involved in the poultry industry; poorly funded and employed established or dormant extension agents to train and provide expert advice to youths actively involved in poultry production; and the scourge of diseases and pests are just but a few of the unique challenges the poultry industry encounters (Heise et al., 2015). Poor infrastructure, such as roads that impede the free entry of trucks carrying feed and other inputs to farms located in rural regions where most poultry farms are situated; poorly coordinated marketing channels; unsupported insurance policy by the government; delayed allocation of land, different levels of technology and low level of production are also some of the issues encountered by poultry farmers (Adeyonu, 2016).

MATERIALS AND METHODS

The research took place in Rivers State, Nigeria because of the significant number of smallholder poultry producers in the state, which was the reason for choice of the study area. Rivers State is bordered on the north by the states of Anambra, Imo, and Abia, on the east by the state of Akwa Ibom, and on the west by the states of Bayelsa and Delta.

Rivers state is known for its tropical environment characterized by many rivers, and wide swaths of agricultural land. Agriculture is the people's primary occupation in Rivers State. Agricultural activities carried out by majority of the citizens include fishing and farming (Ndubueze-Ogaraku and Ekine, 2014). Yam, cassava, maize, oil palm, banana, and plantain are the most commonly produced. Rivers State has a population of 5,199,716 people, with 2,673,026 men and 2,525,690 women, and covers an area of 21,850 square kilometres (National Population Commission, 2016). Rivers state is divided into 23 Local Government Areas and due to its level of closeness to the Atlantic Ocean; Rivers State has low temperatures ranging from 22 to 33ºC and high relative humidity (Fakayode et al., 2011). Respondents were chosen using a multi-stage selection approach that includes both purposive and simple random sampling techniques. According to information obtained from the Rivers State Ministry of Agriculture, Rivers State encompasses of three agricultural zones: zone 1, zone 11, and zone 111. In the first stage, a local government area was purposively selected from each zone based on the predominance of poultry farming, for a total of three local government areas. In the second stage, one community was randomly picked from each local government using the list of all communities as a sampling frame making a total of 3 communities and in the third stage, a total sample size of 150 respondents was proportionately sampled from across the three communities using the list of poultry farmers obtained from the farmers’ associations.

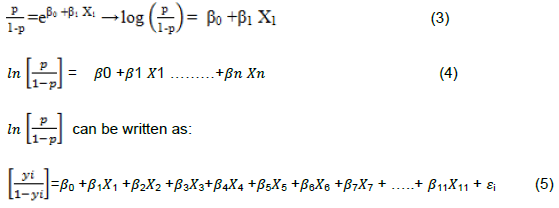

Both descriptive and inferential statistics was used to attain the objectives of the study. Statistical methods such as mean, percentage, and frequency tabulation were used in descriptive studies, whereas the inferential analysis employed the binary logistic model. The binary dependent variable in this study context is credit access, while the independent variables are factors that influence credit access. When the farmer has “access to credit,” the dependent variable Y = 1 is true, otherwise Y = 0 is true. The logit probability function is denoted by the notation:

P gives the Pr (y|x); x is the explanatory variable

The binary logit regression model in equation 3 below is derived from the two equations above.

Where Y is the probability a farmer has access to credit and 1-Y is the probability that a farmer does not have access to credit and i is the ith observation in the sample. β0 represents the intercept, β1- β13 represents the coefficient corresponding to X1.....X11, and εi is the error term.

Yi= β0 + β1X1 + ?1

Yi = Credit Access of ith poultry farmer (Yes = 1, otherwise 0); Xi= Factors that promote or prevent farmers access to credit; XI - X11 are defined as follows: X1 = Sex (Male =1, female = 0); X2 = Age (Years); X3 = Marital status (Dummy; Unmarried = 0, Married = 1);

X4 = Household size (in numbers); X5 = Education (in years); X6 = Farming experience (Years); X7 = Awareness of credit (Well informed on credit sources =1, otherwise 0); X8 = Farm size (Number of birds own); X9 = Monthly income level (in Naira); X10= Extension agent visit (Dummy; Yes = 1, No = 0); X11 = Amount of credit demanded in Naira; Ui = Error term.

The a priori expectations of the direction of change in the probability of access to institutional credit as a result of a unit change in any of the explanatory factors in the model are as follows. Variables such as gender, marital status, household size, farm size and amount of credit demanded may positively or negatively affect a farmer’s probability of accessing credit while variables such as education, years of experience and steady income are expected to have positive influence on the likelihood of a farmer having access to credit.

The Four-Point Likert Scale read from 1 (strongly disagree) to 4 (strongly agree) was used to rank the constraints faced by poultry farmers. The cut-off point was computed as:

Where a constraint with a value of 2.5 and above was considered a high impact constraint and any constraint below 2.5 is considered a low-impact constraint.

RESULTS AND DISCUSSION

Socioeconomic characteristics of poultry farmers in Rivers State

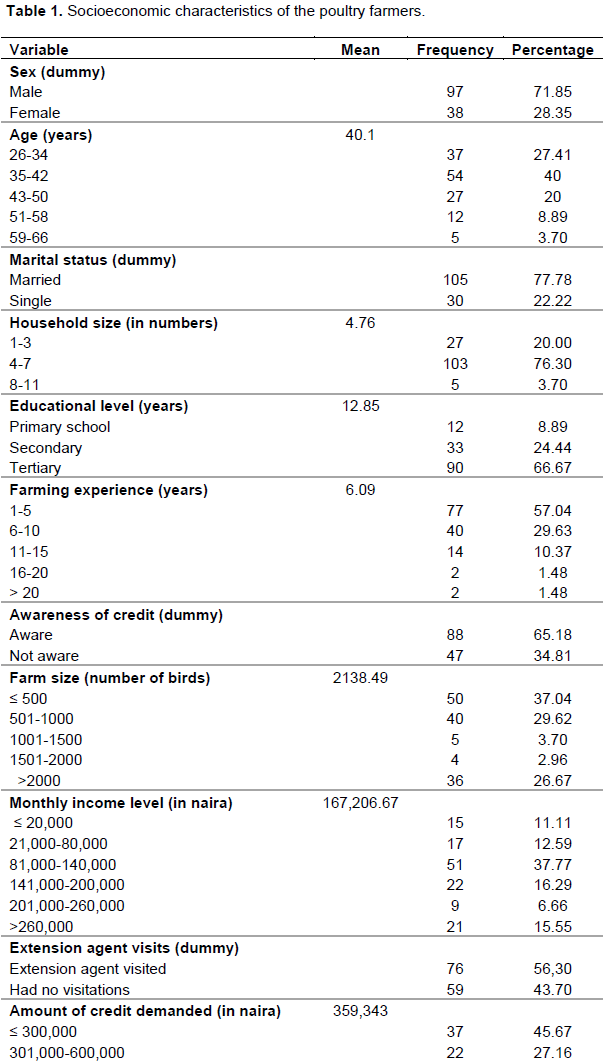

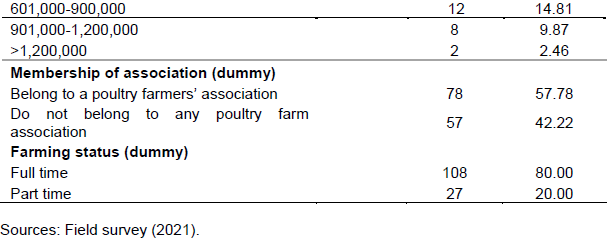

The result in Table 1 shows the socioeconomic characteristics distribution of the farmers. It is seen that there were more male farmers (71.85%) than females (28.15%). Farming is regarded as a tedious and arduous activity that needs a great deal of personal force. This arduous nature of farming could explain why there are more males in the poultry sector. The result is consistent with Olagunju (2010), who found that more men than women participate in small-scale farming. The poultry farmers’ average age was 40 years indicating they were in their prime working years. It is assumed that a farmer's productivity begins to diminish at a particular age (Afodu et al., 2017). Majority (77.78%) of the farmers was married and the rest (22.22%) were single. There is the notion that married persons with more responsibilities have a greater need to implement financial security methods in their households (Ikwuakam, 2013). The result also showed majority (76.30%) of them had a household size of 4-7 while 20% of them had a household size of 1-3 members and 3.70% of the farmers had a household of 8-11 persons. This indicated that the poultry farmers were responsible for one or more persons, who may also serve as a source of household labor. On the average, a farmer's household consisted of four people. This result is similar to the findings of Makinde et al. (2016). The study also showed that many (66.67%) of the respondents had tertiary education. 24.44% of them had secondary education, and 8.89% had primary education.

Education is a major socio-economic factor that significantly affects the productivity of farmers. Farmers with formal education are privileged to have early encounters with innovative ideas and enhanced technology that are aimed to improve agricultural output. This result is in contrast to Chukwuji et al. (2006) reporting of a low standard of education among broiler farmers in Delta state.

Furthermore, it was seen that 57.04% of the farmers had at least 5 years of farming experience. About 29.63% of the farmers had been in the business for between 6 and 10 years, 10.37% of the farmers had between 11 and 15 years of experience and 2.96% had more than 15 years of experience. The average number of years in the poultry industry was 6.09. It is expected that the couple of years a farmer has been involved in poultry farming could have an impact on how he or she arranges resources to reach a high level of productivity. The majority of poultry farmers (65.20%) were informed of institutional financing sources, whereas 34.81% claimed to be uninformed of such sources. Majority of the responders (37.04%) had fewer than 500 capacity poultry, indicating that the poultry producers were operating at a minimal level. 29.63% of the farmers had between 501 and 1000 birds, and 36% of the respondents had more than 2000 birds in their farm. The small-scale farms that most farmers run are responsible for their low revenue. According to Desli et al. (2003), small-scale producers are sometimes not productive, which can lead to low production and income for farmers. According to the percentage distribution of number of visits made by an extension worker, the majority of poultry farmers (56.30%) had contact with extension workers, while 43.70% of poultry farmers had no contact with extension workers. Extension workers who are innovators, consultants, and communicators play a significant role in assisting farmers in improving agricultural performance and improving their living conditions. Thus, it is very likely that the visits made by extension agents may have contributed positively to the farmers’ productivity.

In addition, many of the respondents (57.78%) are members of a farmers' association, while the rest (42.22%) are not. Membership in an association can further improve the access to credit available to poultry farmers, and also increase the amount of credit obtained from any institutional credit sources. Cooperative societies have been shown to have a significant impact on smallholder poultry farmers in terms of product prices, bargaining power, higher revenue, and the adoption of new technologies (Alufohai et al., 2018). Majority of the respondents (80%) said that poultry farming was their primary source of income, while 20% said they ran their farms part-time as a supplementary source of income.

Institutional sources of credit and size of credit demanded by poultry farmers

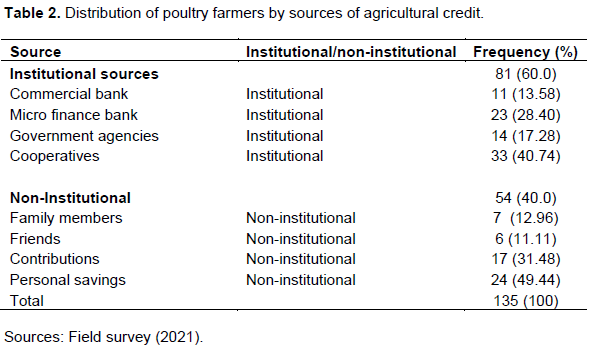

Majority (60%) of the farmers had access to credit through institutional sources, whereas a fewer number (40%) accessed credit facility from non-institutional sources, as shown in Table 2. This could be due to the high interest rates associated with non-institutional credit sources. The result agrees with a study conducted by Ahamefule et al. (2015).

Additionally, most of the poultry farmers who received financing from non-institutional sources used more of their personal savings (49.44%) to fund their businesses; 12.96 percent of respondents said they got credit from relatives, 31.48% got credit through contributions, and 11.11% obtained credit from friends. The result agrees with previous studies. For instance, Anang and Kabore (2021) observed in their study that small-scale poultry farmers’ access of credit facilities from informal sources was mainly from relatives and friends followed by through their savings and traders.

Farmers prefer credit from contributions for a variety of reasons, including the fact that there is no interest to pay and that no collateral or proof is necessary before receiving credit. Although many of the poultry farmers had access to institutional credit, 40.74% got credit from cooperatives, 28.40 percent received credit from microfinance banks, 13.58% obtained loans from a commercial bank, and 17.28% received loans from government agencies. Credit facilities are crucial because of its power to enhance other production elements. Commercial banks, microfinance banks, government organizations, and non-governmental entities accounted lesser proportion of farmers' income. Poor patronage of these institutional sources could be due to farmers' lack of awareness of the existence of formal agricultural lending institutions, lack of or restricted presence of banks in remote areas or delays in loan approval and distribution as well as insistence on collateral security as was noted in Okwoche et al. (2012).

Size/amount of credit demanded and obtained by farmers

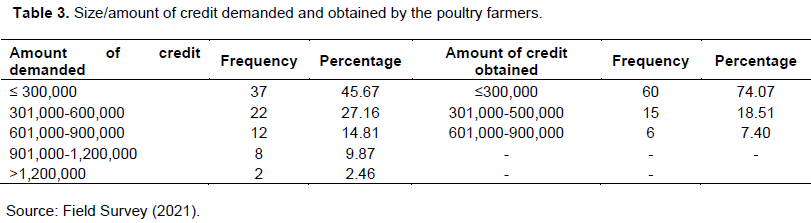

It can be seen in Table 3 that the average amount of loan demanded by the farmers was N359,343 although, 45.67% of the farmers wanted loan amount of less than or up to N300,000 Naira, while 27.16% demanded amounts between N301,000 and N600,000 Naira, 14.81% demanded for between N600,000 and N900, 000 Naira and 12.33% requested for more than N900,000. On the other hand, the result showed that majority (74.07%) of the respondents received less than or up to N300,000. No one received more than N900,000. Thus, it can be deduced that credit supply fell short of the expectations of the credit demanded by the poultry farmers, resulting in credit constraint for most poultry growers. The funds obtained as loans by the farmers may be inadequate to have a significant influence on their poultry farms. Hence, credit-constrained farmers are those whose requests aren't being satisfied to their satisfaction. Given that one's level of finance is a primary driver of requesting for loan, majority of small-scale farmers are unable to obtain adequate capital for investment. This conclusion is supported by (Aligbe and Effiong, 2012).

Factors influencing institutional credit accessibility by poultry farmers

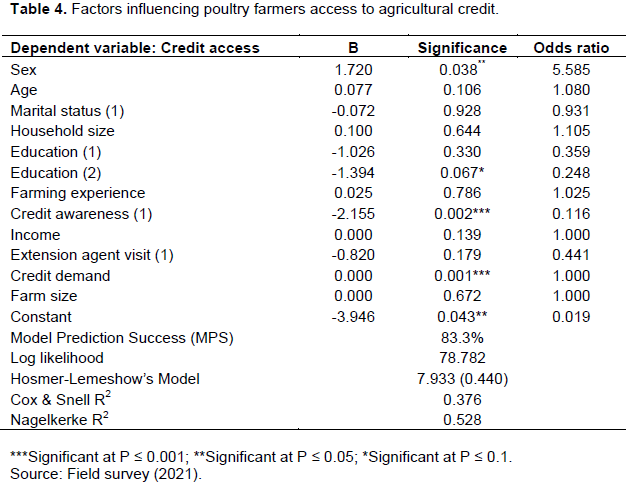

It can be seen in Table 4 that four parameters of the logistic regression are significant at various levels. Sex, credit awareness, education, and credit demand were the significant influencers. When the odds ratio is greater than one, it means that the possibility of an occurrence rises as the explanatory variable increases. Once the odds ratio is below or equivalent to one, it indicates that the likelihood of occurring decreases as the variable grows or that the variable is a neutral influencer (that is, the result is unaffected by a change in the regressor variable). Thus, it can be inferred that the likelihood of males (coded as one) having access to credit is 5.59 times higher than that of their female counterpart. As a result, it can be deduced that men have 5.59 times higher probability to have access to credit than their female colleagues. This can be attributed to cultural norms in most areas of Nigeria where men control more property and have greater financial resources than women (Olagunju and Babatunde, 2011). Farmers with only secondary education (0.25) are also less likely to have access to finance than those with tertiary education. This means that as a farmer’s degree of education rises, so does their access to financing. Quality education has the influence of facilitating loan access for families and improving the understanding of the knowledge on new farming methods and other relevant topics that can improve their well-being (Eneji et al., 2020). Thus, the poultry farmers having a high standard of education, suggests that their access to credit may be improved, which may probably result to the expansion of their poultry business in the future. Farmers who were acquainted with credit sources were likewise shown to be less likely to have credit access than those who were unaware of credit availability. This meant that knowing about credit availability does not translate to demanding or requesting credit. Farmers may refuse to seek for financing for a variety of reasons. Furthermore, the size of the credit demanded had little effect on the farmers' chances of receiving it. In addition, if the significance value is less than 0.05, the model is a poor fit, according to Hosmer and Lemeshow's goodness of fit test statistics. The test p-values (0.440) are, however, greater than 0.05, indicating that the model is adequately fitted. Also, the Cox Snell R2 and the Nagelkerke R2 are pseudo R2 values that describe the range of variance in dependent variable, and this ranges from 37.6% to 52.8% in this case.

Constraints faced by poultry farmers in accessing credit in the study area

Presented in Table 5 is the result of the 4-point Likert scale type assessment to identify major challenges experienced by poultry farmers in obtaining loans. It can be deduced that rising interest rates plays a crucial role in poultry farmers' ability to obtain loans. Since majority of respondents agreed or strongly agreed, high interest rates can be considered a major limiting issue in poultry farmers' access to finance. A large number of poultry farmers believe that credit applications are often difficult to understand, which contributes to farmers' inability to access credit. Unawareness of agricultural credit application is also a determining factor of a farmer’s access to credit, as agreed by most of the poultry farmers. In addition, a larger percentage of poultry producers believe that the cost of travelling to the location where credit is accessible can be a barrier to credit access. The result agrees with Anag and Kabore (2021) findings of challenges hindering small-scale poultry famer’s access to credit facilities and which included high interest rate on loans, high administrative and insurance costs on credit facilities from financial institutions, lack of collateral securities to secure loans and low educational background and lack of management skills among others.

CONCLUSION

Access to credit facilities is considered as one of the most important tools to improve agricultural productivity and reduce poverty particularly among smallholder farmers in Nigeria. The credit facilities can be made available to the farmers through formal or informal institutions. However, farmers are faced with challenges in accessing credit from these institutions. Thus, the study specifically set out to identify the socioeconomic characteristics of small-scale poultry farmers in Rivers State, determine the institutional sources of agricultural credit and the size of credit demanded by poultry farmers and determine the factors influencing institutional credit accessibility by poultry farmers. Based on the study findings, it can be concluded that male farmers dominated poultry farming in the study area, farmers were in their very active years, majority were married with an average household size of four people, and more so majority of the farmers had tertiary education. Also, farmers accessed credit from institutional sources more than they got from non-institutional sources and variables such as sex, credit awareness, education, and credit required demanded were significant influencers of institutional credit accessibility. Furthermore, lack of financial assets, unfavourable interest rates, lack of awareness of credit information, lack access to credit sources, and the transportation cost incurred to get to the area where credit is available are a few of the challenges faced by poultry farmers while trying to obtain credit. Consequently, the study suggests that relevant agencies should engage in creating greater awareness and enlightenment on availability of institutional agricultural credits for agricultural production and how to obtain the agricultural loans. Also, due to the sheer financial advantageous characteristics with agricultural cooperatives, more farmers should be encouraged to participate in cooperative groups to increase their likelihood of accessing institutional agricultural financial assistance and significant issues that hamper poultry producers' access to agricultural financing should be strategically addressed. For instance, institutional credit providers should grant farmers loan amount as have been requested.

CONFLICT OF INTERESTS

The authors have not declared any conflicts of interests.

REFERENCES

|

Abhiman D, Manjusha S, Joice J (2009). Impact of agricultural credit on agriculture production: An empirical analysis in India. Reserve Bank of India Occasional Papers 30(2):75-107. |

|

|

Adesope OM, Ekunwe PA, Familusi L (2014). Status of poultry production among rural households in Obio/Akpor Local Government Area of Rivers State, Nigeria. Journal of Agriculture, Socioeconomics and Sustainable Environment 2(1):70-78. |

|

|

Adeyonu AG (2016). Determinants of poultry farmer's willingness to participate in national agricultural insurance scheme in Oyo State, Nigeria. Applied Tropical Agriculture 21(3):55-62. |

|

|

Afodu OJ, Akinboye OE, Chioma G, Ndubuisi-Ogbonna LC, Shobo B, Ayo-Bello TA, Ajayi OA (2017). Profit analysis of fish farming enterprises in Ikenne Local Government Area of Ogun State, Nigeria. Asian Journal of Agricultural. Extension Sociology 18(1):1-8. |

|

|

Ahmed E, Mohammed BS (2015). Impediment observed in poultry farming in Kastsina State. Northern Nigeria. International Research Journal of Social Sciences 5(3):153-166. |

|

|

Ahamefule BA, Offor EI, Okafor UA (2015). Determinants of poultry farmers' decision to utilize credit: A case study of Abia State, Nigeria. Nigeria Agricultural Journal 48(1):159-166. |

|

|

Alufohai GO, Ekunwe PO, Mogbolu CE (2018). Effect of the activities of cooperative societies on cassava price in Orhionmwon Local Government Area, Edo State, Nigeria. Advances in Research Journal 15(3):1-11. |

|

|

Aligbe JO, Effiong JAL (2012). Dynamics of indebtedness among rural households in Edo State. Conference of Proceedings of the International Agriculture held at Anambra State University Igbariam Campus 6th -9th May 2012. |

|

|

Anang SA, Kabore AA (2021). Factors influencing credit access among small-scale Poultry farmers in the Sunyani West District of the Bono region, Ghana. Journal of Agricultural Extension and Rural Development 13(1):23-33. |

|

|

Atagher MM, Atagher DM (2014). Assessment of the availability of rural infrastructure, agricultural credit and cooking fuel among project and non-project women farmers in Benue State, Nigeria. Journal of Agriculture and Veterinary Science 7(11):17-22. |

|

|

Awe AA (2013). Mobilization of domestic financial resources for agricultural productivity in Nigeria. Australian Journal of Business and Management Research 2(12):1-7. |

|

|

Awotide BA, Abdoulaye T, Alene A, Manyong VM (2015). Impact of access to credit on agricultural productivity: Evidence from smallholder cassava farmers in Nigeria. International Conference of Agricultural Economists (ICAE), Milan/Italy. |

|

|

Badiru IO (2010). Review of small farmer access to agricultural credit in Nigeria. Nigeria Strategy Support Program. Policy Note 25. International Food Policy Research Institute (IFPRI). |

|

|

Chukwuji CO, Inioni OE, Ogisi WJ, Oyaide WJ (2006). A quantitative determination of allocative e?ciency in broiler production in Delta State, Nigeria. Agriculture Conspectus Scienti?cus 71(1):21-26. |

|

|

Desli E, Ray SC, Kumbhakar SC (2003). A dynamic stochastic frontier production model with time-varying efficiency. Applied Economics Letters 10(10): 623-626. |

|

|

Dzadze P, Aidoo R, Nurah G (2012). Factors determining access to formal credit in Ghana: A case study of smallholder farmers in the Abura-Asebu Kwamankese district of central region of Ghana. Journal of Development and Agricultural Economics 4(14):416-423. |

|

|

Ekine DI, Ndubueze-Ogaraku ME, Opute EN (2015). Assessment of broiler production in Obio- Akpor Local Government Area, Rivers State, Nigeria. Nigeria Journal of Agriculture, Food and Environment 5(1): 81-91. |

|

|

Elsadig MA, Badamasi SN (2015). Economic impact of poultry Production in Katsina State, Nigeria. International Research Journal of Social Sciences 5(3):153-166. |

|

|

Eneji CVO, Onnoghen NU, Acha JO, Diwa JB (2020). Climate change awareness, environmental education and gender role burdens among rural farmers of Northern Cross River State, Nigeria. International Journal of Climate Change Strategies and Management 13(4/5):397-415. |

|

|

Etonihu KI, Rahman SA, Usman S (2013). Determinants of access to agricultural credit among crop farmers in a farming community of Nasarawa State. Journal of Development and Agricultural Economics 5(5):192-196. |

|

|

FAO (2020). Nigeria at a glance. Food and Agriculture Organization of the United Nations. |

|

|

FAO (2018). Africa Sustainable Livestock 2050: Livestock and livelihoods spotlight. Nigeria Cattle and Poultry Sectors. |

|

|

Fakayode BC, Rahji MAY, Ayinde O, Nnom GO (2011). An economic assessment of plantain production in Rivers State, Nigeria. International Journal of Agricultural Economics and Rural Development 4(2):28-36. |

|

|

Heise H, Crisan A, Theuvsen L (2015). The poultry market in Nigeria: Market structures and potential for investment in the market. International food and Agribusiness Management Review 18:197-222 |

|

|

Henri-Ukoha A, Orebiyi JS, Obasi PC, Oguoma NN, Ohajianya DO, Ibekwe UC, Ukoha II (2011). Determinants of loan acquisition from the financial institutions by small-scale farmers in Ohafia Agricultural Zone of Abia State, South East Nigeria. Journal of Development and Agricultural Economics 3(2):69-74. |

|

|

Ibrahim SS, Aliero HM (2012). An analysis of farmers' access to formal credit in the rural areas of Nigeria. African Journal of Agricultural Research 7(47):6249-6253. |

|

|

Ijioma JC, Osondu CK (2015). Agricultural credit sources and of credit acquisition by farmers in Idemili Local Government Area of Anambra State. Journal of Agricultural Science and Technology 5(1):34-43. |

|

|

Ikwuakam OT (2013). Determination of socio-economics status of cassava processing entrepreneurs in South Eastern, Nigeria. Journal of Agriculture and Veterinary Sciences 5(2):140-150. |

|

|

Lawal WA (2011). An analysis of government spending on agricultural sector and its contribution to GDP in Nigeria. International Journal of Business and Social Science 2(20):244-250. |

|

|

Mahmood AN, Khalid M, Kouser VS (2009). The role of agricultural credit in the growth of livestock sector: A case study of Faisalabad. Pakistan Veterinary Journal 29(2):81-84. |

|

|

Mgbakor MN, Uzendu PO, Ndubisi DO (2014). Sources of agricultural credit to small scale farmers in Ezeagu Local Government Area of Enugu State, Nigeria. IOSR Journal of Agriculture and Veterinary Science 7(8):1-8. |

|

|

National Bureau of Statistics, NBS (2020). Nigeria general household survey 2015/2016. |

|

|

National Population Commission (2016). The Nigeria Population Commission 2006 Census Figure. Federal Government of Nigeria. Abuja. |

|

|

Ndubueze-Ogaraku ME, Ekine DI (2014). Profitability of cassava production in the floodplain areas of Rivers State, Nigeria. Nigeria Journal of Agriculture, Food and Environment 10(2):79-86. |

|

|

Nmadu JN, Ogidan IO, Omelehin RA (2014). Profitability and resource use efficiency of poultry egg production in Abuja, Nigeria. Kasetsart Journal of Social Science 35(1):134-146. |

|

|

Okwoche VA, Asogwa BC, Obinne PC (2012). Evaluation of agricultural credit utilization by cooperative farmers in Benue State of Nigeria. European Journal of Economics, Finance and Administrative Sciences 47:123-133. |

|

|

Olagunju FI, Babatunde RO (2011). Impact of credit on poultry productivity in South Western, Nigeria. ARPN Journal of Agriculture. Biological Science 6:58-64. |

|

|

Ololade RA, Olagunju FI (2013). Determinants of access to credit by small holder farmer's in Oyo State, Nigeria. Global Journal of Science Frontier Research Agriculture and Veterinary Sciences 13(2):16-22. |

|

|

Olomola AS, Yaro M (2015). Commercial banks' response to government's financial stimulus for improved agricultural financing in Nigeria. NSSP Working Paper 28. Washington, D.C.: International Food Policy Research Institute (IFPRI). View |

|

|

Saheed ZS (2014). Impact of Agricultural Credit Guarantee Scheme Fund (ACGS) on domestic food supply. British Journal of Economics Management and Trade 4(8):1273 1284. |

|

|

Stiles W (2017). Poultry manure management. |

|

|

Yusuf HO, Ishaiah P, Yusuf O, Yusuf HA, Shuaibu H (2015). The role of informal credit on agriculture: An assessment of small scale maize farmers' utilization of credit in Jemaa Local Government Area of Kaduna State, Nigeria. American Journal of Experimental Agriculture 5:36-43. |

|

Copyright © 2024 Author(s) retain the copyright of this article.

This article is published under the terms of the Creative Commons Attribution License 4.0